The current slide in the prices may be attributed to the government considering permanent WFH for IT SEZs by this month-end. We need to wait and watch what kind of labour and tax changes this will bring in for both IT companies and employees. Whether it will be permanent WFH or Hybrid or Return to Office, it all becomes subjective depending on who you are and what you do. I had tried to articulate this back in April last year on Nesco thread over here. What I could add here is that even if we conclude with certainty that the percentage of people working from offices will fall, it will be compensated to an extent by the increase of overall IT industry headcount which has been growing throughout 2020 and into 2021 and beyond. This is true for both Global In-house centers and IT services companies.

Hi I am new to REITs and started evaluating them a few days back. While I understand the absolute NDCF yields are quite high, the proportion of this coming from pure dividends (which has a lower tax rate) is quite low and that coming from interest payment and SPV level debt ammortization is higher (which I understand are taxed based on your tax slab?). Can somebody explain what the difference between dividend, interest and SPV level debt is and how are they calculated? Secondly how is this mix likely to change going forward?

I would suggest you read Q3 Conference Call Transcript which are available on enclosed link

https://www.embassyofficeparks.com/investors/events/

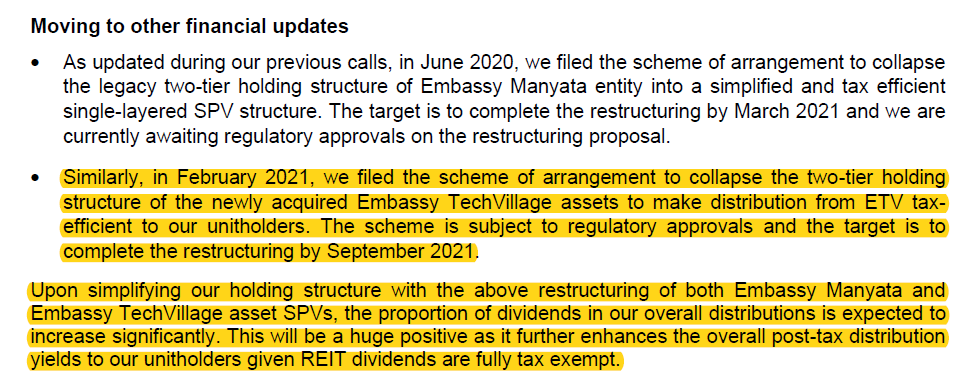

Key extract about change in structure from file the is as under:

Also refer to 26 March 2021 release by REIT providing update on approval of scheme.

From very simple understanding, I expect nearly 60-70% of total distribution would on approval of scheme would be by way of Dividend. Please note that this is my understanding it may be wrong. Please do your own due diligence before making any investment decision. Balance 30-40% shall be in form of capital return (which is not taxed currently but reduced from acquisition cost when units are sold) and Interest (which is taxable).

Thanks for the reply and for pointing me to the concall. Helpful to see how these are going to change going forward.

I had a more basic question; What exactly do the terms Ammortization of SPV Level debt and Interest payment mean? From the operating cash flows of the various rent generating assets, how is it determined what is the interest, dividend and SPV debt ammortization payments to unitholders? Not looking for the actual numbers but more a qualitative understanding of what the terms mean and what drives them. Have gone through all the threads on REITs here as well as the presentations of the various REITs and still not able to answer this basic question.

Mostly, the REIT raise debt and issue unit. It infuse in various SPV (owning real estate), fund which have structure of debt and equity. In addition to loan from REIT, the SPV also can have third party loan (loan from bank).

So while calculating each REIT SPV NCDF, loan interest and principal redemption on third party is deducted beside operational/maintenance expenditure. Such SPV NCDFs are aggregated at REIT level. Now inflow in REIT consolidated is in form of interest payment from REIT SPV, Debt repayment from SPV and Dividend (depending on structure of capital structure). That become source for consolidated REIT NCDF.

From this Consolidated NCDF sources, expenditure like REIT Management fees, trust related expenditure, valuation expenditure and other operational cost are deducted. Further, in case there is any interest payment and debt repayment are payable, same is also deducted to arrive at NCDF at consolidated REIT level.

Whatever is now left (which can be distributed), is REIT NCDF at consolidated level. When REIT manager distribute cashflow, they look at receipt from SPV, which is in form of interest, capital return (debt repayment) and dividend. In same proportion total distribution would be dividend as dividend, interest and capital return by REIT to unit holders. REIT management provide details about form of distribution every quarter (i.e. how much is interest/dividend/capital return).

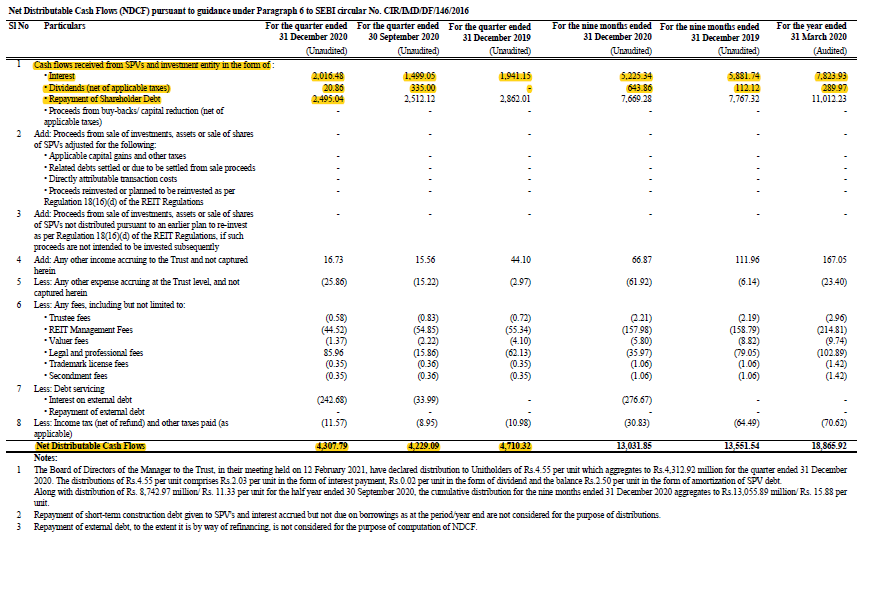

Find enclosed consolidated NCDF calculation for Embassy in December 2020 quarter from results:

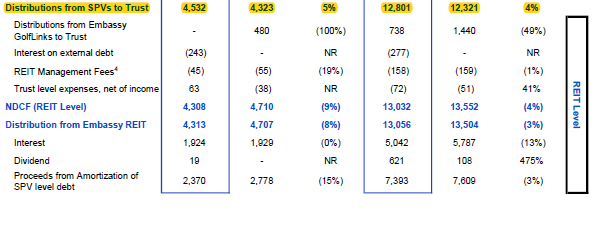

Now in Data sheet for December Q3 FY21, on Page 17 pdf, we get detail about distribution of NCDF to investor extract of which is as under:

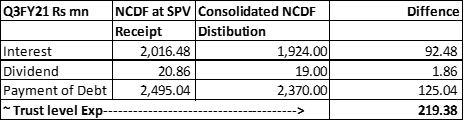

So in Q3FY21, inflow from SPV NCDF to REIT Trust and distribution from REIT to investor when we compare are as under:

Now add Interest on external debt (Rs 243 mn), REIT management fees ( Rs 45 mn) and Net income (mainly interest on funds investment before distributing to investors being income it would be considered as negative , Rs -63 mn). These three would add to Rs 225 mn which would ~219.38 mn shown in above table.

This is what I understand from various data. It may be wrong. Also, every quarter, distribution from SPV to REIT and REIT to investor may vary due to change in business and financial structure. Hope this answer the question.

For anyone worried about work from home.

This is the latest article with the latest quotes and findings from the real estate industry including CBRE that I came across(published earlier this month).

Note that they’ll obviously be bullish so I’d take the 1.6 to 1.7 times increase in need for commercial space comment with a pinch of salt but the arguments they put forward regards how companies won’t save that much in the long run, how India is different Vs the west etc and the arguments put forward regards how TCS spoke about work from home but renewed their leases out of fear of having to pay a higher rental later if they leave now etc plus the rental collections and demand for space in Bangalore etc make a lot of sense.

Considering the USA and Canada are in a better position regards vaccines Vs india I had a brief look at the office REITs there and despite Google and Microsoft talking about WFH I’ve found that they are infact renewing rentals and even expanding with more offices! Most of the office REITs have had a good few months since the pandemic situation has improved too. Couple this with the Brookfield post IPO Call and presentation update regards demand and collections and most fears regards lower office demand and rentals for Embassy should be allayed at CMP(the announcement that 18 years+ can get vaccinated and the private sector can help may be the shot in the arm that’s needed)

Disc: invested in Embassy. not a sebi advisor.

Hello,

Thank you so much for the insightful post and ensuing discussions! They’ve been really interesting.

There are a few things troubling me and I haven’t been able to think through them clearly. Would appreciate it if someone could help clarify my thoughts.

- How are you all viewing future acquisitions?

Background: Despite borrowing at 6.4% and having a roughly 66%-33% Equity-Debt Split and having an asset with 97.8% occupancy and a cap rate/yield of 7.5%, they couldn’t manage to make ETV acquisition significantly ‘accretive’. (Though the claim is it will be 4% accretive, etc. once stabilized, but this year the impact is negative possibly because of only partial period of rent coming in). Source: PG15 Supplementary Data FY21Q3 or even Slide 10 Investor Presentation FY21 Q3.

There is a ROFO for almost 30 msf (possibly spread over the next 5-6 years). The probability of being taken over is higher than the probability of not being taken over. I’m guessing they would have to resort to more equity dilution. If interest rates move up, we’re facing a scenario where the cap rate or yield on the properties could be lower than the cost of borrowing. It would be difficult to make anything accretive then. I feel this potential dilution with each acquisition could be a bigger risk than most of the other items.

- How are you thinking of occupancy rates?

There has been some downward pressure on occupancy in properties outside Bangalore. Even if it moves up, it could would awhile before we see rent coming in or money coming in. This could be atleast 1.5-2 years away (assuming 1 years of downward pressure then another 6 months for rents coming in).

This also implies that the downward pressure on the REIT price would continue (with each distribution, certain payables are being closed on the debt+interest front). That would potentially imply Rs. 20 decline in this period (this is the distribution amount per unit for a year). (btw distributions have also been declining).

- Does anyone have any insight into leasing contracts?

There’s a commencement date. This is different from when the entity leasing it starts paying rent (gap could be upto 6 months). There’s an escalation of 15% every 3 years. And there’s some premium to be paid if the lease is ended before the period. There’s an element of deposit as well.

What are the additional clauses? How do lease renewals fit in? How is WALE calculated while at the same time there’s talk of 3-5 year renewals?

The ICICI report says “We have assumed that the zero coupon bond maturing in June 2022 will be refinanced again on similar terms”

Anyone knows the quantum of the bond?

If interest is not being paid on the bond currently, it is just artificially inflating the cash inflows (and hence distribution) of the REIT right now, isn’t it?

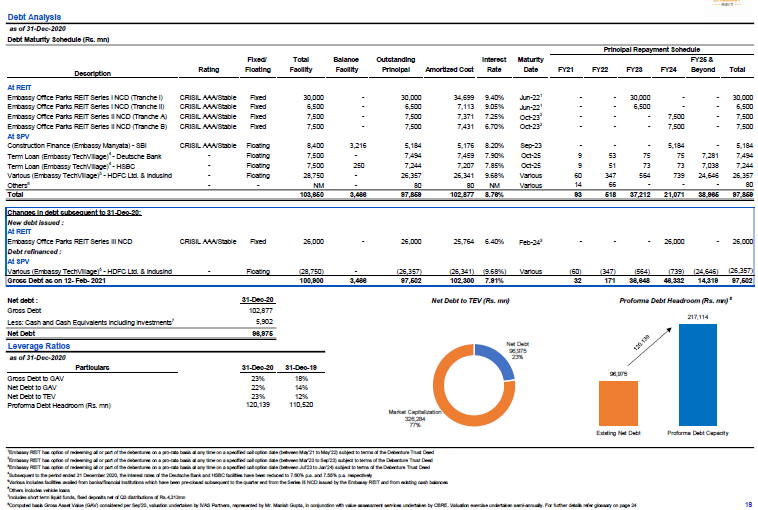

Find enclosed debt details of Embassy REIT from Data sheet available on Website for quarter ending 31 December 2020.

In my understanding, it is Series 1 NCD which is payable in June 2022. While your point is valid and one can say that by delaying interest payment and increasing the cashflow available for distribution. It may make sense to look at total amount, life of assets and use of leverage while evaluating this factor in my view.

REIT having 30-40 years life (with maintenance expenditure to spent on properties), the loan is like working capital for industrial unit. While on working capital, interest is charged to P&L, principal of WC is assumed to raised again and expected to paid only on termination of business. When we compare this with REIT, the interest of 9% on Rs 2000 Cr debt say, Rs 180 Cr would be what additional NCDF generated by REIT. If Embassy can again roll over debt with Zero coupon debenture (again with zero interest accumulated payable on maturity), the NCDF would not decline and remain stable. At one point, finally, the interest need to be charged, however, Rs 180-200 Cr p.a. is around Rs 1886.70 Cr (FY20 NCDF) is around 10% of distribution.

In my view final call would be whether company can refinance this debt on same terms? In my understanding it can given the structure and management quality (with support of Blackstone as REIT manager and promoter).

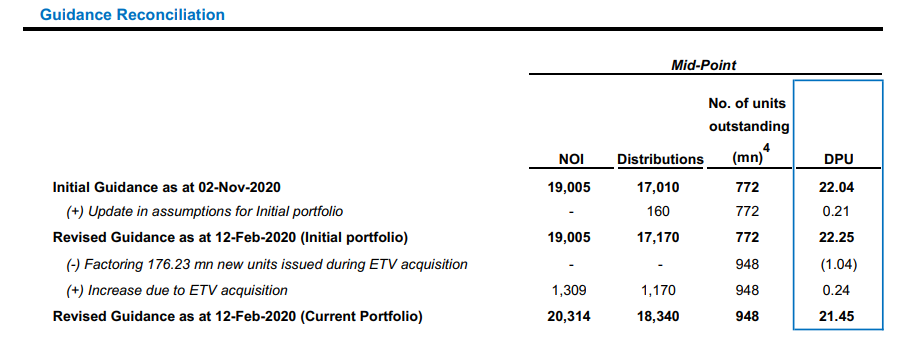

On first point about acquisition of ETV being distribution accretive acquisition, management issued units to raise funds in December. In end December, unit funds utlised to purchase ETV. However, on record data that is Jan 2021 for distribution, the new unit being pari passu where also subject to get same distribution as old unit. The benefit for ETV start from Jan 2021, however, new units issued in December 2020 were also eligible for distribution, which resulted in one time decline in December 2020 quarter distribution. From March 2021 quarter, ETV assts would also add to NCDF and resulting in higher NCDF of around Rs 5.5 unit in March 2021 quarter as per presentation.

In first point you also mentioned about various factor which affect future prospect of REIT, which are very valid. Hence, each future acquisition need to evaluated and voted by investor looking at macro factor and micro structuring before approving. Like any business, nothing can be projected about the business as their are moving part. In my view, one shall evaluate same when such situation arise and if one is not satisfied with business prospect by selling his/her investment in market.

On 2 point about occupancy rates, my personal view for long term, it would remain in range of 90-95% for A Grade building. I may be completely wrong with my assumption. However, in short term, projection of occupancy is very difficult to project, and that is one risk which any investor in REIT shall evaluate and satisfy himself/herself before making investment decision The Past details of occupancy rate in various properties are provided by Embassy on website in case one need that information,

On point3, I would suggest you go through Data sheet for December quarter. This broadly define tenure, amount of lease, market rate and area under lease and expiry expected. I do not have any access to lease contract.

Dislcosure: Same as past post, invested and hence view may biased. Not recommending any investment in REIT. Not a SEBI registered advisor

Thanks for the reply!

You mentioned Rs 2000 cr zero coupon debt, but it’s actually Rs 3650 cr, hence the accrued interest would be in the range of 340 cr per year, or around 18% of the distribution as per your calculations.

In my view, it doesn’t matter much whether they are able to refinance or not, when it comes to the question of whether the distribution is propped up by the zero coupon bond.

Also, as per my understanding, the current distributions do not account for the interest accrued but not paid (at least not entirely, any clarity here would be helpful).

As you said, they treat it like a construction loan where the interest is capitalized into the cost of the under-construction assets.

Hypothetically, if the entire payables in June 2022 will be converted into an interest bearing loan, the annual interest outgo will be something like Rs 300 cr (very rough calculation). This should be factored in in our future distribution projections.

I could be very wrong about any of the above, of course, and will be happy to be corrected.

Thanks for correcting my error. My apology for error.

Even with Rs 3650 Cr, please look at interest rate for loan. It is ~ 9% per annum. If one look at bottom half in portion, it provide information about new loan Rs 2600 Cr being raised for 18 months at interest rate of 6.4%.These funds were utilised to pay back variable cost Embassy Techvillage loan of Rs 2635 Cr which had interest cost 9.68% as on 31 December 2020. This one deal has only reduce interest outflow by around ~ 20 Cr per quarter (Rs 85 per annum).

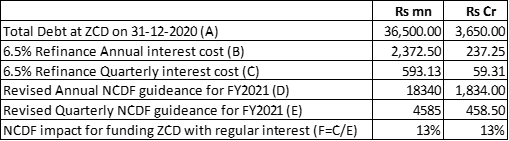

So refinance of Rs 3650 Cr even at 6.5% interest rate would be around Rs 237 Cr as against Current cost of Rs 340 Cr as per your calculation. So during FY22, total saving from lower interest would be Rs 102 Cr from Rs 3650 Cr loan refinance + Rs 85 Cr from Techvillage high cost debt. That would result in lower interest cost by Rs 187 Cr during FY22, other thing being same.

Above calculation would be relevant for P&L but NCDF calculation would have different impact.

Now coming to critical aspect of how it would affect NCDF? In case company finance this debenture as regular interest paying at 6.5% interest, same would result in additional cash outflow of Rs 59 Cr (Rs 3650 Cr @ 6.5% ~ Rs 237 Cr total annual interest cost divided by 4 to get quarterly cost) which is around 13% of NCDF at midpoint for FY2021 revised projection.

I am enclosing my working for reference.

In case Embassy REIT manage to refinance same debenture as cumulative Zero coupon NCD, there would no impact on NCDF from projection.

Thanks once again for asking valid question and bringing out my mistake in calculation. Appreciate your efforts.

Thanks again for the reply. Much appreciated.

I calculated Rs 300 interest outgo on Rs 3650 principal plus accrued interest on the ZCB. Hence a higher figure than the Rs 237 cr you calculated.

If on the other hand, the full amount is converted into another ZCB, then there might not be any impact on NCDF for a few years, but it would mean that they are borrowing from the future in a sense, to make the payout now. Which I think investors should account for in their calculations.

as per my understanding they would not continue with the zero coupon structure as market has flagged it as a key risk. So Embassy REIT team would definitely flip it into a interest bearing bond / ncds.

Further Interest rate assumption of 6.5% - should not be used for the calculation as we are the bottom end of the interest rate cycle. I expect at-least next year the interest rates to increase by 50 to 100 bps.

Also, vacancy would continue to be a factor in medium term. The good thing is they have good assets at terrific locations - especially Manyata on outer ring road with good connectivity to Bangalore airport. So you can factor 90% occupancy and work out your number.

Looks like the merger with indiabull real estate is approved

https://forum.valuepickr.com/uploads/short-url/uX0cveINkBSyh1B1VU5pODrk9Bk.pdf

Any idea what implications this would have on Embassy’s NAV / DPU/Balance sheet? Or is this unrelated to Embassy office. Could it come under their purview in the future?

Also, Embassy office results on 29th April.

This is unrelated to the REIT. No direct impact. Am I missing something?

It’s IB real estate and embassy real estate company merging

That’s what I thought too… but refer to this article when the news first broke last year Jan end

Quote:

“The merged platform will become the development arm for the listed REIT (Embassy Office Parks). The REIT will benefit by getting more developed assets, thereby increasing the yield of the REIT,” sources said. Embassy will raise Rs 1,420 crore from Blackstone and other investors.

“The equity investment will bring significant cash to the merged entity,” It added.

Also, another quote from a different article says the same Indiabulls Real Estate: Merger Plan: Indiabulls Real Estate, Embassy to fix valuation, swap ratio - The Economic Times

“The merged entity will become the development arm for Embassy Group, and it will provide a mechanism to seed assets for its Embassy-Blackstone REIT, India’s maiden real estate investment trust, which was listed last year.”

Also, when the news broke it led to a run up in stock price of nearly 30 percent from 400 to 500+ odd all time high in Feb(before the covid crash)so maybe that was an indicator regards what the market thought the nav/yield would reflect?

Note: invested. Not a sebi advisor. I’m verging on pure speculation above.

Edit: thanks @gurjota and @rushil . So basically in the longer term as the merged entity completes projects(some in the near future) the REIT arm can just buy them(at I’m assuming favourable terms compared to buying from an outside source) and hence improve its yield so it is a plus point long term. However, residential seems to be the main aspect indiabulls is bringing in with just a small percentage of commercial assets equaling about 144 crores in rent if taken by the REIT arm. so this may just be of little to no effect to the REIT. Cheers.

This doesn’t impact the REIT in the short term but can have longer term impact depending upon the commercial assets developed through the merged entity which may end up being acquired by the REIT and will need to be analyzed (valuation, yield, potential, etc) at that point of time.

There a few things that the merger will bring to the table

- 43.2 million Sq Ft planned commercial area

- Future rental potential of 4200+ Cr per year

- The merger will expand the presence of Embassy across other growing commercial markets like NCR,Gurugram etc (A 1.31 MSF office building is under construction in Gurugram)

- This will act as the building arm for the listed REIT and it will benefit both the entities

- The merged entity has Fully paid for land bank of 1929 Acres across Mumbai, NCR, & Chennai and 1424 acers of Nashik SEZ which might be used for future developments

Although there are no immediate benefits but having a listed development arm with good assets and cash flow will certainly benefit the REIT in longer term, and the REIT will benefit the development arm by providing a ready source for monetizing it’s assets whenever they need. The main aspects Indiabulls is bringing in is the land bank that it owns and its presence in markets other than Bangalore helping Embassy diversify.

@sumi00 Agree with your views on “gold-plated facility management contracts/one-off repairs would be another area to monitor”. There was chatter in Commercial RE circles that ETV was acquired from the Embassy Group at a higher than market price @d.investor Need to watch out for acquisition costs for Embassy – India Bulls developed properties that Embassy REIT might potentially acquire. I feel there are conflict of interest involving Virwani. All of these could potentially be rumors, but need to be conscious of such Related Party Transactions.

Disc: Invested in Embassy REIT over last 2 months