The big tech firms have not really stopped buying up property in the US CRE sector too.

Anyways in a infrastructure starved country like India high quality real estate isn’t going to be out of favour for too long.

They can even offset companies leaving by building the place for data centres- Mind space has started doing that. If India grows to 5T dollars economy then do I expect these properties to struggle? My guess is they won’t.

It takes time for trends to reflect in numbers. When big tech hasn’t opened up offices (mandatorily), how can they predict how many people would end up where? Also, if they can buy, they sure can sell the same offices. What needs to be tracked is incremental buying (whether there is acceleration or deceleration in buying.)

Yes good article. It remains to be seen how this plays out.

I was thinking that for the listed REITs one way to counter the loss of customers due to WFH can be to setup data centres in their parks- as done by Mind space.

Had a few questions and would request members to guide if they know/otherwise we can all benefit by searching up on these:

Is data centre leasing a very specialised business? Any one with Tech background know about this?

Can we see these REITs pivoting to this opportunity to deal with wfh related issues?

Mindspace did say their latest leasing of space as a data centre was value accretive Is this the norm? Are data centre rentals higher than usual office leasing?

Size of data centers will not compensate for loss of office space? It is minuscule in size compared to space required by an employee.

It is slightly specialized business in the sense that it has to be highly secure with no risk of flood, fire, non-dusty location, approachable etc. Nothing very specialized.

Plus going verical in data-centre has some design constraints. Most data centers are still one floor setups with easy access to heavy power and cooling needs. Vertical data centers are slowly picking up but in my understanding, beyond a point, it stops being econmical.

I remember 3-4 years back there was such overcapacity that some top datacenters were giving racks away for free for a year. Today we are at opposite end of cycle with high demand and capacity being added.

I was looking at the P&L of REITs and see they are making less profit on consolidated level.

i.e Mindspace is making quarterly profit of 120 cr (vs 280 on standalone) but the distribution is in range of 250 cr per quarter.

Any idea what consolidated statement for REIT means?

As per SEBI guideline which necessitates minimum 90% of Net Distributable Cash Flows (NDCF ) i.e. 90% of 280 crore = ~250 crores to be distributed to unit holders.

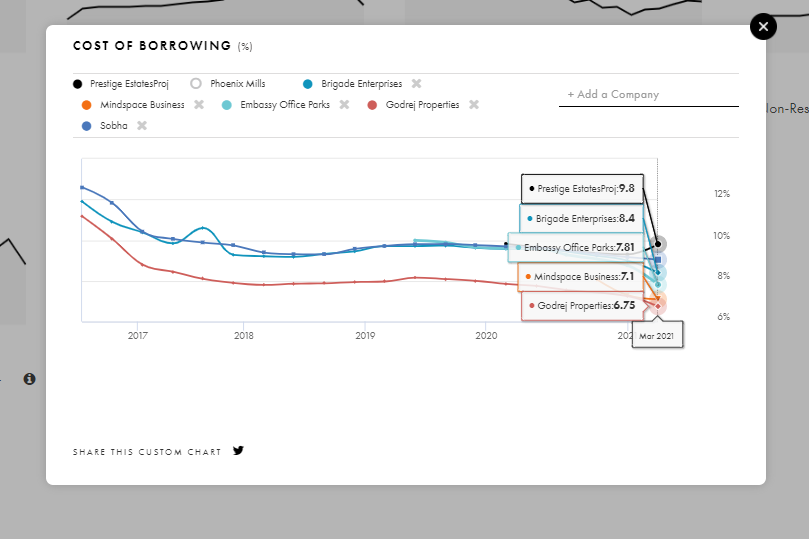

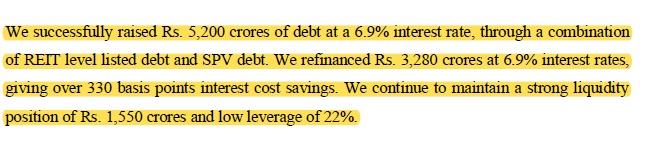

The interest rate decline for Embassy REIT, mainly due to decline in interest cost over last 2 years. Embassy REIT now intend to refinance further debt with fixed coupon debt and expect interest cost to decline. Find enclosed relevant extract from the Mr. Holland in Unit Holder meeting July 2021 where he discussed FY21 interest cost.

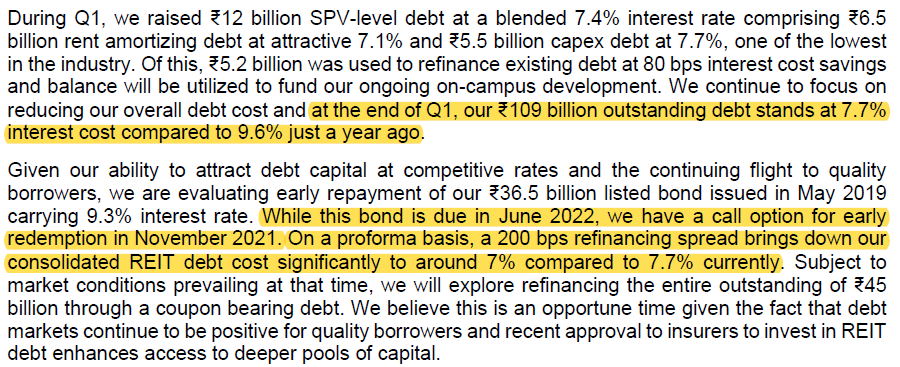

In Q1FY22, find enclosed management comment of debt and interest cost.

So, if they finance new debt with 4-5 years tenure at around 6.9% debt, then cost to the extent of that portion of debt is fixed for the tenure. When that debt come to maturity, then company would be subject to interest rate prevailing at that for the rating it has. Second point to note is funding for assets under construction and lease yield assets. The construction finance cost is relatively higher than Loan against real estate lease. As the new construction of assets get over by 2024, the REIT can refinance same with lower cost of debt.

However, in case they decide to undertake further construction, then it may not be material.

So, in my view, we can expect at lest 3-4 years of fixed cost ~7% for Embassy REIT. I may be wrong and reader shall take note that of that.

Discl: My view may be biased due to my investment. I have purchase Embassy REIT unit during last week. I am not recommending investment or selling in Embassy REIT. I am not SEBI registered advisor.

While planned stake selling by Blackstone group is over, per today disclosure their entire stake is pledged, @dd1474 and fellow VPers - how do you see this aspect of promoter group as this doesn’t seem to be case with other two REIT.( Brookfield and Mindspace zero promoter plegde). Timing is also strange as unlock for offices seem to gain traction and with some wait they could have got better pricing but again insider knows better.

Blackstone declined to comment on the transaction.

The exit was an attempt to provide liquidity to Blackstone’s limited partners, or investors in its fund, and the PE remains the largest shareholder in Embassy, the person cited above said on condition of anonymity.

Capital Group, Dutch Asset Manager, Nordea Bank, ICICI Prudential Mutual Fund, and HDFC Life were among the buyers.

In my limited understanding, as an individual investor, since we also do not like to put all our investment in single company, likewise institutional investment also driven by multiple factors and would evaluating multiple investment opportunities at a given time. In case of Embassy REIT we find that promoter group still hold more than around 30% (systematically reduced from over 40%) as against minimum stipulated stake of around 15% (in my understanding and it may be wrong). In REIT we find sponsor holding reasonably large stake( i.e. ~30% and above), in IRB InvIT, the sponsor holding is only around 15%, minimum stipulated level by SEBI.

Having said that, the movement in holding of sponsor (specifically reduction) need attention of investor. In my limited understanding, since the trust is run by professionals whom I trust, and supported by large institution, I would not have concern with nil level investment by sponsor. The real skill required in REIT is ability to source new assets, manage the property well, ability to lease area to newer tenants and maintain the assets under management. Further, most of this professional team are like Asset Manager of Mutual funds. Their main incentive is to get fee income from running business properly and also grow NAV of assets under management (as fees are linked to Asset value, which in my opinion, align investor interest with professional team running the business).

So, in case sponsor group find other alternative which are better and meeting their risk return profile, I find nothing wrong in them selling their stake and properly disclosed to Stock exchange. This is my current view and it may change in future. Every investor has different risk/return and experience and hence shall apply their own parameters for evaluation for all events including pledge and stake reduction by the sponsor.

In my understanding, recent decline in price may also have some connection to recent announcement of NSE to put REIT inclusion in index in hold. The first announcement of inclusion of REIT in index by Sep 30 could have driven increased investment by investors which try to gain from short term trade in such opportunities. The second announcement on holding decision on inclusion along with sale by sponsor may have resulted in drop in price of REIT. In my limited understanding, there is not fundamental change in business. On other hand, I believe business has improved as compared with Last April 2021 with major case increase in COVID and if real estate company share price movement is any indication.

Disclosure: I am invested and added some more units yesterday. I considered InvIT/REIT as a part of my debt portfolio and it account for nearly 20% of my debt portfolio at market value. My view may be biased due to my investment. Investor shall do his/her own analysis before investment. I am neither SEBI registered advisor nor recommending any investment.

Can you tell me which website have you used to create this chart of “cost of borrowing”. I am new to VP and so don’t have much idea about it. Thanks in advance

with Mr Jitu Virwani, CMD, Embassy Group")