As I have stated earlier, the problem is not with the acquisition itself but the equity capital raise that the REIT is undertaking, which in my opinion is unnecessary, to fund this acquisition. Having said that, I’m not too optimistic about institutional investors acting to prevent this. Historically, institutional investors rarely vote against resolutions sponsored by the company’s management regardless of how shareholder unfriendly they may have been. The recent delisting of ICICI Securities is a case in point.

4 Likes

E-voting for the ESTZ acquisition and Rs3,000 crore equity capital raise has opened today. Depending on your depository, you can use either of the following links to cast your vote. It takes less than two minutes to cast your vote.

https://evoting.cdslindia.com/Evoting/EvotingLogin

While I’m still not too optimistic about the capital raise resolution failing, there still remains a small probability about a favourable outcome. This specific resolution requires 60% of the total votes to pass. As of 31st March 2024, the sponsor holds only 7.69% of the total outstanding units while institutions hold 73.63% and non-institutions hold 18.68% of the total outstanding units. This fragmented unitholder base and high voting threshold present a small probability that enough non-sponsor unitholders may not vote in favor of the resolution for it to cross the 60% threshold. In such a scenario, votes cast by retail unitholders may prove to be the deciding factor. As a disclosure, while I voted in favor of the first resolution regarding the acquisition, I voted against the second resolution regarding the equity capital raise.

8 Likes

Here is a DPU track record of 3 office space REITs. None of them have given any appreciation in DPU since listing. I don’t think any of these are working for minority share holders. All their focus is either to increase their assets under management or benefit sponsors.

Embassy REIT:

First full year DPU (FY 2020): 24.39

TTM DPU: 21.33

Brookfield REIT:

First full year DPU (FY 2022): 22.1

TTM DPU: 18

Mindspace REIT:

First full year DPU (FY 2021-22): 18.79

TTM DPU: 19.2

To me it looks like a failed investment product yielding DPU in the range of 5-7% with no YoY appreciation. Given this track record, do you see any case for investment here?

6 Likes

If that’s the case, then please explain why people buy homes that don’t yield even 3% rental yield? And here we are talking about entire India, where everyone buys home/flat, why can’t everyone live on rent forever?

Now, compare it with REIT that’s offers yield comparable to fixed income instrument (~7%), in properties that are hard to replicate (grade one commercial offices) and offers protection from inflation with rising rentals over time.

Yes, agree, the yields are almost flat since last 5 years, but that’ss due to big blows this industry has suffered, which include :

- COVID, which reduced the demand by half due to Work from Home culture

- Interest rates rise in last couple of years.

I think past is not the mirror of future for REIT’s, time will tell if this turns out to be pragmatic or foolish statement.

Disclosure - Invested and Biased, may turn blind

5 Likes

Well, residential real estate has different equation. Residential rental return is expected to be low with relatively higher capital appreciation. In commercial real estate, capital appreciation is directly proportionate to rental returns.

Moreover buying residential property is not always a financial decision, many a times it is more of an emotional decision and sense of security. Financially person may be better off staying in rental property and investing the funds in other better products.

Coming to your other point of REIT benefiting with rising rental returns, that is exactly my point is. In theory yes it is, but the way REITs in India are operating I’m not seeing this happening. REIT management is busy in acquiring assets which is not distribution accretive.

Thanks for your feedback. We have different point of view , I disagree but dont dis-respect ![]()

My views below:

“Well, residential real estate has different equation. Residential rental return is expected to be low with relatively higher capital appreciation”

Probably, this is precisely the hypothesis based on which residential real estate is bought. However, I fail to understand how capital appreciation can be high without healthy rental appreciation as both are very much co-related in long run.

Residential real estate moved 10 to 20 X in most part of india between 2000-2010. In fact, as kids we knew buying home as most prudent decision of our parents ![]() .

.

Probably that bull run is embedded in our psyche (me included), but if you look at 10 year period (2012 to 2022), residential real estate prices moved nowhere in most tier 1 cities. Capital appreciation is in the hands of market, and difficult to predict.

Real estate is cyclical play, best time to buy is when rental yields are respectable, irrespective of residential or commercial.

Note that these are my personal views, may turn out to be wrong / foolish in future.

5 Likes

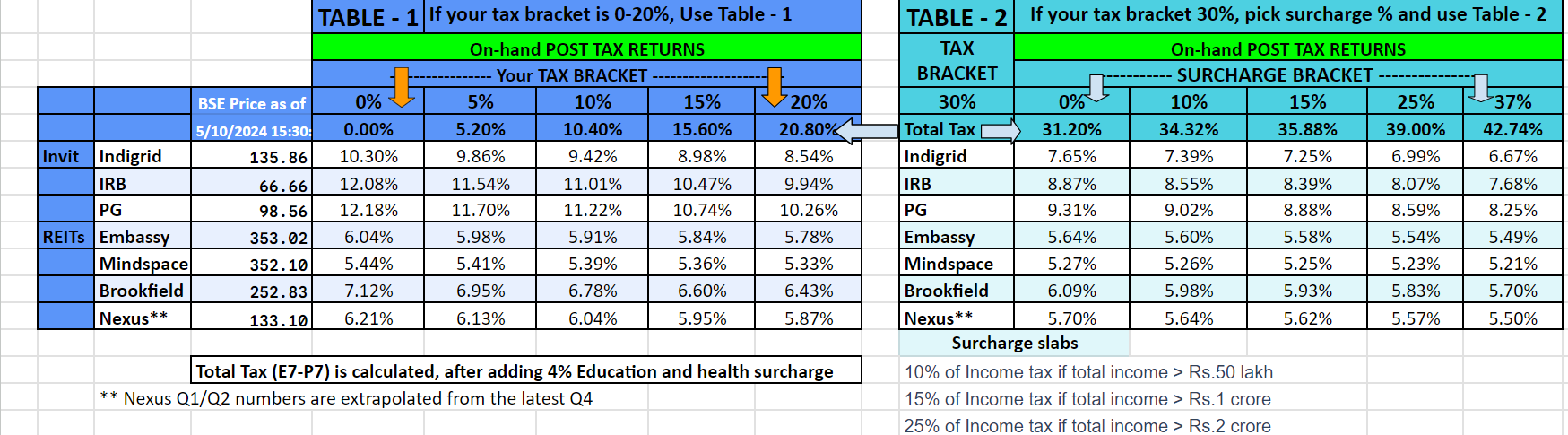

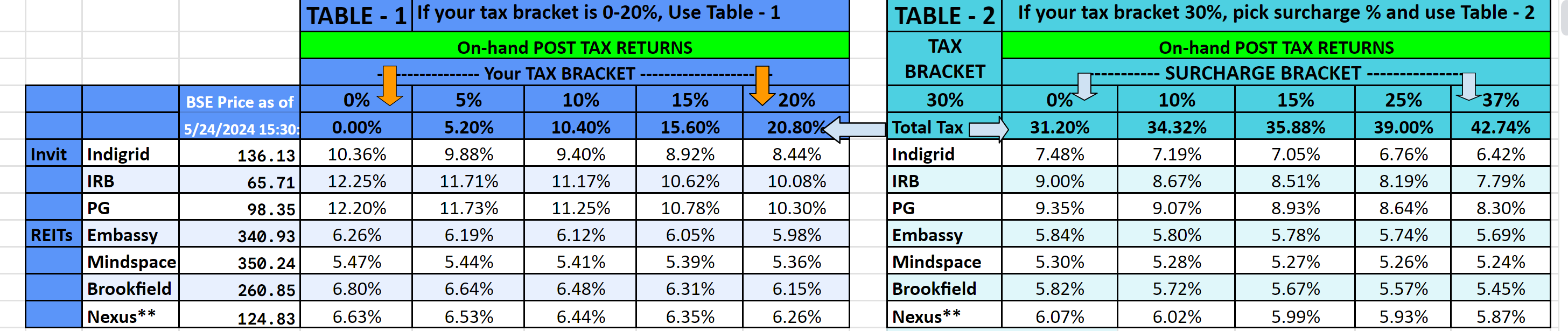

All the REITs have declared the Q4 results and DPU. Indigrid and PGinvit are yet to declare theirs…I have updated the yield table below…(whoever has declared Q4, it is there; otherwise, it is from last year Q4)…in Nexus, there is approximation since they have not done a full 4 Q year…as always, this is my calculated sheet…there can be errors and I am open to feedback

9 Likes

REITs are a great asset class in theory, but they will be good investments only if they are managed and governed well. Based on recent track record, I strongly believe that this asset class is doomed to fail in India unless regulators make significant changes to the way they are structured here.

The biggest problem in my opinion is that REIT management teams have consistently betrayed one of the most important and fundamental principles of management: to always act in the best interest of shareholders. In fact, I would argue that they have actively destroyed value for shareholders, only to benefit their sponsors - primarily by diluting existing shareholders through underpriced preferential allotments, to acquire potentially overpriced assets from sponsors. I am sure that in a more mature jurisdiction, they would face legal consequences for the kind of actions they have done here.

(Perhaps I am guilty of over-generalization here, but Indigird InvIT is the only entity from the REIT/InvIT universe in India I would consider as an exception to this.)

Potential solutions? Perhaps mandating the NAV as the minimum floor prices for equity raises would help. Or the entire manager/sponsor/trustee structure need to be changed.

Regarding Embassy: I exited all my remaining holdings the day they announced the equity raise. (I had trimmed a significant portion a few months ago when it appeared overvalued compared to peers.) I will consider adding a position again after the QIP is done.

18 Likes

Some institutions seem to have taken a principled stand against this daylight robbery but most others capitulated, unfortunately.

5 Likes

I think this an important point. Dilution of REIT equity is here to stay at the expense of minority shareholders. Raising equity at considerble discount to NAV will be value destruction.

The point to think is , whether this act makes REIT as non investible category, or we can still invest in REIT at a price where this risk is captured.

In my memory, I can remember many companies that do capital allocation errors, but the quality, longivity and growth in business compensates against the capital misallocation, when bought at reasonable price. For example ITC diversified into Paper & Hotels, businesses that have sub par economics compared to core business, and it will continue to do so in the future. Still, I think at a particular price ITC is a buy.

Can we think in similar manner about embassy, or we should completely avoid it, is a call that investor has to take.

Disclosure - Invested

2 Likes

Sorry this is not listed so I am not sure if it’s ok to ask… does anyone have any experience or information on https://hbits.co? Would appreciate any input.

Hi have invested in various fractional investment companies including hbits. Hbits has lower performance fees than some kf the others and service etc is good. However all fractional properties are going to be listed on SM reit index soon, I am not doing anymore investments till the listing happens as I am uncertain the impact it will have.

2 Likes

Why does Embassy have 12% capital gain on a one year trailing basis which is comparatively higher if we compare it to Brookefield and Mindspace when Embassy has been facing this issue?

Embassy REIT has done the acquisition using Debt.

Not sure, but it seems that they may not have been getting demand for the QIP at a higher price, since SEBI rules apply to such QIPs.

Given the weak stock, large investors can probably buy in the open market at lower rates.

Am I thinking this right?

Dis- Invested

Apologies to bring this one up again. I tried reading thread but did not get any answer for this. Can someone help?

InvIT REIT are strcutured product based on Cashflow. So Depreciation -Amortisation charge, which are major P&L item, are non-cashflow item. Since in equity, corporate is assume to run indefinite, it would need capex to surivive and grow and hence Maintenance Capex and Working capital requirement are deducted from Profit to calculate free cashflow to equity owners. However, Hybrid products (InvIT/REIT) work on current assets which are already financed from debt/equity mix and are owned. For instance, IRB InvIT have right to collect for say 15 years for Toll assets which is valued say Rs 90. So every year, as per accounting policy, there would be amortication charge of Rs 6. However, the InvIT has already paid for same. Future acquisition in IRB InvIT or any REIT/InvIT would be funded be new unit issuance or fresh debt . Hence, accounting proft or loss (after charging depreciation/amortisation) would be misleading. Hence, better way to look at Cashflow (defined as Net Distributable Cash flow or NCDF). The calculation of cashflow exclude cash avaiable from assets, less operating and maintance cash expenditure, less interest and principle payable to third party (for InvIT/REIT colnsolidated) and to parent (for InvIT REIT standalone subsidiary which normally cancell out on consolidation). Since future acquisition would be funded by new debt/equity mix, the current cashflow shall be look at net available cash (net of interest/princiapal repayment of exisiting loan and not depreciation which is accounting charge). or NCDF to get better perspective.

Hope these answer your query.

Please not that I am not REIT/InvIT expert and my understanding may be wrong.

Disclosure I am not SEBI Registerd advisor. I am not suggesting any investment action in REIT/InvIT. I have invested in IRB InvIT/India Grid InvIT/ Embassy REIT and Brookfield REIT. My view may be biased due to my investment. I am increase/decrease/exti from InvIT/REIT investment without informing forum.

3 Likes

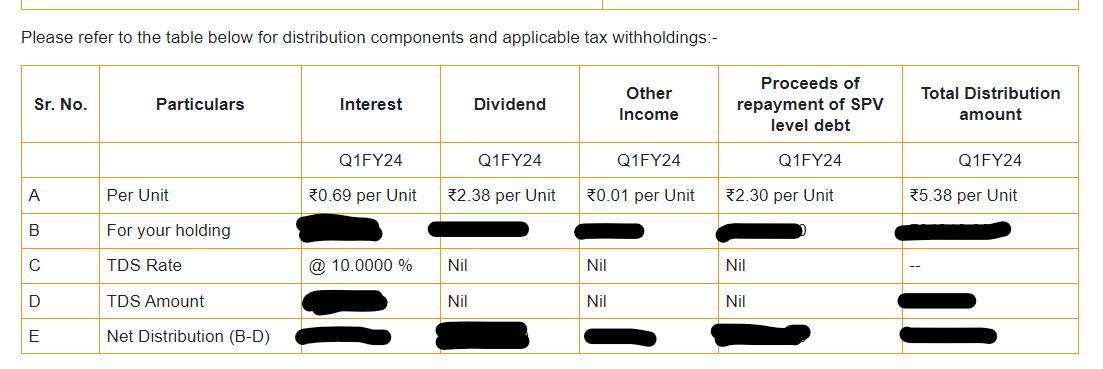

In one of the distributions this year, there was a new component called Other Income.

Is this component tax free in the hands of the investor?

As per my knowledge, The other income portion was tax exempted as there was no TDS deduction for my account. I am Resident Indian and holding same in my personal name. Every quarter, REIT/InvIT provide details of distribution along with TDS. The investor shall keep that and study it properly for its impact. Find enclosed screenshot of Q1FY24 distribution for which on 10 August 2023, I received email providing details of my holding. I have masked personal information. However, one can find that TDS is applied only on Interest portion. Every quarter distribution and taxability would be different and hence investor shall look at details to decide taxability for his/her account.

Discl: Same as last post, May increase/decrease/exit from Embassy REIT without informing forum.

5 Likes

As per the ammendment made in 2023, the taxation of REIT’s distribution is changed. Only if cumulative distribution goes beyond aquisition cost of the units, it’s taxable, that too only repayment of debt portion.

Please correct me if this understanding is wrong.

1 Like