@Amit2saxena @mahesh_s

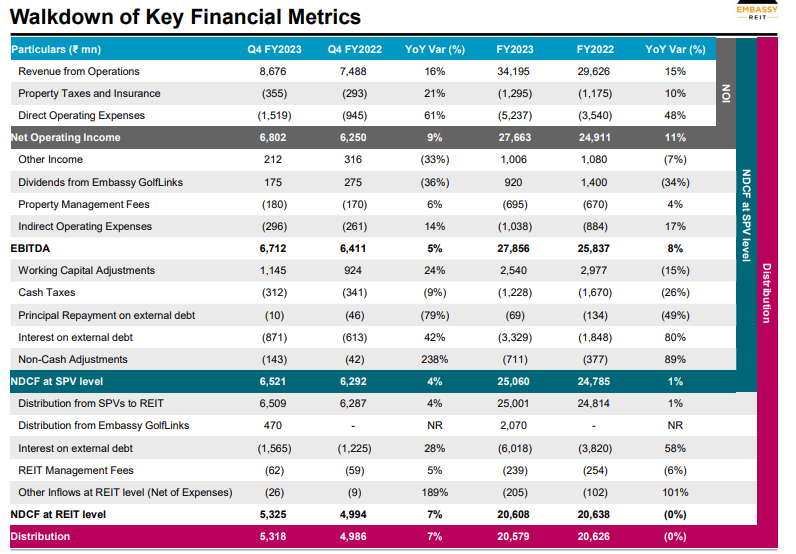

Thanks for seeking my view, although not sure how much it would be useful. I have gone through your postes and the past release of Embassy REIT for Q4FY2023. They have provided detail calculation including most of heads to derive at NCDF for Q4FY203 and FY2023.

I am enclosing same for everyone reference. I find this relatively simple to understand rather than working on my own from financial given my limited understanding. One can easily get understanding of what contribute positively and negatively in NCDFC from P&L and Cashflow .

While it may oversimply, I can not understand complex things and try to keep my life simple.

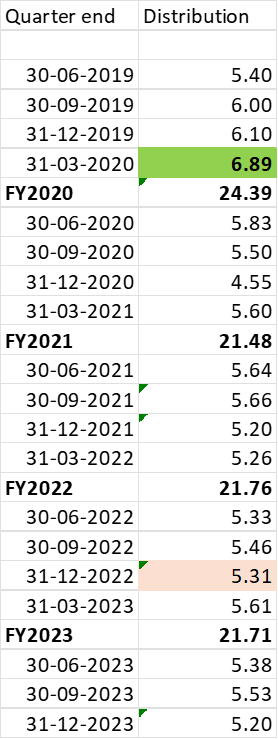

Total EBITA in P&L for FY23 is Rs 26,884.99 mn as displayed in message 259 as against Rs 27,856 Mn as shown in enclosed table. The difference is around Rs 971.44 mn can be attributed to Dividend income from Golflink being Rs 920 mn. So unexplained difference of Rs 51 mn, which is not very large given the operating matrix in my view.

Embassy REIT FY23 Reconciliation of NCDF with P&L.xlsx (9.6 KB)

Disclosure: Embassy REIT is my third largest holding in Debt portfolio and hence my view may be positively baised. I may change my allocation (increase/decrease/exit) from Embassy REIT wihtout informing forum. I am not SEBI registered investment advisor. I am not recommending any investment action. I am not CA and hence my understanding about accounting may not be correct.