Unable to understand the valuation for the latest transaction of Embassy Hub acquisition:

- 1.4 million sft is acquired for Rs. 3348 Million

- Which translates to Rs. 2391 psft which seems to be low

What am I missing?

Unable to understand the valuation for the latest transaction of Embassy Hub acquisition:

What am I missing?

Devil is in the detail. This is not a completed project and 1.4 MSF is when the project completes. There are 2 buildings in this project. Phase 1(0.4 MSF) and Phase 2 (1 MSF). Of this, only Phase 1 is nearing completion and Phase 2 is not even started yet. So the calculation you should be doing is 3348/~0.4 =Rs. 8370 PSF.

Attributing all the cost to Phase 1 may not be the right thing, because eventually (2027?) Phase 2 is also going to get delivered. So in a way this is a total cost for 1.4 msf of which 0.4 is nearing completion and 1 Msf in 2027. right?

The Q is how quickly will it translate to increase in distribution per unit. Increase in NOI needs to flow thru distribution if a judicious mix of leverage is used

As per ISEC report they are baking in 22.7/24.4 per unit in FY24/FY25

There is a new REITS/INVITS index in NSE

Positive move. Curious to see when and how Mutual funds will launch their ETFs and Index funds mirroring the new index. Globally the REIT ETFs also pay dividends based on the income received. Not sure if that will happen in India.

Very early days in India. The number of public listed REITs is very high for a market like US (a google search showed 225 listed (American Tower, one of the 5 biggies in REITs, got listed only in 2012)…not sure, how much is actively traded., compared to our 3 in India. So, it will take a bit more time to atleast get to about 10-15 to get some critical mass before an ETF can emerge.

PS - side bar conversation. One of the fastest field where REIT growth is in hospitals. Medical properties Trust REIT for example is in multiple countries and they made use of the expansion needed during Covid. In a developing country like India, where healthcare is still at nascent stage, I feel that trusts will look out to this field.

Declared distribution of ₹5,317.68 million (Indian Rupees Five Thousand Three Hundred and

Seventeen point Six Eight million Only) / ₹5.61 (Indian Rupees Five point Six One paise Only) per

Unit for the quarter ended March 31, 2023

https://www.bseindia.com/xml-data/corpfiling/AttachLive/704e7346-c34b-43c8-a0ee-299cc4e30fab.pdf

Vikaash Khdloya, CEO of Embassy REIT had put in his papers and in his place, the current CFO, Aravind Maiya takes over. The change is effective from July1

Vikaash had been around, from the beginning and at a time, when there are several headwinds ahead, his departure will raise some eyebrows.

Also to add the new CEO was the former CFO at Embassy before having a stint at Tata Realty

5.61 Distribution per unit: 1.94 (Repayment of SPV debt → Tax free as of now) + 2.81 (Dividend → Tax free) + 0.86 (Interest–> Taxable based on tax slab).

At 30% tax rate should translate into 5.35 post tax per unit this Qtr.

Annualized 21.41 per unit post tax which based on current price (329.69) is about 6.5%

It is 6.44%. Always, factor in the 4% health and education surcharge that is ominpresent.

PS - Lot of times, people confuse onhand absolute amount return from REIT and compare with post tax of other instruments. Getting 6.44% return post tax is equivalent to getting, 9.36% FD like return (30% tax bracket, which means 31.2% total tax and 9.36%X(100-31.2%)=6.44). I am not saying that the risks is these 2 instruments is directly comparable. There is always a chance of capital appreciation/loss in REIT (plus distribution breakup may change and the amount of distribution may not remain constant) and of course, any exit will bring in new complex calculations in Tax, that came in post the watering down in Finance bill

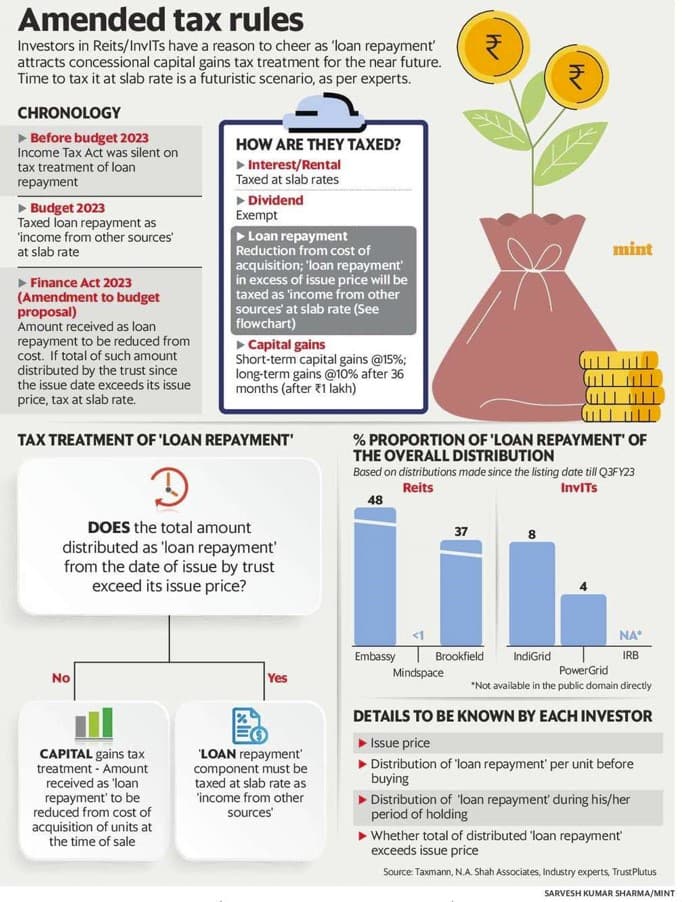

Here is a crucial question on taxation upon selling of the units.

Those, who have read and understood well, the finance bill amendment, this is your chance to answer.

Question is – when an investor sells the units, is the RoC/SPV repayment distributed from the time of IPO or RoC distributed, when the investor was holding duration has to be added back? if it is the former, it is really tedious and will get more complicated with time; on the other hand, if it is the later, at least some statements coming during the quarter can be kept and tracked. Knowing the nature of these sadistic sleuths, I am afraid that it will be the former but asking the question.

Let us take a more specific case On the Ex date of Embassy Q4 dividend (4th May). Say, I buy at 318 and sell at 321, next day ….do I pay tax on 3 (321-318) rupees + RoC from time immemorial? that does not make any sense at all? I have never enjoyed any RoC by keeping this in 1 day….why should I pay for all the past sins?

Similarly, I keep the same units till the next Q1 distribution and sell after the ex-date for the same 321. Do I pay cap gains on the (321-318)=3+RoC for Q1 or RoC since the time of the IPO. A few people I asked have pointed to the later and it does not make sense but wanted to ask

Logically one would think it would be the latter. One cant pay tax on a legacy loan repayment amount

(For Capital gains calculation one would consider only the distribution received as loan repaid. For distribution tax calculation one needs to take historical aggregated value). Please suggest if this is the wrong interpretation

Below article gives an example

So the benefit of loan repayment exemption gets neutralized at the time of sale of units thru a higher capital gains tax amount (as the purchase value comes down)?

Quoting from the article

"The amended tax rules indicate that the amount received as ‘loan repayment’ must be reduced from the cost of acquisition at the time of sale of unit by the investor.

For example, you bought a unit of a reit at ₹400 and sold it after 3 years at ₹500 in the secondary market. During the period of your holding, say, the reit distributed ₹50 as ‘loan repayment’.

To calculate capital gains at the time of sale, you need to reduce ₹50 from your cost of acquisition of ₹400, which would come to ₹350 per unit. Thus, your capital gains will be ₹150 per unit ( ₹500 - ₹350) and not ₹100 ( ₹500 – ₹400).

Effectively, the loan repayment component will be taxed as capital gains at the time of sale of units.

But that’s not all. Just like with every tax rule, this provision is not without ifs and buts.

The capital gains tax treatment for ‘loan repayment’ component is not forever. It is only until the total of such amount distributed by a reit/invit doesn’t exceed its issue price.

For instance, the issue price of a reit/invit unit is ₹300 per unit. Say, you bought a unit of a trust when the total of ‘loan repayment’ component distributed by that reit/invit (from the issue date, not from the day you bought) just exceeded ₹300.

Any distribution that you will receive in the form of ‘loan repayment’, irrespective of your holding period, will be considered as income from other sources, which attracts tax at the slab rate in the year of receipt of such income.

But your predecessor, who held the unit before the sum of ‘loan repayment’ by the trust exceeded ₹300 (issue price), would be eligible to adjust such income from the cost of acquisition and treat it as capital gain at the time of sale of unit.

Now, a doubt might arise to you on how you as an investor would know whether the reit/invit distributed ‘loan repayment’ in excess of its issue price or not. That’s where the disclosures from companies come into picture. The industry players are still unsure of how, what and when such details must be disclosed by trusts and awaiting a clarity from the government.

Having said that, industry experts believe that investors need not worry about it much. This is because they opine that it would take minimum of 15-20 years for the existing trusts before the total amount paid as loan repayment exceeds its issue price."

Looks like

a. For Qtrly distribution tax calculation: historical ROC needs to be aggregated to determine whether ROC component will be taxed or not. Current scenario all investors will fall in tax free status as historical ROC is below issue price

b. For Capital gains taxation (on selling of units): Only the actual ROC distribution received (duration of holding) is to be reduced from purchase price of units to pay a high capital gains tax

Please feel free to correct/modify based on your understanding. Thanks

2 scenarios emerge:

OR

I think this video from PrimeInvestor does a good job of explaining the ROC, taxation and capital gains for REITs and INVITs.

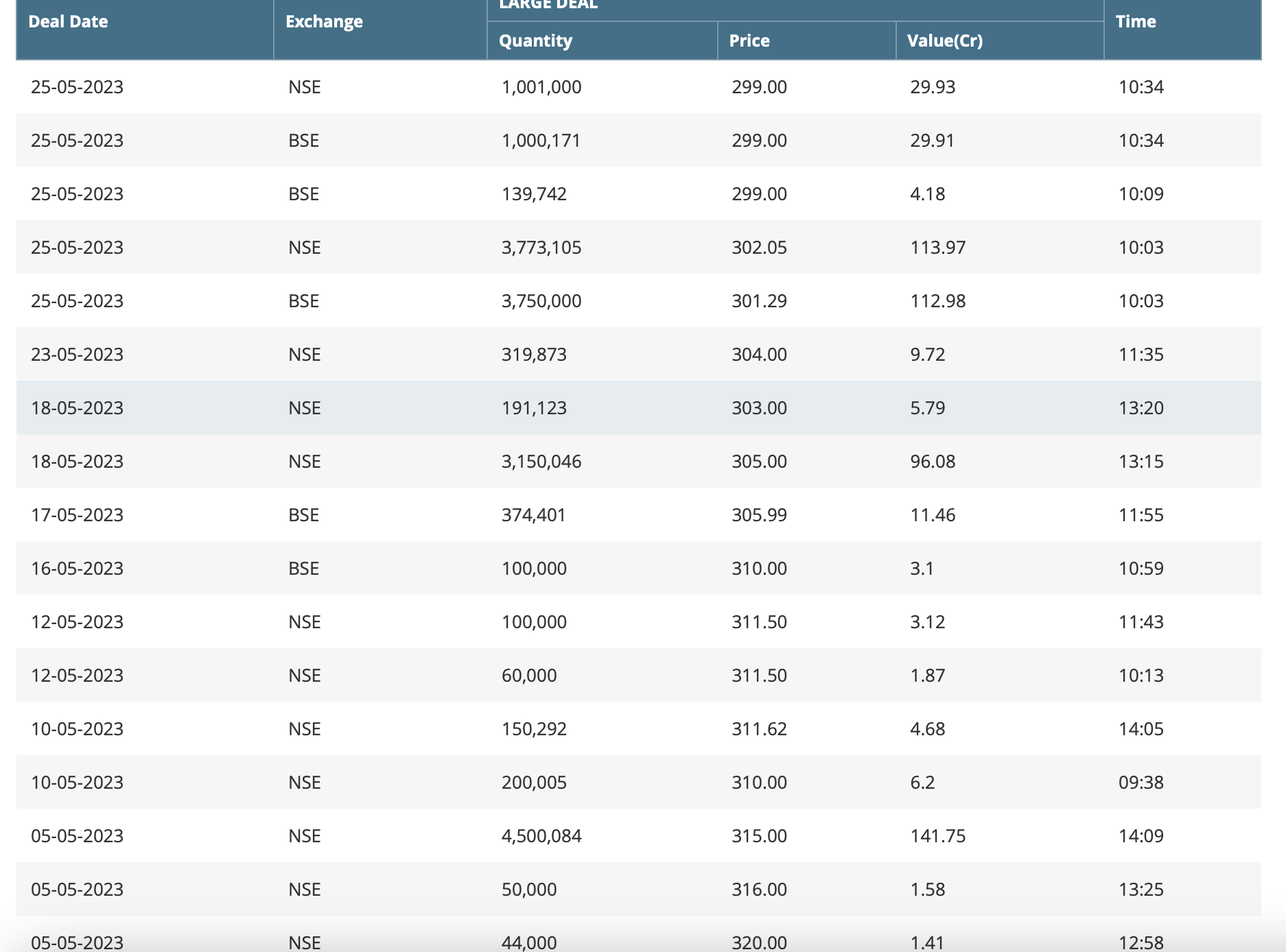

Is there a source which tells us who has been buying the large block deals today and on 18th in Embassy REIT?

CEO stepping down and year on year liquidating his entire ESOP/share based compensation issued to him is bound to raise major eyebrows

He basically had zero belief in long term performance of the very company where he was the CEO. This is despite the fact that by just holding the units, he will receive healthy dividends

Wondering if it might be a good time to add more units. Post tax yield looks pretty attractive given the overall steadying of interest rates and possible reduction going forward

Headwinds include the highly likely US recession ahead (given Embassy is mainly tech occupancy) and ofcourse if there are any governance issues

Thoughts?