@297.39, yday closing price, for 31.2% tax bracket (30% plus 4% sucharge), the Embassy POST-TAX yield is about 6.88% (for same measure, comparison across invits and reits…indigrid 7.11, IRB 8.67%, PG invit 7.27 (higher RoC declared yday), Mindspace 5.82, Brookfield 6.27 (all based on preceding 4 Qtrs Distribution), nexus (based on projections) 6.88)…so, pick your bets…

Pl note that the tax and surcharge bracket is a very, very important factor and any minor change in that will tilt the numbers.

Who has given committed guidance on Distribution, going ahead? Visibility, track record, confidence looks good in Indigrid ; IRB looks like flat to very mild increase in distribution, unless Janta decides to be on the road, every day of the year, in their project areas !!..PG Q4 results came yday and I have to do some more due diligence… On the REITS front, Embassy has stayed away from guidance (this plus their other problems of non-stop sales in bulk) has pulled it down to a life time low, below the IPO price of 300…

PS - Adding Embassy since 310 but cringing everyday, looking at the hemorrhagic pattern

This has been pattern. This reit trades in a band and by the time next dividend date is near it will go up. Next dividend due date will be in Jul so if we hold it for 2 months it will recover. One can do short term trade if they don’t want to get dividend.

You may check charts and see how reit has performed in previous years

I have observed that trend. Last qtr, Embassy kind of reversed it around 301 but this time, it has gone below IPO price. Yday low of 295.xx points to more in the offing. At some point, my fear is the lack of guidance & certainty will prevent it from reaching back the 325 kind of range. I hope I am wrong

I took a position in the same context , i feel like 300 being a strong physiological support .Healthy dividends yield does give holding comfort combined with there have been fundamental investors here who have parked a significant portion of there wealth here so they have done there due diligence.

i have invested in tranches and would buy another dip as long as the yields are intact and no plans to hold it long term just a super safe swing trade bet. (only downside higher STCG on reits.)

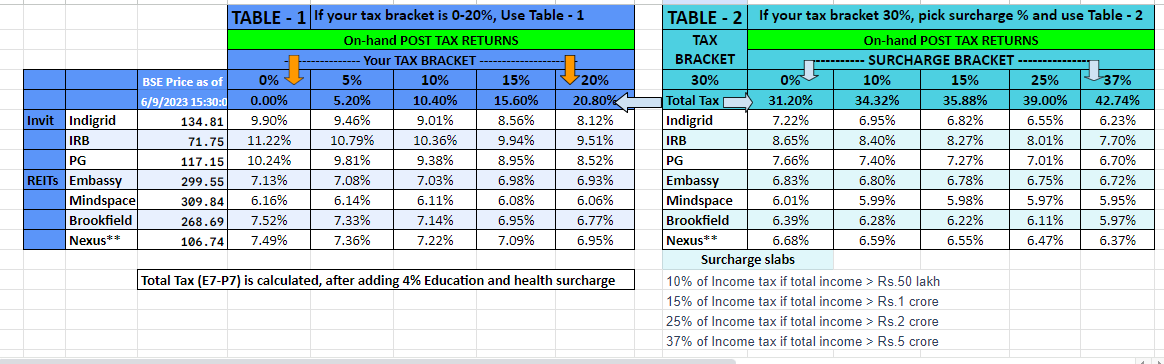

Wanted to give a comparative view of yields, on the prices as of 9th June 2023 (earlier I had shared it on 2nd June. There was a minor error in DPU of PG and I fixed it…won’t change anything drastically and it is a 2nd decimal correction)), and this is based on the rolling 4 quarters DPUs…Obviously, yield will differ for your tax bracket and hence pick the right slab below…

REMEMBER that these are POST TAX, ON HAND Yields for the Invits/Reits, for the price shown. **Nexus yield is based on projections gleaned out from various interviews, during IPO.

Hi all,

Bit curious to see that this thread is predominantly on taxation aspect and very limited discourse on the strategic perspective for a company like Embassy.

A few mid term points for consideration-

A. Nothing in known horizon points to decline in rental rates or occupancy

B. Indian IT growth story is intact and so is GCC growth story

C. Embassy has among the best execution track record - from the EGL golf link days

D. Their hotel business is accretive compared to others - proximity to offices ensure higher occupancy and yield

E. Interest rates direction will be favourable going forward

In fact, one can say that Embasy model is being taken up by others .

So, why would one not buy into this company if one has a 3-5 year horizon . Even if the stock price appreciates only 20-30% , coupled with dividend yield , this could be a 50%+ value with very strong downside protections …Am I missing something ?

Fundamentally I agree with your view. However, globally, REITS are products that give 5-6% asset appreciation value + 5-7% yield via rental income which brings the total annual returns expectation to around 11-12%. I am not sure what your assumptions are for a 20-30% stock price appreciation. That seems a bit far-fetched to me.

Another tail wind here would be the inclusion of REIT/INVITS in front line indices. It will still take some time but globally REITS are a part of index. The S&P500 itself includes 8-9 REITS if I am not mistaken. Once REITS mature as a product in India, there is a very good chance of them getting included in our frontline indices. That will then increase the liquidity and pump up the share price especially by FII’s. However, I see all this happening a few years from now. Until then I believe its a good time to accumulate these and view them as an asset class to hold for the long term.

Just a disclosure from my side. I have significant exposure to REITS/INVITS in personal capacity. My views are based on individual research and could be biased.

I wanted to get everyone’s views on use of REIT as income generation tool post retirement. FD and other debt instruments have fixed interest which stays same over the years. REIT income has potential to increase by 14-15% every 3 years. They also continuously raise debt for new space / redevelopment. So REIT income can potentially keep up with inflation over long period.

This makes REIT a commercial real estate without hassles of managing one. In my opinion, this makes REIT a very attractive income option. In world of retirement income generation, where safe withdrawal rates of 2.5-3 and 4 are discussed, I think having decent allocation to REIT can increase one’s safe withdrawal rate (or reduce required portfolio size).

I understand we are still at early stage of REIT in India and there are risks involved. Would like to hear everyone’s views.

Not only for retirement options but a lot of people who want to F.I.R.E or it could also be a even good swing trade bet ,I don’t mind holding this for a couple of months to even a year the the dividends easily beat bank intrest rates and even F.D and i feel like we are about to touch peak interest rates in the near future so if and when interest rates start falling embassy reits will move upwards to match the yield of that current interest rate period.

Hi Nikrod: Like Raku mentioned, globally REITs are favourite amongst the F.IR.E aspirants combined with Dividend growth stocks for income generation. India is still a very nascent market for REITs INVITs with a handful of listings. Hopefully this will change going forward.

While distribution yield is the primary consideration (benchmarked against risk free rate or a 10 year govt. bond yield), the underlying growth potential of the assets is also important to factor in

Good luck with the REIT journey

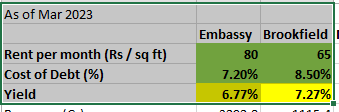

Probably I am making things too simple here, but the yield of REIT depends primarily on two factors 1) Average Rent per Square foot of the portfolio 2) Cost of Debt.

Embassy scores far ahead than others (e.g. Brookfield) here, still their yield is less. see below:

Is it because 1) Brookfield is more operationally efficient or

2) Brookfield is capitalizing more interest and paying higher distributions

The yield will be dependent on the number of units outstanding and the % of free cash flow being distributed. It is not comparable to the other metrics…

Having a significant amount in REIT during retirement years in risky in my opinion…

The risk comes from - what if there is a fraud or any such similar situation where the stock price would fall considerably.

Imo, during retirement years one must focus on capital protection and not capital appreciation.

Ofcourse everyone has a different risk appetite…but one must think of such risks.

One would ideally divide money between 3-4 listed REIT’s and have maximum 15-20% of net worth allocated to this asset class. That limits the loss due to fraud etc. in one company. Also as long as office assets are paying rent, distribution might not be impacted much which should be focus rather than market price.

In my opinion, real estate in India will always have black areas, related party transactions etc. Though most are related to parent company. Structure of REIT insulates unit holders from large scale issues. An example is Embassy parent company and even Blackstone defaulting on debt which had negative impact on Embassy REIT price but zero impact on distribution. These issues were/will be forgotten by market in 1-2 years. So one should take these issues as part and parcel of business.

@Amit2saxena

The distribution from REIT need to seen in context of investors base post tax yield. Generally, REIT is more of investment vehicle for institutional investor and HNI as compared with Retail investors. While tax rate may for foreing investor based on jurisdicton of its registeration, for Indian investors, most of investors would be in marginal highest tax slab in my understanding.

Brookfield distribution for Q4FY23 was Rs 5 (Rs 2.66 Capital return and balance Rs 2.34 interest). So only Capital return portion has tax deferred benefit while nearly half distribution would be taxable at marginal income tax. Assuming 30% income tax, the post tax yield for Brookfiedl REIT investor would be Rs 2.66 Capital Return+ ~ Rs 1.64 Interest (post 30% income tax) per quarter or ~ Rs 17.2 per annum, resulting in post tax yield of 6.56%.

In case of Embassy REIT, Q4 distribution was Rs 5.61, (Taxfree Dividend Rs 2.81, Capital retrun Rs 1.94 and Taxable interest 0.86). Assuming 30% marginal tax, per quarter post tax distribtution would be ~ Rs 5.35 per quarter or Rs 21.41 per annum, giving post tax yield 7.3%.

Hence, in my view, at current level of prices, Embassy Post Tax yield are higher than Brookfield. However, Embassy group promoter are facing some liquidity issue and the management did not released guideance for distribution in Q4FY23 con call (normally the practice followed by the REIT in past) has added uncertainity in investor mind. Even Blackstone has been selling REIT units frequently. The latest MD in Embassy REIT resigned within 12 months of appointment. The business outlook also appear more uncertain then in past with incerasing trend in work from home IT sector, at least in global market, which resulted in major decline in price of Global REIT.

All thease factor contributed to decline in Embassy REIT price.

Disclaimer: I have investment in Embassy REIT and hence my view may be biased. I have not done any trade in last 1 month. I may change my investment in Embassy REIT (including completely liquidating my holdings) without informing the forum members. Reader shall consult his/her financial advisor before making any investment decision. I am not SEBI registered advisor. I am not suggesting any investment action in Embassy REIT.

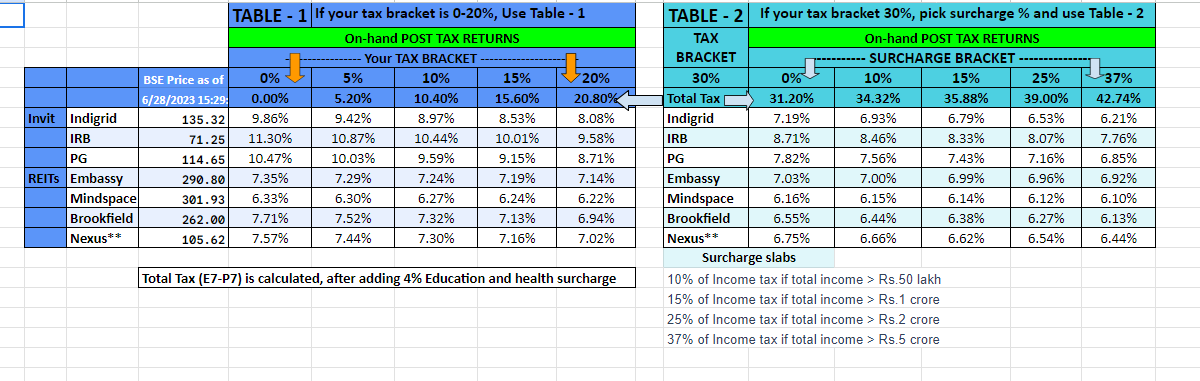

Yield table, as of today morning (publishing it since Embassy has gone down by another 10 Rupees) and PG too joining the slide…Mindspace, Brookfield are no better !!