2 Likes

A great write-up on understanding the global as well as Indian carbon credits market by @Tar

4 Likes

Hey guys. I’ve completely exited EKI in June but have extensively tracked since IPO. In process, have tried to build my understanding about credit markets as well. Have curated a set of questions over time and believe that if there are answers to these, it will be easier to track the company and the space going forward. Putting those questions below as it might help someone interested.

Interoperability between CCM and VCM

- Where do you see interoperability in the market heading? Why I ask this is because there is more focus now towards net zero and at CCM level that should increase the market velocity. So, if VCM could be allowed more to supply to CCM, there could be a sudden expansion of the market.

Quality of VCM credits

- In the market sense for the quality of credits buyers look for, where do we stand in our basket of projects? How would you segment your basket in terms of low and high quality? Is price a meaningful indicator for the same? And if so, what would be the bifurcation in price terms if you could tell from future point of view or in relation to whatever credits we have sold already.

- What is the rough blend between compensation vs reduction projects both from executed and to be executed POV?

-

Could you highlight a bit on the “preference for local supply” part of the VCM in relation to EKI. As in, what has been the historical demand, the current demand, an estimate on the fraction of projects that would qualify for the same?

– And if this is the emerging trend and a metric for assuring the quality of credits for VCM, does this mean that we’ll have to scale up fast and compete in different geos with different rules, regulations and laws? I’m aware that we have and are scaling to multiple nations already. So, how are we and and how do we plan to compete with the global consulting leaders who would have deep expertise and pockets to exploit those opportunities better?

– Are we setting ambitious targets to get more talent on board for the same and if any plans, could you please highlight? -

Could you touch a bit on the point of “additionality” from EKI’s POV in the Voluntary market. As in, how many of the credits that we’ve historically sold or have in the pipeline would qualify as additional to what the corporate would have done in due course of their running the business? Have we had a policy for or are we looking at doing more of those projects which would count as additional? Because that could substantially reduce our risk of finding a buyer, getting a good price and not sitting on inventory, right?

-

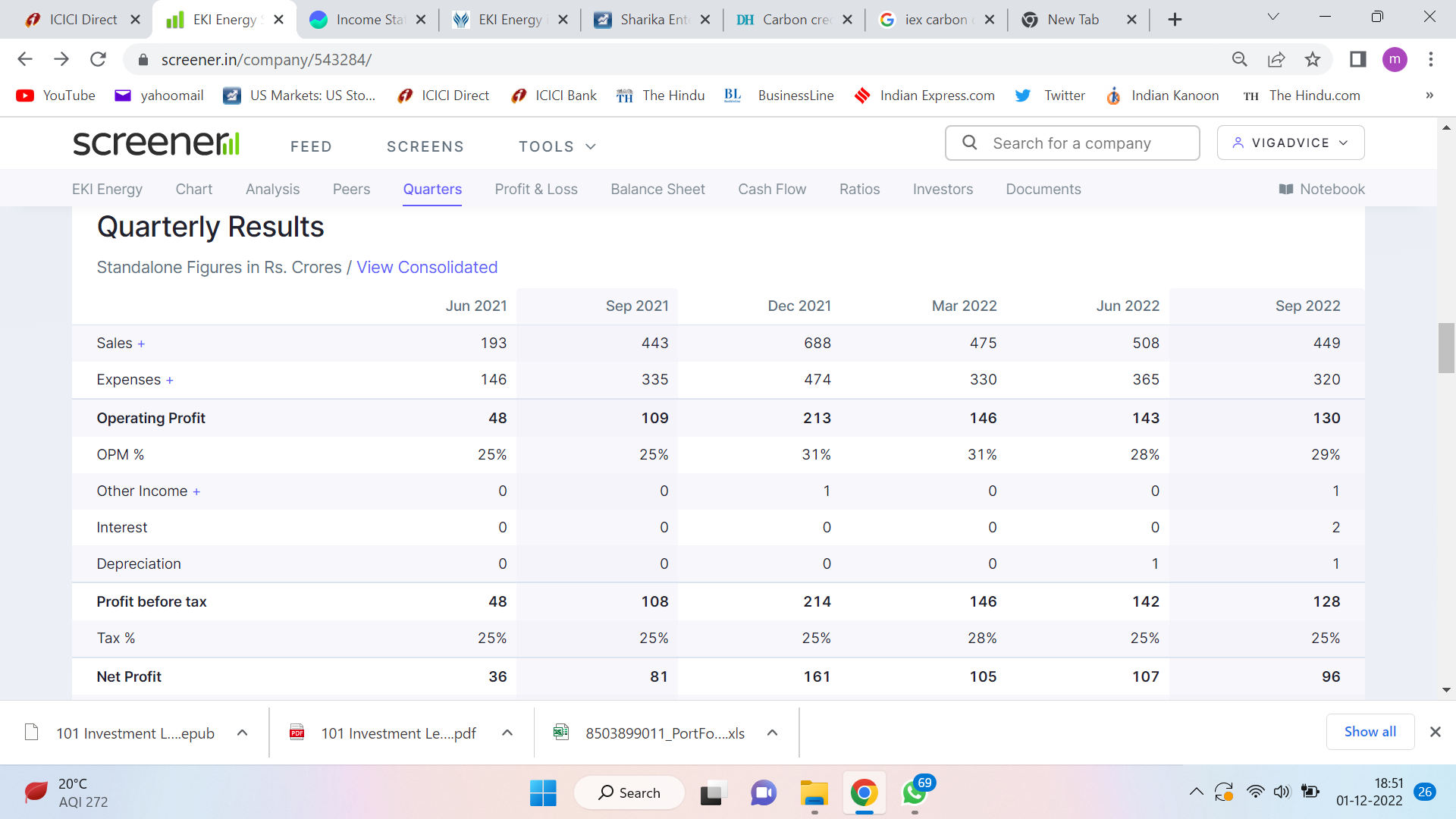

Could you help compare the volumes of credits sold in this Q, last Q and the one before that?

-

If I look at the CBL nature-based offset prices, our revenue trajectory is mirroring the euphoria around COP26 and the subsequent fall after that. And if I look at the current month, the prices are on a further downward slope. So can you help understand the reasons for such a sharp correction in prices? Is the market evolving for higher quality credits? Or taking into account additionality?

-

Could you help understand what will be the vintage of credits we’ve sold over last 1 year. As in, on an average when did we acquire those? Also, how many credits have we purchased in the last 6 months, what is the total inventory currently with is both in number of credits and the value.

-

Are we currently working or planing to work on some projects that involve CCS technologies? Not nature based, not emission-avoidance but technologies that will either have a direct impact like Carbon Capture and Sequestration from say cement manufacturing plants or will have a much larger neutrality push…

— Could you highlight the geographies for the same?

-

What would be the liquid portion of current assets on books? And what will be the quantum of receivables currently?

-

The Compliance Market is quite mature, structured and is exchange-traded. And country wide or industry wide emission norms can directly be incentivised via ETS quotas over there. So, in turn even for the newer cutting edge tech that’ll eventually take out carbon off the supply chains. It’s a possible and more efficient mode of funding than VCM by far… the market size is also incomparable. So, it is very much understood how ETS is being able to work with good liquidity, stability and price discovery because the structure has come about due to conscious deliberation and mandates. But for VCM, one thing is obviously, the ESG end of things. Which is looking in the direction to attract capital for companies or industries that will pollute less or be neutral or negative going forward . But I don’t see price stability and actual value being created unless there’s some formalisation and structure to even the VCM market. Because right now even experts don’t understand how credits should be priced. So, firstly what’s your opinion on it and what risk do you potentially see going forward?

-

If VCM credits get standardised/formalised, would it limit our business potential in revenue share by trading, and restrict us to advisory/consulting services?

-

What makes you think that the price shouldn’t go much lower from here?

2 Likes

Some resignations happened couple of days ago.

Resignation of Statutory Auditors

Resignation of Director

1 Like

2 Likes

Shakira Enterprises is available for ₹7.50!

The share has come down from the dizzy heights of ₹3100 in Feb '22 to the ₹1421 level today. I have gone through the thread carefully. I am not so knowledgeable about either the financial markets or carbon credits, but what comes out is that there were allegations against the company. I am not sure any fraud has been proved. Proved not in the sense of criminal law, but in the sense that it has shaken the confidence of its existing or prospective clients.

In one of the comments at the concerned UN site, there was a mention that EKI had been banned by NHPC. I went through the NHPC banning list, but have not come across this company.

To me a few facts are clear. Its PE is: 8.35, and the ROCE and ROE a mind boggling 236% and 176%. That means it is still one of the cheapest stocks available.

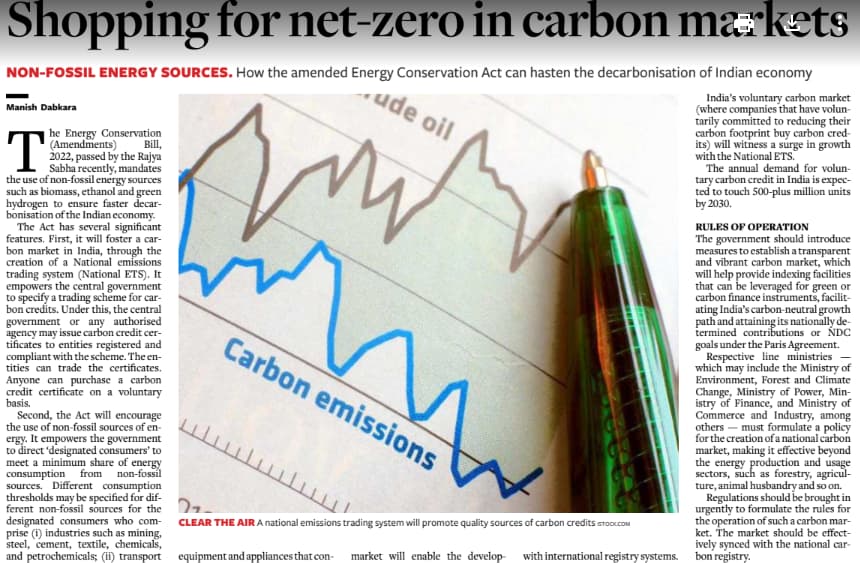

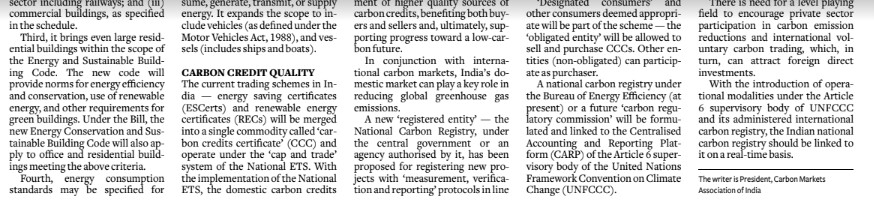

Secondly, carbon credits are not going away in a hurry. Environment is top of the agenda in the west. “In the past, India has made investments in producing carbon credits and exporting them to international enterprises. Between 2010 and June 2022, India issued 35.94 million carbon credits or nearly 17% of all voluntary carbon market credits issued globally. The market for carbon credits increased by 164% globally in 2021. It is anticipated to reach $100 billion by 2030.”

Carbon credits and India’s carbon market | Deccan Herald

As for other companies, IEX project is still in future.

Sharika Enterprises share is at ₹7.46. Moneycontrol shows its EPS at zero.

The profits have reduced a bit, but it is not as if the company has crashed. To my mind, it provides an opportunity to buy.

I have made some investment in the share today, tempted by the quotients quoted above. It is not a recommendation, but like trying to convince myself that I have not made a fool of myself.

3 Likes

According to latest quarterly report Sharika Enterprises Limited has only two subsidiaries:

- Sharika Lightec Private Limited, Subsidiary Company

- Elettromeccanica India Private Limited, Joint Venture Company

Sharika Green Infra Private Limited does not seem to come under the listed company.

2 Likes

BL interview. India will need $800 billion by 2030 to meet COP26 RE capacity commitments

Commending India’s efforts in transitioning to clean energy as part of its pledges at the COP26, World Economic Forum’s (WEF) Head of Energy, Materials and Infrastructure Programs, Benchmarking and Regional Action, Espen Mehlum said it is an example for countries. In an interview with businessline , Mehlum said the country will require around $800 billion by 2030 to meet its renewable energy (RE) commitments.

, CMD & CEO, Manish Dabkara In Talk With Anil Singhvi")

The stock has been going down. Hopefully, the expectations that the new push to environment issues helps it recover.

Great work Krishna, I really like the way you asses people & company. Keep the good work coming!

1 Like

https://twitter.com/BeatTheStreet10/status/1624069911583809536?s=20&t=zJFQSQvChbxUWZ33S9RX4Q

Auditor has given a qualified report regarding non compliance with IndAS 115.

4 Likes

Would like to request VP seniors to highlight the reason for free fall in this script.

2 Likes

Why this company has still not published March quarter results. The auditor raised red flags are still a problem? Why there is reduction in margins, is this a cyclical business or new compitition emerging?

1 Like

What’s the rationale behind buying Sharika over Eki?

There are several reason of the fall owing to uncertainty in carbon market, global price fall in carbon credits, the company’s (eki energy) audit comments etc. The risk reward looks interesting at this juncture with so much negativity around. The Indian carbon credit scheme may be out in 2 weeks as per the recent news.

For more read you may go through the thread I posted on Twitter. Thank you!

https://twitter.com/suryrus/status/1667955342842687489?s=46&t=p8qpu3YrffRKhnSgqAHl2Q

CMD Manish dabkara of EKI energy

#BadNews for #VCM (Voluntary Carbon Markets) - A number of major carbon traders/investors like @EKIEnergy are finding that offsets they bought/invested may now be having less worth / valueless.

Series tweets from CMD here :-

https://twitter.com/manishdabkara1/status/1695776317772300551?t=kmKfE30K-PV4XH_dRf1zwA&s=19

2 Likes