I had been watching this company share after listing, did not give an opportunity to enter into and had reached to 5 fig in 9 months! Being knowledge expert from similar field and expert, I wish others also to shed light on this. The recent news/fact is they signed MOU with Shell. But as a business its not a new one, the way its MD and team is saying on media or as EKI as global leaders! I listened to Mr Manish also. Developed countries already have several Carbon credit and capture consultancy since more than 10 years now. Also its pride for us, that some Indian company is going ahead. But concern is about its ramped up price, and many are here to understand it.

8 Likes

Interesting story, too early to estimate right now but the valuation of this company will be derived from the JV with Shell where it will own a 51% control and Shell is pumping billions of dollars in the JV in next 5 years. With 50 lacs shares and mostly tightly held by individuals, it seems it will become a kind of holding company in the future.

Would really appreciate if the opening post could be more detailed about the company, what’s happening etc. It makes the overall discussion richer for forum members

1 Like

Exactly, the article also talks about Carbon business since more than decade. Why there no major companies from developed World in this yet? It itself tells the story. Rising on wave after listing and riding on news of Shell can be one strategy. But the way it has gone up does not digest to any one. Its still a concept business. India has carbon credit every year and its being exchanged by several other means or traded in exchanges, and it was already been exchanged till date. EKI business model is still not clear to many. Its a good book story still. This is consultancy also, where they may try to sell Shell technologies to companies in India that can gain Carbon credit once implemented. They have global offices, so they should share all their past client records also very clearly. Now that goes a long story. Hence, unless we see something on ground in India, nothing can be predicted, where as, its promotors keep coming to media giving interviews this is not good sign. Anyways, its not a recommendation or any decision. This is just opinion

2 Likes

For such companies, before studying the Business Model, it may be useful to do a check on the Promoters and their credentials.

The economic times article says a formal announcement will be made, post which the share prices moved up.

Has a formal announcement been made in the first place ?

2 Likes

I watched Mr Manish interviews on social media channels like you tube etc. Imp is they have made their own channel on you tube and publishing their rise and success videos! Check the link plz. Also he was invited ( can manage many such invitation by sponsoring!) on 30th Dec at one of the IIMs to share his success story ( Entrepreneurial Webinar | Climate Change | EnKing International | IIM Indore - YouTube) . He speaks nice and has good knowledge and vision also. BUT - The numbers he said from past history are really doubtable. Number of clients across the globe etc, business numbers forecast etc… So, it will be really interesting. He already said, Shell has 49% in it and the money will come in next 3-4 yrs in installments. You see his age and his experience etc- that is another aspect. He was found shaky to reply some queries like- How you choose your client and what is method of delivery? etc. etc…

5 Likes

This company is on my radar since June-2021 for its highest ROE. It was not available to be purchased in an affordable range from then for me.

It is an SME, when I saw close to 8Lakh was the lump sum to be put for one lot. I did not like/understand the business model, valuation but investors citing it is the future of carbon credits trading.

-

When I searched in VP about this company, a fellow member wrote about the luxuries enjoyed by the promoter with the company’s money. That’s a small red flag to me.

-

On further searching, for this type of company only the promoter[single person] seemed to be qualified for the entire operation.

-

The company has only one small office in Indore. All the google reviews of this company seemed to be written in a span of 1-2 months near IPO. It’s a red flag for me when a company is in operations from 8-9 years, there are suddenly reviews popping up in a month’s span. Paid/Forced reviews may be. I have my ways of judging this.

-

Then I saw some interviews articles of promotter, where he discusses the stock price & valuation at least twice. Big red flag for me.

As I learned in VP forum, he must not be concerned about driving the stock price. A similar discussion took place in the recent IIM Indore interview, he was proudly correcting the professor “today the price is 7500”. I thought this guy will never change. Of course not my problem. -

Fellow members may think that, since I missed the opportunity, I may be talking like this. No, it is not my intent to bad-mouth the company. But the amount of return & valuation are too good to be true. Hence, I am watching this drama. I am wondering and learning how the market is valuing this company. Also, I am worried about the newbie investors & crypto gang may come and stuck in this. Now and then this stock surprises me with its continuous upper circuits, hence the research interest.

-

At some point of time, when I got ample time, I was reading about COP26 related stuff, I stumbled upon a website of United Nations which is UNFCCC. It seems the renewable energy companies have to apply for the carbon credits through UNFCCC. EKI facilitates this process. But when we see the number of results EKI gets featured on this website, I thought I really missed a gem.

- Then when we go through these results, the projects are kept for public review/ hearing & commenting. Some whistleblowers claim the working of EKI is not at par or they fake the inspections with another company. You can read the comments in the below links. At some places, it is mentioned that they blindly copy-paste the wind project work to solar and vice versa. I am not going into technical details. I don’t want to know also.

https://cdm.unfccc.int/Projects/Validation/DB/MU8WYEJ8PJ3MAOLNE6XHE1KT88M2BO/view.html

https://cdm.unfccc.int/Projects/Validation/DB/9OMLHY9027IFVJ4V85YZBZLPUQ2AHU/view.html

https://cdm.unfccc.int/Projects/Validation/DB/NZVTU9A35C4238QPB1NO64WZCYRWBB/view.html

Do go through all the above links[Just takes 5 minutes], read comments, You will understand to some extent.

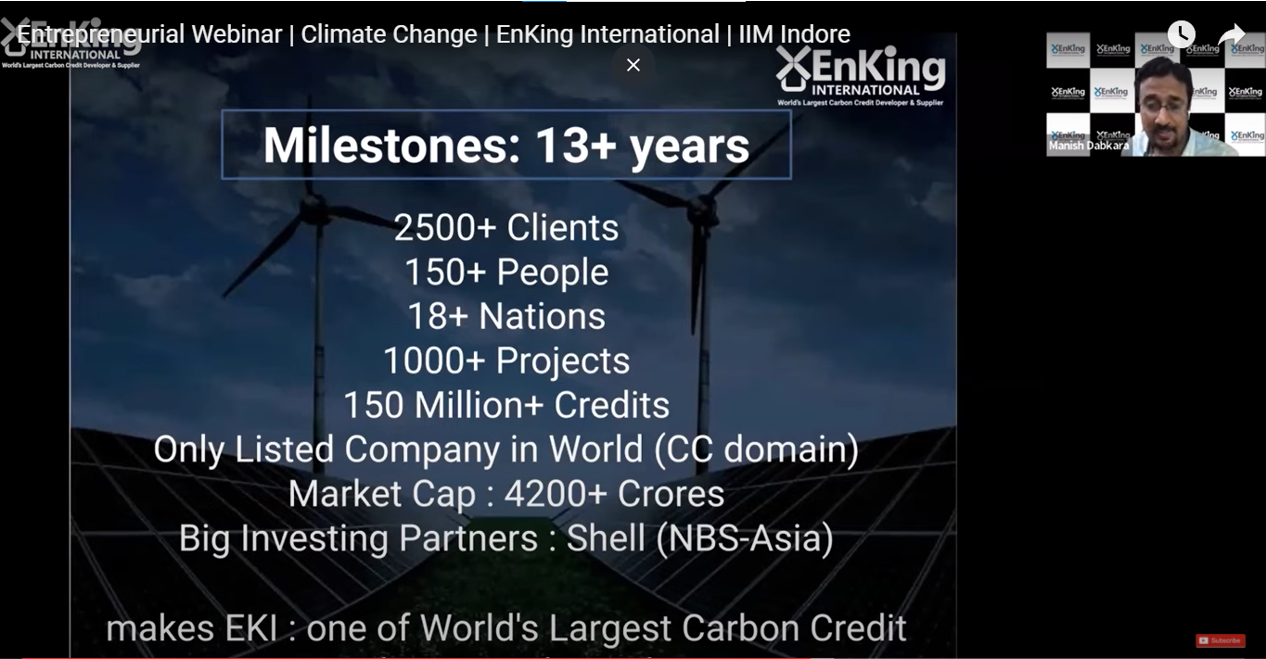

- I saw the interview given to IIM, Indore. The following is from the slide deck.

-

How can the client’s number be more than the projects number. Every client will have at least one project. I may be missing something. So he wants to say 150 people are sufficient to handle 2500+ clients & 1000+

projects. Each employee irrespective of thier skill, experience & knowledge handling 16+ clients.[!!!] -

Also the numbers keep changing, in the next 2nd minute of this video he says 700+ projects, this slide he says 1000+ projects.

-

We could see @sasodekar ji’s comments in the video also.

-

I have just glanced at the Annual report, full glossy with quotes from eminent personalities completely unconnected to the theme and company.

-

In the conference call transcripts, while the analysts and investors press for clear detail of how revenues are made the promoter skips the question and requests he will come back with more detail. CFO was absent during concall and he tells CFO will have to answer the questions raised.

-

This company never stops to surprise me, As of this writing when I searched in youtube, I found the promoters TEDX talk[which can be arranged easily with contacts, connections and money may be]. See it from the first, This man is reading the slides in the guise of a TEDx Talk. Have n’t seen such a talk in the recent past. Sorry to write like this. But Caveat Emptor. I have my way of evaluating people, things, stocks etc.

I have enough red flags for me. ![]()

![]()

![]()

![]()

![]()

![]()

Now I am watching, how this unfolds.

Disclosure: Not Invested, Not interested to invest for now.

43 Likes

This EKI story is very hard to believe. Precisely for the same red flags, I too stayed away. IMO, this is turning out to be another Ruchi Soya kind of rally where the stock prices may be controlled within a closed network? Only time will tell.

2 Likes

Great detaling Krishna and thanks for your deep drive and sharing links. Yes we do not have any critics if company is really doing well or does well in future. But yes, as of now even I was thinking like FOMO… but its very much clear to me, there are lots of visible stories or stocks on board to park your hard earned money. Thanks @Valuepickr forum for opportunity to share such discussions.

2 Likes

For now let us all be spectators to its future. My point is no worries of missing such opportunities, where we could not build our conviction. Many lucky investors might enter at low levels and come out unscathed. But when we don’t have sufficient conviction or understanding, let us not be in that business, however good it may be. Thank you.

1 Like

If the intent of this thread is to feel better that there are others as well who share the FOMO then hope the objective is being met !

Merely the price movement can’t be a barometer to criticize a company, after all the Price rise of Bitcoin got everyone to be aware of cryptos!

Most importantly the co. provides a service to the clients to monetize the benefits of not polluting the environment and possibly this massive price rise is a signal as to how mkts view ESG enabling cos in general for the coming few years…Hydrogen, EV’s, Solar power etc…and like EKI those cos would also set aside fundamentals and have a crazy run-up for few years to come.

All in all it makes sense to connect behaviour of EKI with other cos in the broader ESG domain.

2 Likes

Probably it may be a small factor not 100%. As FOMO happened with many in these 18-24 months for many stocks. However, the way such stocks work in circuit to circuit, there the concern is high. Sometimes poor investors get trapped at highs or so… and when story gets down due to any reason, then the worst hit goes with retail investors. It is also discussed well that its not a new business, and available very well in unlisted space across the Globe. We are trying to connect on abrupt rise w.r.t. even management coverage here. Else, its always a matter of pride for us to have any Indian company become Global leader. They have just expanded in Middle East also with new office, so as things get more visible with numbers and assets with good governance why not, market will offer them good valuation further also. Else environmental concerns, Kyoto, and Net Zero or something else keep coming and Nations sign agreements, and it goes on. But note that currently its trading with very low volume also, and such stories may also become candidates of take over in future if there is sustainability.

2 Likes

Q to folks who track this story closely:

- What’s the Major change in the business? Inventory used to be NIL in FY21. But, the same is now amounting to 81 Cr. in H1FY22.

Disc: Just academic interest.

Just glancing through various stocks and it appears BSE listed Sharika Enterprises Ltd has recently formed a new company called Sharika Green Infra and it intends to do very similar line of business (Carbon Credit, Renewable Energy Credits, Climate Change Consultancy) as EKI Energy. So, it looks like now new players are entering this segment. Already Sharika Enterprises has good client list and this Sharika Green Infra may ride the Carbon credit theme.

3 Likes

I came across this company today and what a story. I went through the investor presentation and company grew multifold in term of revenue and other stats.

Coming to the Carbon credit, it is a global story. e.g. see below news. Companies like MicroSoft are spending lot of money to buy carbon credits since their data center emits lot of CO2. EKI is also benefiting from this story since this seems the only listed company in this space. Lot of countries and companies have committed to be carbon neutral by 2030 or 2050. Hence I see this company growing.

In case above article ask for login, this information is available on other url https://www.cnbc.com/2021/09/30/microsoft-calls-for-more-investment-in-carbon-capture-technology.html

On Thursday post market, there was a news circulating in social media about the company bagging order from ISCDL. But the company disclosed to exchange of the same only on Friday noon. Just wondering how come the price sensitive information is being circulated in social media in advance?

1 Like

seems more competition?

2 Likes

My Anti thesis on EKI ?

Experts see renewable energy’s 2021 rally as a “last hurrah” in voluntary carbon markets for some regions

2021 may also mark the peak of renewable energy (RE) as a major share of the carbon markets, for projects originating in developed countries. RE volumes rose from 42.4 million credits in 2019 to 80.3 million credits in 2020 and remained steady at 80 million credits in 2021, making it the second-largest market category after Forestry and Land Use. Prices for RE credits tumbled from $1.42 per credit in 2019 to $0.87 per credit in 2020 before rising to $1.1 per credit as of September 2021.

“A surge in transactions coupled with falling prices is consistent with a shift in renewable energy credits coming from Asia, now that the financial additionality case is harder to make for RE in developed countries,” says Maguire.

All carbon projects need to demonstrate “additionality,” meaning that they could not exist without carbon finance, in order to sell credits. As renewable energy becomes increasingly competitive with other forms of energy, as it has in developed economies, it no longer needs carbon finance to survive. “RE projects may continue to meet additionality criteria in some places such as less developed countries,” Maguire says, “but particularly in developed countries we don’t expect to see significant new supply in the coming years.” https://www.ecosystemmarketplace.com/articles/press-release-voluntary-carbon-markets-rocket-in-2021-on-track-to-break-1b-for-first-time/ So RE volumes draining down the VER prices/volume shall come down. Flow of certificate from Forestry seems to be black box to me

While I agree to what members here have posted and it’s easy to conclude that EKI doesn’t have best business practices. But what I am confused about it is operating cash flows. If the projects are fraud then from where is the company getting cash flows from?

What is your view now?