For anyone who wants to have an idea about how does the business of flex space works can refer to this pdf which I am attaching. Have explained it in very simple terms for better understanding, still any doubts, feel free to drop the questions.

Co-Working Space Write-up.pdf (401.6 KB)

6 Likes

2 Likes

Same space as EFC

I could not understand promoters till date …they do merging - demerging etc…

Hi,

I am new to this business. And I don’t understand the below para from latest concall. Can someone please help me

We met EFC Management and here are the takeaways:

- Owned Space: 2.5 million sqft, Leased Space: 250,000 sqft

- The company operates most of its portfolio on the straight lease model.

- None of their properties are run on the revenue sharing with landlord model.

- The company has comfort of customers for new office spaces owing to its superior area expertise and lead generation team.

- The company distinguishes itself as a player which focuses on maximum returns out of a specific office space, its priority remains squeezing more seats into available areas while not compromising on modern amenities like cafeteria, recreational areas.

- The company aims to focus its spaces on Pune, Hyderabad, and Noida/Delhi NCR areas.

- The company is confident of maintaining its 90% occupancy levels for the future, they intend to initiate projects only after 90% of occupancy is confirmed by clients.

- Their Design and Build Division: Whitehills Interiors, benefits from Pan India network, positioned to service global clients across the country, the business involves high customer stickiness. Management indicates high strength in upcoming D&B contracts with A Grade Clientele.

Basically, if there’s AWFIS on one hand making office space with more focus on aesthetics and new edge features. EFC focusses more on seat number expansion in a specific area, while maintaining a balance of new edge features like cafe’s, leisure lounge etc.

8 Likes

can anyone analyze the results I am seeing good numbers but was not able to join concall pe after result is 23 odd but stock has corrected by 12 percent intraday just the market mood or something else ?

1 Like

I also felt the numbers were decent and furniture business coming online feels like a strong development. Maybe markets are overreacting to the topline growth being tepid yoy. Not sure.

EFC I Result Update Q3FY25.pdf (784.9 KB)

Even at a 50% revenue growth, it is on track. When mgmt mentioned 100% growth last time, it was assumed to be far fetched.

2 Likes

Everything is justified in bull market while everything is questioned in a bear one even good news are sold into

4 Likes

Last year same qtr had a trading rev worth 47cr and they stopped doing this 2-3qtrs back which is why rev looks flat remove that 47-50cr rev from q3fy24 and rev will be 125 and q3fy25 rev is 180cr

He said that bcz he wants to underguide and he said conservatively they will achieve 690-700cr rev with 140-145cr pat in fy25

Thats 100%+pat growth

And 70%+rev growth from fy24 numbers

In fy26

- furniture factory rev will start kicking in on full pace

- reit structure will also start kicking in which will lead to higher pat reasons explained in the concall

It’s currently trading at less than 20 times, yet the company has one of the best structures in the industry—both in the listed and unlisted space. It’s a fully integrated business, spanning from property ownership through a REIT structure to in-house furniture manufacturing.

By employing a REIT structure, the “landlord” layer is effectively removed, and associated costs (e.g., electricity and administration) are borne by the REIT rather than by EFC’s books. In addition, the company earns management fees for overseeing the assets, which should be on par with its current rental income but with significantly lower expenses than operating outside a REIT setup.

Given the company’s high level of integration and its valuation at less than 20 times earnings, this appears to be a bargain.( on fy25 numbers)

And a co growing at such a pace trading at these levels

Sage one has increased their stake aswell.

Disc: Biased and invested

I can be wrong these are my assumptions.

5 Likes

Hi everyone, 20% value erosion when the results were not that bad (in my expectations) seems too much especially when the stock is available at cheap valuations of <20 forward PE. There must be a reason why Awfis trades at a multiple of >20 EV/EBITDA whereas the market participants feel that the PE of 20 for EFC is expensive. Is there something that we are actually missing? I think market can’t overreact to this extent. Views are welcomed !

Disc. for now & further comments: Invested , biased- don’t think so.

3 Likes

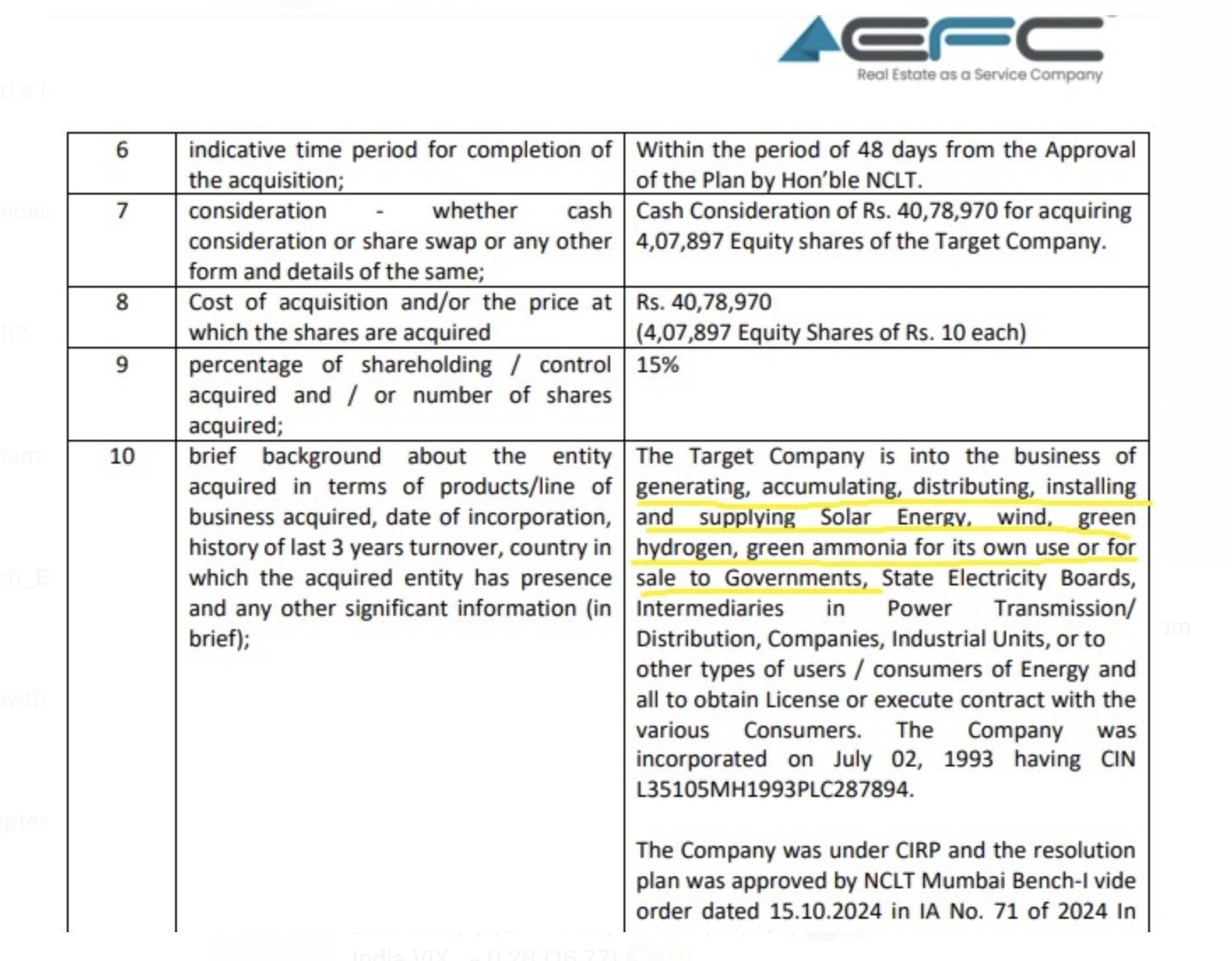

regarding MPF 15% stake:

The Target Company has been acquired through the Corporate Insolvency

Resolution Process (CIRP). MPF Fire Systems is into the business of generating,

accumulating, distributing, installing and supplying Solar Energy, wind, green

hydrogen, green ammonia for its own use or for sale to Governments, State

Electricity Boards, Intermediaries in Power Transmission/ Distribution,

Companies, Industrial Units, or to other types of users.

Company says they are positioned as a strategic investor in MPF, they don’t

intend to participate in the management. Management aims at creating

synergies as it would bring down operational costs for office spaces.

I remain bullish on this counter and continue to stick with my target. Based on my initial projections, I had estimated a PAT of ₹92 crores for the year, which has already been achieved by Q3. Keeping that in mind, I am conservatively targeting a price of ₹1040 by FY27, assuming continued growth and solid performance. The recent pullback can be attributed to the management’s revised guidance, which lowered the revenue growth forecast from double digits to 50%. However, I had factored in a more conservative 40% topline growth for FY25, which still seems on track, with the company having already reported ₹450 crores in revenue through Q3. Looking ahead, I expect the business to grow by 50% in FY26 and 35% in FY27, which supports my positive outlook for the stock.

Here is my report backing my views :

4 Likes

EFC has announced a joint venture with pepperfry for their furniture business.

1 Like

EFC operates in the real estate as a service industry. It has three business verticals:

- Managed offices: It mostly works through a straight lead model here, wherein they take an empty space from the landlords, carry out the capex and then lease out the offices to their clients (corporates/ startups).

- Design and Build: They have a team of architects and interiors to design and build the offices according to the client’s taste.

- Furniture Manufacturing: In order to backward integrate, they have started this division which has commenced operations this year.

Now, additionally, rather than renting the properties from their landlords, they want to start buying the properties. They plan to do so through following ways:

- REITS: They have set up a REIT, whose investors will be funding the acquisition of the properties and getting the yield from their investment (little higher yield than a commercial real estate investment). EFC will be the operator and hence will take the operating and managing fees from the REIT.

- Instead of renting out properties, they would take debt, so instead of rent, they’ll be paying EMI (paying towards building an asset).

INDUSTRY:

The industry has been witnessing huge tailwinds in the past few years, where not just start ups and individuals are enjoying the benefits of co-working space but also bigger corporations are shifting to managed office models. So, let’s understand in detail what does this model have to offer to it’s different stakeholders:

A) For Clients:

- Start ups: Co-working space gives them a good infrastructure where they don’t have to take the time out in handling anything other than their own work, at affordable prices plus the flexibility to add more people to their organisation at a much faster pace which otherwise is not possible in a traditional office space.

- Corporations: Here, what operators like EFC do is they allot them the entire building/floor/space depending on the size of the client and the entire space is designed according to the client’s specific requirements and is managed by them as well. So here, what happens is that the operator carries out the capex and is able to build the infrastructure at a cost much lower than what the client would have been able to do on their own and it also gives the client the benefit of staying asset light.

B) For landlords: a fixed rental income/ share in profits (depending upon the type of model), higher visibility of income for next few years, the luxury of dealing with a single client (landlords just have to deal with the operator vs so many individuals who they would have otherwise rented out the space to).

MANAGEMENT

Now, coming to EFC management. They started the business 10 years back and have scaled it fabously while being profitable. The management sees it as a commodity business where only the most efficient players can survive and grow. They believe in bringing efficiencies at both the capex and opex level and have clearly demonstrated themselves as champions in doing so. EFC’s cost per sq feet is 1250 which is amongst the lowest in the industry. They don’t just want to remain managed office player rather want to be seen as a holistic player in the industry and hence are integrating into design and build and backward integrating into furniture division as 60% of their capex cost is furniture and fittings. Management believes this will bring in further more efficiences. Overall, the management seems to be a growth hungry and competent management.

So, while there are no entry barriers in the industry but the scale at which EFC operates with the level of efficiency in terms of capex and opex, it is very difficult for a new entrant to establish that. Directionally, business is going in the right direction wherein with D&B division contributing more plus with REITS thesis playing out well, it will lead to better ROCEs, a more diversified business, more efficiencies and hence higher margins and a more stable source of supply.

My thesis is here is that we are getting one of the most efficient players in such a fast growing industry at very reasonable valuations (25 times P/E) plus the optionality of REITS.

REITS: The benefit of REITS will be that EFC will have easy access to capital and hence can grow much faster while making the supply chain much more stable for them as they will not have to depend on the landlord to renew their lease after 5 year period. It can even lead to much better ROCEs in the future if pans out well.

The major risk I see here is slowdown in economy and commercial real estate. Additionally, we will have to see how the client diversification pans out as currently EFC is mostly focused on IT where we already see a downturn in the industry where the leaders such as Wipro showed degrowth.

Source: EFC concalls, management interviews, Neeraj Marathe video on co-working spaces.

5 Likes

Can members throw some light on below points @manhar , @sahil_vi

-

Given so much crowd of co-working companies , will supply outperform the demand thus decreasing the margins ? Literally lot of startups are visible nowdays , even sharktank also featured one of it ?

-

EFC is backwardly integrated , that is making its own furniture . they have factory in pune . So is it viable to send that furniture to delhi NCR or deep south in banglore ,chennai given the cost of logistics ?

-

Given the freelance culture , WFH and AI co working can increase but big players may suffer problem , bec in tier -2 cities supply will be infinite and as such model of coworking has no moat in itself?

DISC: invested and biased and scared

2 Likes

answer to qn no 2.

yes, they send furniture to other states in India, one of their orders include sending furniture to Hyderabad. As of now, they do not accept small orders.

Another subsidiary formation !!

Kindly someone explain why EFC(I) forming such subsidiaries and diluting equity. Why they can not do the business through EFC(I) ,which they want to do through subsidiary, instead of forming EFC(I). What’s benefit to shareholders? or it is for benefits of promoters!!

3 Likes