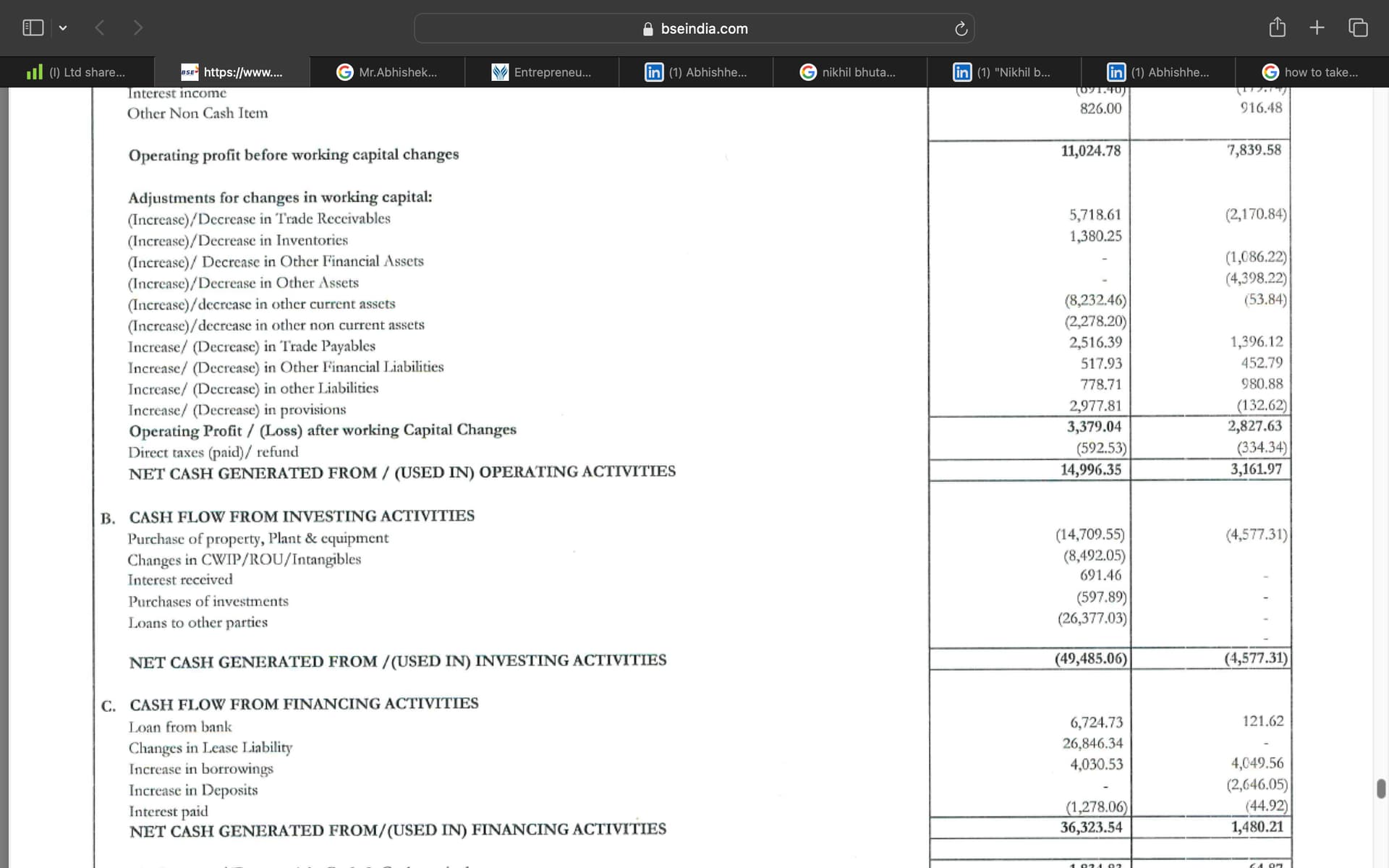

can someone help me to understand following 2 figures in cash flow statement of sept 24.

- loans to other parties - (26,377.03)

- Changes in Lease Liability - 26846.34

can someone help me to understand following 2 figures in cash flow statement of sept 24.

If you are interested in this space, please do watch the documentary on We work

One of the main reason of its earlier collapse was the huge asset liability mismatch and exponential but super aggressive growth on unsustainable lease terms.

Companies in this space working on Straight lease model with supernormal growth will suffer one day.

We work had big corporate governance problem as well, I am sure if somebody would do some google they would find , as to how promoter was building wealth form himself. +

They expanded to various unrelated industries like We live etc etc , on the other had we have EFC one of the most prudent spenders with the highest profitability in the industry. Not a fair comparison at all

EFC as on date is not into just coworking they do D&B and furniture as well do we have 3 verticals.

The most important part is they are the only company to get SM REIT approval of 500cr and in SM REIT I have to bring in income generating properties so EFC existing properties would be put in here. The real estate cycle right now is so strong that if we don’t have a problem for the next 3yrs we don’t know what the mix of EFC would be at that point

As per my understanding maximum would be bought in REIT, there I am replacing the landlord so where is the question asset liability mismatch?

The promoter also prudently wishes to use debt as explained in my earlier post.

This industry is not about SL model or MA model it is about balance sheet strength EFC has the best balance sheet in the industry today, I mean at least 5-10 coworking players equity we will have to add to reach EFC equity

The meaning of balance sheet strength is every body will die before me and I will be the last on to die, I think if they are smart in a crisis they significantly increase their market share as all small once would die no doubt.

All the above are just concepts and nobody know how this would pan out all boils down to promoter execution capability and how profitability you can build the business

The only thing I am sure of is EFC would be among the last ones to die

can be wrong, thnx

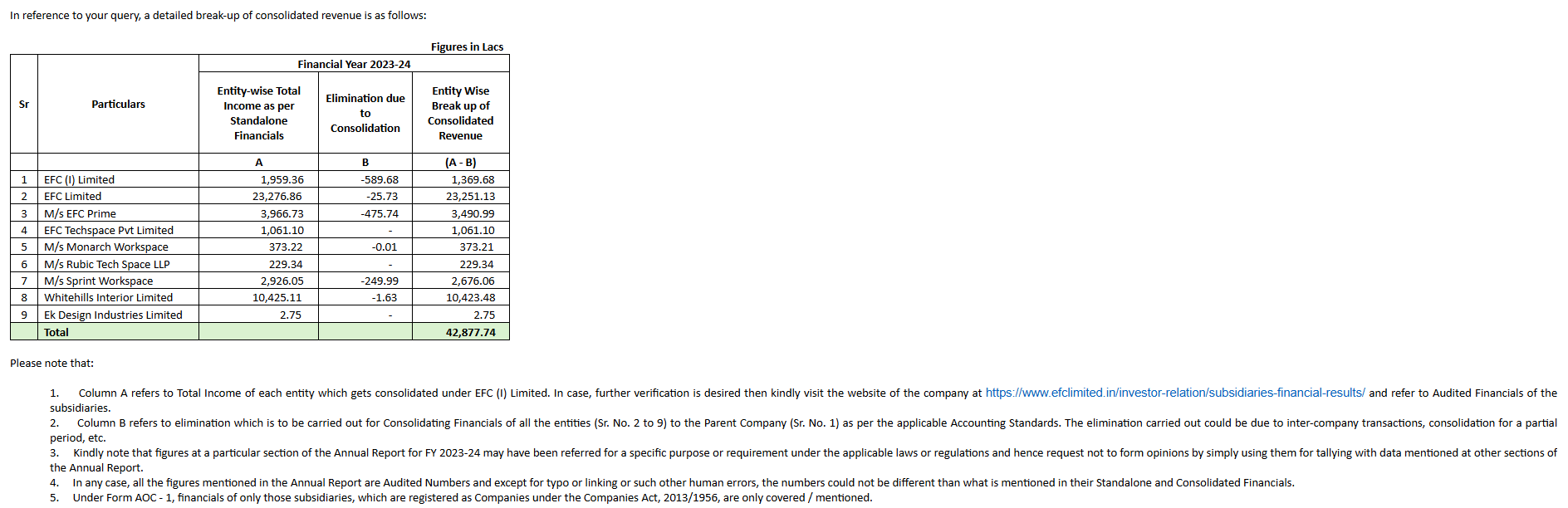

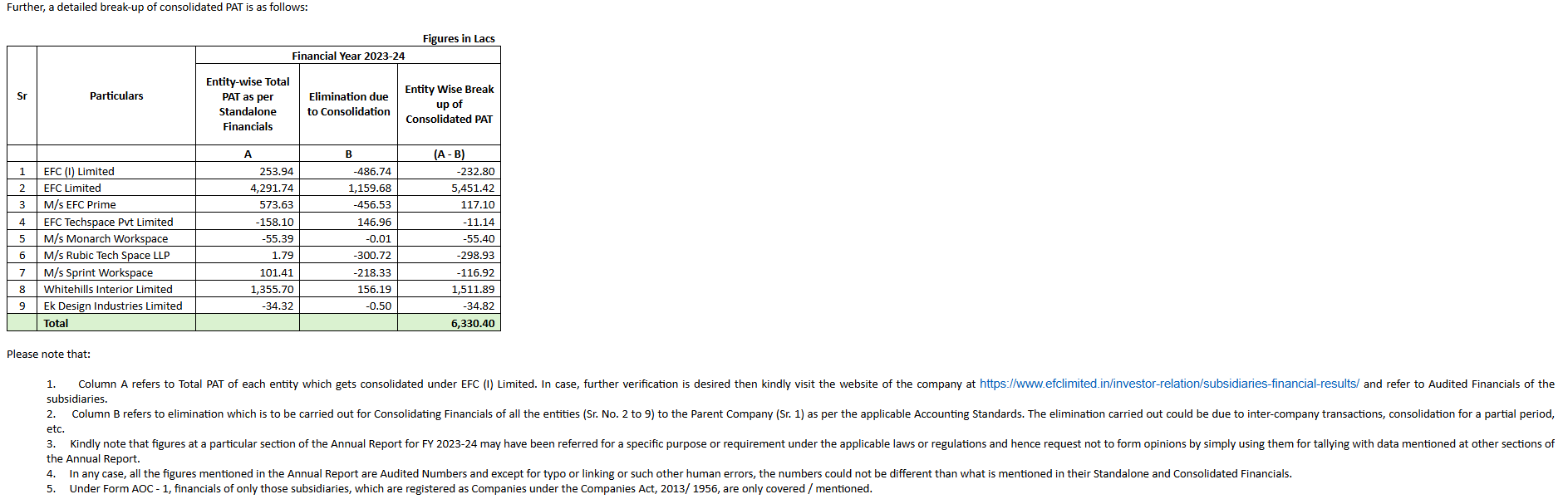

I have sent an email to the company with similar queries and have also asked them about the total number of employees working with the company. I have received a response for the breakup of revenue and PAT numbers. The question on employee count was not answered (may be missed). Below is the response that I have received on their numbers.

Will shareholders of EFC get equity allocation in SMREITs when it gets listed ?

No they wont, the SM REIT will raise funds separately.

The benefit to EFC will be that the properties purchased by SM REIT will be managed by EFC at similar margins, but no risk of landlords/property availability as the SM REIT becomes the landlord.

FY-24

Some concerns:

Discl: Invested.

EFC I LTD Report (BUY).pdf (1.3 MB)

I estimate a 70% upside based on 2027E earnings, open to feedback.

Thanks Sagnik. Is this report written by you?

This report looks good and decent, but FY26e is too low, I mean less than 190 Crores PAT for FY26 but 140 Crores PAT in FY25 doesn’t makes sense, cuz it will be less growth as Furniture unit with 40% margin will be coming at that time

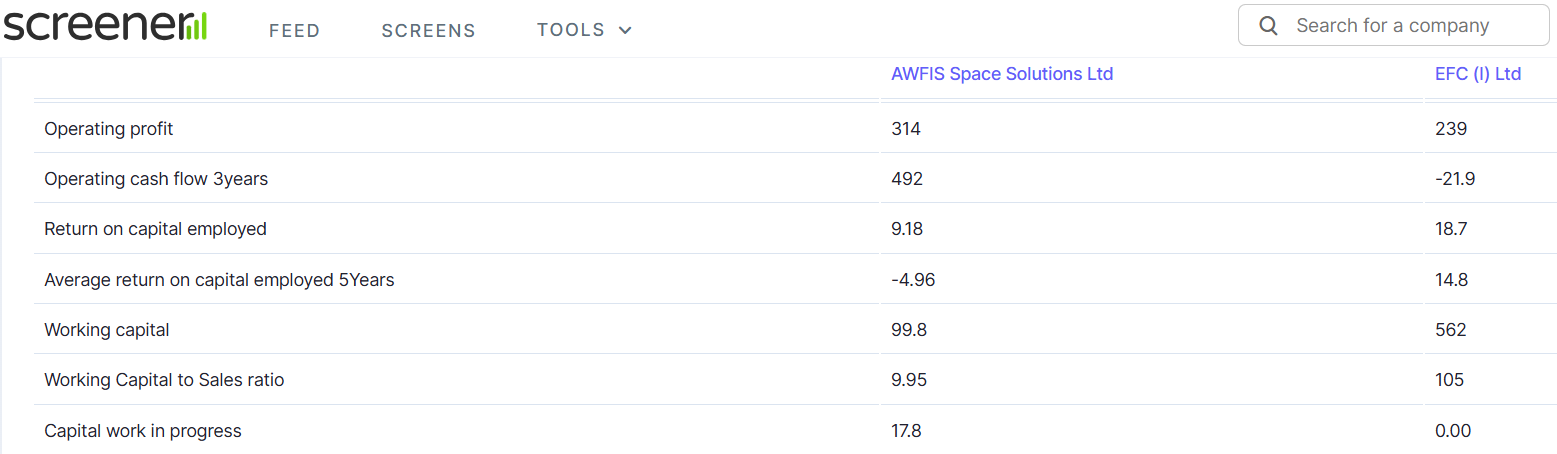

I tried to compare AWFIS and EFC(I) : I could not understand below disparities -

EFC is doing good on operating profit but very bad on cash flow generation. Most of operating profit locked in working capital ? There is no capital work in progress. So where is the operating profit going? Is the profit real ?

check out the cashlows in h1 numbers fy25. company reported very good cash flow from operations

Disc- Invested

Awfis is a loss making cash burning business. It’s very easy to show growth in co-working business it’s a comodity business.

AWFIS space has a 5year cash flow exceeding ₹500 crore and operates as a net debt

free entity. It is not a cash burning company and has successfully grown its assets without significant equity dilution or taking on additional debt.

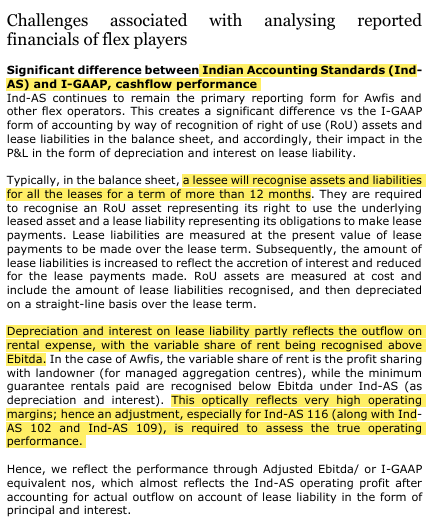

Hi, sorry to bother you. Just seeking a clarification - in the accounting standard under use (Ind AS 116), AWFIS has to split rent under Depreciation and Interest costs (since it is treated as a Right of Use asset).

So when they add back full depreciation and interest cost to the operating cash flow statement, wouldn’t that mean that their actual cash flow is significantly different from when that gets reported in accounting?

I am not able to develop conviction on promoters -

Too many related party transaction, CCDs, QIP, all means of equity dilution. Now this is new, can anyone explain it - please!

People who are comparing with AWFIS, need to consider the corporate financial governance as well…that way, Awfis will always be at a premium…if I am not wrong

You can’t compare Awfis with EFC directly because office is more into flexible workspace and operates on a managed aggregation mode. Basically, it means that it’s customers are small startups, professionals who pay rent up front so it should have at an ideal stage, a negative working capital cycle.

Whereas main clients of EFC are enterprises which have bargaining power because they sign long contracts and don’t pay upfront. Here, the benefit is that since these contracts are long, EFC has less risk of asset liability mismatch and since EFC signs straight leases without any profit share with building owners, their margins are higher (not including that they are backward integrated into furniture and design).

What I get from CCD disclosure if that EFC is issuing these CCDs to its parent company to pay off some debts at 0% interest rate. Doesn’t change much because it’s a wholly owned subsidiary

Hi,

EFC (I) i.e. EFC India raises cash & gives them to its subsidiaries to run their business,in this case EFC Ltd… As per the regulations, the company cannot just simply pay cash to its subsidiary so it is shown as a loan in the form of buying the subsidiary’s debentures. This is common & nothing unusual. Hope this helps !