EFC (I) Ltd is in the business of providing office space solutions like Co-working Spaces, Enterprise Offices, Asset Renting, Turnkey Projects & provides complete Fit Out Solutions via its subsidiary Whitehills Design Ltd. EFC Ltd was started in 2012 by Mr Umesh Sahay and Mr Abhishek Narbaria, both first generation entrepreneurs on a remarkable journey in a capital-intensive industry, starting with virtually no capita

EFC (l) is the holding company of EFC limited. Mr Umesh Sahay and Mr Abhishek Narbaria bought controlling stake in Amani Trading and Exports Ltd and converted it into EFC (l) ltd then EFC (l) bought 100% stake in EFC limited which is into business since 2012

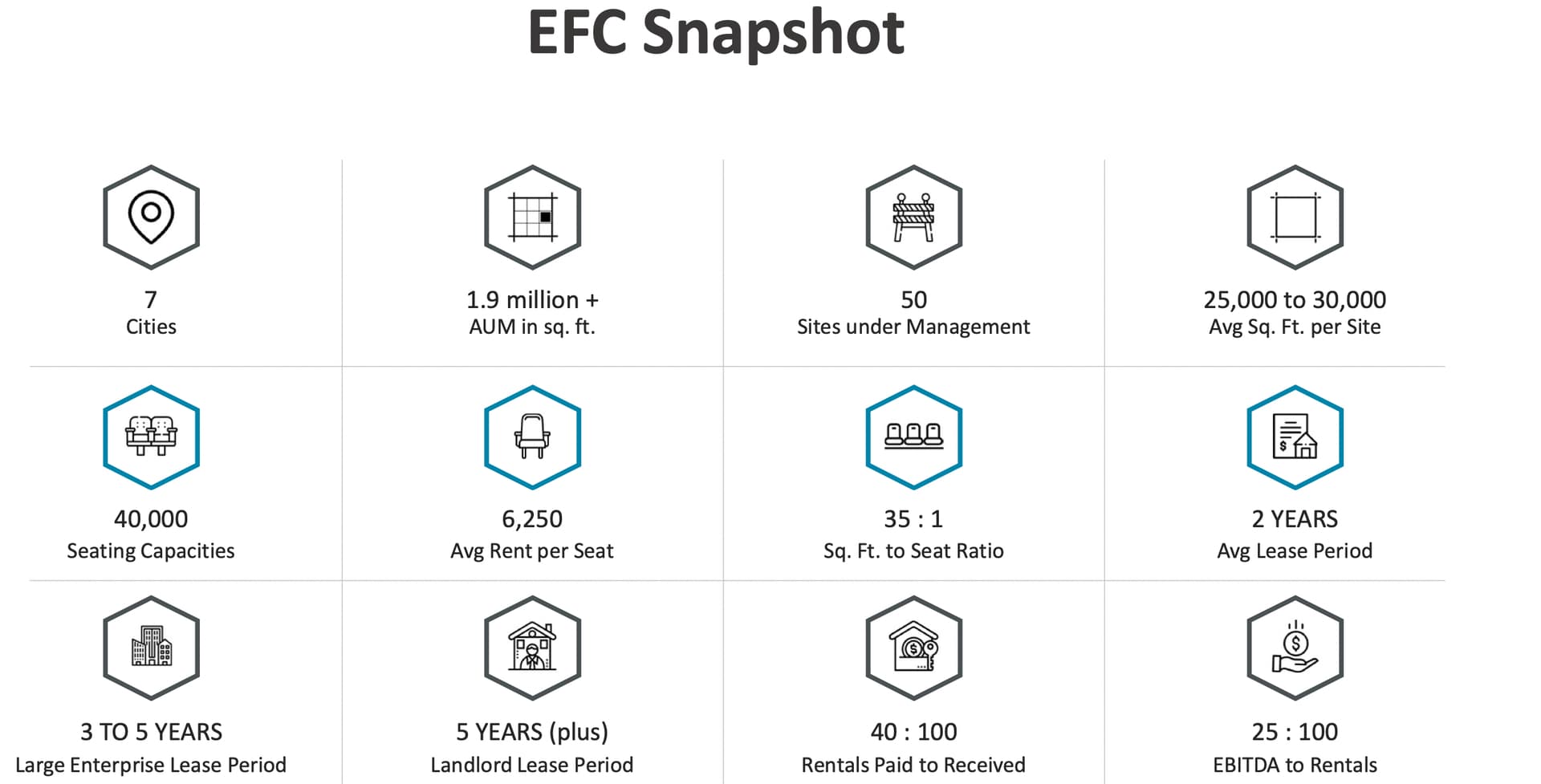

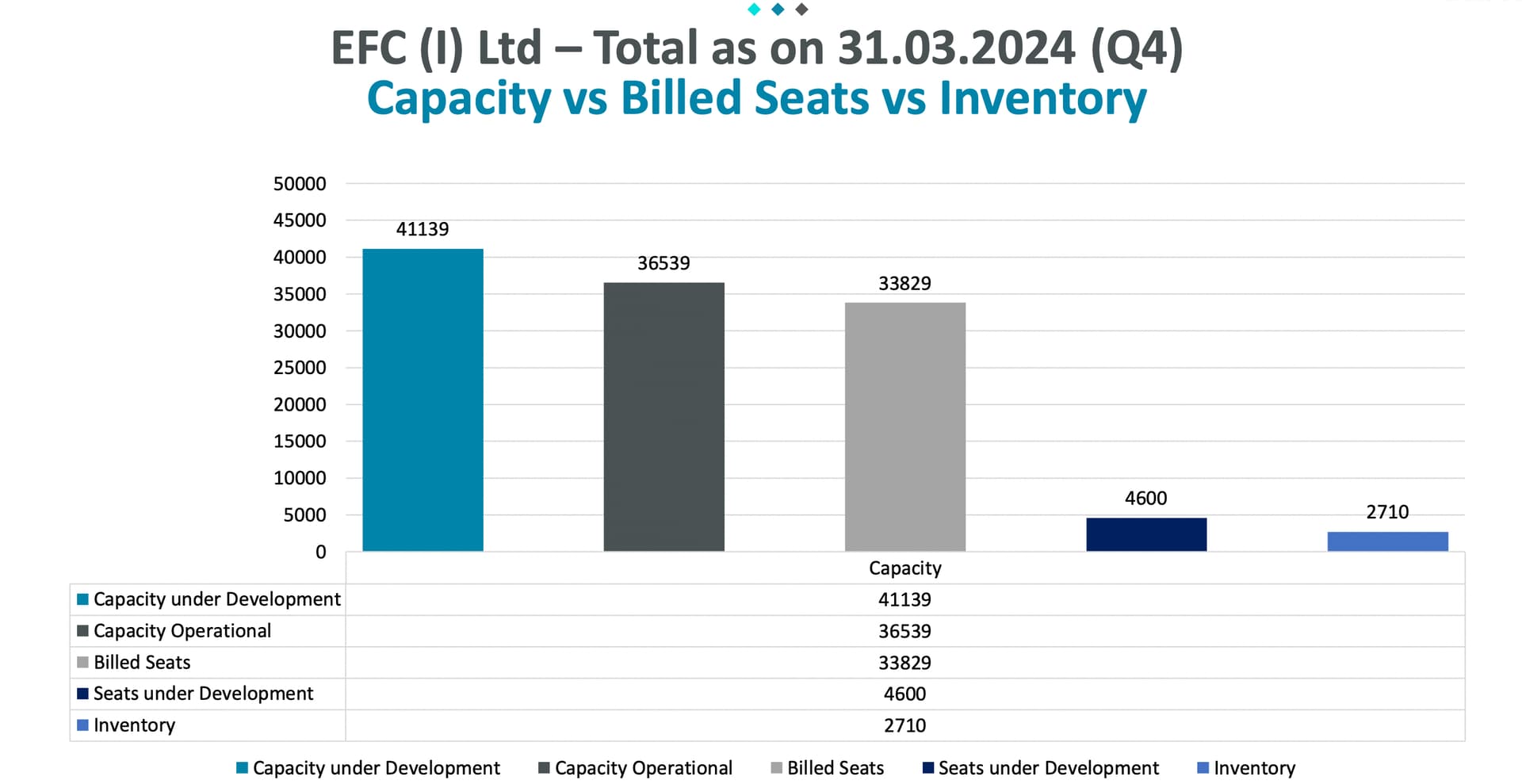

Having about 23000 seats spread across 1 million sq feet by FY23 end and about 32000 seats over 1.5 million sp feet by october 2023.

About Umesh Ji

1 Started doing business from the age of 21yrs. His father was an engineer and Umeshi Ji did his MBA from Pune.

2 Started his first business maverick software pvt ltd in 2006 with his cofounder. They used to provide the entire IT infrastructure and made one of the most advanced CMR software and sold that business in 2010.

3 With that money they started EFC and since then have been raising money on merit and this is how they funded their business with a lot of struggle and working on all level of roles.

Few Quote by umesh ji

- Business asa karo jis mai catchment hau

- Shopper stop mai cycle wala nahi jayega par Dmart mai Mercedes wala jata hai. Dono retail mai hai aur hum is dhandhe ke Dmart hai, cycle wale se lekar marcedes wala sab ate hai

- Promoter pe hai usko apni jindagi kitni mushkil karne hai. Dhande ko asa karo jo apke control mai hai

- Ye industry furniture ko rent pe dene ka hai

EFC limited financials

There are three main players 1 Owner(who owns the space) 2.Operator(EFC) and 3.Client

Different type of business model in the Flex space

1. Coworking- Under this the operator takes large space on lease, does the interior and rents to different people (individuals/entities) can come and work in the same place. Out of the entire seating capacity in PAN india there are very few seats available for individuals.

You can rent seats here even for 1 day, this is a volatile model as you have to maintain the occupancy level.

2. Managed office - This is like a hotel business where one office space is rented out to a cluster of clients. Like you can have 10 clients for 100 seats or 2 for 500 as well.

You can also have 2 formats here one is large format where in the entire office space you make larger sub sections like 100+ section only and short format where you can make smaller subsections like under 50.

Since EFC operates in large format they end up dealing with lesser clients, Which leads to less operational intensive and their occupancy hits 90% within 2 to 3 months once the site is live and their rental contracts is minimum 3 to 5 yrs unlike 18 months for other players

EFC would take 2-3 months for 90% occupancy post launch and this is how others build occupancy

EFC has clients majorly with more than 100 seats and for context tenure would look like this - From AWFIS rhp

So the industry has 70% of their clients under 100 seats and EFC has 70% of clients with more than 100 seats. This make EFC business rock solid and volatile for others because of smaller clients

Within the above 2 models there are 2 more ways to operate one is SL(Fixed lease) and second is MA(Profit sharing).

1. SL - In this I take the property on Fixed lease form the builder and the operator is the one to gain the most and lose the most. This is done by operators who have confidence in their business and their capability of getting the occupancy to 90%+ because any operator who has the confidence would not do revenue sharing. EFC has 100% of its properties under SL model

2. MA - Under this model you do revenue sharing with the builder, he is now part of your profits and losses. This is done by operators with not so much control on their business and who lack confidence on getting occupancy hece they want to play it safe. AWFIS is aggressively increasing under the MA model

Indistary size and growth for perspective

.India’s Grade A CRE market today is close to 810 Mn sqft, adding roughly around 50 Mn sqft new office space every year. Grade A CRE market to scale up to ~1,060 Mn sqft by CY28

India’s flex workspace sector is around 61 Mn sqft (expected by CY23-end), corresponding to ~7% of the total Grade A office stock in India – largest in APAC, and the penetration rate being larger than that of the US as well. Approx 680000-880000 seats

It is expected to grow at CAGR of ~15% over the next 5 years to become ~126 Mn sqft by 2028, from ~61 Mn sqft in CY23. From a value perspective, India would be addressing ~USD 9.0 Bn market by 2028, growing at a CAGR of ~21% from ~USD 3.5 Bn currently

Approximately 26% of the total commercial organized stock in India are institutionally held (REITS) as on June 30, 2023. Further, approximately 74% of the total commercial organized stock in India is non-institutionally owned stock as on June 30, 2023

The demand for seats in flexible workspaces has been growing annually at 30%-40% from 2019-2021. From approximately 59,000 – 69,000 seats per year in 2019 to approximately 167,000 – 177,000 seats per year in 2022 and expected to reach 335,000 – 345,000 seat per year by 2026.

Above are cut outs from various sources, EFC having around 33k seats and 1.5 million sq of area gives us a good context of their size in the market and growth prospects.

Different players in the industry

We work financials

AWFIS financials

Most of the larger competitors of EFC have been burning cash in their quest for scale. Among the players that have raised external equity none are profit making. EFC is the one with the highest PAT margins among a handful of profitable companies.

What is EFC doing differently?

-

EFC is a fully integrated player with 51% stake in Whitehill’s Interiors Ltd. They have their own in-house design and architecture team. They also make their own furniture which is about 20% of capex. Having your inhouse team decreases the turnaround time for interiors like EFC just takes 2 to 3 months to do the interior of a bare shell and 4 to 6 months for 90% + occupancy

-

More than 75% of their business is from managed offices, this is a low asset liability mismatch and higher occupancy business. 100+ seats are generally enterprise clients and below is the industry breakup. (In industry people say more than 12 months contract as enterprise client by that way he is 95% enterprise otherwise on 5yrs he is 70 to 75%

Industry standard is 70% less than 100 seats and EFC is 70% more than 100 seats. When you have a higher number of clients your center size decreases and the number of centers increases which makes your business more complicated and operationally intensive. AWFIS employee cost as a % of revenue is 15% to 17% where as for EFC it is 2% to 3% we can see a huge difference here.

- Being a professional company by being VC funded and having a foreign CEO with 5yrs tenure leads to no skin in the game and leads to the company being run from the boardroom. This also leads to having a large corporate hierarchy which in turn reduces flexibility and increases decision making and you end up having lesser relationships and try to fund your inefficiency from your broker and clients. Example

a) EFC would give their client 20hrs of free usage of the board room. AWFIS 60k per month for 6 seats

b) When you make an office space you make it based on speculation.Lets say 200 seats and your client needs 100 seats with 2 cabins. EFC having an in-house team and an accessible warehouse with all the material stocked they just need to put a wall in btw, fit AC and dismantle/rebuild the cabin and they do it free of cost. Majority of players charge for it because it is outsourced and they end up taking more time

c) EFC does not charge for longer sitting time, no charge from parking, no charge for working on saturdays. Since EFC takes entire buildings also they end up having ample parking and most of the clients come to then just because they have parking, free wifi. Other charge for everything mentioned above like in AWFIS you useWifi through their app and they charge after certain data usage, they keep a tab on their App. They have an app based system to track everything.

d). Other companies end up taking longer rent free period because their Fit outs process is slow whereas EFC takes for 5 to 6 months this also increases their ability to acquire properties from brokers

e) Having your own interior team helps in economy of scale. You start manufacturing furniture in bulk, you buy AC in bulk like EFC buys at 20-25% discount and if you are left with some you sell it to sub vendors at 5% to 10% discount and still end up making 10% on it. Like in Q3FY24 they make 9cr PBIT on 40cr trading.

f) During covid EFC used to share his entire cost with clients they became extremely transparent like lift was not working so common maintenance reduced, electricity, water, internet everything was discounted and passed on to the client and with that they used to pay their lease. This is the emotion /relationship /flexibility they offer.

g) If I have 100 sq of carpet area and out of which 20sq is common area with 10 seats. My per seat area is 8sq and blended is 10sp. This means higher common area and inefficient seating capacity would lead to higher sq per seat. EFC has one of the lowest area per seat in the industry

If you make money and create value you can share it in the ecosystem but if you are loss making you fund it from the ecosystem

EFC also turns out to be 20% to 25% cheaper than most of its competitors. So one of the lowes cost provider with highest margin

Most of them chasing top line with ton of money and not caring about occupancy and making it too lavish

What does the client want/looks at

- This is not a brand or a cost based industary, relationship and accessibility is what this industry is about. Location is the most important thing here so your ability to bargain with a broker and access to all location is what gets you clients

- Turnaround time plays a huge role here for the broker (will have to give a lesser rent free period) and client. Having an inhouse team gives you an edge

- Quality of fitment, design and flexibility of the operator also plays a huge role

- Having good parking space also plays a role here

What is driving the demand in this industry

- Taking up space from a flex workspace operator can lead to 20%-25% cost savings for the occupier, as compared to traditional leasing. Some of this cost saving is passed on to landlord who ends up with more yeild

-

If I have a large space I will have to rent it out to multiple clients and deal with multiple clients but if I give it for co working then I will have to deal with one

-

Selling an empty property is difficult from selling an occupied one the saleability increases for the landlord when the coworking starts

-

Grade B property in pune rental yield commercial is 5% but when coworking comes into play it becomes 8% (source ppafs)

-

There are no operational hassle like cleanliness, security, repair and they will also give free tea and coffee

-

Flex space acts as a hedge against head count uncertainty, where companies avoid committing to fixed location and high upfront cost. It also give flexibility to startups to upscale and downscale their team as and when required

2008 kind of recession is possible but covid like situation is one time. Any kind of 2008 recession forces large corporations to not own office space and rather rent it in a flexible way which actually increases demand for flex. WE WORK USA was born after the 2008 recession

Covid also accelerated the demand for flex space. So head count decreasing can be an opportunity to move more towards flex

https://www.youtube.com/watch?v=QP20QMad1eE (definitely see the entire video but check out from 3 minute now)

- Start up driving the demand. WIthing startups the share of GIC & Foreign company is 40%

- GCC being one of the biggest driver of demand in this industry

With India having cheap labor and lower rent, global companies coming here and setting up their office is one of the biggest drivers of demand in the flex market.

IT companies have nothing to do with this industry. There is no software company who would do flex working because they get state sponsored infra . Since they generate employment they have government schemes which help them get land at peanut rates so it would never make sense for them to do managed office. It is only ITES who drive this industry. So slow down in TCS/INFY have 0 impact because they are not the clients.

They can only give Fitout work which EFC already gets

New model which EFC is entering

EFC now wants to own property instead of taking it on lease and they are going to do that in multiple ways

- They would be creating REIT to operate in the flex space. So the operator would be raising money from investors for the REIT and that REIT would buy office space and give it on rent. The yield is now passed on to the investors and the REIT operator takes their fees/cut.

- They would start owning properties by taking debt . So instead of paying lease I am paying fixed EMI every month and after the tenue I own the property 100%

- They would also raise money in AIF and start buying the property and operating

This model leads to no equity dilution and cutting off the landlord from the picture because you are buying the property and also reduces the asset liability mismatch.

What happens in a 2008 kind of situation

If you own a property via debt it is the same as taking it on lease as you have a fixed contractual obligation but with owning via debt as the year passes my interest and principal repayment reduces and during a down cycle I can sell my property at huge discount and exit the debt.

Let’s say I have a 10yrs repayment and a crisis occurs in year 5. So by this time my property has x amount of appreciation so now the devaluing happens from the appreciated price + half of my principal is paid so I have to sell my property at 20% to 40% kind of value to exit my debt. But as an opertor If I already own huge amount of property during down cycle I can take loan against them and buy properties at deep discount.

EFC is making their business so diversified and with economies of scale their purchasing power in each vertical would increase so much that their cash position relative to the entire industry would be extremely strong during such down time. Like they do furniture, interior, REIT, AIF etc etc.

Since the number of clients with more than 100 seats is high for EFC they would be the last one to be impacted in such a crisis. So companies like Awfis would have to consolidate and EFC would expand. This is exactly what they did in covid and they were one of the largest buyer in Flex industry during covid

Valuations

Very subjective and a lot of assumptions here, can be 100% wrong but once I get more clarity can update this. But as of now it looks like this

Cash Flows

Their receivables have gone up by 10x this year but this is primarily because of the huge amount of interior and trading in Q3FY24. Almost 100cr

Interior business is such that by the end of the quarter if I complete 50% of the work I would recognise the revenue but I might get the payment after the entire work and trading is them selling AC and furniture to sub vendors. All are under 6 to 8 months and should clear off by next qtr

Why Negative Cash Flows ?

I am growing at 100% so the moment I get cash I need to put it in working capital. If I slow down I would be flushed with cash. Let us understand where cash is going

- If I want a building today I need to block it 12 months prior. It is like reserving a hotel

- The longer the rent free period the higher the Minimum guarantee, need to pay this to builder

- When you are making a new building large infra despite it being rent free you have to do a lot of work like cabeling/infra. Like if the building is 15yrs old you have to change the entire urinal line as it can choke, u need to check density all these expense are there

- When I come live it still takes time to build on the occupancy an meanwhile I have to pay the entire common area maintenance, electricity etc etc

Majority of cash goes through other financial asset/ other asset. Except receivable if cash is flowing to other section they are not a big concern imo

Major cash goes into other deposits/advances so we need to understand where the clash is flowing out and in this case we know it is purely for expansion. Receivables is a concern but now we understand what exactly it is

New developments

- They are coming up with a 3 acre furniture factory in navi mumbai with all german machines

- He would make furniture here and sell it to middle class consumers and coworking space

- They are going to come here in a big way

This would be 100% owned by EFC and in my valuation report the revenue form here is not included

EFC Clients

RISK

- Industry is Cyclical and commodity type only if you understand the business and are present in the entire value change with enough diversification you can minimize the impact

- Lot of new players are entering. This can increase the competition and there can be a possibility of supply exceeding demand leading to lower occupancy.

- Any further equity dilution can reduce the skin in the game for the promoter

- High growth funded by debt can be a huge risk if things go terribly wrong and you end up with negative cash flows

- There is an asset liability mismatch in this industry. If you cannot fill up your space then you end up paying lease and earn nothing

One of EFC office space in feb 2024 with 1400 seats, entire building leased out with 200+ parking

As on 08/06/2024 within 4 months with 300+ seats booked

EDIT

EFC is guiding for 800cr to 900cr revenue for next year with 130cr to 150cr PAT. They are also saying that the new factory would generate 300 to 400cr of revenue and going forward they expect huge amount of interior work as well

Link - [Video] ET Now Swadesh on LinkedIn: #corporateconnection

Source

Flex Workspaces_ A USD 9 Bn Market Opportunity By 2028_compressed.pdf (6.0 MB)

Profit Mart sees 58 UPSIDE in EFC Limited_compressed.pdf (631.2 KB)

Awfis-Space-Solutions-IPO-Note-Axis-Capital_compressed.pdf (548.7 KB)

- AWFIS DRHP

- EFC annual report

- https://www.youtube.com/watch?v=-xJlmIdUYEg

- https://www.youtube.com/watch?v=vfqgWB6km5g

- EFC takes 3.6 lakh sq ft office space in Pune, Noida to expand its coworking business | Zee Business

Special thnx to sahil sir and nikhil bahi

Disclaimer - Invested and my views can be biased