How can an ethical promoter claim a valuation of 5,000 crore ![]() , only to close a deal a year later for 3000 crore? This is why these promoters are never trusted by the market

, only to close a deal a year later for 3000 crore? This is why these promoters are never trusted by the market ![]() and fail to create any wealth for investors

and fail to create any wealth for investors ![]() . Edelweiss has not created any value for investors in the last two decades

. Edelweiss has not created any value for investors in the last two decades ![]() .eated any value for investors in the last two decades

.eated any value for investors in the last two decades ![]() .

.

3 Likes

while the 15% stake has been sold at 3000 Cr valuation for having a marquee name like WestBridge; we should wait for rest of the 85% to give better valuation in future

2 Likes

Just a note to be considered when business non-controlling stakes are sold it’s usually sold with a ‘lack of control’ discount and that’s probably why it’s valued at ₹3000 crores including the discount for lack of control. Only 15% stake right - they don’t have a voice on the board.

In the case of Bandhan led consortiu buying the IDFC AMC - they were getting control so there isn’t a discount.

This bit should be considered.

However yes 40% discount is a bit steep. But however this valuation may be reached by the time they plan to IPO.

Disclosure: not invested but tracking

5 Likes

Although there are caveats, this appears to be a classic asymmetric bet — “Heads I win, tails I don’t lose much.”

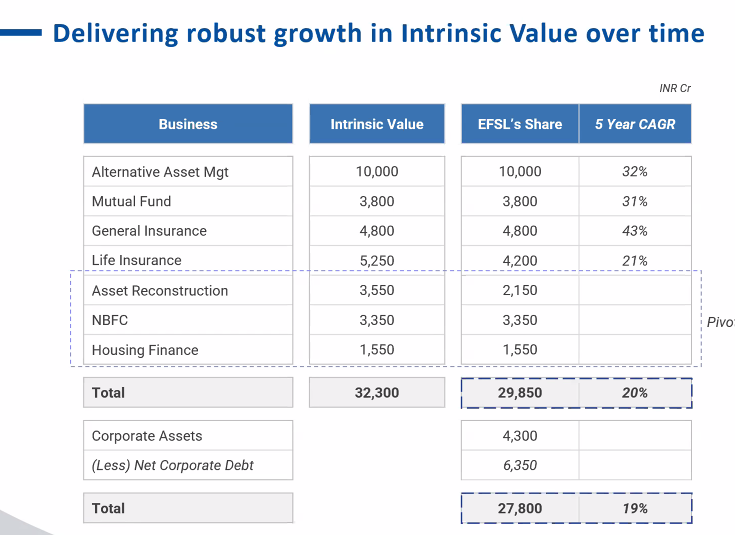

AMC (₹3,000 crore) and EAAA (conservatively valued at ₹5,000 crore) together account for nearly 90% of the company’s market capitalization (₹8,900 crore).

One might wonder why the market hasn’t rerated or valued it appropriately. While there’s no definitive answer, it could be due to the management’s historical track record and the lingering impact of the 2018 NBFC crisis.

Investing is as much about the future as it is about the past — it’s about identifying where the business is heading.

The demerger of the wealth management vertical (Nuvama), the AMC stake sale, and the upcoming EAAA listing all suggest that the company is moving in the right direction, with management showing strong intent to unlock shareholder value.

Unlike the Nuvama demerger, shareholders may not be rewarded immediately through these stake sales, as the proceeds are likely to be used to reduce corporate debt.

For a patient investor willing to wait 4–6 quarters, this seems like an interesting bet.

Disclosure: Decent allocation in the portfolio.

5 Likes

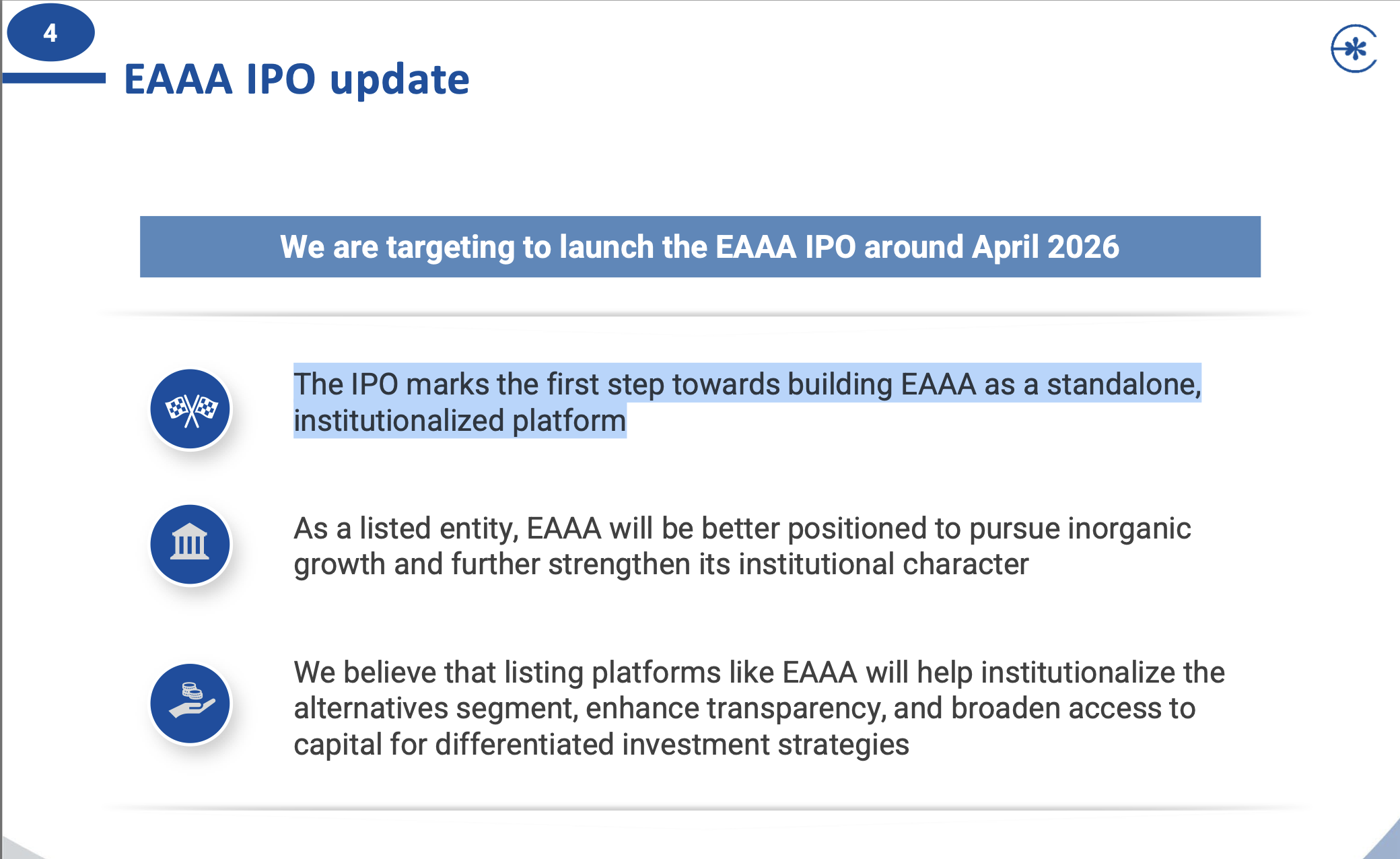

Most probably yes, intrinsic value is way up for EAAA. The IPO is expected to come with valuation of 6-7k crore. I would personally not use this table for valuation as it doesn’t has holding discount and stretched valuation.

I think it is at a decent price for a horizon of a year or two and expect potential upside of 30%.

Disc: Invested

2 Likes

The table is provided by company themselves

10-15% discount to intrinsic value is fine but a 40% discount is way too high

They couldnt find buyers willing to pay more than 3000 cr

For EAAA ipo what stops them to say that due to bad market sentiments they have further delayed the ipo?

Disc : Studying have a small tracking position

5 Likes

5 Likes

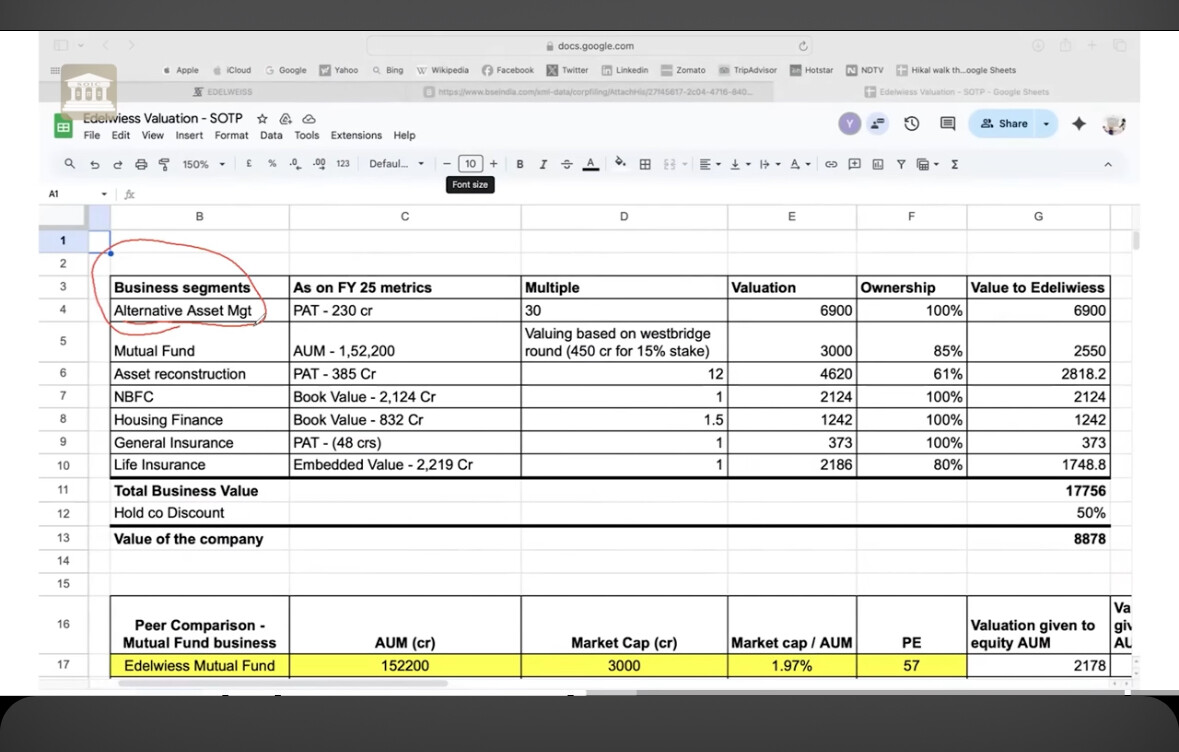

Edelwiess Valuation - SOTP.xlsx (10.1 KB)

SOTP valuation spread sheet referred in above video. Attached here for future reference as the story unfold in the next 2/3 years

Very well thought and details PPT @Worldlywiseinvestors Thank you very much

7 Likes

You have to discount for the high level of debt at the holdco level, so value will come down because the management has already stated most of the proceeds from selling stakes and ipo will go towards paying off the debt which by managements own admission is too high.

I think 50% of Holding Company discount is too much and we should value General and Life Insurance a bit higher as in that business, initial losses are almost guaranteed but after few years the profitability can multifold so I think its fair market value should be a bit higher.

2 Likes

Only way the stock can move is if the management decided to spin-off rather than coming out with IPO’S for its subsidiaries

2 Likes

4 Likes

You’re right sir. They have been messing with the intrinsic value quite a few times. But this is my POV - do let me know what you think. Edelweiss’s share is 29300cr. Let’s be pessimistic and discount this further by 20%. That gives 23440cr, which is a bit more than double the market cap.

So downside risk is zero. Why do I think that? AMC, Alternate Assets, and insurance (both LI and GI) are growth industries in india, they will grow sooner or later. The risk originated primarily from the lending business but theyve been cleaning that up. NPAs are close to all time lows in the country in general. Corporate india is mostly deleveraged, and lending will have to pick up now for the next capex cycle. If the wholesale book wasn’t reduced as mentioned - then further downside could’ve been expected. But now - the primary question on everyone’s mind is about hwo much upside? and when? and less about the downside. That being said I believe I am biased because Mohnish Pabrai has 20%+ in his fund.

Disc: Tracking position initiated.

2 Likes

Won’t you factor in any holding company discount in the valuation of Edelweiss? Discounts range from anywhere between 20-80% for listed holding cos in India. You factor in a 50% holding company discount and we have no upside left.

So Edelweiss is overvalued after 50% holding co discount.

True that is definitely a concern. But as explicity stated by the management, EAAA is not going to be a listing, rather it’ll be a demerger just like Nuvama. So you’ll make your gains there, whilst holdco is still turning around - LI and GI, and running the nBFC, housing finance and Asset Recon. business - while waiting for a potential listing or demerger for MF business.

It is definitely a bet with 70% knowledge of future, 30% uncertainty. Westbridge capital ivenstment was another litmus tests - as history of their investments have to proved to be very successful.

In the previous table highlighting the 50% discount, I think apart from MF and EAAA, the multiples for everything else is a bit too low… P/B for NBFC and HF should be at least 1.5 or more.

LI and GI will have a higher multiple once profitability is attained.

Management has been categorical about going for IPO for EAA. Any source which is suggesting that EAA is going for demerger?

They’re not doing the IPO for liquidity but rather for the independence of the platform…

Would also ask you to read the transcript (latest) to understand Rashesh’s tone.

But caution prevails since the management has delivered although not verbatim to what they promised.

Just to correct- EAA they are going to IPO not demerger.

There was no IPO for Nuvama as it was demerger.

However, EAA is is going through IPO and existing shareholders will not get any shares unlike Nuvama demerger.

2 Likes