I agree with your most of the views.

They cash in book but diluting the equity at every small opportunity is became passion for them and in media interaction they say this very proudly that its not a cash transaction just equity swap.

They are disturbing the good business and investing in these penny companies which may not give profit in the life time.

They want to improve the cash flows of corporate clients but what about easemytrip cash flows? FY23 has -ve cash from operations, this kind of initiatives will boost the receivables.

Yes, At least this time they have disclosed the valuations indirectly or by mistakenly.

We don’t have any clue about previous acquisition’s valuations.

I am looking for good exit opportunity .

Zero convience fee facility is still there, what they told in last con call is that they have stopped applying that promo code by default for every booking, but as I see now it’s getting applied automatically.

I agree with your indigo booking comments, indigo has reduced the convience fee and also booking in their web/app is much better cost than OTA’s.

All these unnecessary capital allocation policies are making institutional investors to stay away from this counter, in the meantime MMT zooming after becoming profitable.

New to this business, wanted to understand the sanctity of discounts given to the customers.

If say a hotel is Rs. 1000 / night, and OTA is making it available at 700 / night>>> then does the OTA bear the difference of 300? If so, what is the working capital cycle around it for the OTA?

Isn’t it diworsification as per sir Peter Lynch said in his book one of wall street? Meaning isn’t this entirely unrelated business than the core business of easytrip?

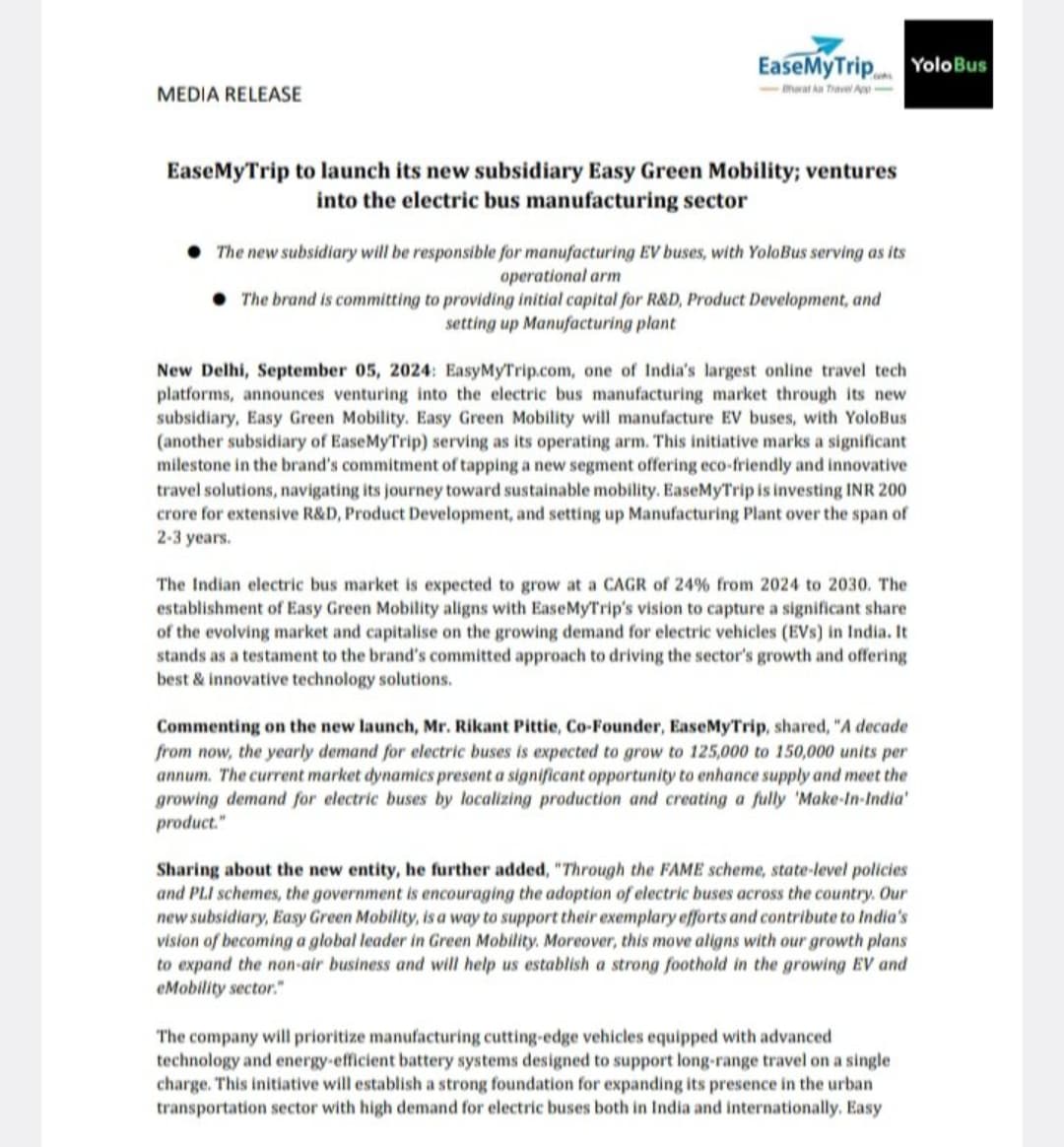

Yes, earlier they invested in the establishing a new 5 star hotel and now diversifying into EV buses. Now business is shaping out from asset light business model to asset based business.[quote=“Prashant_Karandikar, post:187, topic:60084, full:true”]

Isn’t it diworsification as per sir Peter Lynch said in his book one of wall street? Meaning isn’t this entirely unrelated business than the core business of easytrip?

[/quote]

It seems like a poor decision by the promoter. There have been 3-4 acquisitions, a venture into the insurance sector, the acquisition of GoAir in a personal capacity, and now a move into the completely unrelated and risky business of assembling electric buses. Despite these concerns, I am surprised to see the market react with a 10% increase.

Disclaimer: I am not holding any position in this stock as I exited at the right time (as mentioned in a previous post).

I don’t think this is fully accurate when you say that its totally unrelated business. They have a reasonably successful subsidiary by name Yolo Bus (https://yolobus.in/) which operates in 400+ routes across India and they also operate 80 own buses. They want to aggressively expand that fleet of own buses by adding EV buses (EV for obvious reasons). When they tried procuring those EV buses , they understood the shortage of supply in the market considering the huge demand and the delays from the existing EV bus manufacturers and their orders pile up.