Starting a thread on Easy Trip Planners (Easymytrip).

Note: This is my 1st company analysis, let me know if I missed something or you have any comment.

About Company:

EaseMyTrip commenced its operations in 2008. 2nd largest among the Key Online Travel Agencies in India in terms of booking volume.

Business: Online ticket booking mainly airlines, hotel and holidays.

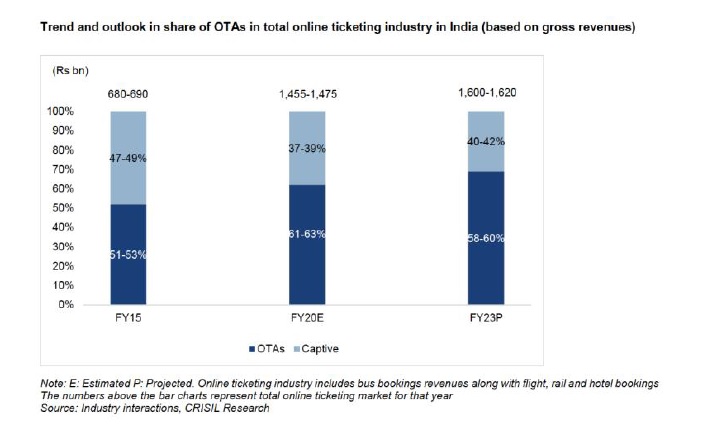

Summary of Industry

The online ticketing industry, in terms of value, expected to reach approximately 58% to 60% by Fiscal 2023, based on gross booking revenues (Source: CRISIL Report).

Review of the online ticketing market in India

In Fiscal 2020, the Indian online ticketing market increased at a CAGR of approximately 15% to 17%, from ₹ 680 billion to ₹ 700 billion in Fiscal 2015 to approximately ₹ 1,455 billion to ₹ 1,475 billion.

The air ticketing segment accounts: approx 60% to 62% of the overall online ticketing.

The rail ticketing segment accounts: approx 23% to 25% and

The hotel segment accounts: approx 13% to 15% of the online ticketing industry.

E-ticketing in 3 sub-segments:

Airlines have a relatively high online penetration of approximately 68% to 70%.

e-ticketing in total rail ticket bookings improved from approximately 55% in Fiscal 2015

to approximately 73% in Fiscal 2020 (Due to IRCTC).

Online penetration of hotel bookings in India is relatively lower at approximately 24% to 26%.

The bus ticketing segment has less than 2% share in India’s total online ticketing industry.

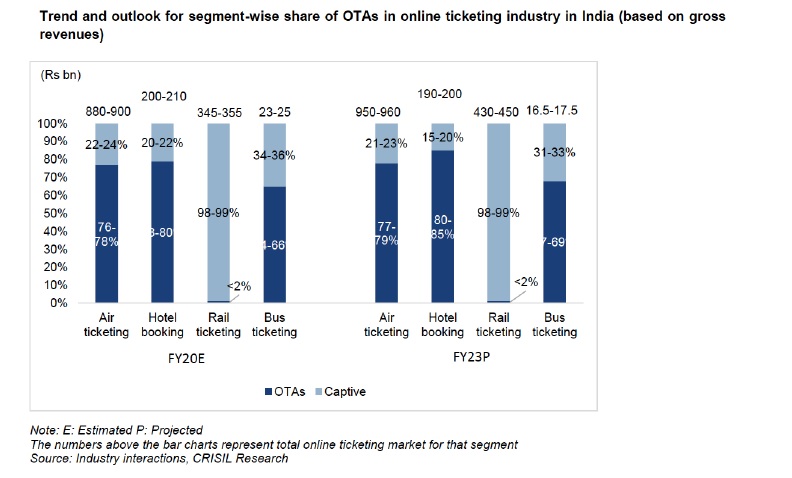

Share of OTAs and captive websites within online ticketing market in India

In the online air ticketing segment, OTAs have the highest share of approximately 76% to 78% in comparison with captive websites which account for approximately 22% to 24%.

OTA vs captive website based on Gross Revenue.

I n value terms, OTAs accounted for approximately 61% to 63% of the total

online ticketing industry in India in Fiscal 2020, based on gross booking revenues. In absolute terms, the market size was estimated to be approximately ₹ 900 billion to ₹ 910 billion in Fiscal 2020.

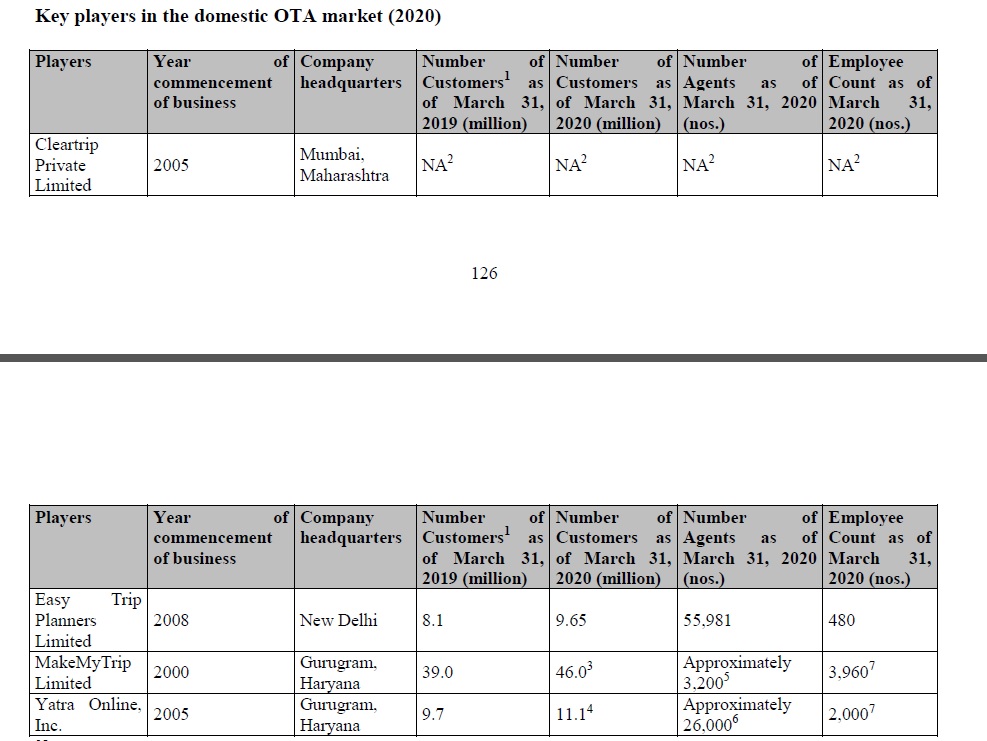

Indian OTA industry:

Competitors:

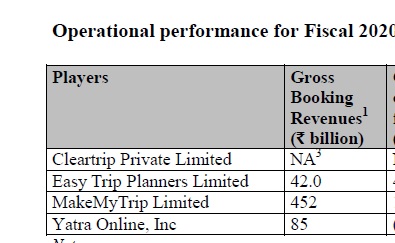

Competitors based on GBR:

Promoters are Mr. Nishant Pitti, Mr. Rikant Pitti and Mr. Prashant Pitti.

CEO is Mr. Rikant but Mr. Prashant is the key man. He holds a bachelor’s degree in electrical engineering from the Indian Institute of Technology.

USP:

- No-convenience fee

- Profitable since inception. They have bootstrapped the company, never raised money before IPO.

- Lean operations:

EMT vs Ind leader (In %)

Employee cost: 1.0 vs 6.5

Adv & Promo: 0.7 vs 1.4

Other Exp: 1.3 vs 3.1

Risks or red flags:

- Promoter is taking high salaries; 2 promoters taking total 7-8 cr salary.

- Out of 3 promotors; most holding is by Nishant and Rikant; however key person is Prashant; he has less than 0.5% holdings.

- Certain corporate governance issues. In the past, the company had funded movie production and other business operations of promoter entities.

- Stock increased more than 100% in month or so and trading at 70 PE

- Risk on industries: Impact of the COVID-19 pandemic on the tourism industry

Valuation:

The stock had more than doubled (IPO price of Rs 187 per share) since then to the level of Rs 450 level. At present, it is now hovering around Rs 400 per share (Market Cap: Rs 4350 crore).

It’s trading at M Cap / Sales value of 39.1 whereas MMT is trading at 18.6 and expedia is 5.7.

Key matrix to watch:

GBR (Gross Booking Revenue) is halved to 2128 Cr (Fy 21) from 4204 Cr (Fy 20). However PAT is increased to 61 cr (Fy 21) to 33 cr (Fy 20) due to cost cutting in Marketing, Employee exp, payment gateway exp etc.

Key figure to keep track - Revenue as % of GBR; in Fy 21 it was 5.0 and Q4 FY 21 it was 6.3%. Whereas cost as % of GBR is 3% in Fy 21 vs 3.1 in Fy 20.

Resources:

Disclosures: Invested since post IPO; added more post Q4 results. Hence I may be biased. This is for educational purpose only, am small retail investor not sebi registered.