Ease my Trip was once among my top holdings (back in 2022), when the growth was strong, demand for travel was rebounding and management was guiding very clearly.

Below are factors which turned me off and now I will not touch this company with a 10-feet pole (at least at the current valuations):

a) Management Churn and indescision: Nishant Pitti and Rikant Pitti (Brothers) have built the company from scratch. Prashant pursued his IIT and post -degree career is US while they were both hustling for “Zero-to-one” in India. During IPO roadshows, Prashant came back became the face of the company for investors, media, etc. and naturally so as he had be highest pedigree credentials to his name among the 3 brothers. The two brother gave him some equity each (adding up to 10%) with both brothers retained 65%. Promoters still had 75%. So far, so good. But then, soon after IPO, they were unclear about who gets to be the CEO. Prashant never became CEO, although he is the one representing company on con calls, media, roadshows, etc. Nishant was also not clear if he wants to be CEO as they briefly made their long term employee (Nutan, President, alliances) as their CEO but quickly turned back and revoked he position back to President Alliances. Meanwhile, Prashant went to pursue hi personal dreams to build a lending / NBFC business (Source: linkedin). Rikant being the youngest, was never the CEO candidate. They did hire a COO, but that guy left within a year. Now Prashant is coming back as CEO and MD. In this whole musical chair, as an Investor I have lost confidence in their leadership stability.

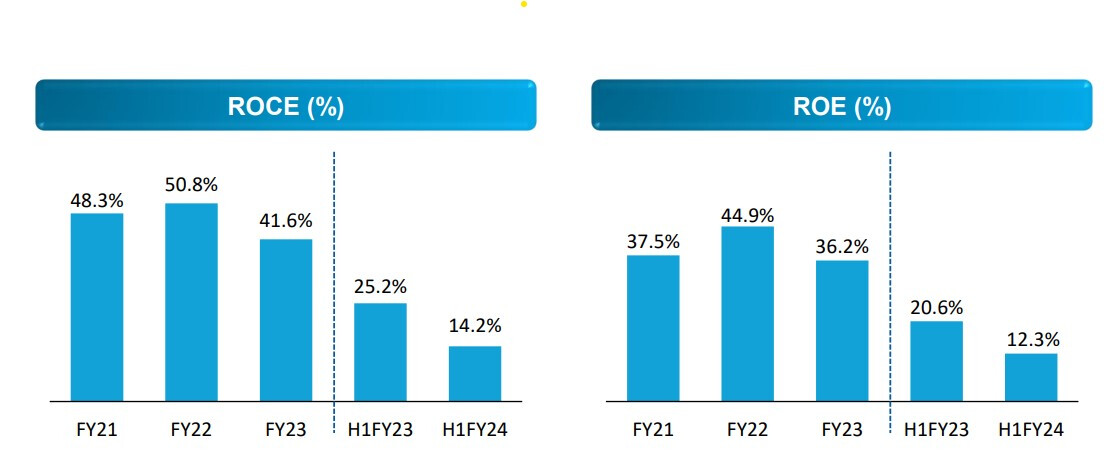

b) Acquisitions and Expansions: The company’s management made lot of noise about many acquisitions between 2022 and 2023 and their ambitious plans to move into non-air space and grow via inorganic route. Most of the Acquistions were too small to move the needle and they hardly have been EPS accretive. Acquisitions like Yolobus and many other have no updates on their profitability, etc. Also, The Management made lot of noise when they went Internation and open Dubai office and many subsidiaries in Europe, middle ease, etc. None of them so far are meaningfully adding up to either top-line or bottom-line. The USP of this company is them being a low-cost player and their OPEX is far lower than MMT, which made them bootstrapped and profitable up to IPO. Unfortunately, I do not see them being good capital allocators as incremental ROE and ROCE is now in mid-teens (don’t go by what it shows on Screener, here’s the real ROE and ROCE picture as per their own Q3 Investor presentation:

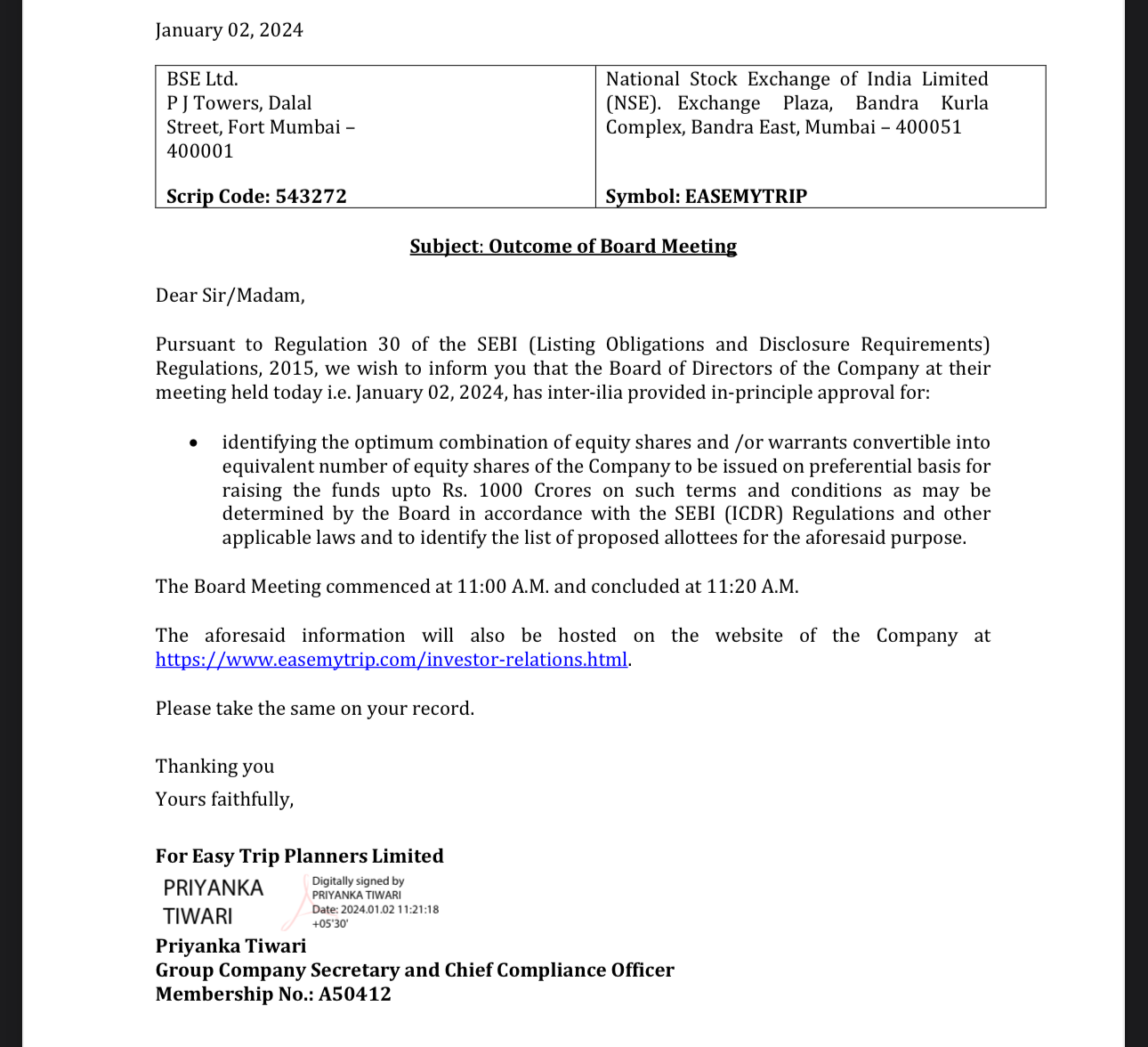

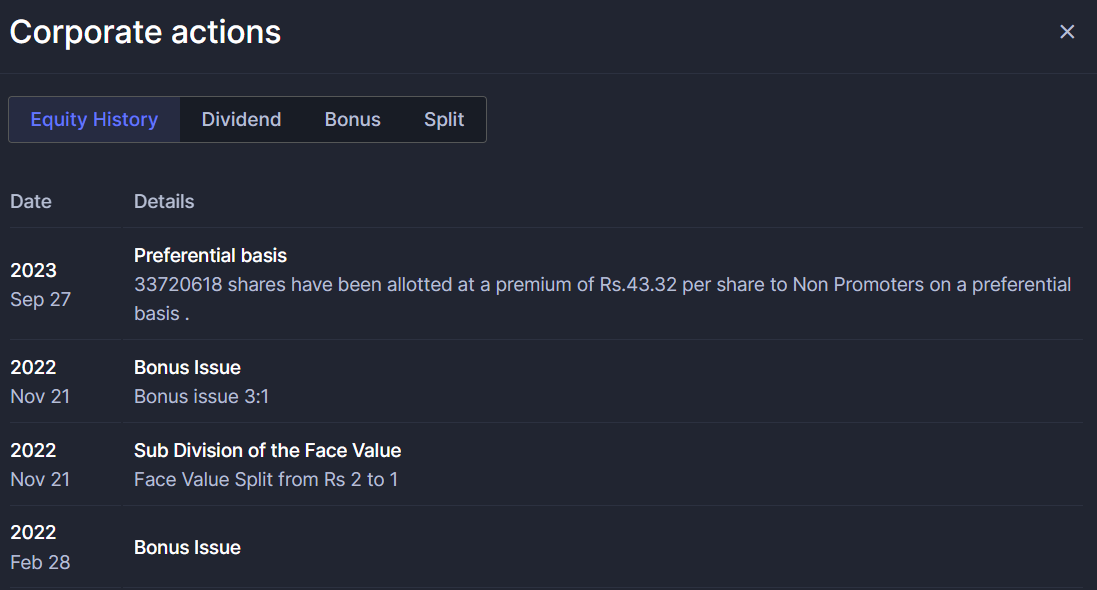

c) Dilutions and corporate actions: If the company is a Free Cash flow generating machine, why do you need so many QIPs, Bonuses, retail distribution, etc. Just look at the kind of corporate actions, dilution and distribution done by the promoters:

All this has resulted in crazy retail distribution. Look at the retail shareholders growth:

d) No Clear Strategy: From building hotels in Ayodhya, to bidding for Go Air to multiple small acquisitions to openings subsidiaries in all continents, management seems to be doing what “young money” usually does - Go out shopping! These businesses may not be ROE and ROCE accretive, going by their own track record of butchering their ROE and ROCE.

e) Lack of Moat and Pricing Power and inherent Vulnerabilities: Ease my trip is a small fish in a large pond. Their deposits of 90 Cr. on the verge of being written off with Go Air insolvency are proof what can happen if such incidents happen in industry privy to casualties. Probably they are rooting for Go Air revival because they are already stuck with huge dues. Might as well revive and recover their dues. It doesn’t work out so well in reality. Go air has long list of debtors and they won’t be the first one in queue to recover dues.

All this and much more has built a lethal cocktail, which I am unwilling to drink.

Others, please exercise due diligence and if anyone wants to restore my faith back in the company, please be my guest.

Disclosure: Not invested.