Whatever they do to please investors and QIB’s no body is going to rerate the company due to management activities, foolish board members ( Who can’t oppose the 100 Cr investment in building hotel). I believe some money laundering is also happening in the company in the form of these undisclosed (value) small acquisition’s.

Nobody knows how much these small investment companies are contributing to the top & bottom line. Yolo contribution is also unknown.

I bet that their QIP (1000 Cr) would be most unsuccessful QIP in the history.

They keep on diluting the equity to fullfill their person wishes rather than business needs.

4 Likes

Very predictable move…Who will be the buyer, interesting?

Disc: As mentioned in recent past post.

3 Likes

Eager to know who is the buyer, no marquee investors…

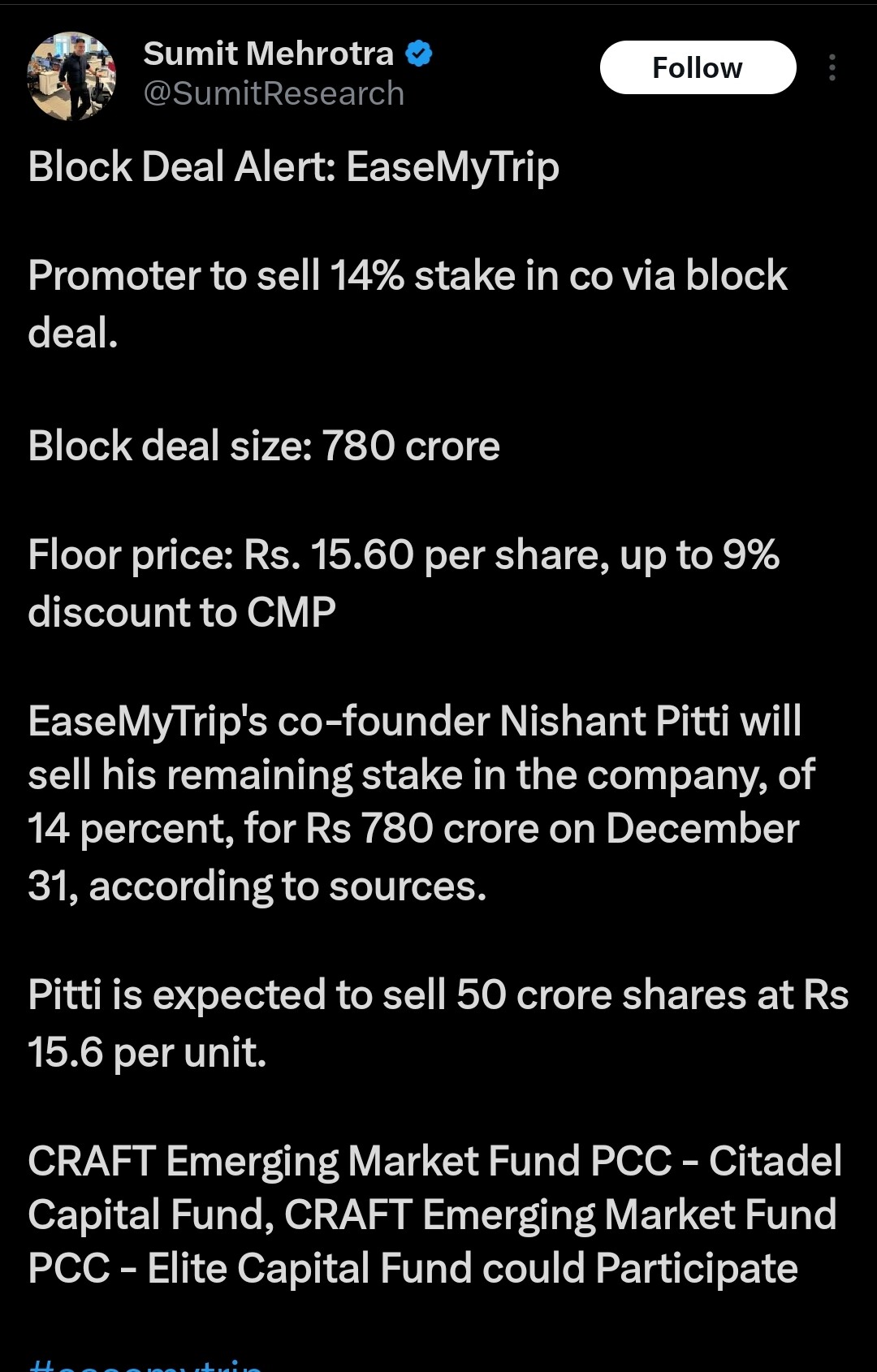

Nishant Pitti sold 24,65,49,833 shares, amounting to a 14 per cent stake in Easy Trip Planners. The shares were offloaded in the price range of Rs 37.22-38.28 apiece, taking the combined transaction value to Rs 920.06 crore.

Buyer: Core4 Marcom picked up 5 crore shares and

Craft Emerging Market Fund PCC acquired 1.05 crore shares

Craft Emerging Market Fund PCC - Elite Capital Fund is an Anchor investor actively investing in the SME space in India. They have invested in 10 SME IPOs

CORE4 MARCOM PRIVATE LIMITED no much information found.

2 Likes

I think all are traders arranged by Nishant himself, as if there are no buyer for this offload then it’s very shameful for the company.

Earlier also they offloaded stake by saying that they want to start an NBFC to fund small companies…

1 Like

It’s another shocking movement by promoters to rig share price. It’s now ~34, they want to see it below 10 as penny stock by issuing further unnecessary bonuses

3 Likes

@abhijitjph Though I agree with your statement, it would have been better if you had elaborated on why you think so, rather than just providing a one-liner.

One more reason to be bearish on EMT: the new acquisition—30% of the paid-up equity shares of Rollins International Private Limited for a value of INR 60,00,00,000 (Sixty Crores). Rollins operates in the wellness and healthcare industry, focusing on gluten and lactose-free foods, allergen-free supplements, and technology-driven health solutions. This is completely unrelated business line.

Turnover of Rollins:

FY 2023-2024: 2134.98 (audited) - should ignore the latest one; it seems inflated.

FY 2022-2023: 938.06 (audited)

They paid 60 crores for a 30% stake, valuing the company at 200 crores. Hence, they paid 21.32 times the sales of FY 2022-23.

I started the post of easymytrip, invested significantly, and exited timely post-GoAir issue (& because of it). Everything is documented in the above thread. I would put my neck out and say, “Iss stock may fasna mana hai.”

7 Likes

Find out who is owner of few of the companies emt invested.

You will start finding the answers

Hi @Deven I am new to the forum, thank you for starting this thread. I am one of the investor in EMT since over a year and would like to continue holding my positions.

Following are my thoughts on the recent acquisitions of different business verticals:

- The company has 460 Crores of cash reserves as of March 2024.

- Since the main business of the company is the travel booking app which does not need capital expenditure to scale other than marketing costs as it holds a good market share.

- What do we expect for the company to do with the piling cash reserves?

- Ideally investing in the new age businesses would definitely makes sense to me.

Regarding the stake sale, currently we should not see that as a big red flag as the promoters still hold around 55%+ stake. I guess it is part of strategic dilution to welcome new investors to the group and for the promoters to take cash out of the company for their personal purposes and investing in other ventures. Most of the newly listed IPOs do the same in the next 3-5 years post listing. After all promoters had put such a big efforts to build the company from scratch to IPO and it is obviously their time to take cash out of the business to diversify their portfolio.

Regarding the bonus issue, I see it as a smart move to distribute cash as bonus equity rather dividends which are taxed heavily. The cash stays within the company and also shareholders benefit in the long run as we sail through the growth of the company.

Please let me know if I had missed anything obvious. Thanks

2 Likes

Knowing all the moves from a long time, I’m surprised to see retail participation in EMT. If some one read this thread starting from post 1 to till date, the journey of EMT will easily breakthrough for anyone on how greedy the promoters are, and especially the allotment of bonus shares for every year is a big move to trap retailers, and once in a time EMT is trending under the top 3 in Twitter handles. Paid promotions and influencer marketing via offline channels are the reasons for trending this. And I feel even the profits are manipulated; that is why they keep on announcing the bonus to maintain the equity under books without giving dividends. For me, a company with sound profits having retail free float is on the higher side; not giving dividends is a betrayal, as companies are smart to allocate ESOPS, routing money via subsidiaries, related party transactions, higher depreciation costs, and many other ways that follow.

It’s too hard to see your confidence in this stock by looking at all these factors in EMT, and fundamentally no other travel-listed players are earning this much OPM except EMT itself, which is a reason for exiting the stock. Exit early and safeguard your investment and hard-earned money

And lastly, I wouldn’t surprise if they had people hired in Vakiepickr to promote this stock by stating some positive posts on EMT. Hahaha, this would definitely become the heights of marketing.

10 Likes

I appreciate your views and they are totally valid as per the data we see.

It’s just that I am an investor with contrary views and I look things from a different perspective. I might either loose a fraction of my portfolio or make big gains, over the course I will definitely learn a lot through my journey with EMT.

Also, I have no direct association with EMT other than just invested in the stock ![]()

3 Likes

Hi @VijayBenda,

Thank you for sharing your thoughts. You said “I might either loose…” - Charlie Munger said, “You don’t have to pee on an electric fence to learn not to do it.”

As indicated by Nishanth, the thread is rich with information, and all the details are there. However, you mentioned some data points, so let me respond to them:

460 cr – They don’t have that much cash. They may have less than 100 cr. Please recheck. Indeed, they went negative on cash in FY 23, then did some QIP/warrant @ Capriglobal.

Bonus issue: Smart move to distribute cash? How???

A bonus issue has no impact whatsoever. It’s similar to asking whether you want a pizza in 4 or 8 slices—does it make any difference?

I was banging my head when I saw the shareholding data of EMT:

When the promoter held 75% / public held 10% with Nos of shareholder 47,600,

Now, the promoter holds 64.3% / public holds 30.5% with Nos at 744,165 (15x).

Recent data will be more horrible.

7 Likes

I completely agree with the views as promoters tried to manipulate the share price in last bonus issue and rigged it till 80 levels now again same game started but now I think it would go to 20 levels as other than retailers no body is interested in buying. I bet who will give them 1000Cr through QIP.

They do all undisclosed transactions with unknown small entities, actual existence of those entities is also questionable but they don’t disclose valuations of acquisitions, all these things are just routing money through acquisitions

3 Likes

What a loser of a company

- losing share in domestic market

- can’t raise money and hence now buying companies given majority of shareholders are promoters only. 150 crore rs of shares will be issued.

- now has more companies in subsidiaries than its stock price.

Expecting another selling by promoters soon.

The stocks is heading towards single digits

5 Likes

Promoter selling huge stake was a indication that they are not interested in running the business. Listening to concall it is is evident that the promoter selling will continue as they provide no assurances that the business will do well in the coming future.

2 Likes

Still, On insta people are promoting EMT with a target of 80.

1 Like

May not related to Easy Trip. I was comparing global OTAs with Make My Trip and Ixigo. To find out how they compare to India based OTA on scale and margin. One finding is they all focus mostly on Hotel and accommodation rather on ticket book. Compared with Trip Group , Booking Group , Expedia group. All figures in $ million. Data of last reported quarter taken from SEC filling . Ixigo data also in $ million

| MMYT | BKNG | EXP | TRIP.com | IXIGO | |

|---|---|---|---|---|---|

| Revenue | 211 | 7994 | 4060 | 2261 | 25 |

| Hotel & Packages Revenue | 103 | 3317 | 1191 | newly started business | |

| Hotel & Packages Revenue% | 49% | 90% | 82% | 53% | |

| Marketing & Sales Promotion | 35.8 | 2151 | 2047 | 482 | 2.14 |

| Marketing & Sales | 17% | 27% | 50.40% | 21.30% | 8.56% |

| Personnel Expenses | 39.37 | 868 | 320 | 4.6 | |

| Personnel Exp% | 19% | 11% | 8% | 18% | |

| G&A Exp(for MMYT & Ixigo its other expanses) | 53.37 | 575 | 229 | 149 | 1 |

| G&A Exp% | 25.20% | 7.10% | 6% | 7% | 4% |

| PBT | 25.55 | 2869 | 874 | 994 | 2.14 |

| PBT % | 12.10% | 36% | 22% | 44% | 8.56% |

1 Like

Yes, that is the key area where EMT was lagging few quarters before.

As take rates in the airline tickets are not in the control of OTA’s, its purely airline decision and OTA’s has no power to bargain required rate. Whereas in hotels take rate is higher 15-20% of the GBR, this is where OTA’s can make some good margins. MMT is in good position due to 49% hotel & packaging business, as this % raise the bottom line multifold.

1 Like

If price geos below 10 then i will definitely look into this.

What are these promoters upto? in last call when they invested or acquired multiple companies they kept on saying that they hold more than 50% and their interests are aligned. Now after selling 14% they will give again logic it is more than other platform companies promoters. This is getting messed up

seeing finances and business, airline passenger business has been challenging but that is expected as there is consolidation at one layer below(mostly indigo and air india now domestic players)

Their growth in hotel business is good which is what bigger players are too focussing on. SOme of their investments in medical and educational tourism also made sense.

but the promoters selling is happening like there is something going to crack.

No return in company since 3.5 years(4 years since ipo) i think this has become another of retail investors being taken for a joke of a ride.

PE derating galore for last 3 years

2 Likes