Domestic aviation

Q42023 will show an optical 50-60% growth in domestic passengers but a muted less than 5-6% growth as compared to Q323

what happens starting Q1 2023, max growth perhaps in the range of 6-8% Yoy, coupled with some incremental benefits of international opening up

Eventhough airtraffic growth is low, their growth will be intact due to market share grab from other OTA’s and shift of customers from direct airline booking to EMT as there is no convenience fee at EMT.

Moreover now their focus is on hotels segment, it’s high margin business than air segment. We would see a good contribution from hotels segment in the upcoming years.

In my opinion Growth in air traffic is a bonus for EMT

They are going to enter new segments which can boost the revenues.

Slowly they are trying to decrease revenue share of air ticket segment and move towards the high margin business like holiday packages, hotels and newer sectors.

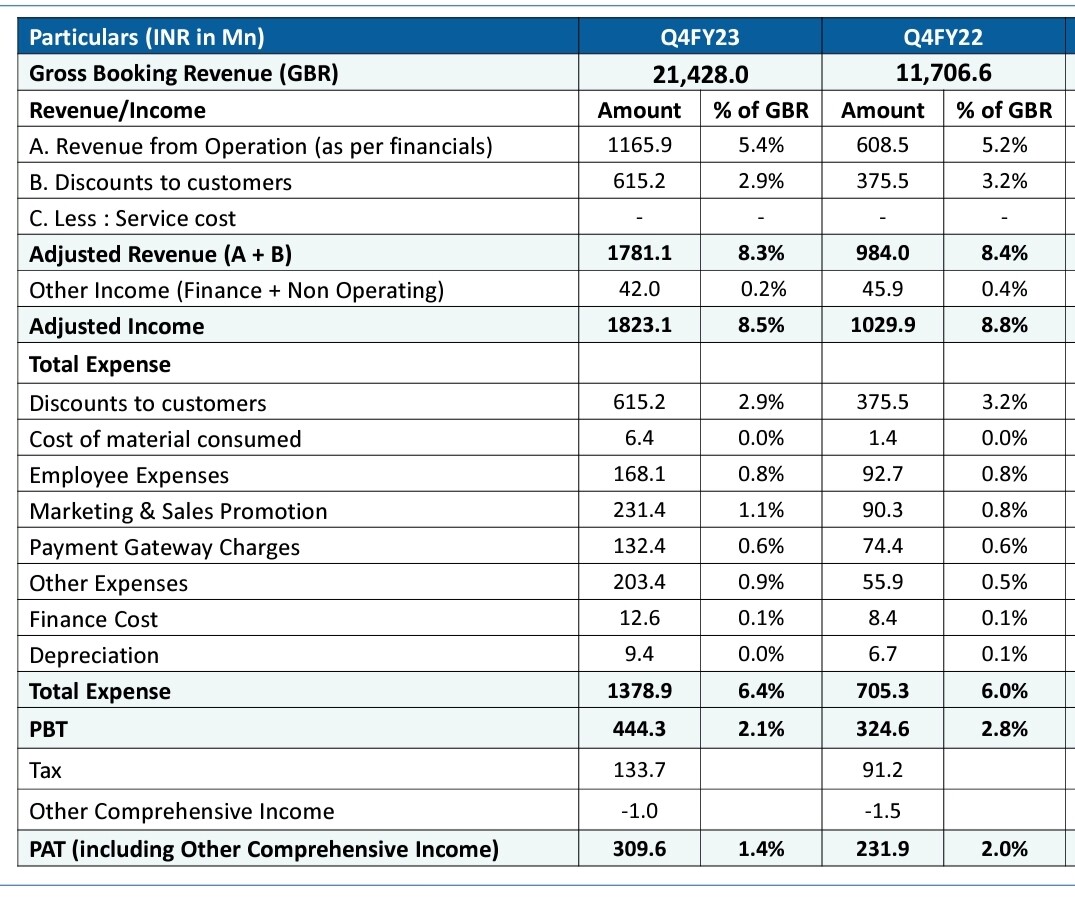

Why there is huge gap between GBR and Revenue. And also Discounts are shown as exp then why they have added this in other income? Due to this revenue have gone up. Didnt understood this adjustment.

In any commission business revenue is small part of GBR. Indeed as GBR increases revenue will increase but main part for us to take into account is revenue, profit and cashflow.

GBR for EMT includes total ticket cost, e.g. 10k, where revenue is their commission say 5% of GBR.

Their reported revenue is 120 cr; 116 cr + 4 cr other income. You posted PPT slide this is just to understand.

Said so their cashflow is scary for last 2 qtr, its negative. All cash is given to airlines etc to get more discount is what management is saying.

Also no one is talking about GO air exposure of 126 cr. In con call their was slight indication and management indicated they will get as airline become operational. am much concerned but street seems not.

Disc: Invested since IPO. Taken partial exit post results. Not buy sell advice. Am retail investor, not sebi approved and wrong manytime in past. Do your own analysis.

Thank you for explanation… Yes they have reported 117cr sales dont know why they have added discounts to customers in income side in presentation. Yes you are right GoAir recevables is a bit concerning. Also nutana airways is in initial phase, once operation starts will be intresting to see how it goes as Running airline is not easy.

company has manipulated its stock price in recent past , one stock becomes 16 stocks by bonus, split. again company declare 3:1 bonus but no record date declared .delivery is below 50% . operators create volume by bulk deals . stock price rose from rupees 10 to 70 in 21 months. Shares were under surveillance of SEBI . I always thinking why promoters are manipulating stock price, instead of focusing on business . 2 days back I come to know that promoter sold stock worth rupees 222 crores. smartkarma.com also says risk is there ,over all narrative don’t look attractive, confusing business model . independent director Mr maxy also a chairman of audit committee resign within 8 months

. this is the only company in industry to be profitable . market leader MakeMyTrip is not profitable, it means the companies performance is not inline with the industry, but doubtful. when there is doubt get out , by this principle , should we sell stock ?

266 CR block deal by nishant pitti to wilson holdings. Approx 4% holding. Even i think they are manipulating Stock price. One more red flag is there cash flow is negative and higher debtor days. Even though management is guiding for 50% growth there cash flow doesnt comfort me.

Today also block deal happened but in CNBC interview management guiding something else, No further stake sale, FY24 GMV & PAT is going to double, they hinted that some aquasition is on card.

If they can meet the guidance then stock is trading at ~25 P/E multiples of FY24 earning.

I am still confident about business, hotel segment will run at break even in FY24 but once it’s pickup in FY25, it’s high margin segment as compared to air segment.

Multiple factors that help the management’s credibility, and one would be that they do not appear frequently in the media or TV meetings to give the business prospects . Historically, such business had a dark truth that no one of us is aware of. I have a clear citation that they appear in the media very often to speak about profitability. And after all, it looks like the company is exiting steadily, and eventually this will lead to retail.

There are a few issues (or red flags as some may call them) I have encountered on this scrip. Though I can be dead wrong here. Hopefully, someone can clear it up on a few issues I encountered.

Margins expanded from 0% to 50% as soon as they got listed. Very tough to do that in a short span of time given they were getting hammered for losses and bad OPM for nearly a decade before that.

2. Makemytrip(MMT) and Booking don’t have such high OPM. MMT still makes huge losses despite having 8x more traffic and double the average page duration of EMT

3. It didn’t lose much revenue in FY21 (pandemic year) compared to MMT whose revenue came from 500M USD to 113m USD and recovered to 590M USD only now. Similar story to Booking if you read its statements. EMT had a better FY22 than FY20 and at more OPM. And these guys claim in PPT that they don’t charge any convenience fee for most types of bookings. Total transactions they claim don’t seem to be in touch with ground reality as I hardly see anyone use its app.

4. Never seen anyone use EMT regularly and its app downloads also are minuscule on the IoS store compared to all other big players. The sites do tell me that they have good traffic (but can’t see the traffic trend unless I pay). Also, clicks can be bought and there is no way to verify whether the actual traffic that comes is from genuine customers.

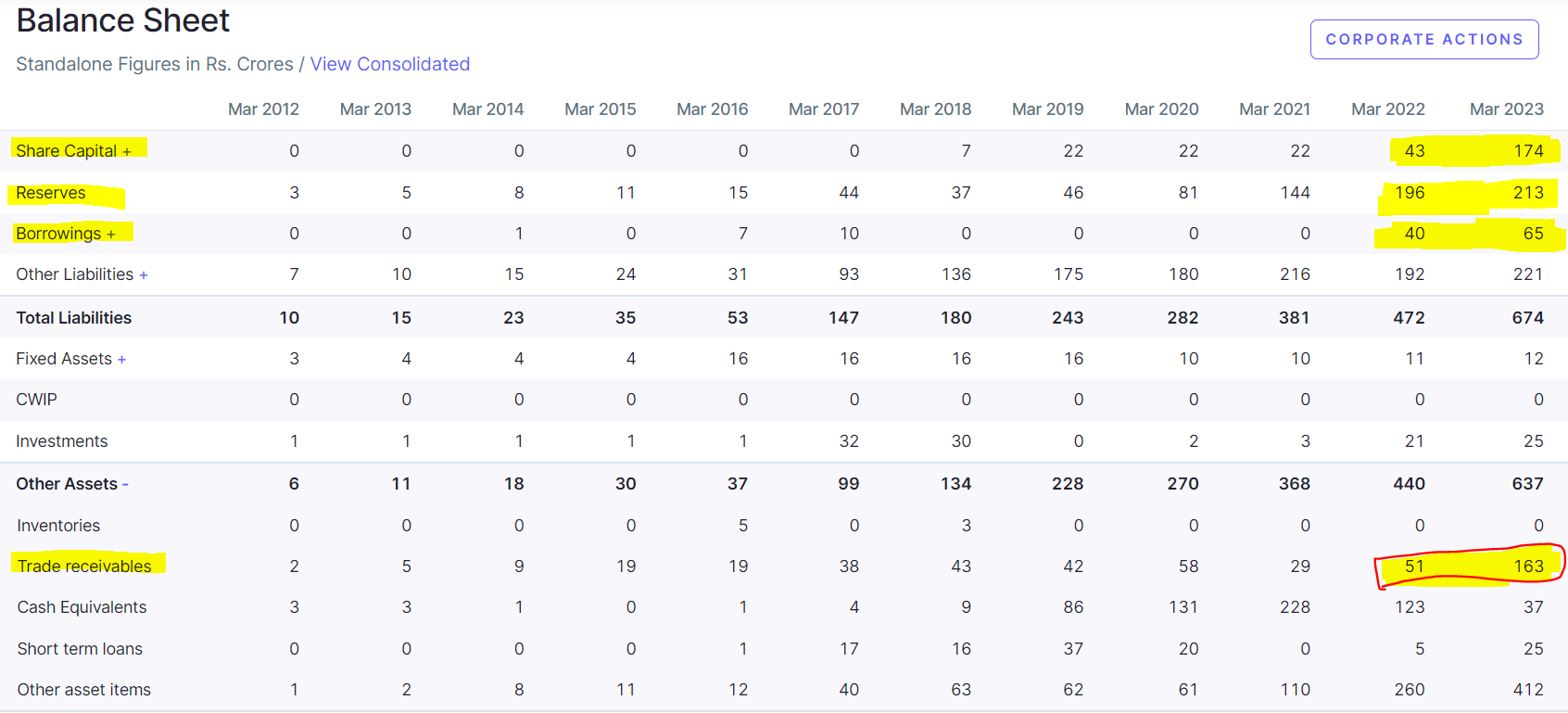

5. Balance sheet (of reserves 213 Cr) has trade receivables of 163 crores. Remember that this is an online business that earns most of its money through B2C transactions. Trade receivables shouldn’t be a big part of the balance sheet ideally. Cox and Kings also had a similar situation with regard to trade receivables even though the business model was a bit different from EMT

6. 116 Cr of cash in BS is in the form of ‘advance to suppliers’. Given the nature of business, it warrants a lot of questions as most of the dealings should be done through online channels without any advance.

As NN Taleb says 'Probability compound, don’t add '. It’s hard to ignore all of these things when taken in conjunction. Would love some counter views

A simple look at the company’s balance sheet on screener shows that the company’s equity base (share capital + reserves) increased by Rs 148 odd crores. On the asset side, there are no major investments being made, but a majority Rs 112 crores has been blocked in trade receivables, which is one of the primary reason for the company posting negative operating cashflows.

A question regarding this was also asked in the Q4 FY23 concall. The company stated that this substantial jump in trade receivables is due to the share of GMV from the B2B business has increased from 9% to 12%.

margin expanded: Easemytrip other income was the major reason. this was the money they didn’t refund for 2 years to customer of canceled booking which customer forgot to claim. shady practise.

MMT revenue came down because Hotel is pretty big in mmt. MMT did 4 Crore room nights booking in 2020 Fy before covid hit. Easemytrip does peanuts. entire easemytrip revenue is nothing but flights.

they claim their major business is b2c which is not true. check for their payment gateway expenses as a gross sales. it is in the range of .6, it is .9-1.1 for MMT at 5X more gross sales. low PG cost reflect b2B business being heavy

trade receviables: this business doesn’t have much in terms of trade receiveables barring some commission from amadeus/ GDS providers

advance to supplier is GO air money and at time paid to spice jet to get special fare…as special fare vanished, so did high margins…

starting q3 this year, this company wont grow even 10% in net profit… expect more promoter selling:) abhi to party shuru hui hai

Because I don’t think you understand OTA business.

Griss Booking revenue is amount of Airline tickets they sold: Gross value: 2142 Crore

the margin on airline ticketing including services fees/ special fare/ other things they showing is about 8%. that means they earned 178 Crore. but out of which they gave 61 crore as discounts to lure customers. so Net earning is 116 crore from the business.

PBT at 44 Crore , PAT at 30 Crore.

from here on, the Growth in airline ticketing will slow down to 10-12% instead of high 50% easemytrip showed due to low base effect.

at an yearly Pat of 120-150 Crore, EPS would be around 85 Paise. So figure out how much valuation you wish to give to this business, which still has lots of promoter selling left. No MF is invested and LIC picked some stake don’t know for what.

the selling by promoters will accelerate.

there is no reason for it not to accelerate.

the OTA industry is extremely competitive in airline field and now with consolidation happening between airlines to largely 2 domestic airlines, the Supplier direct booking contribution will increase.

Airlines and OTA will remain as it is. There could be some kind of consolidation. Pie is increasing at a good pace. Selling by promoters is ok as long as we onboard good marquee investors which was the case in last time prom selling

PR - EMT partially acquired 3 companies. I checked all their websites - failed to understand what emt is buying?. Cash flow and unrelated acquisition seems big issues.

Disc: Exited as indicated in my earlier post in same thread. Not buy sale advise, do your own research.

There is no cashflow company has. Money stuck in airlines.

wait before slow growth in air txn hit them. this is is classic taking consumer for a ride by issuing more shares and follow it up with more promoter selling.

Taking Revenue of 2020-21 as current yr revenue is unaudited and seems inflated (Some are gone up 4 times in one yr). As such for travel company, need to see profit, revenue has no much meaning but profit and assets are not given by management.

Valuation Cr Revenue 2020-21

Co 1: 32.64 / 12.7 cr

Co 2: 35.7 / 2.73 cr

Co 3: 61.2 / 4.81 cr

Need to see assets, but prima facie seems red flag.

Disc: No position as of now. Not sebi registed. Do your own research.