Per the Founder/Directors, they will not be spending anything additional to boost their airline business as they believe they are already well placed there. Any tailwinds in the air travel sector will also help them. All their future spends/investments/in-organic growth will be focused towards Bus/Hotels/Travel business as that is where they see they have a huge market to address and with higher margins.

there are no tailwinds left in domestic air. the share will reduce from here on, not increase.

I don’t know about the share price but the intent to invest and focus more on Bus/Hotels/Travel makes sense to me.

Share in domestic market is at a reasonable level which requires them to just mantain their Operating expenses and not expand here. Raising human resources in domestic market makes lesser sense as they might need to work aggresively on the international front. Thus the NZ and Dubai expenses in recent past. Also, gaining share in hotels - buses and other adjacencies makes more sense vs others.

if share in domestic market just needs to be maintained and margins are going to get lesser and competition intensity will go up, how will this company show growth in profits by 25% year on year? what is the lever??

Volume growth? Domestic aviation is still expanding right?

20%? 25%?

starting next year, (ignoring the base effect), it will grow at 6-8%, the 2 airlines will have 90% of market share (tata owns airindina/vistara. air asia)… supplie direct will increase too

now what p/e you will be comfortable buying and what growth in profit would you expect form next year after the low base thing is of the past

1 Like

Found interesting hence posting for VP friends…

1 Like

Lot many public announcement in recent time and besides company announced another bonus event ; events like Forbes, WhatsApp Announcement about success story, bonus issues, media coverage etc reminds me the shade of Tanla Platforms;

Little afraid that nothing wrong in fundamental.

I Don’t have access of articles, advance thanks if one share gist of it…

Disc: Invested since ipo, no transaction since long. Idea is to present both pro/cons.

1 Like

Unable to read entire article . Can you list down prime concerns . I saw a tweet by Nitin Mangal which was appropriately answered by Prashant Pitti . Didn’t found the concern raised very material .However if you can list down all the concerns , will help in further deep dive . thanks

Another red alert, thread #EaseMyTripStock is under treding tweets! possible chance of pump and dump activity

Another bonus & stock split, It is a honey trap for retailers… Be careful

wait for Q2 results

it will be lower than Q1 in all probability

Can you help with some logical numbers supporting your views . I see good traction in Air traffic and Hotel bookings , so wondering why EMT should not benefit

1 Like

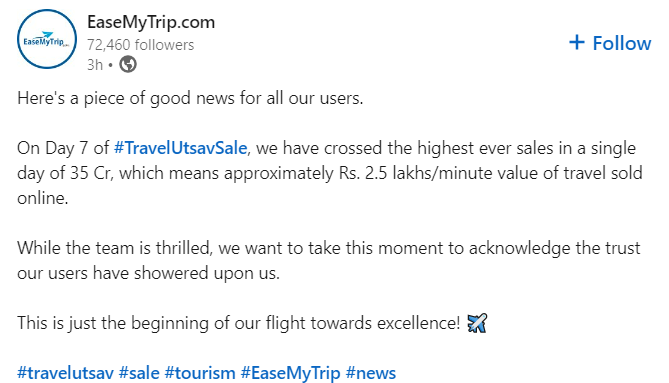

Yesterday Nishant pitti tweeted that they have done 35cr Sales in just one day by launching travel utsav offer. Later he deleted the tweet and edited the same as “massive response to the sales”. If this is true then Q3 will be intresting to see after.

Disc:- invested

1 Like

Apparently, linkedin handle of EMT posted the same info that Pitti deleted!

1 Like

@sidkat2006 EaseMyTrip witnessed an unprecedented sale of more than INR 350 crores in the sale period from 6th to 16th October. It looks good that EaseMyTrip is gradually getting its ground. [Details may be found in BSE BSEINDIA] (Disc: Invested)

1 Like

How does gross sale matter In airline Ota business ![]()

Extremely bullish by Prashant (co-founder)

1 Like