thanks for updating forum about promoters reaching out to you!! can we get further insights if you had any value adding conversations?

You are talking about $1Tn mkt cap software company(Nvidia) not taking partnership and alliance work seriously enough with prompt updates, is ur personal experience based on similar size companies and could you share same?

Lets turn the question around - would be more appropriate to ask if this partnership status is so simple - why not every other infra vendor listed on India partnership? Till we establish facts lets not under or over play facts.

It might be the case that they are just well prepared to be early in ride and eventually more partners will come in, however this needs validation and clarity on how mgmt intends to leverage this head start.

I agree with this assessment. It is definitely possible that the page is outdated but E2E and NVIDIA preference is not a very recent occurrence. I have seen this line in several past investor presentations. So it seems unlikely that it is simply outdated. E2E management had a great foresight of the AI rise and prepared for it with the launch of A100s.

To add further, even though the barrier to entry in this business is (relatively) low, making a mark and capturing large, reputed clients is extremely tough because of how popular and ubiquitous multi-billion dollar providers are. E2E has done this well.

I love the business model of NMDC. Mines iron ore, crushes it and sell to make a shiny buck at a handsome margin. Doesn’t get more straight than that. That does not undermine the profitability of the company at all. Sophistication/commoditization of an offering does not limit the potential of a company. If E2E continues to grow at 25-30% p.a. I have no complains. It doesn’t need to be sexy, just make money.

With reference to promoter reaching out to me, it was a linkedin connect request I got from Mr. Tarun Dua just 2 days after posting my first comment on this thread. Extremely low probability that this was a coincidence, as I do not work in the cloud industry for them to find me on linkedin and reach out. However after that initial connect request, I sent Mr. Dua a message asking how did they find my profile and he didn’t respond. I have not communicated further with him. Hope this clarifies.

On partnership and alliances, my comment was in the context of recent work I did for one of the presentation i was working on where I had to showcase “partnership and alliances” of my organization in a specific area. I cross verified the the list I got from our internal team by visiting the web pages of each of the partners and it was a hit or a miss. However, internal teams confirmed that alliances do exist and projects are being done jointly even if some company webpages do not have the name of our organization listed under partners page. Against this background I made that statement about companies not updating their pages promptly to highlight all partnerships. Hope this clarifies too.

Nvidia GPUs are commodity, just that they are in high demand right now. I am sure they would have other partnerships and alliances with other players in the country too. Even if they dont have it and we assume E2E is only partner in India, it does not automatically bring much competitive advantage to E2E in this specific context. One has to understand the level and depth of partnership and the kind of projects they are doing together to determine whether it brings any competitive strength (for e.g. does the partnership give them exclusive rights to buy and distribute Nvidia GPUs in India? I doubt that big time!). Just my 2 cents!

Sir, Netweb Technologies (NTIL) IPO is coming up. NTIL incorporated in 1999 offers a range of computer server solutions such as HPC, storage, deep learning, big data analytics, cloud and virtualization. It has role in implementation of Kabru supercomputer and PARAM YUVA II (fastest supercomputer). Will it bring interest in this server sector?

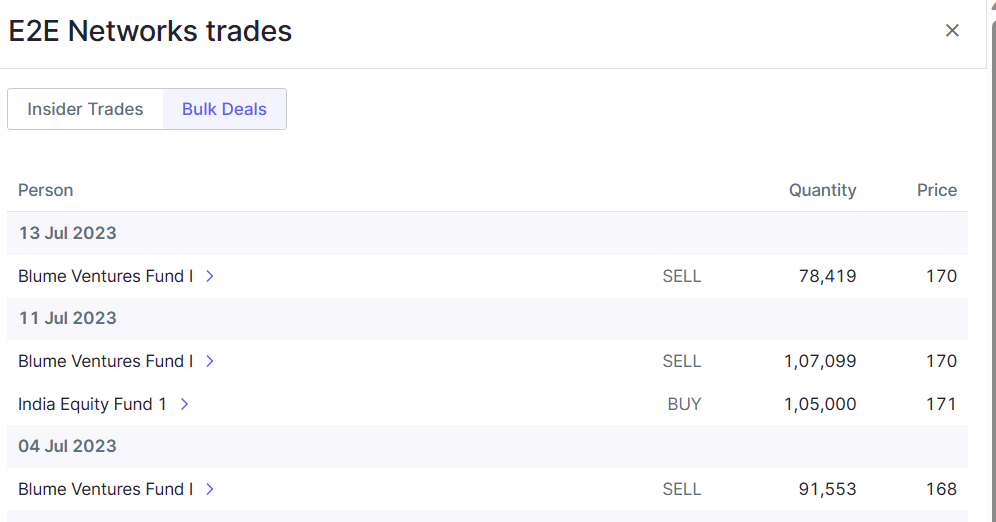

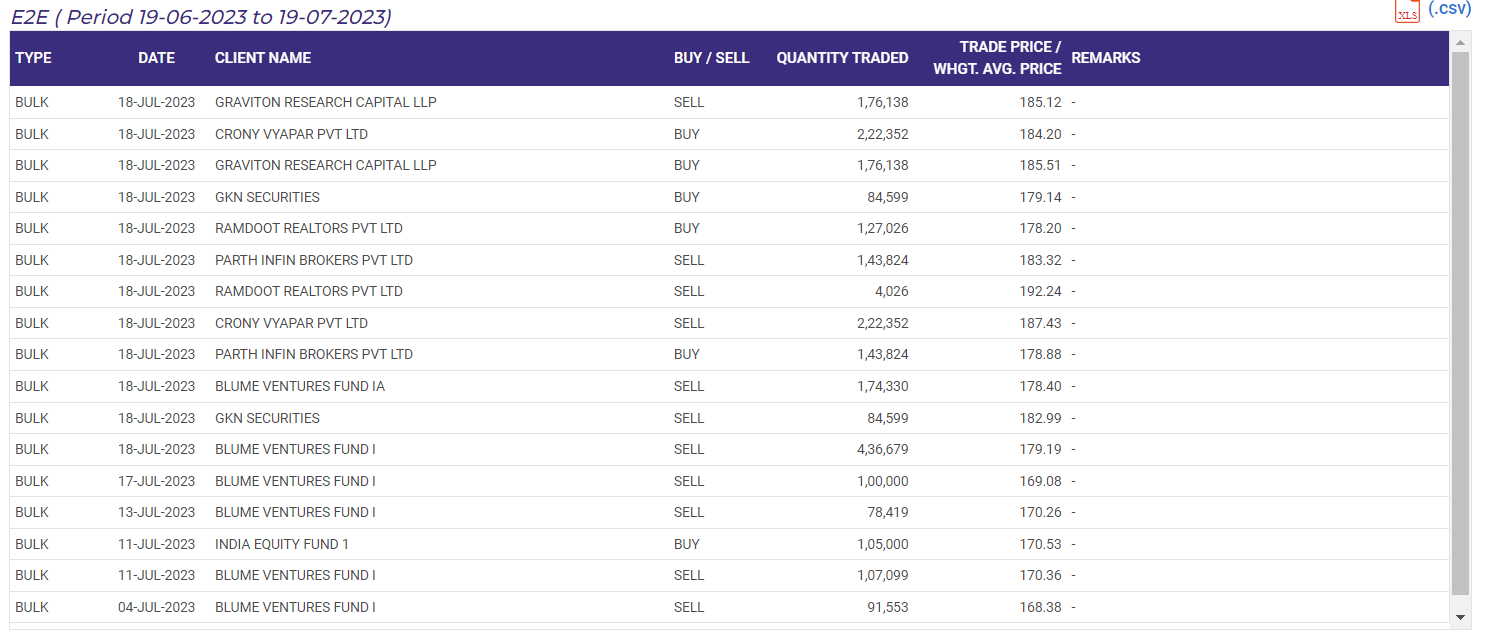

Huge volumes today! Wanted to inspect what had happened.

Found it interesting that most of the bulk deals are just day trades (right?)

Regarding Blume, they have additionally sold ~6L shares, totaling to ~10L shares (which should account to 60% of their holding, based on the previous posts here mentioning 11.5-12% holding )

Net buyers are India Equity Fund and Ramdoot Realtors which accounts ~2.2L shares

Some points from recent IR communication (Valorem)

120+ total employees and 40+ sales staff - ramping up this further - says its a lot of push work.

However they seem to be seeing lot of demand from SMB where large peers do not have much focus per co, they count digital ocean as a competitor

*MRR (monthly run rate) should see secular growth here on

Might start concall this Qtr

Doesn’t seem any exclusivity angle with Nvidia (yet to be validated by mgmt), however relationship and purchase size gets them meaningful discounts

Growth cagr rates of 30-35% achievable, ebdita 50% type doable

Revenue mix tilted towards GPU segment and would increase

Capex heavy business - planning sizable capex in near future and primarily be debt funded (again this needs further validation by mgmt, however said is backed by demand) -

Pricing and customizable plans per SMB(key target segment) is key differentiator per co - comes v cheap compared to biggies /more flexible plans/cust svc etc stand out compared to biggies (customer growth /churn wd b key metrics to track here)

Blume exiting per VC own internal mandates

All in all it seems a play with demand tailwind and. couldn’t assess any major differentiator as such as of now, large opportunity size and some head start on latest offering stand out, will require capex to support this high growth(hence high dep), even though there are larger players - there is room for nimble small players esp in SMB segment which can offer relevant offerings at price point.

recently there is some heavy volume price action, however lot seems jobbing/intraday type, should reduce with full exit of Blume

IR is responsive and folks interested in co can write to them

D - small position, kindly apply your discretion with own analysis , some of above points need to be validated by mgmt directly

Thank you for sharing!

Adding my 2 cents on 2 points from IR communication

It is not correct that SMB is not a focus area for large players…players like Azure are also actively getting involved in startup ecosystem and even offering free incentives/concessional rates and good support for startups

Huge capex…this was my initial worry and sort of anti-thesis pointer at that time. However, based on my interaction with a friend who works in the cloud area, he said these days big hardware players in cloud area have also started to offer hardware on long term rent (3+ years). I am yet to get full details on this model, but what I understood was players like E2E networks can now rent the necessary hardware to build their infra and instead of large capex, show it as yearly Opex. I do not know if E2E network leverages this model or has plans to do so

Good to get validation that GPU revenue going up. Would be more important to learn about margins in this area vs CPU. Volumes today have been crazy (compared to 3-10k average volumes) so need to get a sense if it is only due to Blume transaction and some intraday adventure by traders or something else is cooking. This counter has very low trading volumes, so price swings are wild.

a combination of everything. VC fund sell-off- so no selling overhang, recent IPO valuation is very high compared to e2e so coming to many funda guys, and the price breaking out a range to the stock is coming on the radar of traders. Most important the current euphoria to tech stocks in small and micro caps.

When a stock comes in the radar of both funda and technical guys… the magic happens

The way I think about this is Routemobile transaction recently happened at ~19x EV/Ebitda. Routemobile had ebitda margins of 15%, E2E has ~50%. Ofcourse the two companies offer different products but both are 1. Horizontal SaaS, 2. Majority India revenue, 3. Play on Digital transformation. Both are growing well but Route was growing faster, albeit at slightly poorer return ratios.

Overall, I see market is trying to assess if E2E should also be valued around same multiple as Routemobile. Discounting the multiple for lower growth and lower scale, the EV can stablise at around 14-15x of TTM Ebitda.

Investing in cloud computing companies can be a compelling opportunity for several reasons:

Rapid Growth Industry: Cloud computing is a fast-growing industry with a substantial market potential. As businesses and organizations increasingly adopt cloud-based solutions, cloud companies stand to benefit from the growing demand for their services.

Scalability and Cost Efficiency: Cloud computing companies can scale their operations efficiently to accommodate a wide range of customers without significant upfront capital investments. This scalability can lead to improved profit margins as the customer base expands.

Recurring Revenue Model: Many cloud companies operate on a subscription-based or pay-as-you-go model, providing them with a predictable and recurring revenue stream. This stable revenue model can be attractive to investors seeking consistent cash flow.

Innovation and Technological Advancements: Cloud companies are at the forefront of technological innovations, constantly introducing new features, services, and improvements. Such innovation can attract customers and provide a competitive edge.

Diverse Customer Base: Cloud services cater to various industries and sectors, making their customer base diverse and less dependent on the performance of a single market segment.

Reduced Capital Expenditure: Investing in cloud companies can be less capital-intensive compared to traditional IT businesses since they don’t require significant investments in physical infrastructure.

Global Reach and Market Penetration: Cloud companies can reach a global audience, allowing them to tap into markets beyond their physical locations. This global reach can lead to broader market penetration and growth opportunities.

Mergers and Acquisitions: Cloud companies are often involved in mergers and acquisitions, which can create additional value for investors through synergies and strategic partnerships.

However, it’s essential to recognize that investing in any company carries inherent risks. In the cloud computing industry, competition can be intense, and technological advancements can quickly disrupt the market. Investors should conduct thorough research on the financial health, management team, competitive positioning, and growth prospects of cloud companies before making investment decisions.

I respect the management and the company to bring in product in India for Indians.

Here is my 2 cents :

Basically E2E provides more of cloud services, good computation & performance at a reasonable cost.

What differs E2E from big cloud vendors likes AZURE, AWS?

Its not a apple to apple comparison but still I will try my best to differentiate

* SAAS : In E2E you don’t find tools/software which help in data engineering aspect to data warehouse, mining, data exploration, analytics etc. but what you can do is query the DB - using Postgres SQL make SQL procedure to run, write code for data molding or engineering (meaning its a quite a manual one).

The ideology that they are mentioning about AI here is that it contains a notebook

A notebook is a empty land wherein you need to code from scratch to develop any AI or ML based program now if you look in Azure or any other bigger player - they have lot of tools such as Databricks, Azure data factory, Azure Synapse, Auto AI/ML - all these are engineering products to mash and squash your data for neat and cleaner extraction - that goes to the analytics side - all these tools from Azure are kinda plug and play.

Now the advantage of E2E for India companies :

Storage & Retrieval

Faster computation

Cost effectiveness

Scalability

Now doesn’t the Indian companies have analytics and so on?

See the trend here now - Most of the companies are now onboarding to cloud in the sense they are migrating slowly.

About the data engineering and analytics prospective most organizations are still using on premise applications such as ETL Tools (for which they had paid perpetual cost), ANALYTICAL Tools (for which they had paid perpetual cost) so they will use a hybrid approach as long as they can and meanwhile E2E provides a simple user interface to write you PL/SQL & AI programming - but this is manual way.

Since the storage part of it gets costlier each time when their data expands - this product offers a innovative solution to help organizations cut cost on - storage racs, power consumption, dedicated team for server patching, maintenance and vulnerability checks, anti virus, infrastructure team, admin team for troubleshooting much more.

I sense this is a win- win for most organization if they onboard to the cloud as it takes off lot of data burdens.

That’s all for now, please post your query about IT - I can help. And am open to constructive criticism

In E2E Networks, Is there any possibility of pump and dump? I can see continuous upper circuit from past few weeks. Of course, fundamentals looks strong but the share price is almost doubled from past weeks…

Doubling of share price is no evidence of pump and dump. You’re right in that the stock is pretty solid fundamentally with some strong tailwinds. It is also true the valuation is stretching from a traditional ratio. The major trigger I think is Netweb IPO which has pretty astronomical valuations based on fundamentals. So, in comparison E2E looks like a good bet.

As a long term investor, all this doesn’t really matter. It could go to 500 or back to <200 over the next week. Will stay invested.