In the last month, the company has posted around at least 30 job openings. This is a huge expansion considering the employee count was 85 as per the last annual report.

Disclosure: Invested.

In the last month, the company has posted around at least 30 job openings. This is a huge expansion considering the employee count was 85 as per the last annual report.

Disclosure: Invested.

The other side of the coin is that there has been attrition in the IT field. It would be helpful to find out how much of that has impacted the company.

3QFY23

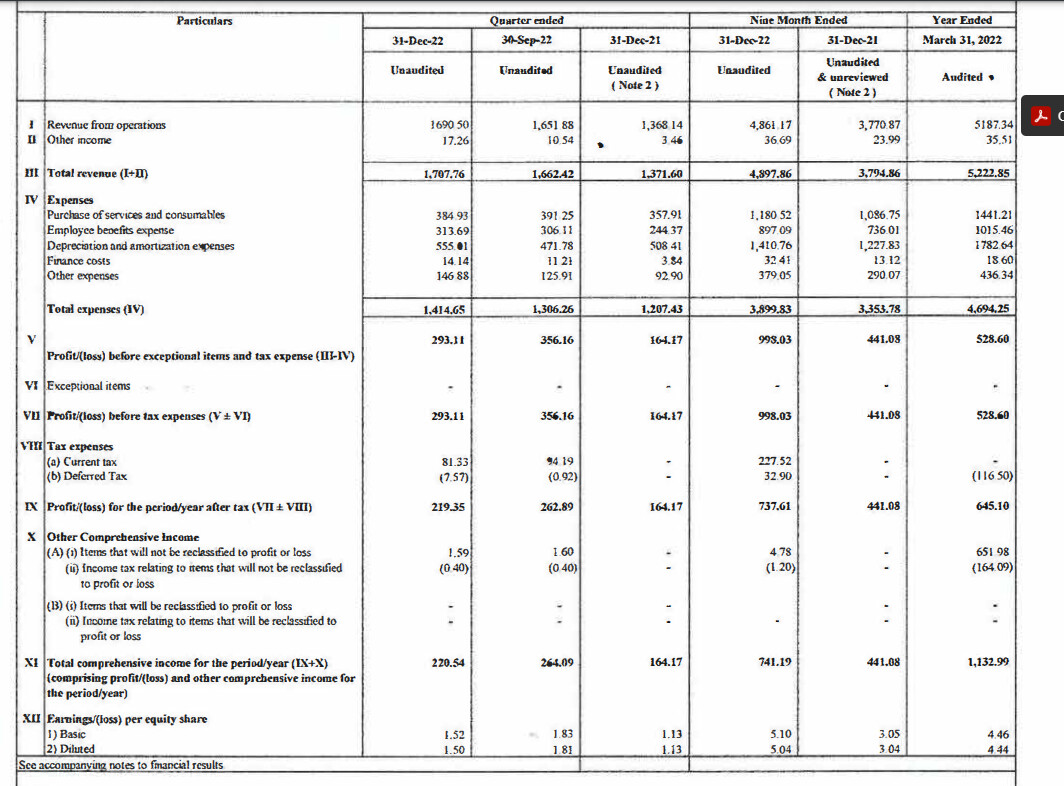

Revenues : Rs169mn +24% YoY

PAT : Rs21.9mn +34% YoY

9MFY23

Revenues : Rs486mn +29% YoY

PAT : Rs74.1mn +68% YoY

Stock has done Rs5.1 EPS in 9MFY23. Should do atleast Rs6.6 in FY23. Stock trades at 27.0x FY23 which is the cheapest internet cloud commerce profitable stock in India

The number are great YoY. But given the small size of the company the industry tailwinds supporting it, we should be looking at much impressive number QoQ. Those numbers at flat. I was hoping for a 8-10% growth QoQ.

The company is hiring quite aggressively (refer to employee cost growth YoY and openings posted form the company online) but those are yet to translate to topline. Hopefully, these will cause sales to pick up.

Disc: Invested since CMP 55.

Yes, this sector has enormous and persistent tailwinds, so we expect high growth. This quarter may have been affected by the fact that many startups have closed down or got smaller recently. If so, we should see higher growth going forward. This is just a guess and needs to be confirmed with the management.

Good set of number overall. Welcome jump in the PAT YoY. Overall in line with growth. Some mediocre stats I would like to see improvement in subsequent Q and FY are:

Mr. Dua was a little tight lipped in the last (first?) concall about the growth path in mid-long term. The proxy stats are good like employ expenses, job listing. My ideal situation is for the company to position itself as the go-to solution for cloud in India for cos and gov. The transition is one major controversy/case away and will give a 4-6 quarters period to firmly establish itself as the leading cloud provider in India. (Thinking Atmanirbhar Bharat). E2E needs to be prepared when that happens.

Disc.: Invested. Biased.

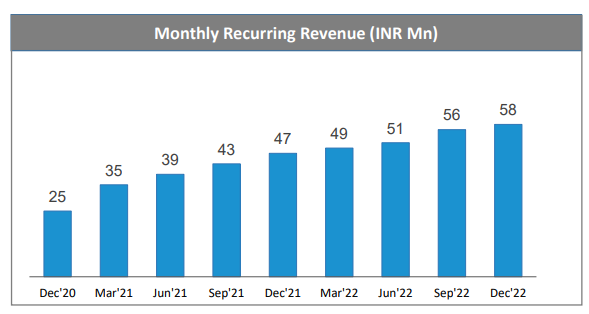

Results seem to be on expected lines. Steady top line and bottom line growth, recurring monthly revenues increasing steadily, and good cash flow. To me it seems like a solid business trading at fair valuations, and growing steadily without needing debt or dilution.

Disclosure- Invested

E2E Networks Investor Presentation June 2023.pdf (6.3 MB)

The latest investor presentation. They seem to be positioning themselves as a AI play. Could they be a beneficiary if AI start-ups in India increase? Slides 19 and 20 talk about this specifically.

Disclosure - Invested

Unlike the big daddy’s (GCP, Azure & AWS), E2E does not have the money power or the expertise to provide AI solutions (read: library of ready to use algorithms, AI/ML platforms, plethora of tools to test, monitor, tweak, provide explainability etc. etc.). So in that sense, AI play is very limited for E2E right now - basically providing GPU infra and Machine Learning deployment and monitoring software.

Having said that, would be of interest to know what the margins they would make on GPUs vs normal CPUs…it should be higher, but difficult to know with certainty as they share very limited data (understandably given their size).

Will they be able to hold and still grow very fasts against the onslaught of global players needs to be seen. Growth has slowed down post the Covid surge and that is also reflecting in share price movement.

Just my 2 cents…on watch list.

This is precisely the question i had as well. They have 2600 clients. But they dont disclose any details. Like data on Clients by Sector, Client using normal CPU vs GPU vs other value added services, etc.

Interested in attending the AGM. Couldnt find any red flag so far. Has anyone else found anything suspicious?

GPU is the future however, the business model does not have a moat here because any company with decent investment can replicate their business model within a year. Reddington could hijack this model? Need to study more about what special they provide.

I have been invested in the stock since CMP was 55. My rationale for investment was not that this can go and challenge any of the existing big tech players or that their business can’t be replicated. But I see counter examples to this theory quite often.

Zoho is a perfect example. Bootstrapped and replicating the product mapped to Google’s offering. A bootstrapped company going $ 1Billion+ offering what Google already does? Seems next to impossible except that it’s happened.

Furthermore, even if we consider Zoho to be an exception that proves the rule, I personally realistically don’t expect this to take on AWS head-on. But all I expect this to do for now is to becomes a run of the mill mid cap company where the CEO/CFO make a quarterly appearance on television like all companies and just … exist. Nothing exemplary.

My play for this company is that I have an in at a market cap of ~ 90 crore. If it does become an average 9000 cr m-cap company, I would’ve 100x my investment. I can live with that ![]() .

.

There are potential boosters dormant like Data Retention Policy, Atmanirbhar Bharat, incidents related to cloud infra hostility with foreign big tech (risk of Russia’s payments being cutoff in the conflict or their infra being confiscated worldwide is a serious national threat) contributing to strong push by GoI to go indigenous.

Great point. It’s unlikely to be the next blockbuster innovative company. Don’t think they have a moat. But they could coexist with Amazon, Azure and Google as a low cost cloud provider. And since it’s a prepaid subscription model, they don’t have cash stuck in working capital. So if they have a reasonably competent marketing team they can grow at the rate the market for cloud computing is growing (estimated to be around 30% cagr over the next few years) without having to raise money through equity or debt. If they do anything more, I’d consider that a bonus. That’s the thesis for my investment in them.

Notable that while Nasdaq biggies are showing some recovery from last year lows - NVIDIA has done very well on NVIDIA AI promise/earnings delivery - 3X returns in a year says something mkt is excited about

https://www.investors.com/news/nvidia-stock-2023-buy-now/#:~:text=In%20Q1%2C%20data-center%20sales,%2C%20Nvidia%20earnings%20fell%2025%25.

recent earnings -

https://www.investors.com/news/technology/nvda-stock-nvidia-smashes-estimates-on-strong-data-center-sales/

interesting to see there are only two partners listed in India under cloud service provider - as of now there seems exclusivity at “competency level”

As we can see NVIDIA AI & compute sub segment only partner is E2E networks - this needs to be validated if thats the lasting case and for how long. Nvidia story theme is on basis of Generative AI & compute power/scale.

High ebdita margins and high growth will attract competition - company didnt seem to have been challenged on defending these yet - tells some credibility in execution, company is not a innovation powerhouse, however a good distribution franchise(high growth biz like NVIDIA and other cloud providers etc) and solid execution can create meaningful scale given their tiny size and large opportunity.

Another point worth noting is the pivot from large ac concentration to de-risk biz, now to many small ac(Jabong used to be their main and large customer) - makes business model more resilient.

Capex intensity for growth and cashflows usually are key areas to watch out for. Management communication has seen some efforts, though lot more details need to be understood on growth strategy, product/service mix, op lvg etc

D - tracking

Now, this could be a complete co-incidence but I had posted before on another forum about the need for the company to upgrade its UI to match the kind of industry and AI focus its marketing. And lo and behold! a few months (quarters?) down the line the website got an uplift. I have also posted about the need to target developers to try their platform and not just target the management. In my experience as a developer, I have been introduced to DigitalOcean, Linode through developer centric communication. And I, in turn, often (based on requirements) suggest these and not default to AWS to my clients. And the latest investor presentation has the slide mentioning targeting AI developers for marketing. Again, it is probable that my thinking is simply well aligned with that of the management but I like that these 2 things got implemented.

I agree on the lack of management view and product roadmap communication. CEO was pretty tight lipped about it in the last concal. Would prefer more info and vision from top management including product wise breakdown of the sales numbers. The limelight is moving quickly bringing E2E to the fore. PR, product, infra scaling better be prepared! A single quarter could be make this stock a multibagger taking PE to much higher level. Although I don’t invest on market sentiment, but if the co gets highlighted like Olectra in the EV space, the short term implications on could be quite volatile.

I am quite happy with the features that are being rolled out every month like the Jupyter notebook for data scientists in June. The NVIDIA preference was mentioned but I didn’t realize that it was this exclusive. Awesome!

The weird part is that even with such a stellar customer base, the company doesn’t become a part of the conversation in the dev community. And this is something I’d absolutely love to see. The company has burnt its hands before with customer concentration risk and is looking for granularity in customer base. If that is so, they should be looking to engage devs and make it lucrative (via UI/UX, referral programs and a free tier) for them to come onboard and spreading the risk.

Why the number of employees growth in epfo site stagnating for last 6 months? It is in the range of 71 to 78 for last 6 months.

Any view on this?

Don’t solely rely on the web pages for this exclusive partner thing. Most of the times company web pages do not reflect fully the partnerships and alliances. this is based on my personal experience where I was researching for something similar and there was big gap between what was listed on web pages of multiple companies vs actual alliances they had on ground.

Updating web page is not first priority, especially when it comes to listing alliances and partnerships.

I am suspecting that promoters are scanning forums (they reached out to me on linkedin 2 days after I made my first post on E2E networks on this forum!)

Anyways, as earlier called out…this is more of infrastructure as a service play…nothing extra special here…it is commodity business, period! There are dozens of Indian vendors operating this space (if not more), though not many are listed or are focused only on cloud services. That is the advantage E2E has from a investor perspective…