E2E Networks is a microcap company functioning in the cloud computing space with a market cap of 114 cr on the NSE Emerge platform. The company had a good IPO with an offer price of 57 opening at 91.

Some financial parameters as on date are shared below:

Founded in 2009 and EBIDTA positive since inception, E2E Networks Limited is India’s #1 Pure SSD Cloud player.

E2E was the first company in India to launch contractless computing, way back in 2009. It has hourly billed pure SSD public cloud and private cloud. Its Cloud Infrastructure has been used by many well-known Indian Startups for their journey from Seed Level to Unicorn Stage and beyond.

Experience in implementing and managing infrastructure for the web, mobile or enterprise-centric workloads have built their (fully cloud agnostic) CloudOps platform, which supports 2,000+ public clouds across the world.

A short note on the financials, business, opportunity and queries is being shared below.

The Good – Financials¬

- Profit making Tech Startup

This sentence is perhaps an oxymoron. True however, the company has been profitable since its inception and building profits at a healthy rate.

Q. What is the determinant of its profitability?

- A growing industry and the company’s differentiated business model focusing on the right target audience (value based products for SMB’s and startup’s). Gartner projected a rate of growth of 30% + from 2014 onwards. A similar rate of growth in cloud computing is projected in the next few years. The industry is in unison that growth lies in SMB’s.

Q. What was topline growth?

Q. Is this sustainable?

- Yes and No. Though it is a small company with a promising product and proposition, operations are in a competitive, complex and disruptive market, thus forecasting would be tricky.

Q. What does the company do with its profits?

-

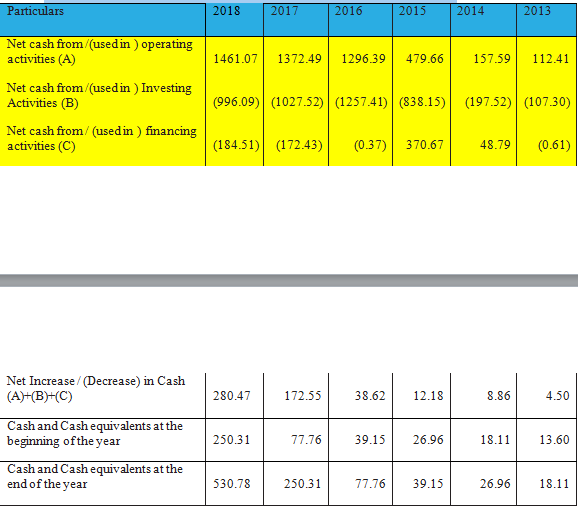

Mainly invests in data centers and computing equipment’s. (in Lacs)

Given the demands of an IAAS model, the company has built up storage by itself and hosts its data on vendor centers and in partnership with vendors. The Company has been spending on its capability to facilitate cloud transitions, offer Hybrid cloud services and build expertise in cloud based transitions and allied services.

Lower cost of service due to learning effects and reducing asset spends with increasing asset turnover has increased cash receipts of the company. The Company is either using this to pay of promoters or parking it in investments. Self-sustainable growth is a determinant which could give an insight into the future profit potential of the company. This is only whence the question of sustainability of the business model of the company is validated.

Though the company had a negative working capital a few years back, receivables have been growing at a high rate over the past 2-3 years

The Bad- Competitive Intensity - {Detailed Risk Analysis]

-

Disruptive Nature of the Industry

The company offers SSD based cloud storage. This may change with the upcoming storage technology of Flash, NAND, 3D Chips etc which are catching pace. This is where the industry is migrating. However, SSD should remain suitable to a small players looking for cheaper cloud technologies. Gauge uncertainty and risk and see where the company stands. -

Elementary Service Model

The company functions on the premise that 80% of the required services can be provided at 20% of the cost. The other services can be paid for by the user on a need basis. Bigger players such as AWS and even Wipro etc provide great customized options and high responsibility of data but they wouldn’t bid or engage smaller clients which fall in E2E’s domain. The only USP the company possesses is price. Company offers significantly reduced prices for cloud services compared to competitors. Well, price is a decision maker, especially for bootstrapped low cash startups (which majority of tech companies are). The question really is whether larger companies would make inroads and compete for E2E’s clientele. I think not. The market is large enough and there are bigger and more funded players who are more apt target customers. How fragmented is the smaller market in that case? -

Regulations and Compliance

Cloud is getting controversial with governments mandating norms for data storage in country of origin. The Indian Governments has expectedly followed suit of EU’s policy and introduced GDPR. While this is prima facie good for Indian service providers with localized data centers, it also faces the issue of high penalties and compliance costs mandated in the Act. Foreign companies are in no mood to desert the Indian market and a host of these players are transmissioning to Indian centers. Would this lead to high costs and advantage Indian players. Maybe temporarily.

Conclusion

E2E is a niche player with a cost based business model growing and sustaining and an impressive pace. A first gen entrepreneur who built the company from scratch through tough phases. With a price to Sales of 2.9 and an average sales growth of 68%, zero debt, sufficient funding to fuel growth post the successful IPO, the company is well poised for growth (Closed listed affiliate is the infamous 8K miles with a dodgy management but impressive financials).

However, the following questions come to mind

-

Are TCS, AWS, Microsoft, Persistent, Wipro, etc direct comeptitors of E2E. If yes, would the company be able to differentiate its product/service from these large pocket players based on target audience/services/costs/size, etc. If no, how intense is the competition in the companies domain and why should it do well than the others?

-

Given the changing landscape in cloud computing (technology and compliance), what is the susceptibility of the company losing market share to larger, more innovative and resourceful players.

-

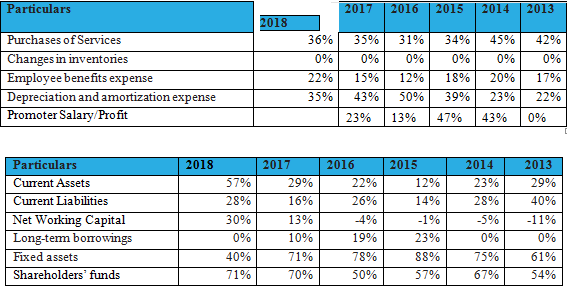

While the management has performed and should be incentivized, promoter salary has been on the higher side. (in lacs)

Note:- Salaries for 2018 are not released yet, but employee expenses have doubled.

Though it was tax efficient for the promoters to draw out money through salaries rather than dividends (made sense before the IPO)and the company was cash rich, should such high salaries be a red flag or a common feature when companies begin to get funded?

- Though the industry is bound to grow, what determinants tilt scales of growth in favor of a cloud company in the industry? What determinants would make it fail? Basically your investment thesis in a cloud company. ¬¬

Disclosure - No Holding

Would love to hear your thoughts.