Dynemic FY21 AGM Notes:

- We have already started Food colour production.

- Dye intermediates expected to start by next qtr.

- Total Capex incurred – 210 crores. Addition in capacity post revised capex is only done in FC. (Earlier estimated addition was 2,520 MT. Actual has been 2,760 MT). Rest everything has been due to cost overrun and delays.

- Earlier there were 3 plants planned. Addition has been plant 4.

- FY22 Estimates - Sales - 265 cr, EBITDA - 51-55 cr, PBT - 33 cr

- FY23 Estimates - EBITDA – 110 crores, 20% + /- margins

- Total Revenue from Dahej - 58 cr for FY22, 330 cr FY22-23 (not additional)

- Total Revenue for FY23 – 550 cr

- Peak Revenue – 650 cr definitely but beyond that depends on market

- We do not foresee any major risk and expect smooth operations

- Dahej plant – peak revenue to be achieved by FY24-25.

- FY22 – CU – 40-45%

- FY23 – CU – 75-80%

- FY24 – CU – 80-85%

- FY25 – CU – 85-90%

- PEAK REVENUE - Revenue – 207-210 cr from Ankleshwar, 38 cr Profit from Ankleshwar. Dahej: 400-450 cr excluding captive consumption

- Products manufactured in Dahej for backward integration will improve the margins

- Interest impact - 1.8 cr on term loans 1.5 cr on WC loans Qtrly for FY21-22

- Depreciation impact - 3.6 cr Qtrly impact

- Debt repayment – FY25-26 to repay the entire debt. 60-65 cr repayment within 3 years.

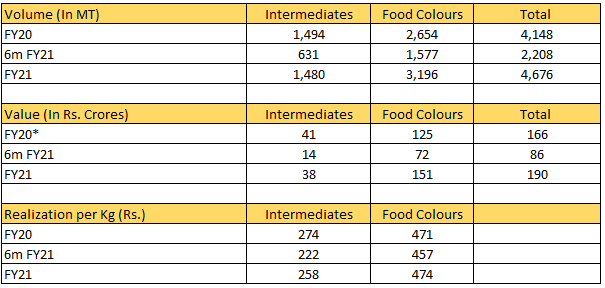

- FY21 Production - 3095 MT FC, 3303 MT Dye intermediate.

- FY21 Sales Volume - 3196 MT FC, 1480 MT for Dye intermediate

- FC existing capacity – 3067 MT. Additional – 2760 MT. Total FC capacity 5,827 MT

- Overall cost overrun is 45 cr – land, building and machinery.

- 60% space in Dahej currently utilized. Balance 40% space in Dahej unutilized for future capex.

- Interest cost 9 cr and Depreciation 18 crores for FY22.

- Interest cost 13 cr and Depreciation 13 crores for FY23.

- Capacity utilization for Q1 FY22 – 82%, FY21 - 87%.

- Do not foresee any pricing pressures.

- Dye intermediates made are value-added in nature. They are not commoditized. Our intermediates are import substitutes of China. Dye intermediates that we are planning to make does not have much competition. Atul is a competitor in this segment.

- Our existing capacity of Allura and Sunset was too small in front of demand. That’s why these FC products were planned.

- Main market is synthetic food colours. Due to pollution, US and other players don’t want to make it themselves. They would rather source it from India.

- When asked about the reason behind cost difference between capex of Dynemic and Vidhi. Management’s comment – “Abhi joh vidhi ne estimated cost bataye hai, sir unhone plant start nhi kiya hai abhi, jab plant start karege aur jab aayege, toh aap dekhna ki estimated cost kya aati hai. These are estimated costs.”

- Additional plant has been set up as well.

- We have already planned for IR.