Added to my position again after reviewing results and price action bumping it to 2.5%. Average buy pice:972

2 Likes

Dipan Mehta has bought 66523 shares in it on 15th Dec.

1 Like

Dipan mehta commodities pvt ltd sold 63823 shares the same day.

1 Like

Sorry, that didn’t come to my notice.

What does such buying and selling on same day mean? Is it like pump and dump?

No. High frequency traders use algos to buy & sell huge quantities on same day to pocket small price differentials. Due to high volumes traded, they make profits even on small difference in buy & sell prices.

2 Likes

Got order from rbi value of 250 crore approximately

2 Likes

Can anyone help me with total order book as on today for this company?

Rating update.

This report gives a number to order book which is more than double TTM sales. Discusses debt levels, payables/ receivables etc. Anyone serious about investing here should go through and understand positives and negatives. No concalls or investor presentations making it difficult to take more informed decision.

However, another announcement that the company appointed an investor relation agency indicates things may improve in this front and company understand its weakness in lack of clear communications. Will they start investor presentations, concalls and if any such changes will rerate this counter is a matter of speculation or some one can try to reach out to investor relations and update here

1 Like

2 Likes

About the Company

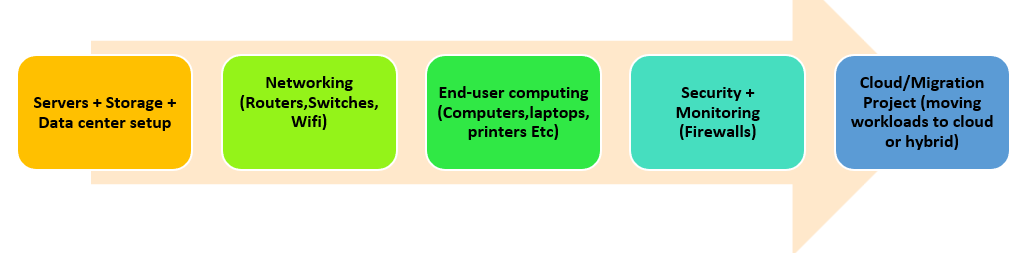

Dynacons Systems & Solutions Ltd is an India-based IT infrastructure and systems integration company that helps large enterprises and government organizations design, build, and manage their technology backbone. It delivers end-to-end solutions covering data centers, networking, cloud, end-user computing, and managed IT services, serving banks, PSUs, corporates, and government bodies across the country. With a strong execution track record, marquee clients, and a growing order book, Dynacons operates a project-plus-annuity model—combining one-time implementation work with multi-year maintenance contracts—positioning it as a scalable domestic IT infrastructure player.

Business Model

Management Quality

- Shirish M. Anjaria (Founder; ~30+ years experience in IT infrastructure & systems integration)

- Parag J. Dalal (Executive Director; ~25+ years experience in enterprise IT solutions, project execution & client management)

- Dharmesh S. Anjaria ( Executive Director & CFO; ~20+ years experience in finance, operations, and IT services management, CA – Cost Accountant)

Financial Snapshot

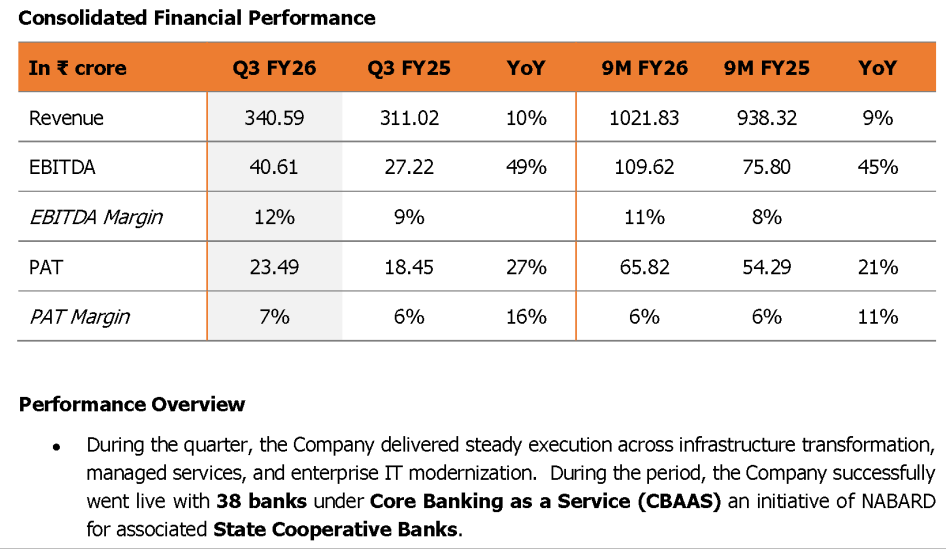

- H1 FY26 Revenue: ₹681 Cr (Jun ₹329 Cr + Sep ₹352 Cr)

- H1 FY26 EBITDA: ₹69 Cr

- EBITDA Margin (H1 FY26): ~10.1%

- EBITDA Margin Trend: Jun 10% → Sep 11%

- H1 FY26 PBT: ₹57 Cr

- H1 FY26 PAT: ₹43 Cr

- PAT Growth QoQ: +15% (₹20 Cr → ₹23 Cr)

- Annualised FY26 Revenue Run-rate: ~₹1,360 Cr

- Annualised FY26 PAT Run-rate: ~₹86 Cr

- Interest Cost (H1 FY26): ₹10 Cr

- ROE (FY25): ~35%+

- ROCE (FY25): ~35%+

Order Book

- ₹233 Cr – Core Banking Solution upgradation & migration on ASP model from NABARD

- ₹280 Cr – Turnkey data centre IT infrastructure augmentation project from Canara Bank

- ₹138.44 Cr – Digital Workplace Solutions contract from LIC

- ₹62.98 Cr – SD-WAN solution order from State Bank of India (SBI)

- ₹19 Cr – Private cloud infrastructure project from Central Bank of India (CBI)

- ₹18.84 Cr – CTS scanners order from Bank of Baroda

- ₹108 Cr – Advanced Core Banking as a Service (CBaaS) order from NABARD (Haryana State Co-operative Bank)

- ₹51.28 Cr – Additional CBaaS orders for State & District Co-operative Banks (NABARD initiative)

- Recent RBI Order – ₹249.51 Cr Enterprise IT / digital platform project for Reserve Bank of India (multi-year execution)

- Unexecuted order book: ~₹2,700 Cr (Revenue visibility: ~2 years at current execution pace)

Positives

- Revenue increased to ₹1,273 Cr in FY25 vs ₹1,024 Cr in FY24 (~24% YoY growth).

- EBITDA margin improved to 8.3–8.8% (vs ~7.6% in FY24).

- PAT ₹72.4–72.5 Cr , up ~35% YoY.

- ROCE 38.9% , RONW 31.4% in FY25.

- Net worth ₹231 Cr ; gearing 0.60x (from 0.23x), still within comfortable range.

- Interest coverage 8.4x ; Debt / EBITDA 1.24x.

- Net cash accruals ₹74 Cr in FY25 vs debt repayment obligation ₹5.8 Cr.

- FY26E cash accruals ₹90Cr , indicating internal funding capability.

- CFO conversion from PAT is around 60-65% (3 year Avg)

- Stock is up 21% in Past 1 Month

- Cash & Bank balance of 85 Cr (H1FY26)

- Management expects double digit margins in next two years

Negatives

No Institutional participation

Working capital remains elevated with GCA ~155 days and debtors ~126 days in FY25; milestone-based billing keeps liquidity tied up.

High utilisation of banking limits (~65% fund-based, ~91% non-fund-based) increases dependence on timely collections.

Operates in a highly competitive and fragmented IT infrastructure market, leading to pricing pressure and margin volatility.

PSU/BFSI-heavy order book exposes the company to procurement delays, payment lags, and execution risk.

Singapore subsidiary reported loss of ~₹129 Cr in FY25 with negative reserves, weighing on consolidated perception.

Conclusion

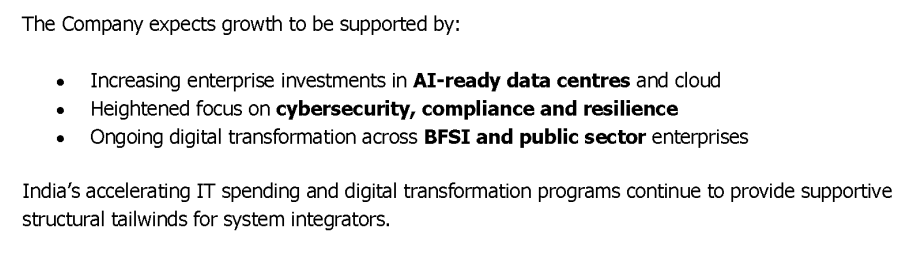

With increasing AI-led infrastructure and digital transformation spending, Dynacons remains positioned to benefit from higher demand for cloud, data-centre, and network modernisation projects. The company has demonstrated strong and sustained order inflows from BFSI and public sector undertakings, providing multi-year revenue visibility. At a valuation of ~16.5× P/E, which is below its earnings growth trajectory and supported by a ₹2,700 Cr unexecuted order book, the stock offers scope for re-rating, subject to continued execution, margin stability, and working-capital discipline.

3 Likes

Order book - ₹2,389 cr vs TTM sales of 1351 crores. Order pipeline 3083 crores (historical win rate of ~30%)

Claims to be wide spread with 1300 locations.

Data Centre and Cloud Infrastructure is now 37% and grown by 68% CAGR since FY21.

Networking and Security now at 13% grown by 77% CAGR

Digital Workplace Solution grows slowly at 8% (now 29% from 65% in FY21)

Managed Services grew by 37% to reach 21% now from 19% in FY21.

They see good tailwinds for system integrators. Margin expansion over the years. (PAT 2% to 5.7%) clearly indicating moving from an equipment seller to high value added services.

Improved debt to equity over the years, reduced net working capital days

Please go through the investor presentation for more details.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/c0ba1729-5145-4525-9b46-40350d520f2f.pdf

Disc: Biased as bullish as I am invested for approx 3.5% of portfolio (added few today). I am not SEBI registered and not qualified to advise. Do your own due diligence.

4 Likes

New order win from Punjab & Sindh bank for 108 crores.

The recent concall was first time as per screener.

2 Likes

The main question for Dynacons to succeed is if it can catch the AI ride. I personally think that most of its current business model will benefit from the recent ai and data centre expansion but some of its revenue can still easily be disrupted by Agentic AI based automation.

IT Managed Services – AI and automation (AIOps) can handle 70-80% of standard IT workloads, such as patching and ticket resolution. This reduces the need for manual intervention, resulting in lower revenue per unit.

Digital Workplace Solutions - Traditional manual tracking is being replaced by intelligent automation. This reduces billable hours for manual audits but if the company is able to integrate AIOps in their solutions then it can create a new revenue stream for them.

Work from anywhere can also easily be set up by AI instead of relying on 3rd party integrators like Dynacons.

Overall, the good thing is that Data Centre and Cloud Infrastructure plus the Networking and Security segments are growing at the fastest pace. While AI automates away their manual “hands-on” revenue, it simultaneously fuels the massive infrastructure build-out they specialise in.

Key thing to look out for will be their service v/s product revenue mix - the shift towards higher-margin system integration in Data Centres is a sign they are winning the pivot.

Disc: Tracking

2 Likes

₹750.82 crore Reserve Bank of India (RBI) order announced in early May 2026

The ₹750.82 crore order is massive relative to Dynacons’ market size

This single contract for private cloud infrastructure is the largest in the company’s history.

Before this announcement, Dynacons was sitting at a market cap of roughly ₹1,500 to ₹1,600 Crore. A single ₹750 Crore order represents roughly 50% of the company’s entire market capitalization

The RBI deal is a 5-year contract to set up, implement, and completely manage the Private Cloud Infrastructure for the RBI’s new Next-Generation Greenfield Data Centre in Bhubaneswar. For institutional investors, if Dynacons can clear the RBI’s notoriously strict security, compliance, and execution audits, it completely de-risks the company’s profile for winning future mega-deals in the BFSI and government sectors.Their unexecuted order book is now well over ₹3,000 Crore.

The stock’s short-term moving average crossed above its long-term average

On May 13, 2026, Dynacons was included in the Financial Times High-Growth Companies Asia-Pacific 2026 list for the fifth time.

Strong operational metrics, including a Return on Capital Employed (ROCE) of 33.3% and a low Debt-to-EBITDA ratio (1.39x)

attractive target for fundamental investors looking for growth at a reasonable price (PEG ratio of 0.7)

Note: Not investment advice. Biased, invested at 1000 levels.

4 Likes

The stock continuing to do well, making it best performer in the portfolio on back of major order win from RBI. I expect the margin expansion also to continue as the company executes bigger orders.

Disc: approx 2.5% of PF

1 Like