It is to check if the company is getting cash soon or if the cash is just getting stuck in receivables. Companies which get cash faster can reinvest back in the business faster, these companies are more attractive relatively.

2 Likes

Gr8 and thanks so much for your kind reply.

Is there any ideal value for this ratio or just the higher the better. I mean how we compare between multiple companies and industries, keeping this as a parameter for high value companies analysis.

| 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

|---|---|---|---|---|---|---|

| 12 | -6 | 21 | -4 | 29 | 39 | 91 |

| 24 | 28 | 30 | 29 | 31 | 56 | 198 |

| Ratio | 0.45959596 |

Is this a good company?

1 Like

I look at this to see if there is any fraudulent accounting. In the past, companies have declared profits, however the cash never arrives. Ideal ratio for me is CFO to EBITDA to be around 80%, but as you indicated it depends on the industry. Some companies collect the cash up front and provide services later, those are the best businesses

4 Likes

Thanks for your feedback and guidance ![]()

1 Like

Typically for good B2C companies, the ratio could be 80 % and for B2b companies 70 %.

1 Like

but looks like even money from 2020 has not been received. cash from operations is abysmally low

1 Like

It depends on the type of business. If a company is in a B2C business that is it sells its products directly to customers CFO/PAT should be north of 0.7

If it is in a B2B business(selling its goods to another business or government) 0.5 to 0.6 is a decent number.

1 Like

This seems to be genuine issue. I checked Sept 2022 results also to see if same high EPS is reported, and it is.

But the screener shows lower number there, not sure how they got that, most probably they calculate it and don’t rely on posted EPS number.

Will avoid this company because I feel this is a serious blunder.

@james_kerala do you have any views on this company now? I have recently started tracking this company, looks an extremely interesting space and the return ratios are very interesting, however I am not sure if there will be PE rerating at 31x?

Then it all relies on how quickly it can grow its earnings, considering they do not enter in export opportunities and margins stay the same.

Please correct me if I am wrong. Thank you

Great to hear from you and thanks for asking.

After recent great results and some correction, I had a look at it appeared on a screen for very growth companies. So I took a tracking position of just 0.3% of PF now again here. I had missed a great run earlier.At PE 31 and PB above 10,( PBxPE 327 as per screener) I am not expecting any great PE re-rating as it is trading already at high valuations. But I can be wrong as market is not always don’t behave as we think. But remember small and micro caps Trading at very high historical valuations in this peak bull market. So any delay in order flows or revenue compounding or overall market correction it can de-rate as well. Recently they got a decent sized order again from a bank. So now going looks good and I may buy more if valuation cools down little more or results continue to amaze me.

1 Like

Hi James, thank you so much for your insights.

I guess you and I sit on similar page, where even I hold apprehensions of the valuations whilst I have no doubt on the capability of the company to post profits.

Also, what would be an ideal PE x PB if you would want to re-enter this stock, I understand it is not a rule, but a range according to you

1 Like

If you look at Stock price CAGR vs Profit/revenue growth CAGR, you can see that the stock price went ahead of profit growth, thus it already undergone re rating.

Generally I am very happy if company gives clear growth forcasts or if company already appears to be undervalued. Since both are not clear here, this will remain more like a trading bet where I like to protect my downside using a stop loss and sell when I feel things are not working well for stock price (like price going below 50 DMA). If company starts investor presentations or concalls we can be more sure, but now that’s not there and only annual reports, rating agency reports and order wins/announcements only source to know what is happening

Yes, even I feel company should start with con-calls & Investor presentations to gauge more interest and trust from shareholders.

However, great insights sir. Thank you very much

Why company have high Receivable and inventory year after year?

1 Like

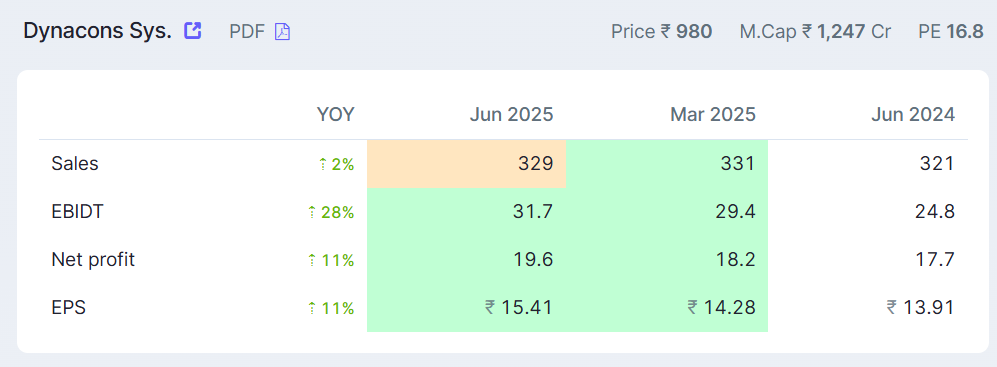

Any view at current valuations of 16x PE TTM??

It looks attractive to me and I am adding already and brought my allocation up to 3.5% of PF (I consider 0.5% as Trading side which I may sell for 10-15% upside).

PE & PB below 5 year median PE & PB. Also close to long term support levels of 950 range and I believe the stock should find aupport here.

I do not see major downside and I believe DSSL need not follow typical IT stock trajectory. However, I can be wrong and do your own due diligence

Disc: Invested at an average of 1040, so now at notional loss. I am not a SEBI registered analyst and views are for educational purposes only.

1 Like

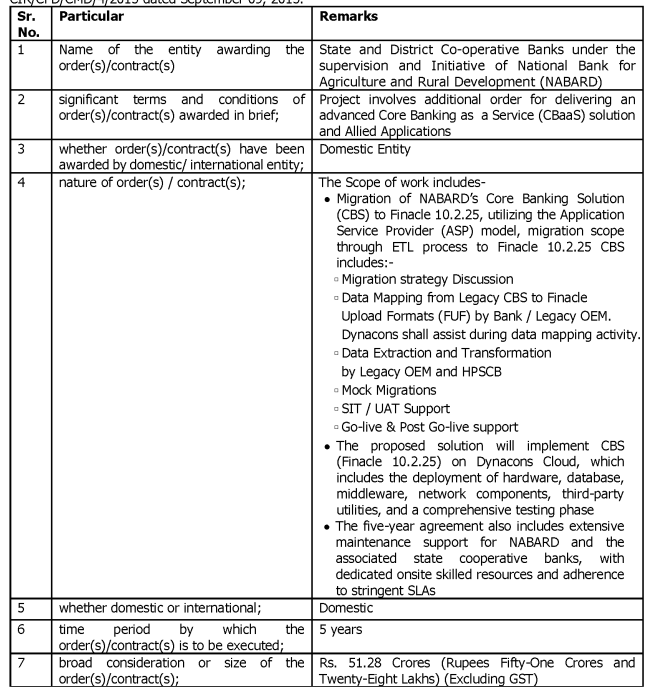

50 crore order win.

May be good to see some news when I expect the stock price reached the support and hopefully start reversing.

Yes. Good news. But the size of order is only 51 Cr. Thats not much.

1 Like

Update: The support in HLC bars looked at 920-930 range, so i waited and saw it closed decisively below that on thursday and went further down today, making a weekly close also below previous expected support. So i exited significant portion at loss, making my position close to 1.5-1.6% of PF.

Disc: I am not a SEBI registered analyst and views are for educational purposes only. And i analyse stocks only at superficial level.