BUSINESS BACKGROUND

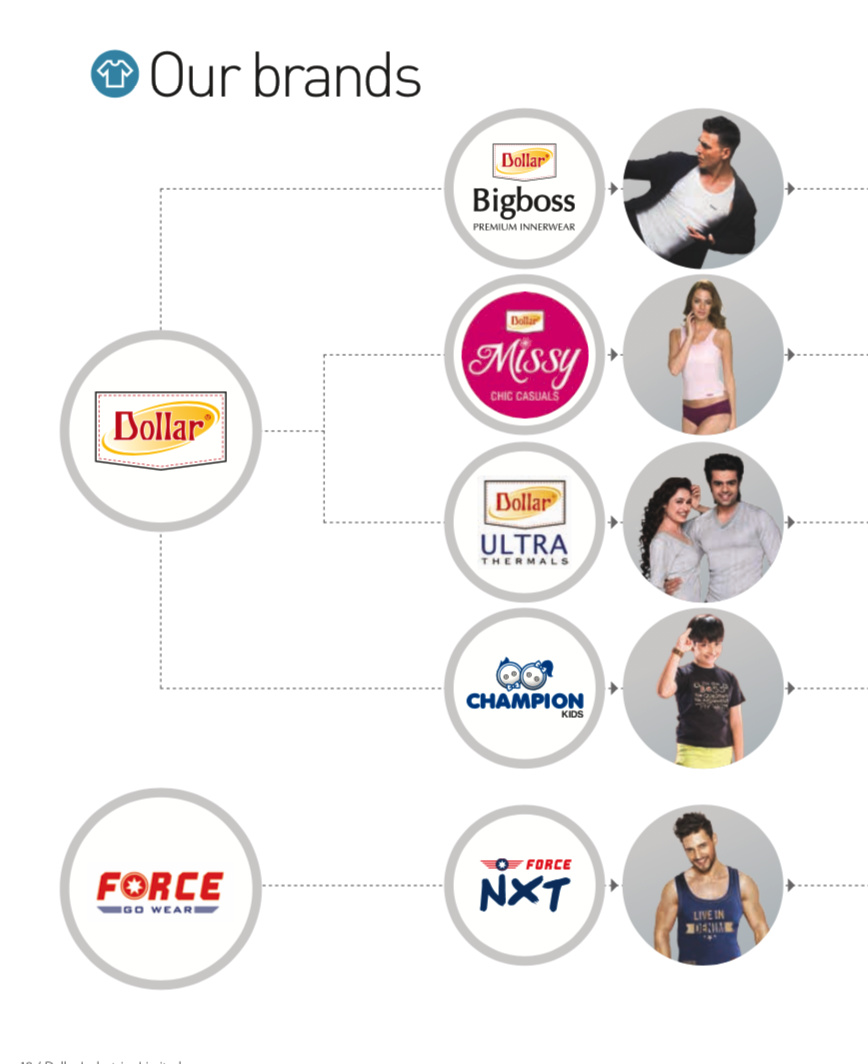

Dollar Industries Limited was promoted by Dindayal Gupta under the name Bhawani Textiles and now has created substantial presence in India under the Dollar umbrella. Dollar is present across segment in innerwear space with its brands Big Boss, Force NXT, Missy, Champion, Ultra, Force Go Wear, Economy range etc. Dollars manufacturing facilities are located at Kolkata,Tirupur, Dindigul, Erode, Delhi and Ludhiana. It has fully integrated facility at Tirupur with presence in spinning, knitting, processing, cutting,stitching and packaging and caters to high end products.

In the past three years, it increased its distribution from 750+ distributors and 70000+ MBOs to 850+distributors and 80000+ MBOs.

A brief from the Annual report:2017

It took us more than 40 years to get to nearly C1000 crore in revenues; we are now driving the Company to achieve the next C1000 crore in just seven years. At Dollar Industries, we recognize that this challenging target will only be achieved if we outperform our sector, with respect to our peers and our retrospective average. And this extensive outperformance will only be achieved if we run our business in a different way from how we have done so until now.

So the big question is: how differently can we run the business in a conventional sector? Where is the room to reinvent our business model?

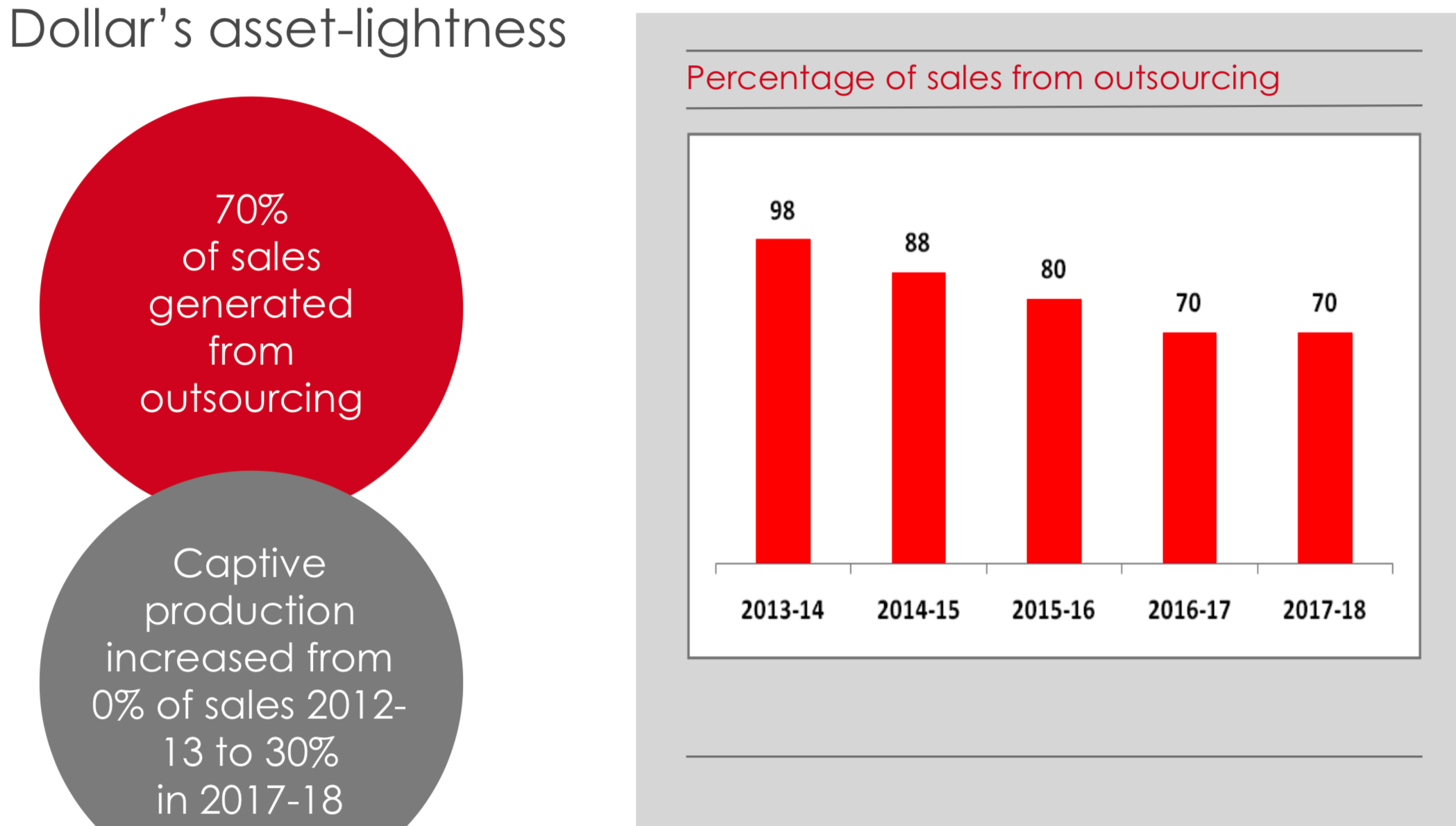

We were engaged in asset investments that extended our value chain; we seek to emerge asset-light, increasingly preferring to outsource products from like-minded quality-driven manufacturers.

We were a Company that marketed products through traditional distribution networks; we are investing increasingly in modern retail formats to enhance our respect, margins and visibility.

We were a Company that selected to grow patiently through the organic building of our business; we are prospecting inorganic investment opportunities in brands and distribution networks driven by visibility, volumes and value.

Dollar enters in to a JV with PEPE for branded innerwear products:

Dollar Industries has entered in to a JV with PEPE Jeans of Europe which will be a 50:50 joint venture and will involve a capex of Rs 250 crs and be valid for the next 1o years on a exclusive basis for catering to markets like India, Srilanka, Bhutan, Nepal, and Bangladesh.

This partnership under this JV will require Rs 36 crs to be invested each by both partners that is Dollar and PEPE over the next 4 years and the rest will be funded by banks and working capital loans. Dollar expects that it will be in a position to launch these PEPE branded products in the domestic markets by March 2018 (As per last Concall product launch should be around July 2018)

These products would be marketed under the PEPE Jeans London brand here. The products made here will include innerwear and loungewear categories like gym wear, track suits, and sleepwear.

Big Boss new ad: featuring Akshay Kumar, contract with Akshay Kumar is recently extended for next 3 years.

Dollar Big Boss New TVC - HD 40sec - YouTube.

Missy new add: featuring CHITRANGADA SINGH

DOLLAR MISSY NEW TVC 2018 :: CHITRANGADA SINGH :: CARRY ON MISSY - YouTube.

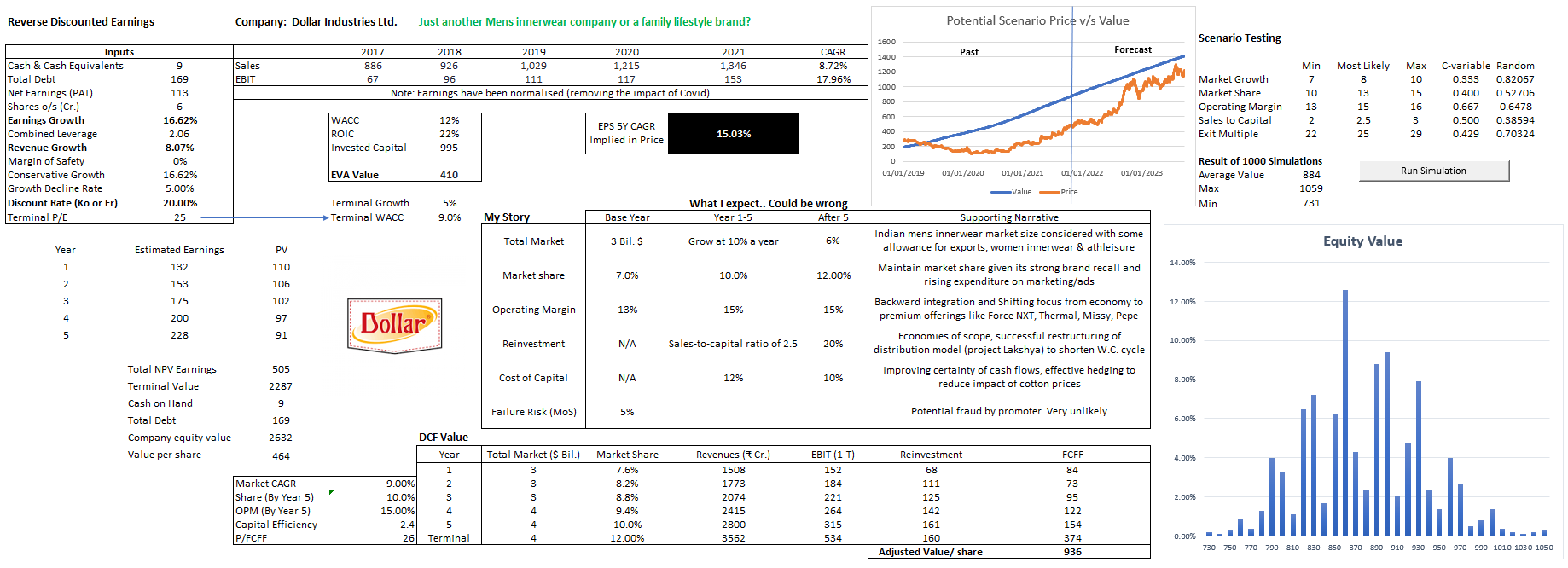

Valuations:

The company was listed in April 2017, Stock hit 52 weeks low during last few days.

Its a consumer business and growth stock, not a value buy @31 PE Multiple.

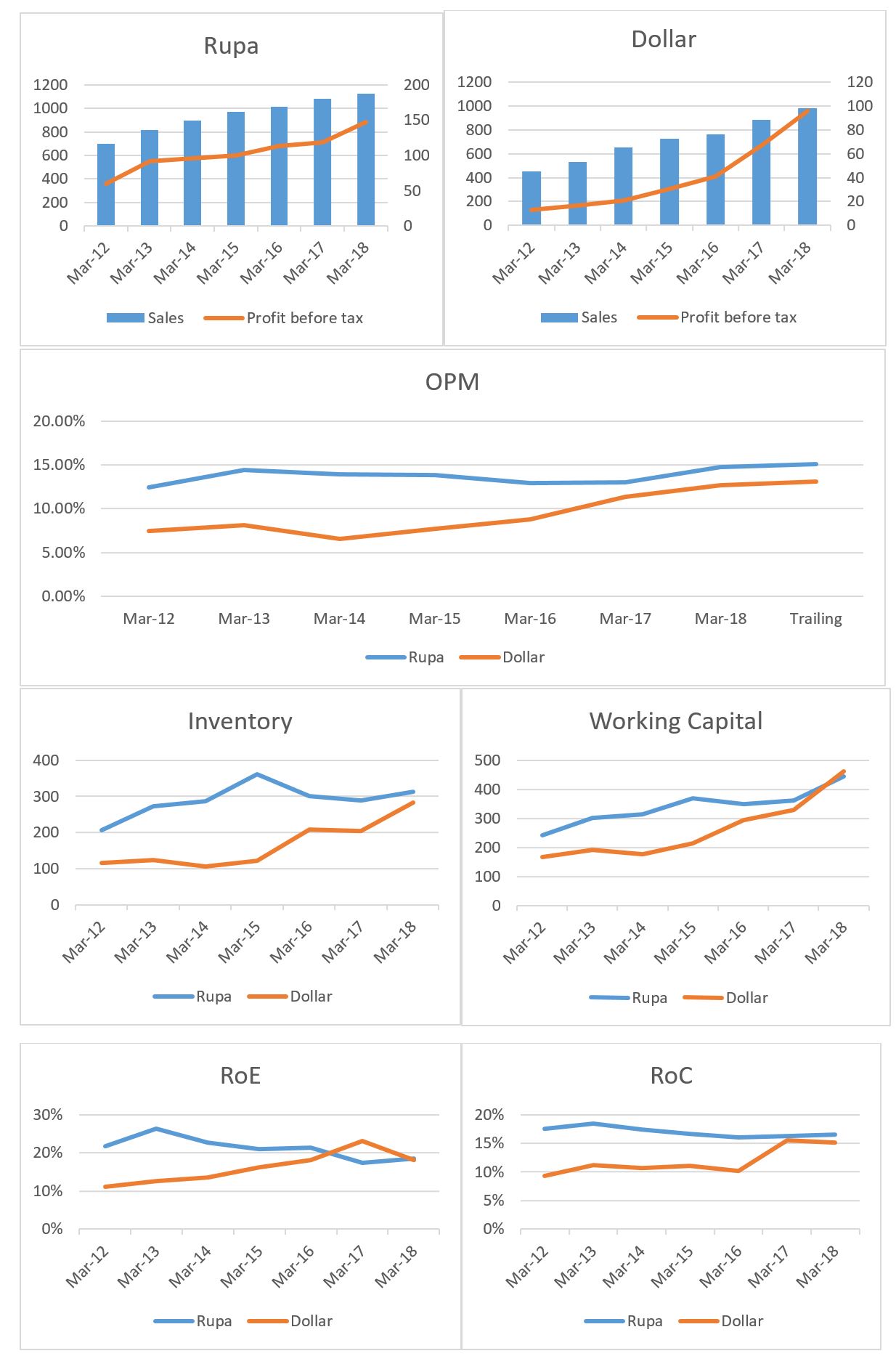

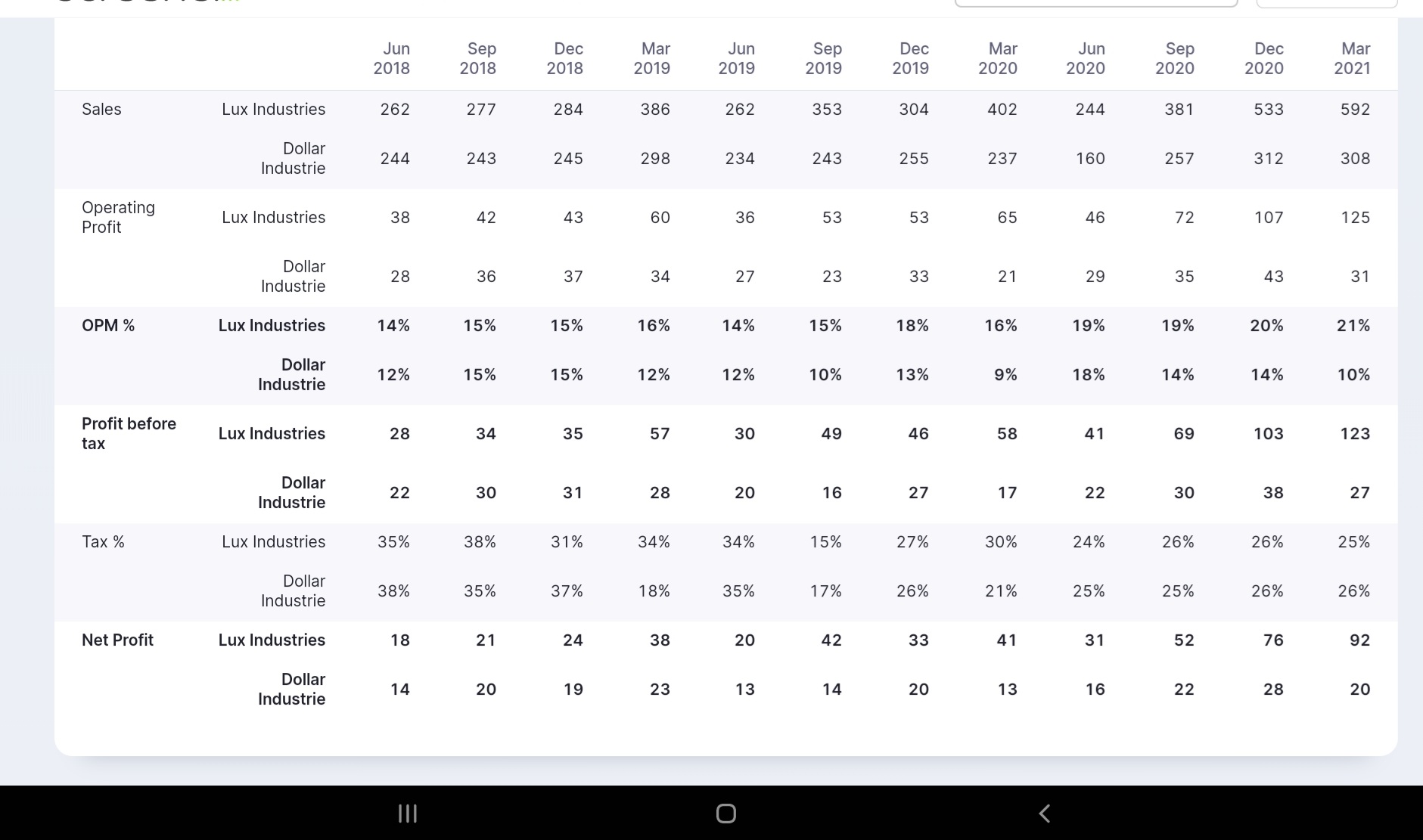

Peers like Rupe is trading @37X.

Page industry is in another orbit, so it’s not a comparison with Page, but Dollar is being ambitious after the JV with Pepe & new brand launch + ~86cr of Ad spending, rest only time will tell how things turn out.

Investment Rationale:

-

Overall the Innerwear Market is likely to grow at a healthy pace.

The Indian innerwear market is currently estimated at Rs. 24,000 crs. The segment has grown at 15% during the period from 2010 to 2015. During this period, the share of intimate wear in the total apparel market increased from 6.4% to 7.1%. The innerwear market is estimated to continue at the same growth rate over the next five years and expected to become a Rs. 47,000 crs market which is nearly 8% of the total estimated apparel market, by the year 2020. -

Unorganized to organized shift beneficiary:

as currently, almost 65% of this market is unorganized, as aspirations are increasing branded products will gain market share.

New retail(Online + Organized retail) to support branded sales. -

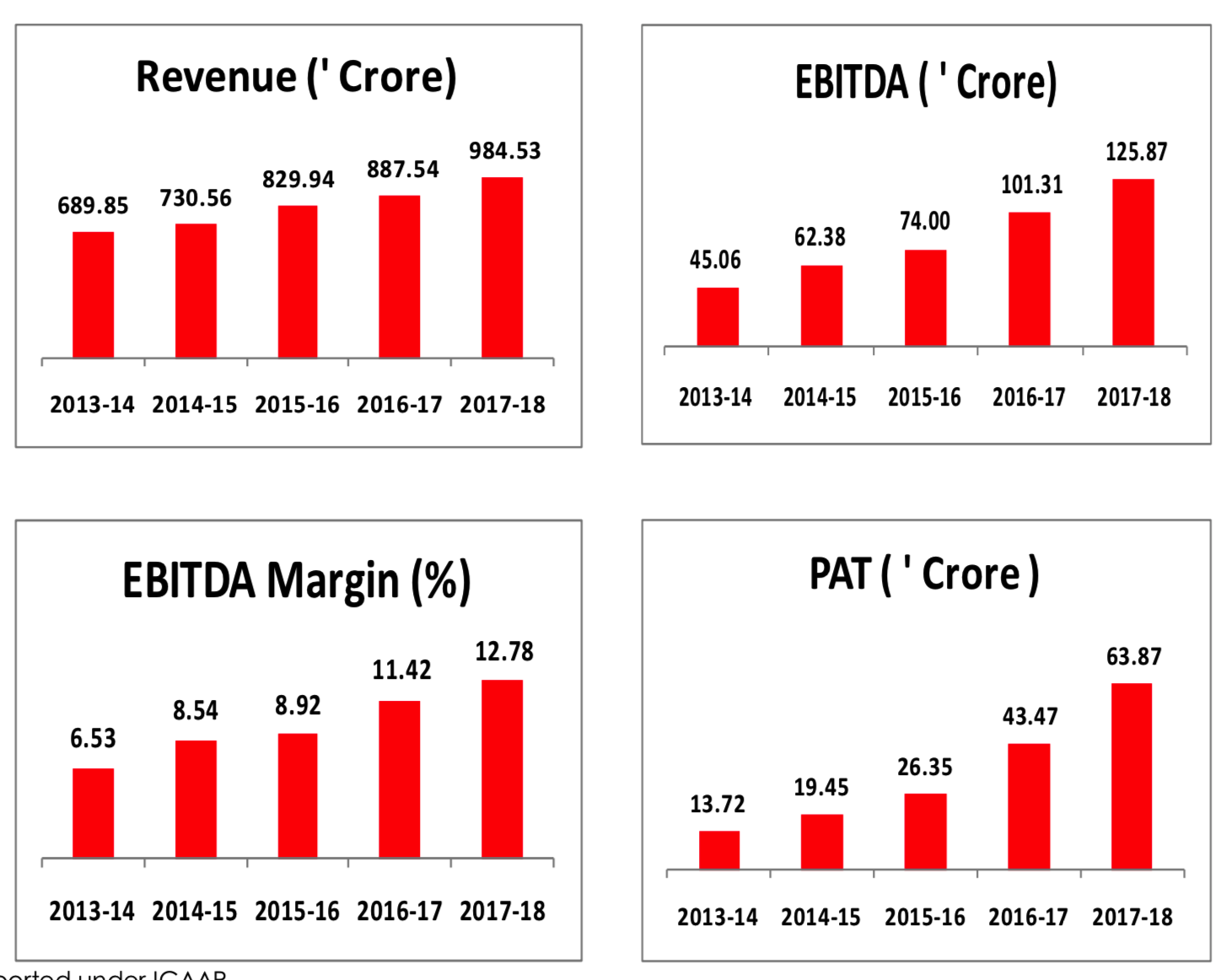

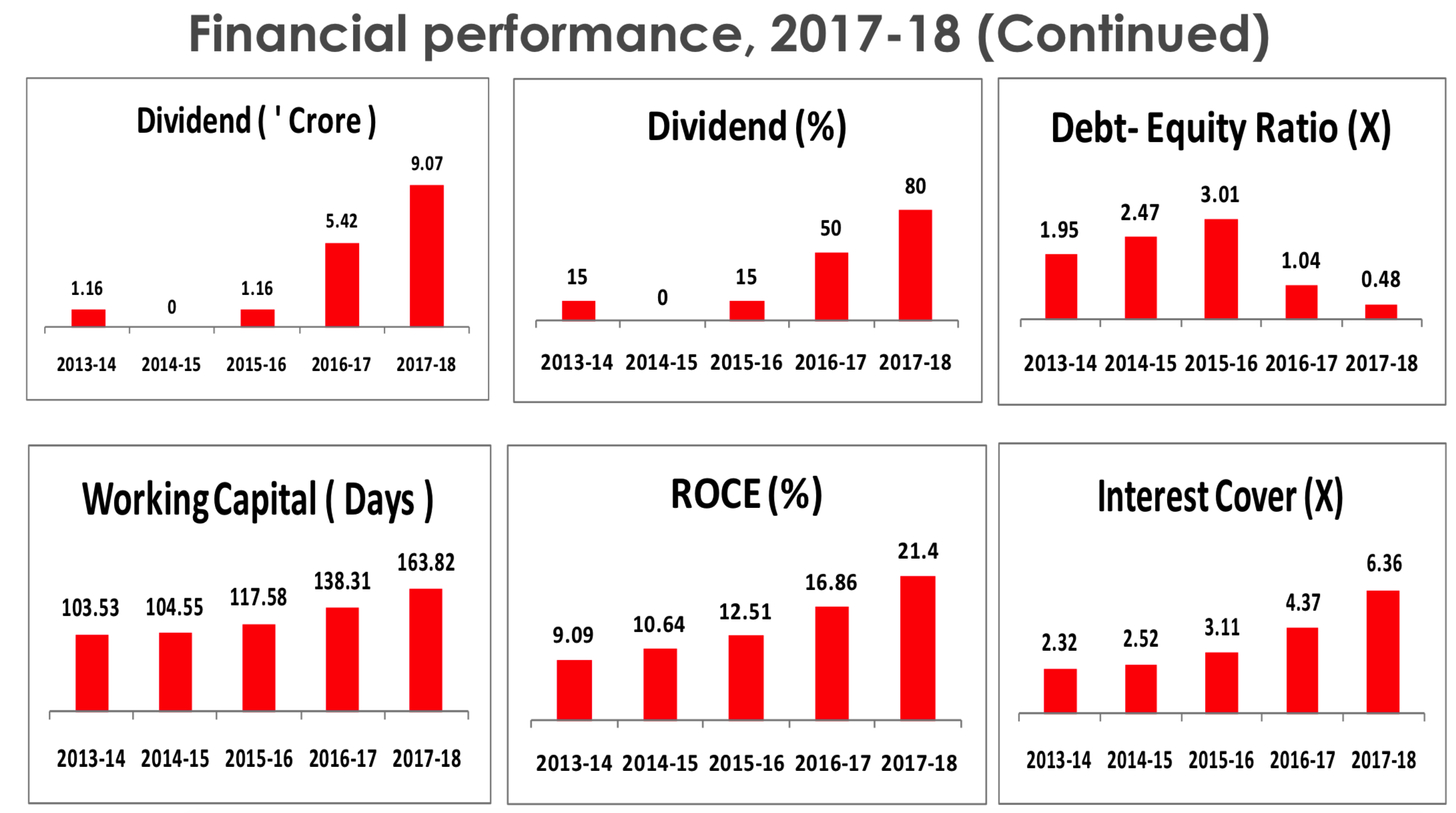

Healthy performance across all parameter’s, sales, Margin, PAT, ROCE all are improving and debt is going down, however working capital days has deteriorated after GST, which need to be monitored, although management assured to reduce the same as per concall.

-

Dollar enjoys a wide distribution network which is very important in this business.

-

Premium products to drive EBITDA margin improvement:

Going ahead focus will be on scaling up ‘Force NXT’ & ‘Missy’ brands.

Dollar has traditionally been present in the economy and mid-premium segment through its Dollar Regular (Realization Rs 35/piece) and Big Boss (Realization Rs 62 per piece) brands with 34% and 44% revenue contribution, respectively. It is now focusing on super premium category with its brand Force NXT (Realization Rs 114/piece) launched in August 2015 and which contributed 2% of FY17 sales. It aims to grow this brand focused on the aspirational segment to over Rs 1 bn in next 3 years and would go for aggressive advertisement to position it. Further, Missy is expected to do well with women innerwear and leggings. -

Robust ad spends:

Dollar is one of the highest spenders (10% of sales) on advertising among peers Page, Rupa and Lux (4%, 8% and 6%, respectively). Dollar is also planning to maintain advertisement spend run rate at 8-10% of revenue in future as well. Of the Rs 86 crs expended in FY17, around Rs 40 crs was on TV, Rs 20 crs was spent on newspaper medium and the balance on outdoor activities. Dollar has roped in celebrities to promote its brand in 2010 wherein Akshay Kumar was brand ambassador

Risks:

-

Valuation risks, as stock is trading at 31PE, hence no margin of safety.

-

Pepe jeans JV: product launch is already delayed by 4-months, may get delayed further.

-

Pepe jeans JV: Joint ventures always have the risks of failure & conflicts.

-

Increased competition from peers like Page Industries, Rupa & Company, Lovable Lingerie, may affect performance.

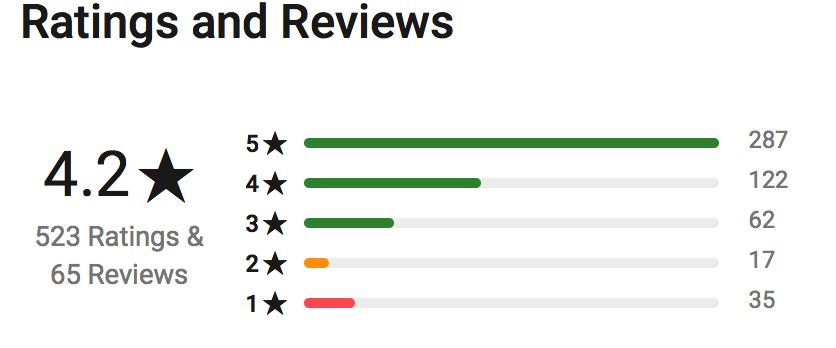

Product Reviews:

Reviews are good on both Flipkart & Amazon, I have used dollar products and quality is good.

Disc: Tracking position @340, I don’t have much understanding of finances, this post is not a recommendation, the intention is just to start a discussion and have other member views.

References:

-

Earning Presentation:

DOLLARINVESTORREVISED.pdf (948.1 KB) -

Brokerage report

Joindre_Capital report on Dollar Ind.pdf (455.4 KB) -

Distribution channel Interview-Dollar industries limited

- YouTube.