Q4FY22 Concall Notes

50th year of operation

Revenue: 1356cr; dividend 3

Ad

-

Prinicpal sponsor of RR IPL Team

-

Signed Yami Gautam for Women’s wear

Breakup; Vol Growth was 9% though in Q4 there was degrowth of 2%.

-

Big Boss: 43%

-

Regular: 35%

-

Missy: 8%

-

Thermal:7%

-

Force nxt: 3%

-

Force go wear: 1%

-

socks : 1%

-

Champion (junior): 1%

launched bra in UP and east india

WC days: 154 from 178 days

Debtor days : 99 from 121

Average realisation rs65

FY2025 plan:

-

Revnue: 2000cr

-

70% distributors under project lakshya

-

120 EBO

-

Women’s Bra could be 20-30cr revenue

Capex: 70-80cr thisyear

Integrated warehouse and spinning mills to coplete by Nov 22.

Plan to open 25 EBO this year

Exports: focusing on Africa market in a big way

Disclosure: Invested

Does anybody know how to track historical cotton candy prices in India?

This link provides current prices and a short history only - Cotton Rate, Today’s Cotton Price in India: Cotton News on Economic Times

All the hosiery players are having a very tough year due to incessantly falling cotton prices. They have been holding higher inventories while the sales price realizations have dropped in line with cotton prices. This has squeezed their margins significantly and also caused a volume stress due to distributors not wanting to take on additional stocks.

The reverse of this will happen when cotton candy prices start going up.

March 23 Concall notes

- Volume growth of 37% in this quarter, Value degrowth by 29%, revenue growth of 8%

- Ad expense of FY23 was 101Cr , 7% of revenue

- The premium segment and women segment had a volume growth of 15% and 10%

- Opened 14 EBOs this year.

- Modern retail ( e-commerce ) showed a volume growth of 33%

- Contribution split: 42% Big Boss, 37 % Dollar Always, 9% Missy (women), 6% dollar winterwear, 4% Force NXT (premium)

- Further margin reduction in this quarter is because of the 4-5% price reduction and high-cost inventory. Cotton candy in Feb was at 65k/Kg , currently at 55k/Kg. Yarn prices however have not reduced.

- Management believes that COGS and margins have bottomed out

- Price cuts were only 4-5% but value degrowth of 29% was because of the higher growth in economic product (dollar always). 53% growth in dollar always, 14% in big boss

- Ad spends in FY24 will be 6.5% of revenue

- FY24 guidance: revenue growth of 12-13%, EBITA margins of 11-12%

- Raw material split: 20% cotton, 80% yarn, and fabric

- 20% of yarn required is manufactured house, this is used for the manufacturing of premium segment

@nirvana_laha you can check the historical cotton prices here

Yarn prices are of more relevance as far as dollar is concerned, cotton only comprises of 20% of their COGS.

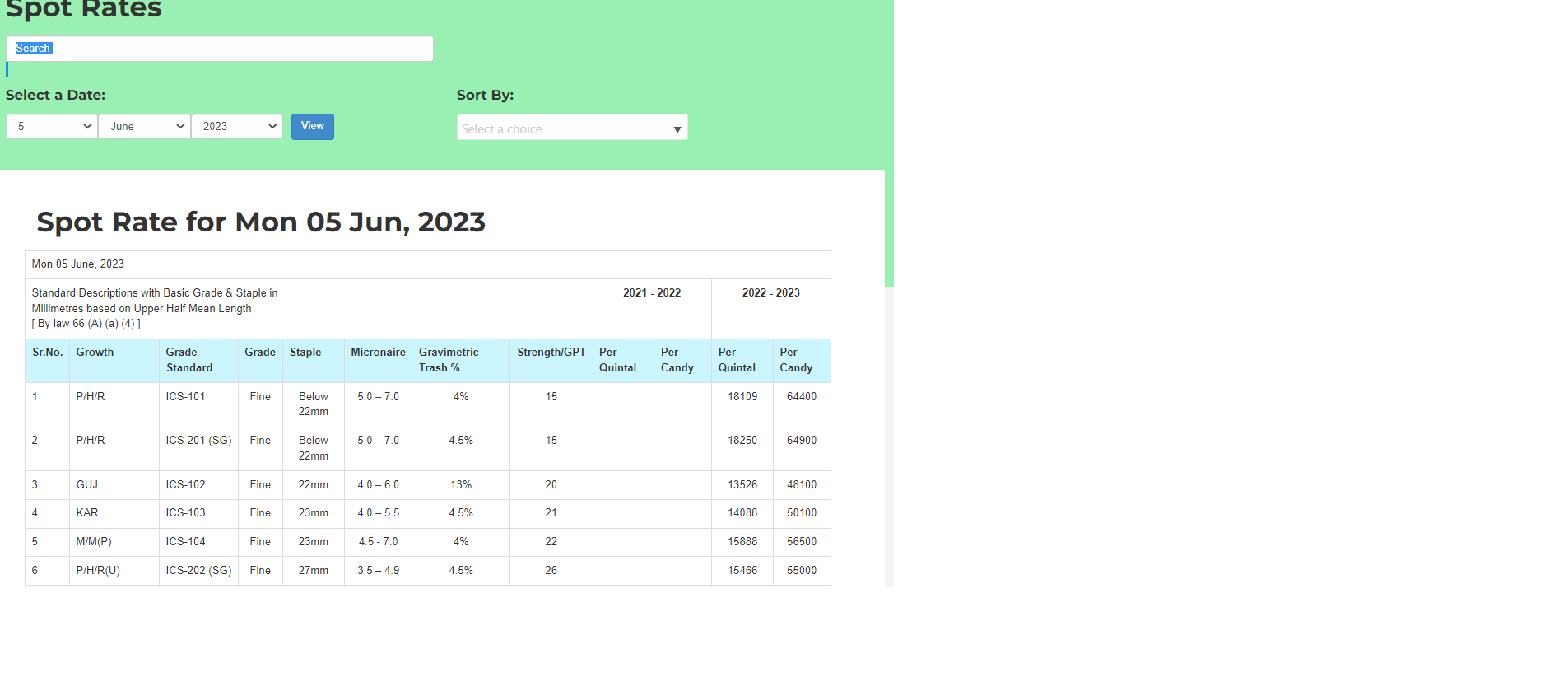

cotton association of India is superb source to track this data. Below is the link for the same;

https://www.caionline.in/site/spot_rates

We can track the data backwards till 2012. Data is also available statewise and based on cotton grade, staple etc…as shown in the below pic.

As per Page Mgmt Commentary - “Too much ongoing offers/schemes in the marketplace by competitors to liquidate their inventory | Page inventory is 3+ months whereas competitors inventory ranges from 9~12 months”. I believe this is the reason for value de-growth.

I think there is a deep structural shift in Dollar Industries currently underway. The gravity of this shift has been missed by the broader market.

Claim: Dollar Industries has the right to win distribution model in the industry, and the growth / return ratios may look very different in the medium term.

Legacy Distribution Models

There are five innerwear companies that operate in the economy segment - Rupa, Dollar, Lux, Dixcy and JGH (Amul Macho). These five have conventionally used a traditional distribution framework.

Here, a company produces products at their factory, and then gives these products to a distributor. Distributors then make a small margin and pass on the products to a customer facing retailer. These distributors usually make 6-8% margins, and are given 3-4 months of credit before they need to pay a Rupa or a Lux.

Now, these companies often have no visibility on their end customers beyond the distributors and have no control on the particular SKUs that are being sold. They keep sending products into the channel, and hope the market absorbs the supply. On the distributor’s side, one distributor may cater to 2-3 brands, and will push the product that gives them the highest margin at the time. There is also no organisation between the retailers a particular distributor sells to, so you may have more than one distributor selling to a retailer.

During periods of downturn in the industry, this messy distribution model turns ugly. Distributors start undercutting each other, and margins fall from 6-8% to 2-3% seen in the last year! Companies like Amul and Rupa have also tried to cut down their working capital, and have demanded their money back from distributors within 21-30 days! As a result, distributors are squeezed at both ends, dissatisfied, and the inventory turns have suffered.

Dollar’s Distribution Model

In 2019, Dollar started a pilot project to implement a completely different distribution model. They mapped out all the retailers in a particular area, and mapped these retailers to a particular distributor. They gave distributors fixed margins of 6-10%, and implemented a system to track inventories, particular SKUs, and would know which part of the country needed replenishment.

They also took charge of the demand generation entirely, building a large call centre, where they regularly do a lot of ground work in reaching the retailer, telling them about promotions, etc. This means the distributors don’t have to undercut each other, don’t have to lower their margins, but instead focus purely on distribution, and are incentivised with things like loyalty points.

The benefits of this system are obvious: less stress on the channel, controlled levels of inventory, control over the SKUs that are pushed, visibility and data on the end customer, and distributors that are happy and empowered with stability, and extra incentives with the reward programme.

From scuttlebutt, I believe this model has been incredibly successful. In Rajasthan, they were able to double their market share in 2-3 years, and have since been replicating this in other states. Today, some 20% of the distributors have been brought under this model.

Proof in the Pudding

If you want to read about Dollar, the annual reports are the place to start. If you want to understand Dollar, search for @ankush12495 in each of the concalls. He’s done some brilliant work, and has been first to this idea, I believe.

In various calls, Dollar has given numbers on the difference between the old distribution network and the new one.

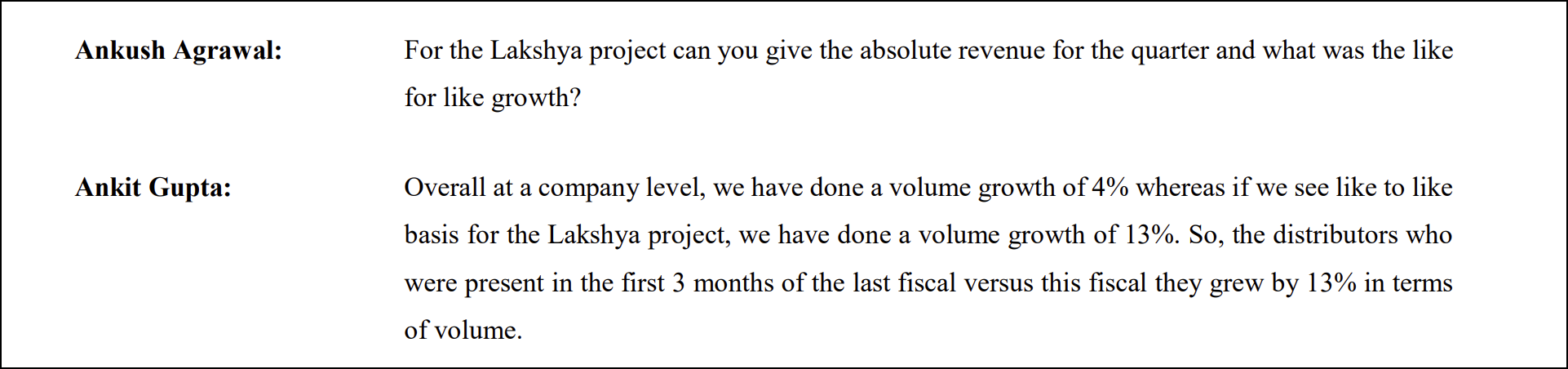

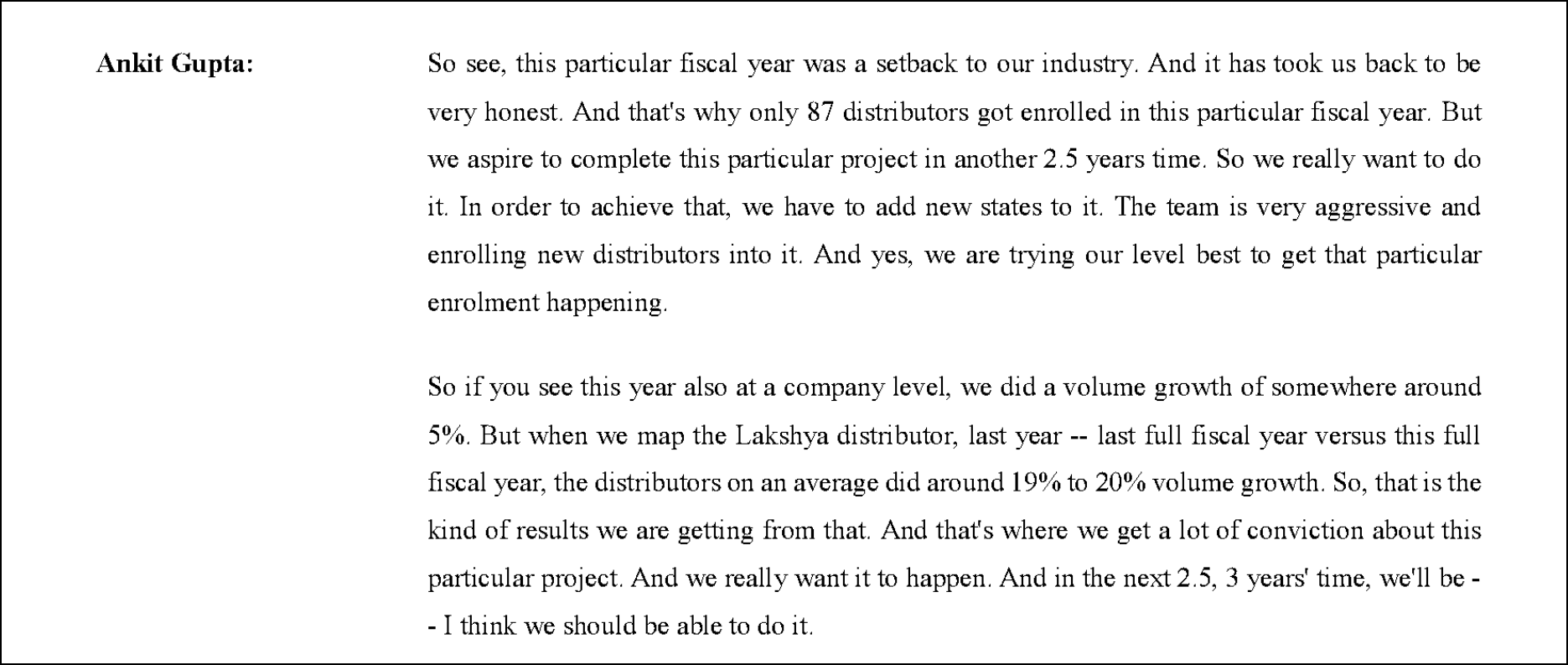

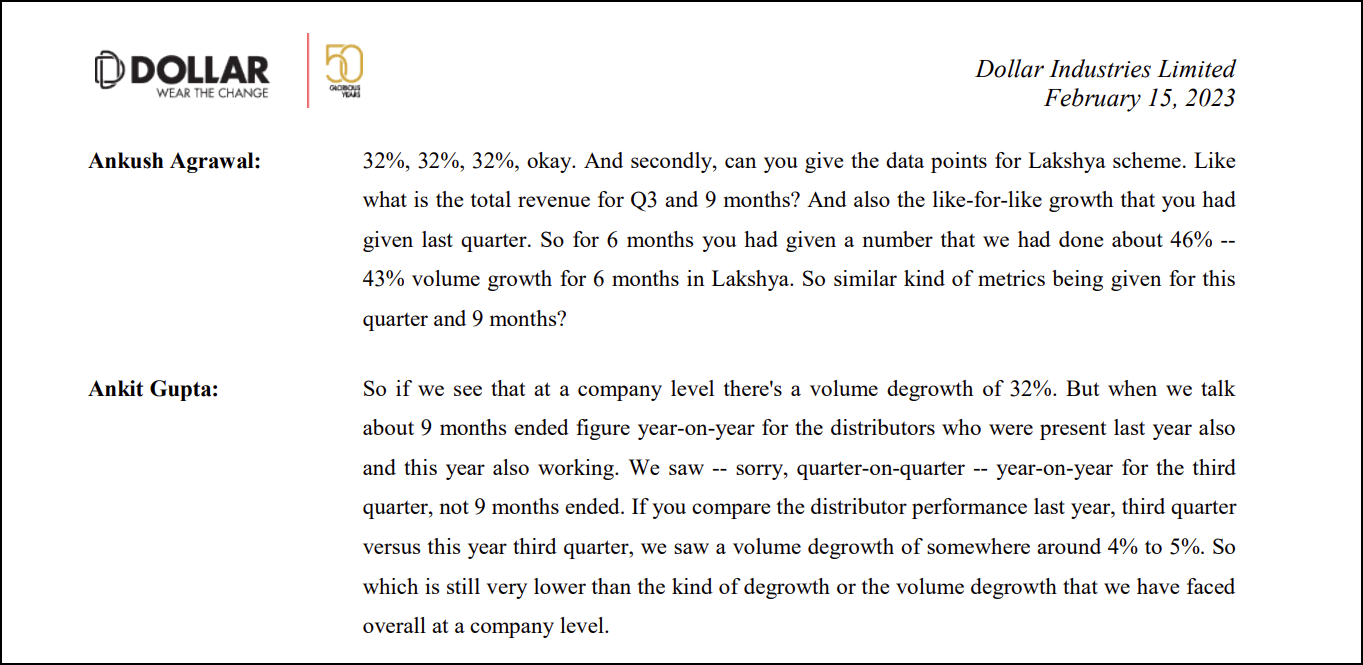

Q2FY24

Q1FY24

FY23 vs FY22

Q3FY23

The new distribution model has outperformed the legacy model by double digits in volume growth. The most dramatic data point is in the last image, where the company’s volumes fell 32% YoY, the new model only lost volumes by 4% in the same period, an alpha of 28%.

What makes a moat?

Dollar has spent 4 years in bringing nearly 300 distributors on to this new model. They’ve explained that it is a very careful procedure that needs to be done, taking 3-4 months to bring on a single distributor. They cannot interrupt ongoing sales as this would lose market share, and therefore the roll out is very slow.

Bringing more distributors under this model is vital to capturing market share, improving the return ratios, etc. By my estimates, at their current pace of adding 100 distributors a year, the contribution from the new distribution model will look something like this:

| Year | Percentage of Distributors Under Lakshya |

|---|---|

| FY24 | 30% |

| FY25 | 40% |

| FY26 | 50% |

| FY27 | 60% |

| FY28 | 70% |

Because the number of distributors under this model is still only 25%, we don’t yet see the benefits of Project Lakshya in the numbers. However, once we cross FY26 and the majority of distributors are brought in, things can look very different.

This is exactly the sort of thing that moats are built out of. If it takes 10 years to roll out a complex change to your distribution model, it is very difficult to replicate and execute. It’s a testament to Dollar’s management that they’ve been this forward looking to continue with this rollout for 4-5 years now.

Infighting

There are five innerwear companies that operate in the economy segment - Rupa, Dollar, Lux, Dixcy and JGH (Amul Macho). These five have conventionally used a traditional distribution framework.

Another rather lucky fact rumour in Dollar’s favour right now is that all of the remaining four companies have divides in the second and third generations in the family. Lux’s divide is probably the most public, but I have heard that this is present across Rupa, Dixcy and JGH as well. If the rumours are true, it’s another barrier that adds to a competitor having the wherewithal to implement a complete redesign of a distribution model.

Valuations and Outlook

Today, at ~1.7x sales, the valuations are undemanding if this structural change in Dollar plays out. Once Project Lakshya accounts for more than 50% of the distributors, I would expect Dollar’s growth rates to rise higher than the industry. It is also a fallacy to compare valuations to what Dollar has historically traded at, given the difference in the company before and after 2019/20.

As a rough sketch, I think it is possible for Dollar to get to 2800 Cr. revenues by FY28. Hopefully by then, RoCEs should improve to north of 30% if this is successful, and if the industry comes back into favour, I can imagine a multiple of 3-4 times sales if the market agrees with the differentiation. Therefore, I’d expect around 11-12k Cr. market cap by FY28.

All of these insights came from a scuttlebutt discussion with the former employee of Rupa, currently at JGH. Thanks to @nirvana_laha, @Lynch and @yrm91 for their efforts in working on the company with me.

Disclosure: Invested, transactions in the last 30 days.

@Chins - Excellent analysis. Well done.

If they do 1500cr this year, then 2800cr should come sooner than FY28, ideally. If it takes that long, then it’s a bit of slow growth ?

Would love to see you break down Skipper Ltd.

Ajay Upadhyay is a common investor in both Dollar & Skipper, and is know for picking odd gems.

Historically it’s been a slow growth company. Good money was made in riding the recovery of the cycle but not from the sales/profit growth.

But yes, Project Lakshya can help them improve market share driven by growth. With increased efficiencies they may be able to deliver better growth or it may make sense to grow at higher rate if the ROE/ROCE improves.

Disc: No reco to buy or sell

Praveen

Sounds good. But sounds too good for a company which has very low employee satisfaction.

Trying to be the devils advocate here.

Any FMCG/FMCD, Retail company worth its salt organizes its distribution in the manner explained . The distributors are assigned a fixed territory with retailers mapped and with the use of digital tools ensures that territories are adhered to and undercutting is not happening. Plus most of the companies reduce their credit to distributors as they move up the value chain.

I might be plausible that in the value for money inner ware segment Dollar is starting this initiative of structured distribution and might get some benefits out of it .

But the same can be replicated by all companies with a seasoned Sales and Distribution guys at the helm.

P.S: Not following Dollar industries , just my 2 cents on the distribution model .

Looking a various e-commerce portals and commentary from Page.

Online discounts are fierce and can’t sustain but right now there is actual pain irrespective of the model.

Cred. amazon if browsed for chaddis and cos do smell of cash burn in this inner sanctum inside all the things they sell.

Chart shows Dollar was at 1600 on 1/5/2017 and fell down to 390 … can someone explain this? Or is my chart incorrect.

Hi @Midhunjoe

You are right, any retail company worth its salt will have this kind of secondary sales visibility across its channel. The more important question is - Are the traditional “branded” hosiery players worth their salt when it comes to secondary sales visibility, retailer mapping, retailer incentivization, usage of loyalty programs etc? If you do some channel checks and speak to a few employees/distributors, the answer you will receive is a clear and emphatic no. One current employee from this cohort at a Regional Manager level told us that while Rupa/Lux/Dollar are classified as organised players, they barely qualify for that tag given how age old their distribution setups and mindsets are.

Having worked in a building materials company with a legacy distribution network and supply chain, I can tell you how difficult and risky it is to attempt to change the core of a traditional, legacy sales supply chain. The sales team often has a very old and traditional mindset and isn’t up to speed with modern retail and supply chain SOPs and nuances. You often have large distributors with huge territory whose families for several generations have been in the same business and they may even have direct links with promoter family who can leapfrog a sales leader and reach out directly to senior levels. This creates huge resistance to change. Its not at all easy to break through this.

It needs tremendous promoter will and focus and the right hiring and the right technology enablement to be brought in. It shows massive foresightedness on part of promoters IMO. So yes, while if you compare this with an FMCG supply chain, you will feel that this change is nothing out of the ordinary but the right comparison is with its peer set.

While they are building moat and may end up with distribution & MIS edge over competitors, what about the industry/market as a whole?

What is the market size, how much is that growing, and what about the influx of e-commerce & startup-brands which are tearing into tier 2 & 3 cities?

Is there any industry report?

It’s good to see management has been trying to create a moat in distribution. And if one looks at the guidance given for FY26 (2000cr revenue and 14-15% margin), the stock looks inexpensive. But I noticed that the management has had a track record of under-delivering on guidance and sometimes they’ve even under-delivered on quarterly guidance sitting 2 months into the quarter. Do you think this is due to management being too aggressive in giving guidance or is it just that under the traditional distribution set-up, management didn’t have any visibility at all regarding the demand, pricing etc. which would change with Project Lakshya?

@Pradyumna_Choudhary what are your calculations to conclude this is inexpensive at current valuations?

My sense is the company can do 185-190cr PAT in FY26, purely based on management’s guidance of 2000cr revenue and 14-15% EBITDA margin. Based on that, it is 14-15x FY26 P/E. Which for a well growing FMCG company with a solid brand and a structural improvement story (led by Project Lakshya) looks inexpensive. Even RoCE will improve due to improved WC cycle. But the question remains whether to trust the management on guidance because they haven’t had a great track record of delivering on guidance

Generally FMCG cos are valued highly becuase of the consistency in growth and lower cyclicality in margins. But when it comes to innerwear cos (exccpt for page) both the growth and earnings were cyclical and would probably stay same is future. So, calling this a FMCG co and justifying the FY26 P/E is a risky bet. Eventhough the management has given guidance of 2000 cr, It’s difficult for both management and investors to predict how the cycle would play out. So, we should take management guidance with a bucket of salt.

I’m not saying the guidance could be achieved. They may or may not achieve it and may even surpass margins guidance. But, we should not predict it and justify 15x 2y forward P/E to such business.

It’s a different ball game if one can invest and hold till the cycle turns around (it may happen in 6 months of 3-4years, only god would know).

It’s always better to look at alternatives while investing. As per me currently good businesses are available to buy instead of dollar. For ex. HDFC Bank, Kama holdings (Hold co of SRF Ltd), IIFL securities, Fino Payments bank, South Indian bank, Vishnu Chem, Mayur uniquoters could be better alternatives from my tracking universe.

It’s upto each one of us to look at our tracking universe and weigh current co (Dollar Ind) against them and decide for oneself.

DIsc: Just sharing my thoughts. No reco to buy or sell. Holidng some of the cos mentioned