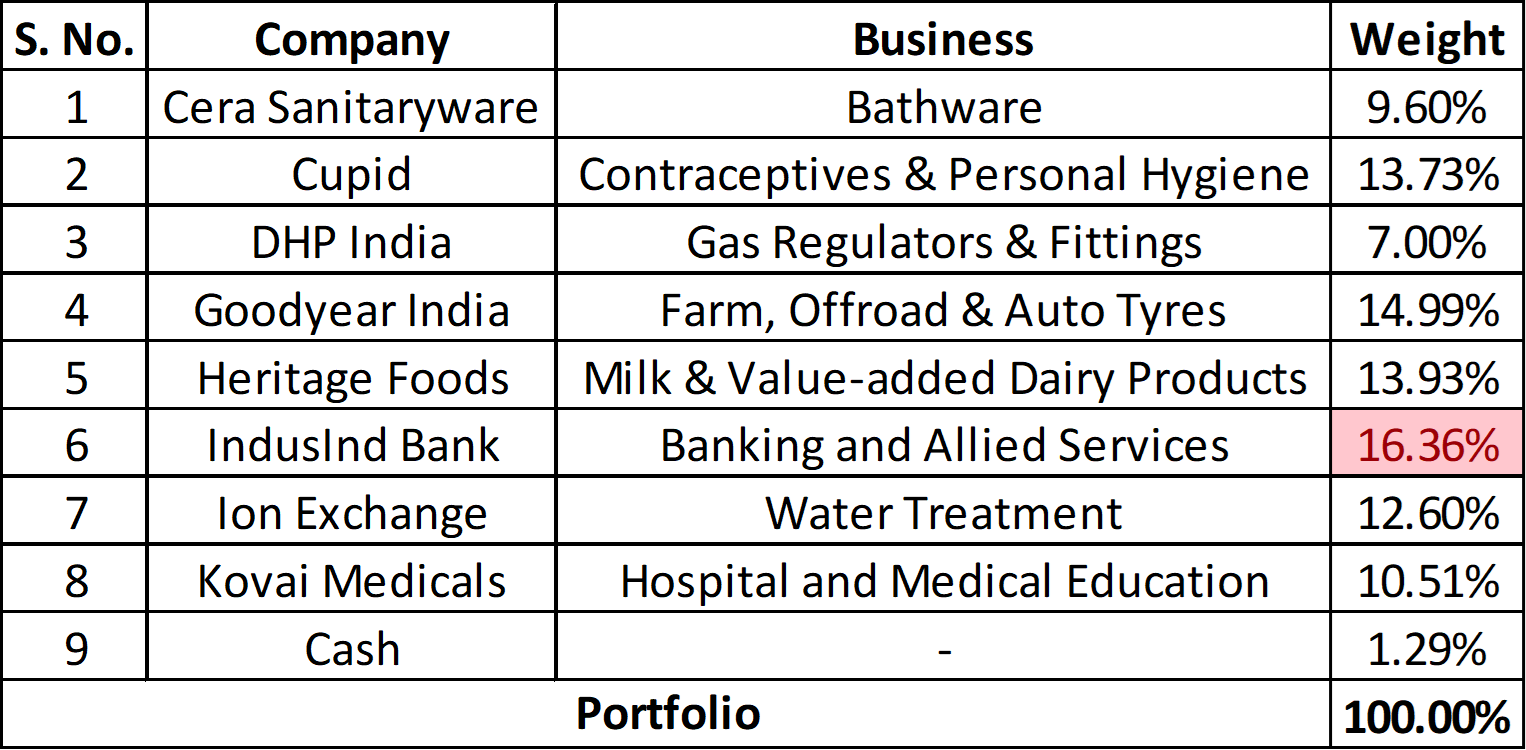

As I had mentioned earlier, IndusInd has an inherent strategy of having a riskier loan book than most banks of their caliber. So during a debt downcycle, they have to suffer. The decrease is profits is largely due to provisioning.

The double whammy from auto sector has also hit them, since a considerable portfolio of their lending book is auto loans.

Provided there are no new negative surprises, it should get fixed once demand picks up.

I think Mr. Hazari’s posts are sometimes useful. But mostly he is always negative. He even tweets about trivial things like “CEO of this bank was awarded this title and he should not have got it.” and so on. I consider his posts for taking out facts, but completely ignore opinion (The same way I do with research reports).

This is completely wrong and misleading. Berkshire Hathway has Deferred Tax Liabilities which is similar to negative working capital while HDFC Bank has Deferred Tax Asset which is the complete opposite of DTL and leads to a decrease in cash flow. When accounting pre-tax profits are less than the taxable pre-tax profit you pay more tax than you should leading to Deferred Tax asset (HDFC) on the other hand if accounting profit is more than taxable pre-tax profit you pay less tax than you should increasing your cash flow leading to DTL (Berkshire). Criticizing an expert is fine but don’t use wrong examples to do that.

I follow Mr. Hazari on Twitter too and consume his research to a good extent. But my point still stands that he writes about a lot of trivial stuff too (In my opinion), while also having a high negative bias.

Appreciate the detailed explanation of the difference. Do you see this as a red or Amber flag on the corporate governance and management quality of HDFC? Thanks

I am not an accounting expert however I don’t see it as a corporate governance issue. Hazari’s point seems to be when DTA reverses accounting profits will suffer. However DTA as percentage of net profit is higher for banks with higher NPA s like ICICI so if HDFCB is going to be impacted with this reversal other banks might be impacted even more. Also with the recent cut in tax rates companies have to write off DTA anyway so I don’t see it as a big issue

@dineshssairam

I saw that you have 1.29% cash holding. So, is that kept for opportune buying or just for your day-to-day & emergency expenses? In either case, do you have enough funds to cover any emergency or do you have to reach for your equity holdings in times of need. Btw, I am not talking about super emergency incidents which require huge money & is often tough to judge.

My cash holding is low because I have been continually Investing in my PF whatever cash I get. But once I see the under valuations going away, I will most probably start investing more in AAA Bonds or funds that largely hold GOI Securities. As I keep saying, I always aim for at least 10% / comfortably 20% of my PF in cash.

It’s just that I cannot let a good correction go to waste.

Pretty much any liquid fund with 70%+ in Money Market Instruments and Sovereign Bonds will do. Some examples are:

HDFC Liquid Fund

Parag Parikh Liquid Fund

Some Liquid Funds like Axis, IDBI, Union etc are a little riskier since they hold several Bonds too. But they all pretty much return the same 6-7% YoY.

Of course, go for Direct Investment (That is, invest from the Fund’s website yourself) to avoid brokerage.

No, I’m talking about the transaction charges when you transact via a brokerage. You can avoid it if you invest via the fund’s website directly.

Also yes, all Mutual Funds have an Expense Ratio. In fact, Expense Ratio is more important for Debt / Liquid funds. In Equities, a higher Expense Ratio usually indicates higher salaries paid to the Fund Manager and his team. So, although the Expense Ratio is higher, increased performance is also expected (Ironically, this is not always the case).

But when it comes to Debt and especially Liquid funds, the major aim is preservation of capital, which does not take too much effort to do. So, a higher Expense Ratio simply eats into your return and is not likely an indicator of improved performance.

To park your liquid funds, what do you think about Franklin ultra short super institutional bond fund? It gives 9%+ (instead of 7.5% which other liquid funds give you).

Well yes, that’s because they hold 72% in Corporate Debt.

But my major aim is capital preservation, which means I don’t want to take any risk or at least, take as low a risk as possible.

Think about it this way… how long are you going to park your funds? Maybe if the market remains stretched, a period of 3 years together? That is possible. Now what is 1.5% extra returns over 3 years? Peanuts, to be honest. I would gladly trade the extra 4.56% for the promise that my money is pretty much safe.

But of course, if you are looking for substantial returns from your parked money as well, that is a different story. Some people trade with their parked money. But I don’t know much about trading, nor do I practice it. So I’d refrain from commenting on it.