I looked at Wabag too when I was considering investing in this space. But a bulk of their orders comes from the government and as a direct result, their Working Capital position is terrible.

This situation is a good case study on why Working Capital management and therefore, Cashflows are important to a company.

Don’t you think Indiuind is more risky die to their higher corporate exposure? I don’t see any indian bank making serious money lending to corporates [ at least in the near future] .

Well, yes. IndusInd’s strategy itself (Has been for quite some time) is to purposely have a riskier loan book than most banks. Clearly during a scary period in the loan cycle like this, they have to bear the brunt of their strategy. That is also why the bank came down from mighty levels of valuations to more reasonable levels.

In the past (Before Mr. Sobti), the bank has been ever more disoriented. To understand the entire backstory how IndusInd used to be and how it evolved, read the following document I came across while doing my research on the bank:

(For instance, did you know that IndusInd’s vehicle lending arm used to be Ashok Leyland Vehicle Finance? I certainly didn’t, before reading this document)

My personal thesis for IndusInd is:

It is a bank that knowingly takes risky loans on its books. They have built a strategy around it. This will cause setbacks during a Debt down-cycle (Like we have today).

The bank has been able to create all this wealth without having an NBFC, research, advisory, AMC or insurance arm i.e. only on core banking.

All of these ancillary business are in the plans. BhaFin is already merged. In a couple of years, there are plans to roll out the Research and Insurance businesses. An AMC may follow in the distant future.

The only real risk here is the replacement of Mr. Sobti, who has added tremendous value to the company. But if one were to believe his words, the successor has been groomed personally by him and should be able to handle the business equally well, if not better.

Almost a decade back when I just started with markets, one of my first long big idea was water and waste management. Maybe way too early of time and still early…and the only company I could find then was wabag. I think the stuck gov orders, as rightly pointed out by you, destroyed the prospects of the company. What is the order mix and target audience for ion exchange in comparison? Also do you see any potential listed company in waste management business? Thanks

I recently presented on the topic “The Intrinsic Value Puzzle: Components and Case Studies” on a SEBI-sponsored investor awareness meeting of the Tamilnadu Investors Association (TIA).

Not really sure where to put it, so I’m posting it here for now. Mods, if you think this is not the right thread, kindly point me to the correct one.

Ion Exchange mostly does B2B. For instance, their current bids are for Refineries, Steel, Food & Beverages, Oil & Gas companies. Their B2G is a tiny portion (I think they do 1-2% business with IRCTC).

I think ‘Eco Recycling Limited’ is the only listed waste management company in India. But I have not done any research on this.

Great notes and information. Very helpful

Been invested for last 18 months . Bought a good chunk between November 2018 and may 2018 and been doing SIP ever since till today.

Disc: invested , 2nd highest holding in portfolio

Hi @dineshssairam It seems report has been moved from drop box. I got message that report is missing. Can you please double check and share the link again?

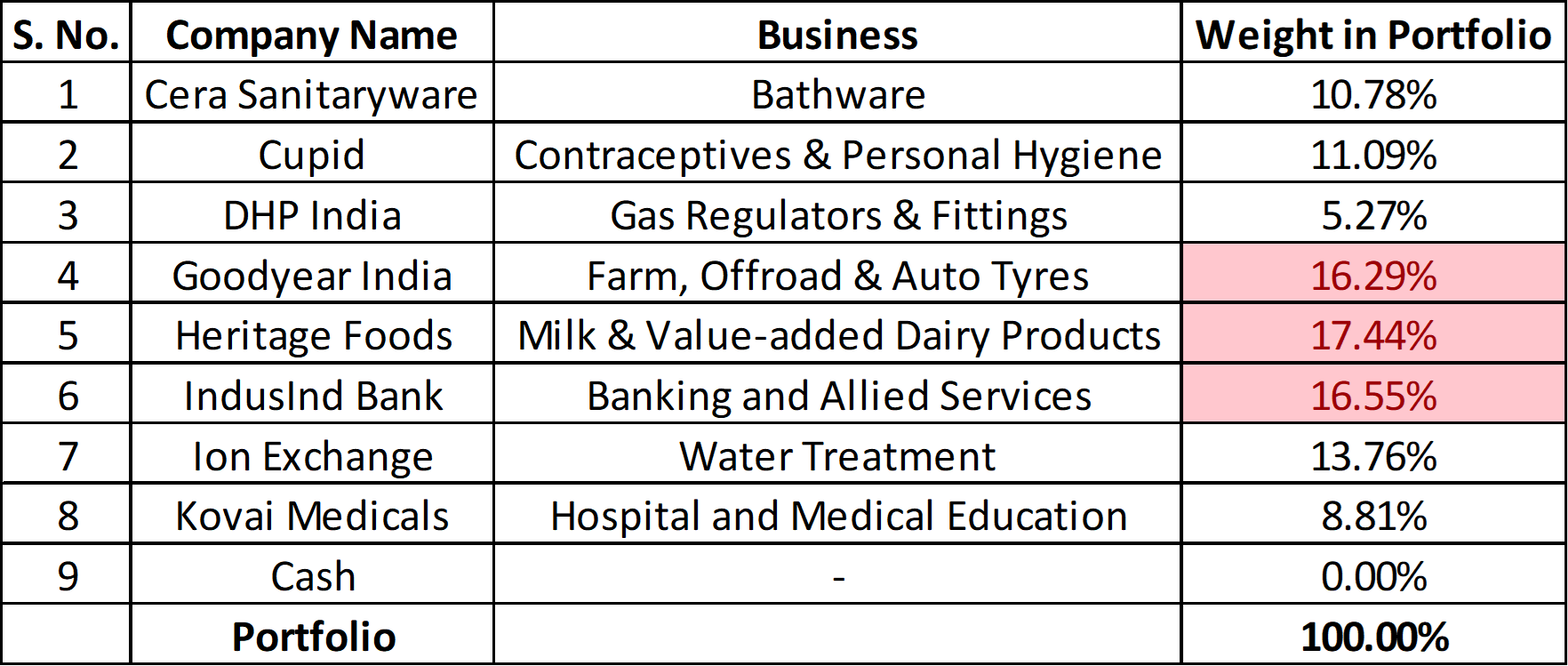

Deployed the remaining cash mostly in IndusInd Bank, DHP India and KMCH (I did buy a little bit of Heritage Foods some time ago as well). I have also added a tracking quantity in Shivalik Bimetal Controls, but the exposure is too small to warrant a special mention.

Top 3 holdings now form slightly more than a 50% allocation.

Are you only tracking Shivalik or are there any other Auto ancillary stocks that you are tracking too? What are the main points you shortlisted Shivalik over others? I am looking at JBM Auto, Minda, Shivalik and RACL. Not even tracking quantity yet. I will decide after next OR dec. quarterly results of complete auto sector whether to invest or not.

My current watchlist / tracking list is as follows: Eicher Motors, GCPL, Grauer and Weil, Marico, Mayur Uniquoters, NESCO, SIS, Shivalik Bimetal Controls and Timken India. I also track Motherson Sumi on and off, but mostly interested in seeing how their next couple of acquisitions go.

I can see you are very bullish on IndusInd Bank and that is the only bank or financials stock you have. What makes you think this bank is best of the lot in terms of valuation and future growth prospects.

A quick look at screener, I could see compounded profit growth is coming down over the years.

What would worry me is the claim that it provided around 2000 cr unsecured loan to ILFS in early FY19. Like the credit rating agencies, they were also incompetent in analysing the publically available financial statements of ILFS.