Just wanted to ask why you dropped CCL products from your watchlist?

Have been tracking it for some time; it offers a quality management and a clear moat due to its assortments, variety and stickiness. Saw one of your previous answers on Quora where you mentioned that a price of ~ 260 was little more than your comfort zone. Would think that it looks good for the long run at current levels. Has anything changed?

2 Likes

That’s very coincidental, I should say. I literally added CCL Products back to my watchlist just today. I would like to have it at 180. But 200 isn’t bad either I guess.

The problem is, I don’t have a lot of Cash now. I will be able to raise more Cash around March. If it’s still around these levels or below, I think investing in it would be decent.

My current watchlist is as follows: CCL Products, CRISIL, Eicher Motors, IEX, Marico, Morganite India, NESCO, Tinplate, United Breweries.

6 Likes

Do you have any idea about beekay steel industries, part of their revenue comes from fixed margin conversion business… OPM going up consistently in last 5 yrs.

Pl share your views

If possible can you write more on your rationale behind having this on your watchlist? I believe you have a better viewpoint than many of us since you work with them.

Hi

CCL i had in my investment but sold it long time back as found that performance did not live up to the expectations after holding for long time . There was explanation for every shortfall . Do you plan to hold for long term and is there any change in its growth drivers? Many thanks

It’s exactly because of this that I cannot write more about it. If anyone has specific queries, they can DM me. I will help as much as I can.

I don’t think there are any unknown growth drivers. The Instant Coffee venture in India could be a good optionality. But generally, the B2B is a nice, sticky business. USA and Europe are the biggest markets, but the rest of the countries are far behind. There’s a good amount of ground to be covered by private coffee players (Of course, there’s a lot of them too).

But my concerns are with the new management (Mr. Challa Srishant) and their obsessive interest with the Indian B2C market (They’re spending about Rs. 10+ crores in Advertisement alone to earn a Revenue of Rs. 50 Crores for the branded business).

But at Rs. 180 or below, I think it would make a good bet.

3 Likes

I haven’t discussed about my history as an investor here. So maybe this is a consolation:

https://ayakconsultancy.com/from-the-horses-mouth-dinesh-sairam-investor-profile/

9 Likes

wonderful sir, will you please tell us which MFs are you invested ? thanks in advance

Mirae Asset Tax Saver (50% of SIP)

Axis Long Term Equity Fund (30% of SIP)

IDBI Equity Advantage (20% of SIP)

All Direct - Growth plans (i.e. I started the SIPs via their websites, with Dividend Reinvestment). Of course, they also help a bit with covering 80C too - that’s a small additional return.

But as mentioned several times in this thread, my Mutual Fund investments are just a buffer since I am new to investing. In a couple of years, I may decide to shift a majority of it to direct investments. So be careful with putting any stock on this.

3 Likes

What is your current stance on Indusind bank? Seems as if there was a lot of divergence and in this quarter they adjusted nearly 720 crores directly against their net worth. Doesn’t seem prudent at all. Moreover, after yes bank, Indusind banks real estate loan book has grown the fastest in the last couple of years. Old troubles will definitely come to bite back. Bharat financial acquisition seems like deworsification, no expertise in Microfinance. A place riddled with risks and bank diversifying into it. All this has already spooked the markets and maybe it doesn’t deserve the p/b of 4-4.5 times it was being ascribed earlier.

1 Like

-

Divergence is a worry (Including rise in SMA1 and SMA2 Assets). I will wait for Mr. Sumant Kathpalia’s comments on the same later this year. Broadly, the stance looks like he will kitchen sink most bad loans. We’ll see. Already, the next 3 Quarters are going to see continued Provisioning, as per guidance. This will help with the PCR, which has been going down the entire last year.

-

The bank’s latest set of goals seem to include moving away from CV loans (https://www.bloombergquint.com/business/here-are-the-key-highlights-from-indusind-banks-analyst-meet). Specific to Real Estate, there’s no saying when it will recover - but the RBI’s and FinMin’s support seems positive.

-

I don’t think the Bharat Financial acquisition was in a bad stance. In fact, I would say it’s one of the bright spots for the bank amid a generally gloomy scenario for lending in the country. Again, the goal here seems to be making the entire MFI book self-financed in 5-7 years, which needs to be tracked. But as of today, no, I don’t think it was a diworsification.

Clearly, as I’ve been saying all this time about IndusInd Bank, I understand that there are overhangs. But good times and good prices seldom occur together. At the cost of sounding cheesy, I’d say I am “cautiously optimistic” on IndusInd Bank.

On a related note, Bandhan Bank seems an interesting one these days due to the Assam issue. I’ve added it to my watchlist, but I’ve not done any deeper analysis as of now.

5 Likes

1.If a bank needs to kitchen sink its loan then it is not in the healthiest of places to begin with.

2.Nearly 100% Cagr of loan growth to property developers from fy16-fy19.

3.Writing off Losses directly against the balance sheet rather than P&L. If this isn’t a red flag then i don’t know what else is.

4.Nearly 8% of Bank capital given out as unsecured loan to IL&FS. Moreover, disclosure wasn’t made in a timely manner.

5.Acquisition of Bharat Financial is like a double edged sword. In good times it will lead to a bump up in ROE, but if the bad times strike which they do in our country. ROE’s will go down and credit cost will spike. Let’s see how this goes.

How many red flags does one need especially in a levered business. Why take such cyclic bets in levered institutions? No one can actually get to the bottom of the problems bank will go through in the future. Just taking a view only in terms of valuations is extremely myopic in my view, just simply ignores the generallist view of the world. A guy who lends co’s like IL&Fs(that too via SPV) and Essel group. How many skeletons are there in the closet who knows? Coupled with charging losses through balance sheet rather than P&L.

At the cost of sounding realist, I am extremely pessimistic on what comes out in the future. Banking is one business where true extent of the problem isn’t known untill everyting is out. Given it constitutes nearly 16% of your folio, you might just need to consider the disconfirming evidence and only if you find merit, then change your mind.

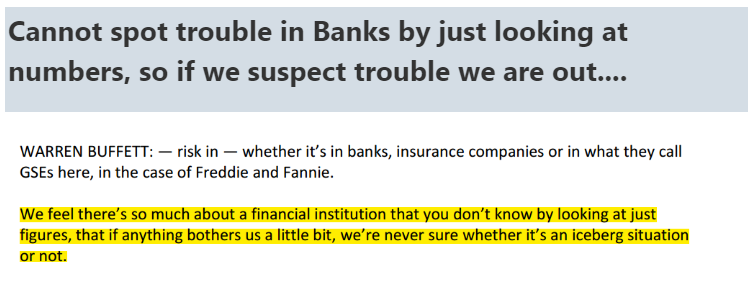

Warren Buffett puts it beautifully

Disclosure: Not invested

11 Likes

The problem is, these risky loans (Say to ILFS, Essel, DHFL) and other similar ones were already there on the Books for some time. But it’s only now, at the bottom (Possibly) of a bad loan cycle that it is being diced and analyzed.

I don’t deny that the bank has bad loans. In fact, having a riskier loan book than most other banks is in their strategy. So, I would much rather than the bad loans be covered with Provisions rather than thumb-sucking. A Risky strategy doesn’t always come bearing gifts. Costs have to be paid too.

Quoting Warren Buffett is great, but if you’re actually being real, let’s not forget the recent Wells Fargo saga. Lending is a simple, not easy business.

Thank you for your point of view. Ultimately, it’s all relative to the Value for me. But if you’d rather not take this kind of risk with levered institutions, then I can respect that.

2 Likes

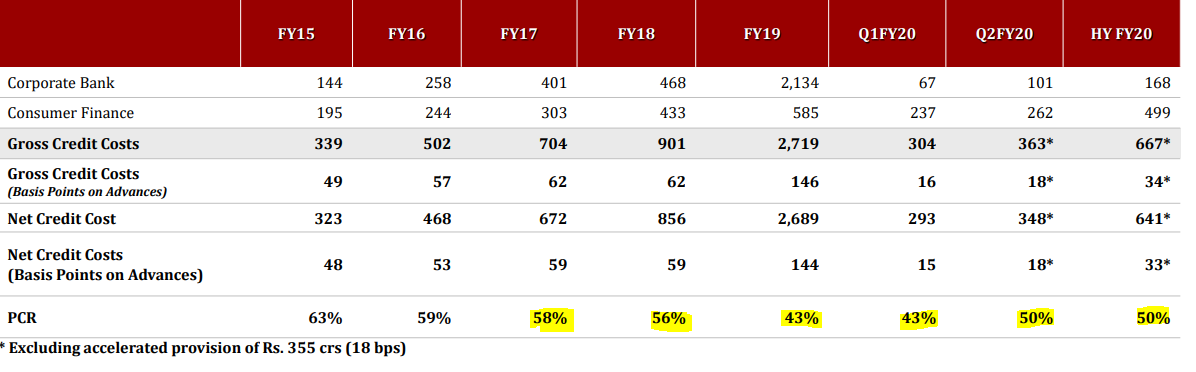

Let’s look at the provisions when the problems started in 2018

PCR is too low when compared with the stalwarts or with other players like Axis during that time . Why suffer the consequences later and mask the earnings with good today pain tomorrow kind of strategies? These little things just give an insight into the culture of the bank and quality of reporting. Only now when problems have become overblown has the provision risen.

I respect your opinion too. Just presenting a variant perception @dineshssairam ![]()

7 Likes

thank you so much sir for diclosing MFs investement, One question arise in my mind we should invest in that MFs in which AMC FUND HOUSE OR FUND MANAGER INVESTED ,What is your opinion sir .Thanks in advance.

1 Like

If that’s a filter you’d rather apply, sure. Why not? But I generally restrict it to looking at the Fund Manager’s work history and performance history.

I don’t mind if they don’t have skin in the game. The Mutual Fund industry, unlike most Corporates is very professionally managed. SEBI is also a good regulator, at least as far as Mutual Funds go.

1 Like

Thanks for bringing up these points @Worldlywiseinvestors - I was evaluating IndusInd and they certainly are helpful.

Moreover, the below seems another red flag as we connect the dots looking backwards:

"Chartered accountancy firm S R Batliboi & Co has resigned as statutory auditor of the private sector lender IndusInd Bank. IndusInd Bank has appointed Haribhakti & Co as statutory auditor for the financial year 2019-20, subject to approval from the Reserve Bank of India and shareholders.Jul 14, 2019 "

1 Like

The “resignation” happened because RBI banned SR Batliboi & Co from Auditing a Bank’s Book for 1 Year. The Private Banks named in this fiasco by the RBI are actually Axis Bank and Yes Bank.

8 Likes

1 Like

One should be highly skeptical when bad news starts coming out in Levered institutions. It doesn’t take much time for virtuous cycle of high valuation and fund raising to turn into a vicious cycle of Low valuation and pessimism all around. Indications were always there, major red flag was in this quarters result, of losses being written off against the Equity. I personally have learnt through experience of other investors to not be courageous in this sector and take cyclical bet. How far the valuation lowers and how many things that will come out, one never knows. Lets see how they manage the downside.

10 Likes