Hi ValuePickrs,

Dinesh Sairam here. I have been investing in the Indian markets for a very short time now, just about ~1.5 years. I follow my own investment code-of-conduct. I look forward to your feedbacks regarding my portfolio of stocks.

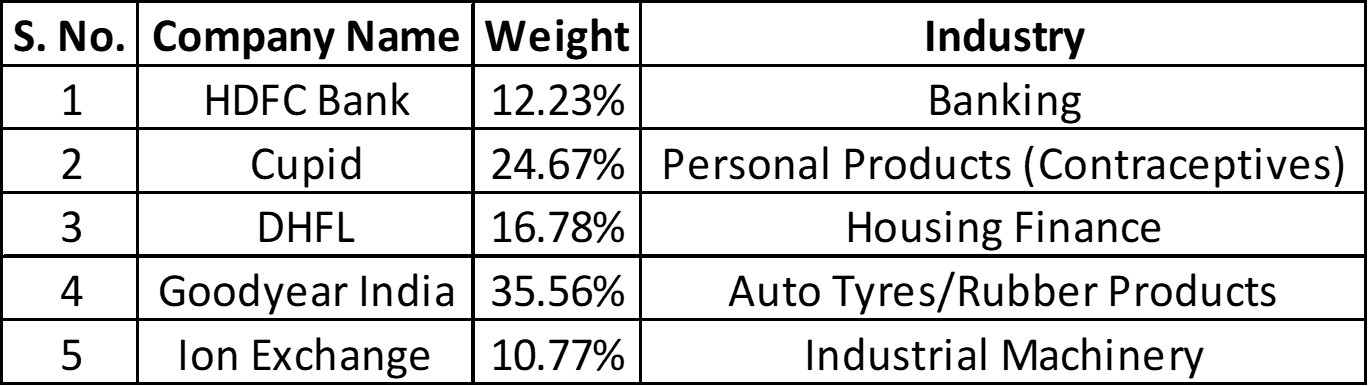

HDFC Bank: The One Man Story

My investment rationale in HDFC Bank is largely dedicated solely to Aditya Puri’s stellar management of the company and the way he has shaped the company’s culture. I have heard several stories from several people about how the company’s culture is hellbent on returning shareholder value. I also identified HDFC Bank’s leading position in the Private Sector Banking industry in India. All my family members have a SD account with HDFC and their customer service has been satisfactory so far.

Cupid: The Turnaround Story

I had been following Cupid’s business for some time before I invested in it. The company has a monopoly in Female Condoms in India, but I have my doubts on whether that is a real moat or not. However, what attracted me to the company was that it has managed to turnaround its sales and operations in a quick span of time. Cupid has been churning out cash for the past few years (Well, relative to their size, anyway) and even paid off a majority of their debt, which was bogging down their returns. I tried looking into the reason behind this, but the best I could come up with was their CapEx cycle turning. Recently, they grabbed an order from WHO to supply condoms to Africa, which could possibly be an expansion opportunity for them. Regardless, I believe that the company has a great future.

DHFL: The ‘Affordable Housing’ Story

No points for guessing why I bought DHFL. The government’s push for affordable housing has created a temporary economic advantage for all housing-related companies. Out of the lot, I believe DHFL to be the most equipped to take advantage of the opportunity to scale up. They were able to successfully scale up and still maintain their returns on equity largely. However, I have my doubts on how much they can really continue scaling up and of course, there’s always the ever-present threat that DHFL doesn’t actually have a moat all by itself.

Goodyear India: The Value Story

Once again, my conviction in Goodyear India began with the fact that there is still a lot of demand to be fulfilled in the mechanization of agriculture in India. Goodyear India commands market leadership in both the rear and front tractor tyres market. Their list of suppliers is impressive, including all the major players in India and even some foreign players. My determination was steeled when I valued Goodyear and found out that it was way undervalued than what I expected it to be. This explains the portfolio concentration on this company.

Ion Exchange: The Future Story

I’ll be honest, I started tracking Ion Exchange only because Rakesh Jhunjhunwala is invested in it. Although their B2C business faces extraordinary competition from all directions, I believe that they are one of the few players in the water treatment industrial machinery business. India’s demand for clean drinking water is projected to seriously explode in the coming years and companies like Ion Exchange and VA Tech Wabag are perfectly positioned to pick up the slack. I would really like it if Ion Exchange concentrated more on their B2B business more than their B2C, but I’ll take what comes.

P.S. I understand that my portfolio is concentrated. I definitely believe in diversifying up to 10-12 stocks. Earlier I had such a portfolio which I diluted completely to create this portfolio (Because I wasn’t strictly following any code of investment back then - so, a fresh beginning). Since the markets have been riding up all the stocks in general, it’s become very difficult for me to solicit good businesses which are also intrinsically undervalued. I am more than willing to buy into 2-3 more companies if and when they fall within my comfort for valuation.

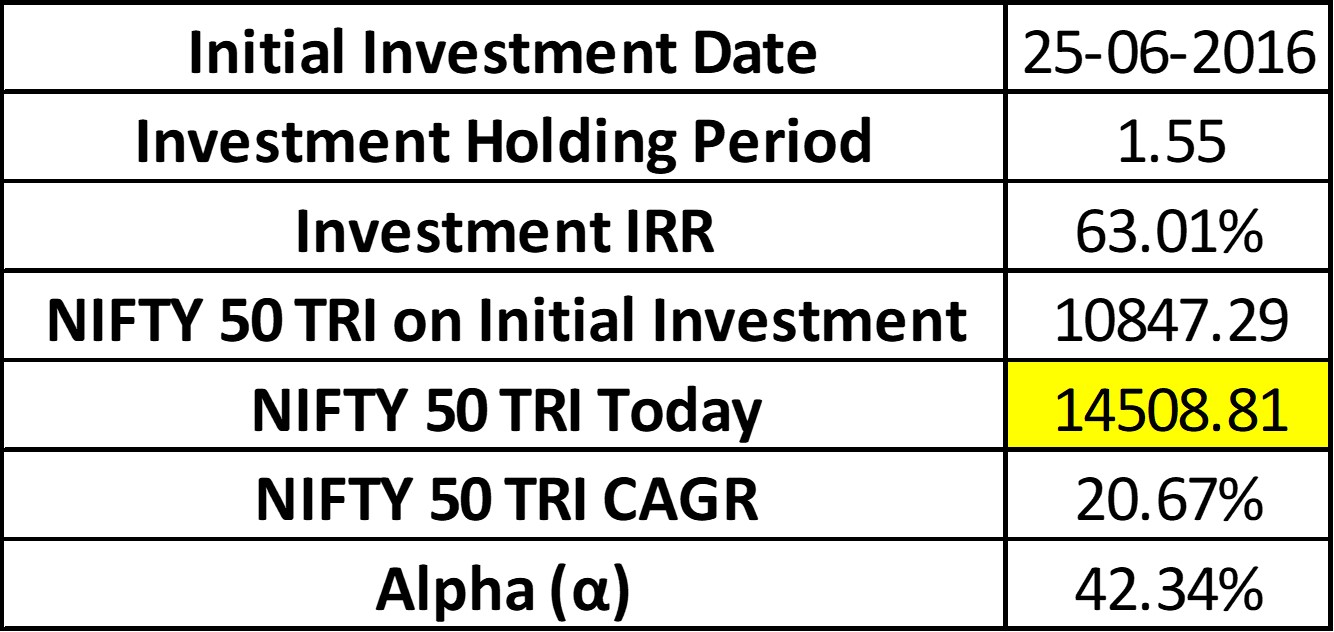

The following have been the returns on my very short investment journey so far (This is inclusive of the returns from my previous portfolio as well, FYI):

I would specifically like feedback on either my investment code, the stories attached to my portfolio or the lessons I learned on my prior holdings. Thank you.

Summary of Feedback:

- @arunsg: Include more objective factors to identify the ethics of companies in the investment code.

- @hitesh2710: In a concentrated portfolio, invest in industry leaders with growth potential. Too much weight in a single stock should be checked.

- @bharat.jain: Compare investment opportunities with their competitors for financial metrics.

- @jamit05: Stick to high-growth companies for capital protection.

- @Savishesh: As far as possible, stick to facts and numbers. Avoid trusting ‘gut feelings’ or ‘convictions’.

- @red2red: Growth potential is important in identifying investment opportunities.

- @SlownSteady: Diversify.

- @paraacbe: Concentrated portfolios perform well in bull markets, but not so much in bear markets. Prepare for it.