In a recent development, Niti Aayog member Ramesh Chand has expressed optimism about the growth potential of India’s agro-chemical industry, even in the face of stiff competition from China. This positive outlook for the sector has significant implications for companies operating in the agrochemical space, such as Dharmaj Crop Guard Limited, a leading player in the Indian market.

Dharmaj Crop Guard Limited (NSE:DHARMAJ), based in Ahmedabad, India, is actively involved in the manufacturing, distribution, and marketing of a wide range of agrochemical formulations. Their product portfolio includes insecticides, fungicides, herbicides, plant growth regulators, micro-fertilizers, and antibiotics, catering to both B2C and B2B customers.

Dharmaj Crop Guard Ltd (DCGL) is correctly positioned to capture growth in both domestic and international demand for agrochemicals.

Domestic demand

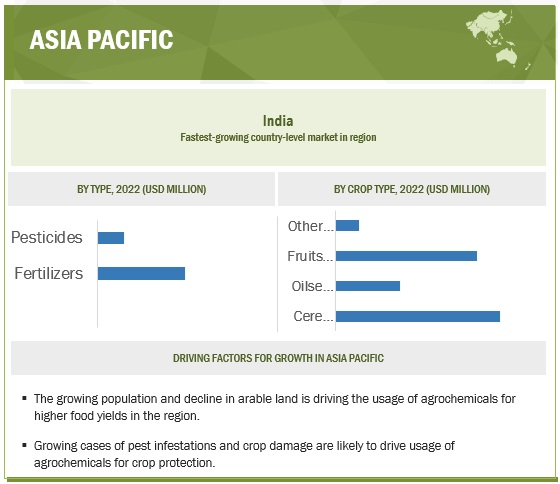

India is one of the largest consumers of agrochemicals in the world, and the demand is expected to grow at a CAGR of 7-8% in the coming years. This growth is being driven by factors such as increasing agricultural productivity, rising incomes, and growing awareness of the benefits of agrochemicals.

DCGL has a strong presence in the domestic market, with a wide range of products and a well-established distribution network. The company is also expanding its manufacturing capacity to meet the growing demand.

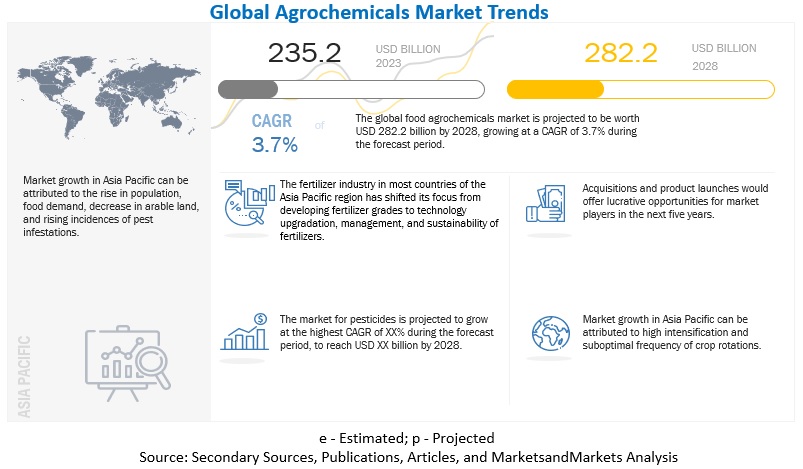

The global agrochemicals market is also expected to grow in the coming years.

DCGL is already exporting its products to over 20 countries, and the company is planning to expand its global reach further. The company has a strong focus on research and development, which is helping it develop new and innovative products that meet the needs of international customers.

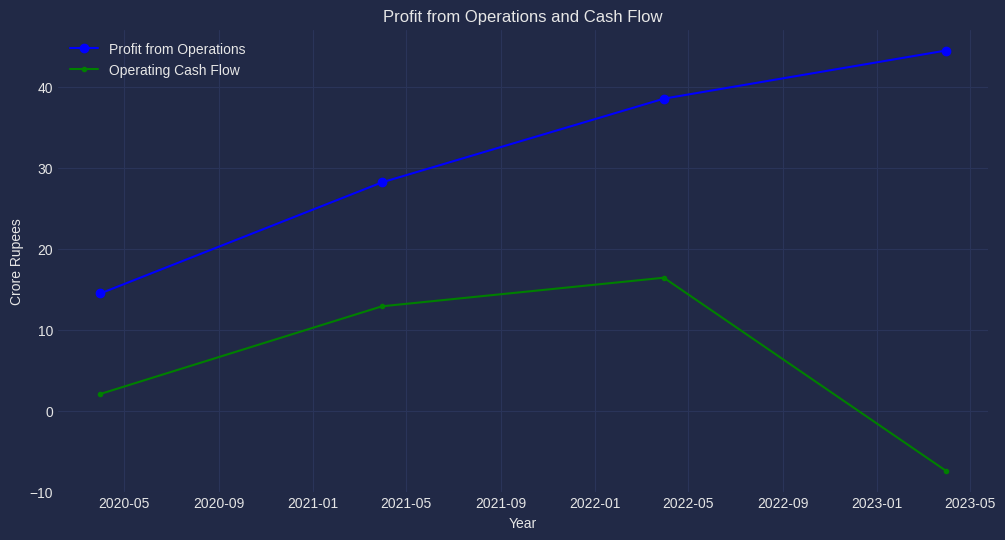

The financials are strong with sustained revenue and profit growth. However, the cash flow in recent reports has been on the lower side.

Risks

The agrochemicals industry faces challenges from technological advancements, price fluctuations, and intense competition. Changing laws and regulations can impact product compliance. Remaining competitive depends on anticipating technology changes, industry trends, and customer preferences, and addressing unidentified needs promptly. Success relies on factors like meeting schedules, supplier performance, hiring qualified personnel, and cost efficiency. Obtaining necessary technological knowledge is crucial, and failure to do so may strain resources and negatively affect business operations. Effective strategy implementation hinges on timely knowledge acquisition, which could impact business results.

Weather conditions, including rains, droughts, floods, cyclones, and pest infestations, significantly impact the agrochemical company’s business. The presence of greenhouse gases in the atmosphere raises concerns about global temperature changes and extreme weather events. Sales depend on crop volumes, and adverse early-season conditions, like droughts, can lead to lower demand for crop protection products. Weather also influences planting timing, pest infestations, and commodity prices, affecting sales. Increasing climate change concerns may lead to stricter regulations, potentially increasing operational costs. In India, agrochemical sales are seasonal, peaking during the monsoon season, making quarterly results variable and unreliable indicators of future performance.

The use of alternative pest management methods like organic farming, biotechnology products, and genetically modified crops could reduce the demand for chemical pesticides, potentially impacting the company’s financial performance. Zero budget natural farming, a chemical-free approach mentioned in the 2019 Indian Union Budget, may also affect the sale of agrochemical formulations and the company’s revenue. Genetically modified crops with improved characteristics may reduce the demand for certain products. Conversely, resistance in weeds and insects to crop protection products may result in decreased demand, which could harm the company if they don’t adapt their product range.

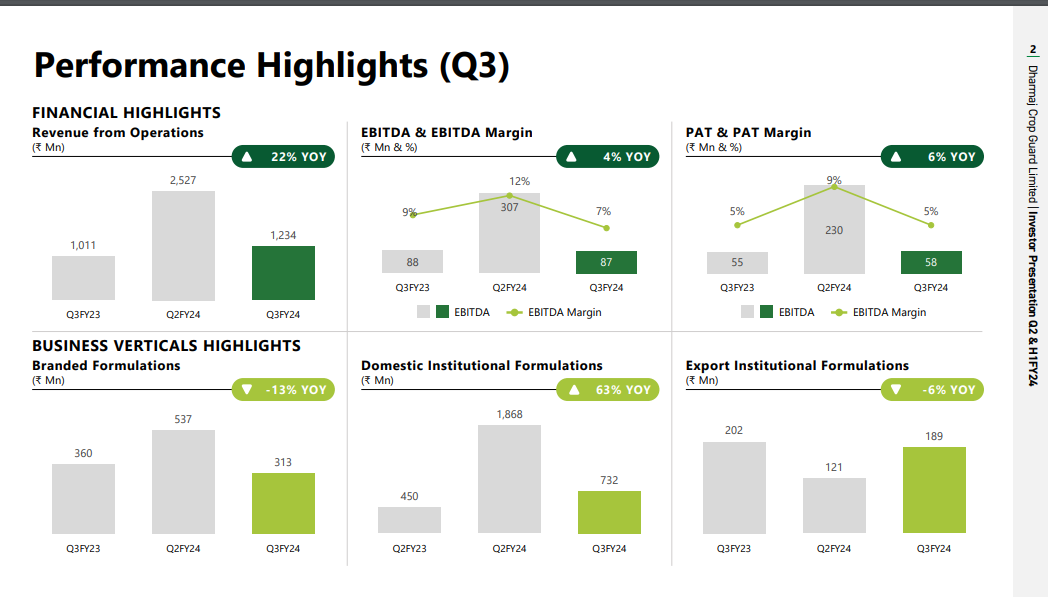

Dharmaj came with good set of results with sales growing by 14% and profits by 44%. These results are especially good given the weak agchem scenario currently. Their technical plant will be online this quarter, which might lead to subdued numbers for the next few quarters (depreciation costs + plant operating costs). Concall notes below.

FY24Q2

Sayakha plant will be commissioned in November, it witnessed some cost overruns (cost escalations + additional equipment in MPP to improve product mix). Increased cost from 200 to 220 cr. Expect 10% utilization in FY24 and full utilization by FY27

Will do external sales of ~600 cr. from plant + 100-150 cr. of internal consumption

Inventory management: Purchase technical at the end to reduce price volatility risk

90-120 days receivable cycle. Increased receivables this quarter was because of higher sales in August which will be realized in October

Have seeded smaller volumes to Rallis this year, expect higher growth in next year

Fire incidence was minor and brought under control in half hour, not much losses

CTPR: have got 9(4) registration to manufacture technical

Technical pricing: have to compromise on prices in older molecules, but in newer molecules (such as CTPR), don’t expect lower pricing

Gujarat, MP, Maharashtra are established markets for Dharmaj

Farmer reach: 3L currently

For any new product, 1st year is for field level demonstrations for demand generation, and 2nd year is for selling volumes

Fixed costs for technical plant: 40-50 cr. in FY25 + Depreciation will be 24 cr.

Hoping to do 60-65 cr. PBT in FY25

Disclosure: Invested (position size here, no transactions in last-30 days)

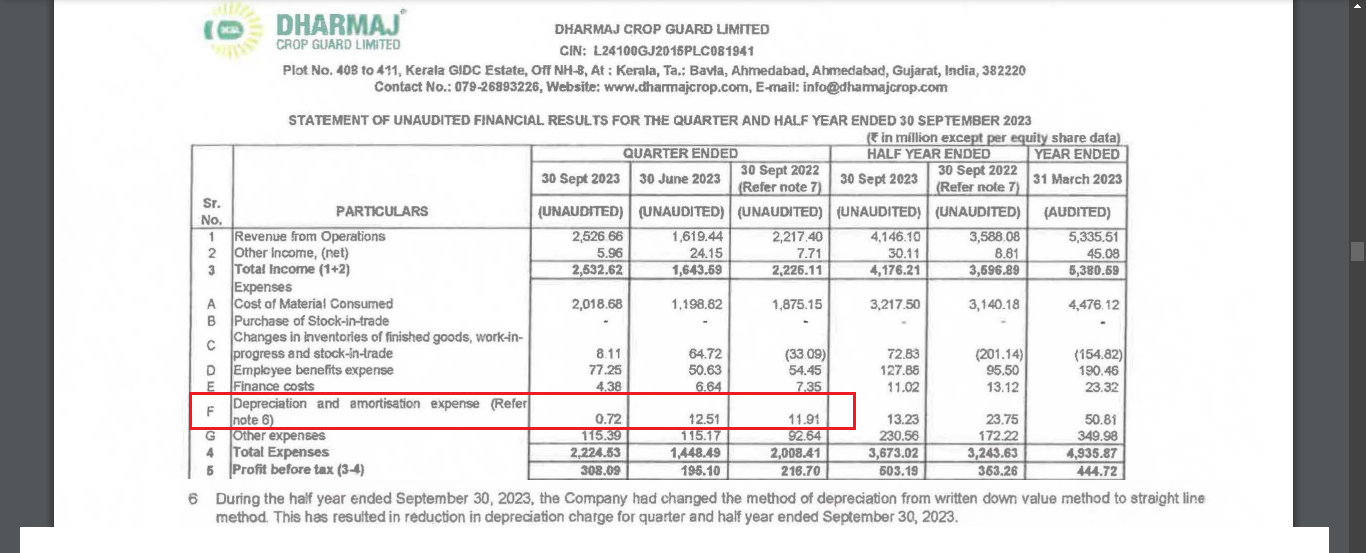

One observation which merit attention on 2Q FY2024 results. Depreciation policy has been changed during quarter which has resulted in lower deprecation for quarter by 94% y-o-y. Given that a large capital work in progress (INR211cr) is going to get capitalised most likely by end of year, not sure what is the real intention behind change in deprecation policy.

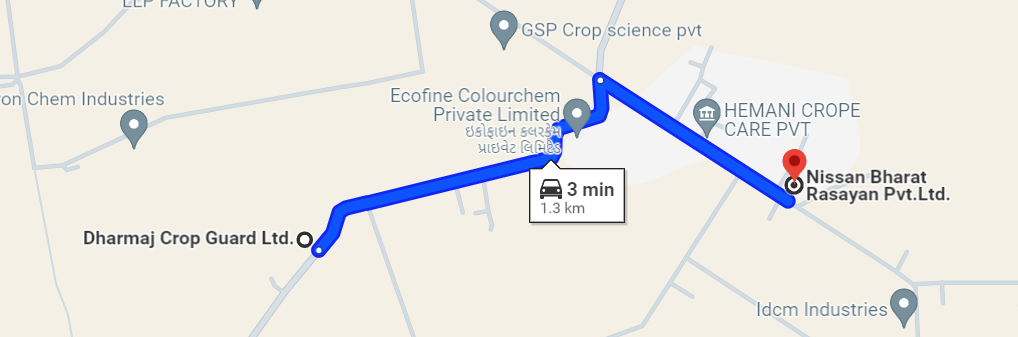

Dharmaj’s new plant is almost adjacent to Nissan Bharat Rasayan plant in Saykha. Given the huge ramp up expected from Nissan JV plant by Bharat Rasayan, this looks like a strategic sourcing decision (Dharmaj being one of the suppliers).

Main thing to track would be how management is going to capitalise this CAPEX, as technicals seems to be new market for management and it’s major market is exports and mostly B2B, whole new different customers

Though management had a good experience in sales but for cracking the exports market more and more registrations (process is keep on getting difficult, though acting as a barrier too) are the key as per my understanding

Promoter is very frank and explains the strategy that they are using. They expect to do revenue oof 900-1000 Cr in FY25 and in FY26 expects to have a EBIDTA margin of 13-16 %.

They feel products have stabilized and showing some increase in prices. However timely monsoon remains a key risk.

As per the management being a small company they are nimble and connect with the farmers. They also track the cropping cycle and have products for every stage of the cycle. Q1FY25 will start to see depreciation for the API capex.

The EBITDA & Revenue targets are very ambitious. This is more than 50% YoY growth in revenue for FY25.

Let’s say the company grows 15% YoY for FY26 (It is very conservative considering the capex the company is doing but let’s be on the safe side). So the revenue in FY26 would be around 1150 crores. At 13% OPM, the EBITDA would be 150 crores atleast from the current TTM of 60 crores. Again very ambitious.

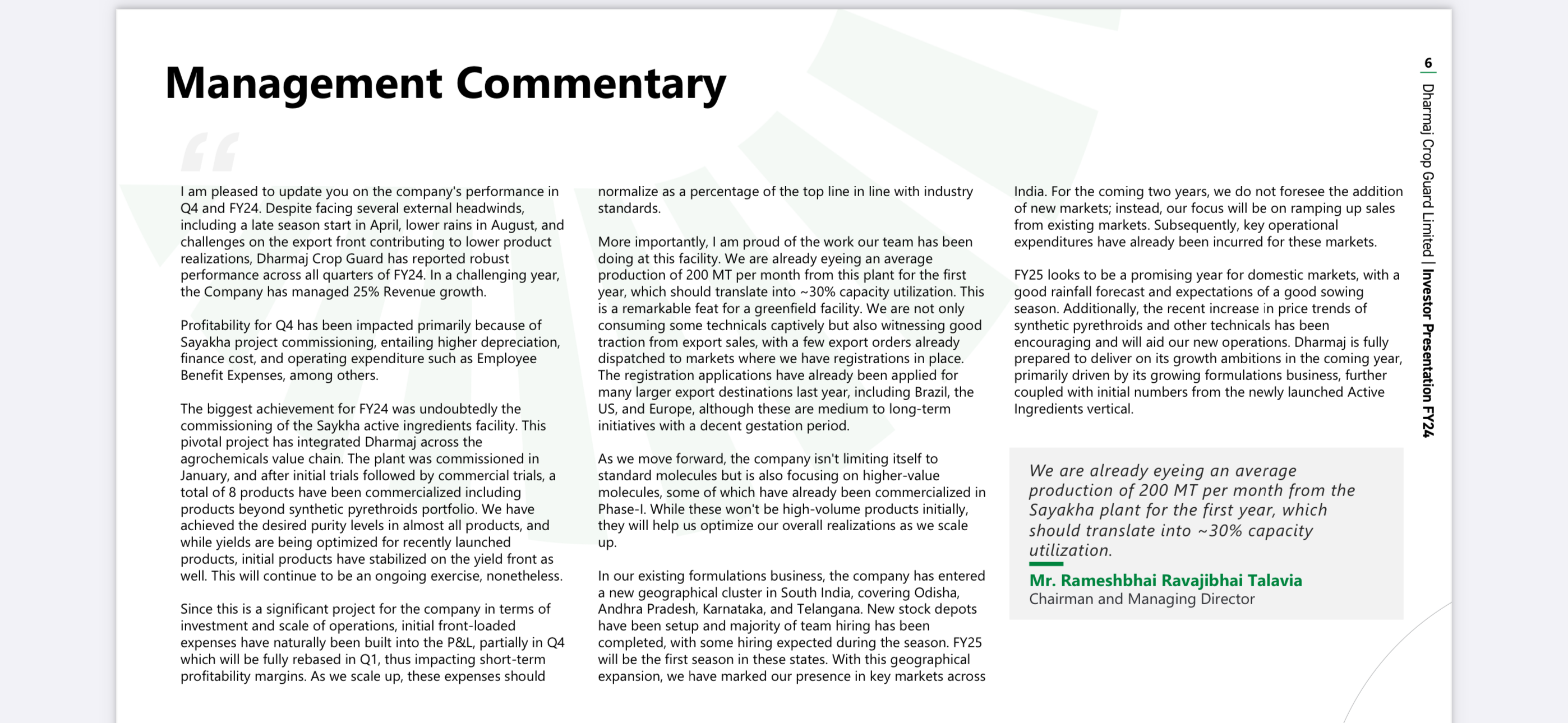

While results look optically bad, the management commentary is important. During commercialisation of new greenfield capex some of the costs are bound to be front loaded which gets normalised as capacity utilisation kicks in. Overall looks quite positive given the sectoral headwinds