Dharmaj had a very good FY24, with sales growing 24% and EPS by 34%. This was a year when most agchem cos had a very bad year. They are confident of 25%+ sales growth in FY25. Concall notes below

FY24Q4

Targeting 900 cr. sales in FY25

Technical division

Started with 7-8 products in phase 1, 5 synthetic pyrethroids (Cypermethrin, Alphamethrin, Lambda Cyhalothrin, Bifenthrin.) + 3 non-synthetic pyrethroids (Thiamethoxam, Chlorantraniliprole, Pymetrozine, Dimethomorph). Have achieved desired purity levels in May

In phase 2, will commercialize 3 new molecules in 2024

Average monthly production of 200 metric tons per month (30% utilization in FY25) - 275 cr. capex

Witnessing price increase in pyrethroids . Gharda is the largest manufacturer for synthetic pyrethroid and have shut plant for last 6-8 months as they are shifting plant from Dombivli to Sayakha which will become operational in 2 years

Started exports in April, achieved 27 cr. sales in April + May (sold 300 tons of synthetic pyrethroid)

Quarterly expenses: depreciation 3.7 cr, finance cost 1.1 cr. (this includes government subsidy), fixed overheads 9 cr.

Targeting 70 cr. annual overheads (33 cr. fixed + 37 cr. variable), 150 cr. sales and 15-20 cr. EBITDA loss

Will breakeven at 200-220 cr. (40% utilization to be achieved in FY26)

Will see 3-4% EBITDA margin improvement by FY27 (and 400-450 cr. external sales)

B2C

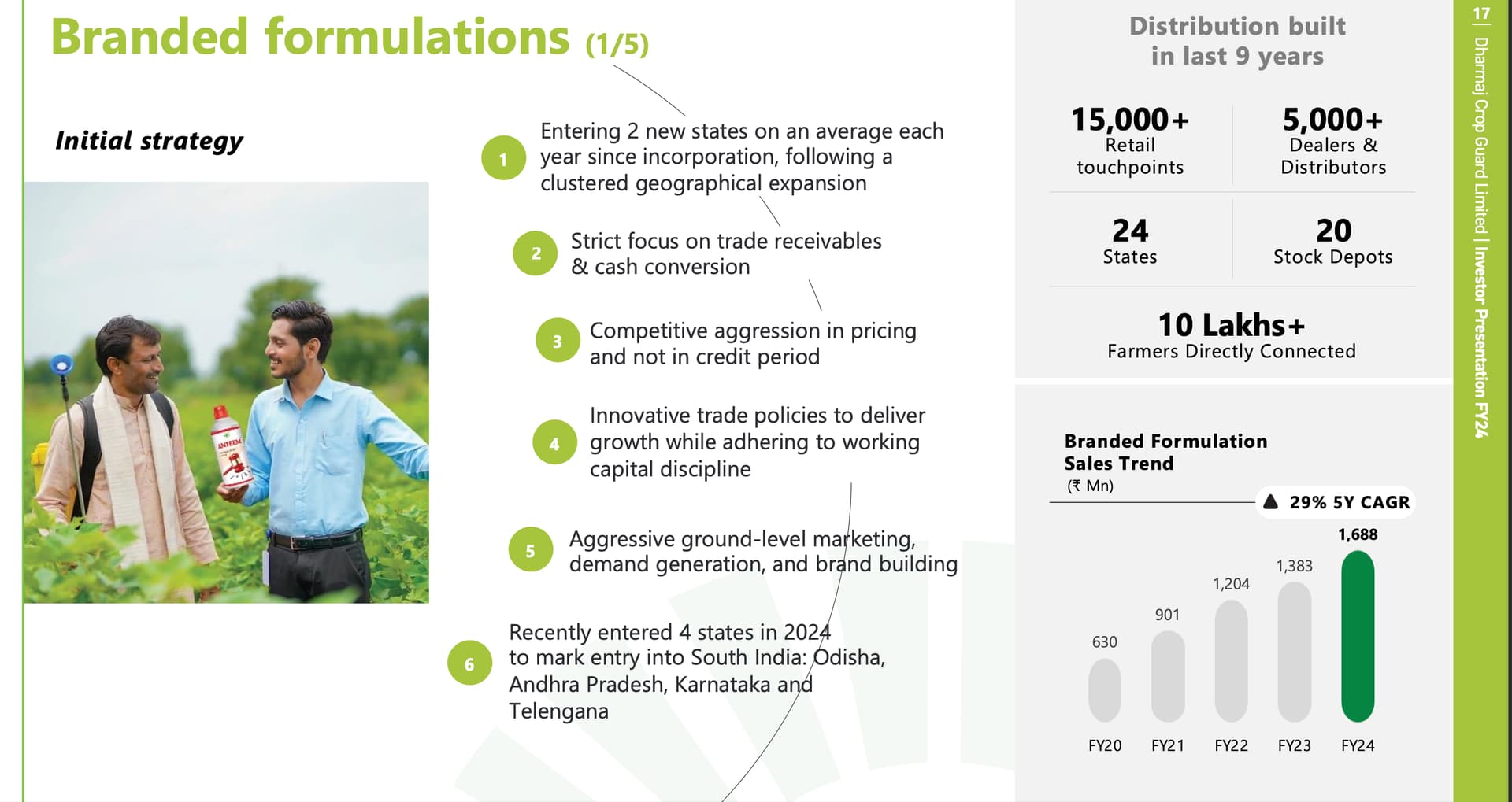

Tapped 4 new states in South India (Odisha, Andhra Pradesh, Karnataka, Telangana) expanding to 24 states. Wont add new states in FY25

Rajasthan grew to 23 cr. (vs 13.5 cr. in FY23)

Gujarat sales was 80 cr.

25% growth target in FY25

B2B

25% growth target in FY25

Volume growth was 45-50% in FY24

Targeting 800 cr. formulation sales in FY25

Reduced payables to avail cash discount

Formulation has 90 days credit period, technical division will have 120 days credit period

Accounting changes

Cash and quantity discounts were earlier reported as other expenses and will now be netted directly from sales. (FY23 revenue has been restated by ~9 cr.)

Out of 275 cr. capex, 260 cr. was on physical assets with remaining being capitalization of interest, consulting fee, intangible items.

6.25 cr. expenses in FY23, one-time professional and consulting fee for Sayakha project

Disclosure: Invested (position size here, no transactions in last-30 days)

Have clocked 35% CAGR revenue growth in last 5 years (though from a lower base). Remarkable that they have been able to achieve 25% growth in FY24 despite a challenging environment where most of the AgChem players were struggling on volume/margin front.

Significant 9x capacity increase underway, major part of that being covered by IPO proceeds (reduced impact of negative leverage in the initial years).

Capex is focused on Pyrathroids, which is 2nd highest type of AgChem globally. 2 levels of backward integration (Technical and intermediates) will help them be cost competitive to gain market share.

Pyrathroids (Global perspective):

Pyrethroids were first developed in the 1950s. Are synthetic chemical compounds that are procured from chrysanthemum cinerariaefolium flowers. Pyrethroids are cost-effective alternatives & less toxic compound as compared to conventionally used insecticides. They are also replacing traditionally used or ganophosphates (majorly used as insecticides).

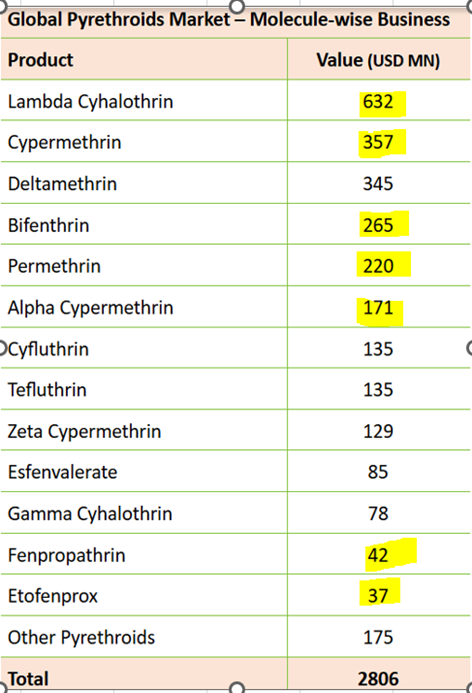

Global Pyrathroid market is estimated to be ~2 Bn USD.

The consumption is concentrated in developing markets like Asia, LatAm and Africa while developed markets like the USA, Canada and the EU have been witnessing a declining trend owing to the newer chemistries and local regulations imposed for restricted usage. (could be a potential threat if the developing markets adopt to the restricted usages guidelines)

Among the Pyrethroids, Lambda Cyhalothrin, Cypermethrin, Permethrin, Alpha Cypermethrin, Bifenthrin and Deltamethrin contribute to about 70% of the total Pyrethroid business generating a revenue of USD 1990 MN.

Global pyrethroid market break up by key molecules. (Highlighted in yellow are the molecules which Dharmaj intends to produce. Good news is that production has already commissioned for top 5-6 molecules starting Q4’FY24. !!!

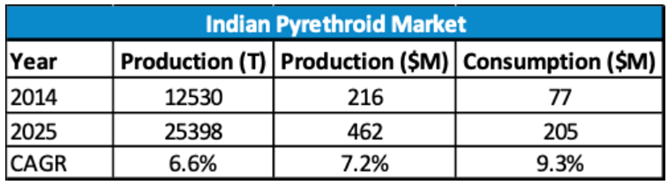

India is the the biggest manufacturer of pyrethroids. In fact supplying intermediates to China.

On demand size, China accounts for more than 50% of global demand for pyrethroids. China used to manufacture pyrethroids after importing intermediates from India. However, China’s pursuit of the ‘Blue Sky’ initiative to realize green GDP lead to the closure of several chemical plants. This in turn resulted in higher volumes of pyrethroids being exported out of India.

The pyrethroid market in India is expected to grow ~10% CAGR. The key driving factor will be regulatory outlook, China factor, wide spectrum crop application and the substitution of organophosphorus compounds.

In 2019, Heranba Industries Limited dominated the India pyrethroids market, accounting for a share of 19.5% of the total Indian pyrethroids production values. Heranba Industries was followed by Tagros Chemicals India (14.8%), Hemani Industries (9.9%), Dhanuka Agritech (8.7%), Insecticides (India) (7.9%), Syngenta India (6.2%), Sumitomo Chemical India (5.8%), UPL (4.2%), Bayer CropScience (3.9%), Rallis India (3.6%), Excel Crop Care (3.4%) and Others (12.1%).

One of the key reason for Heranbas pole position in India pyraethroids market is backward integration in CMAC (Cypermethric Acid Chloride). The EOU facility has made Heranba one of the largest manufacturers of CMAC in India, with new production capacity of ~3000 metric tons per year.

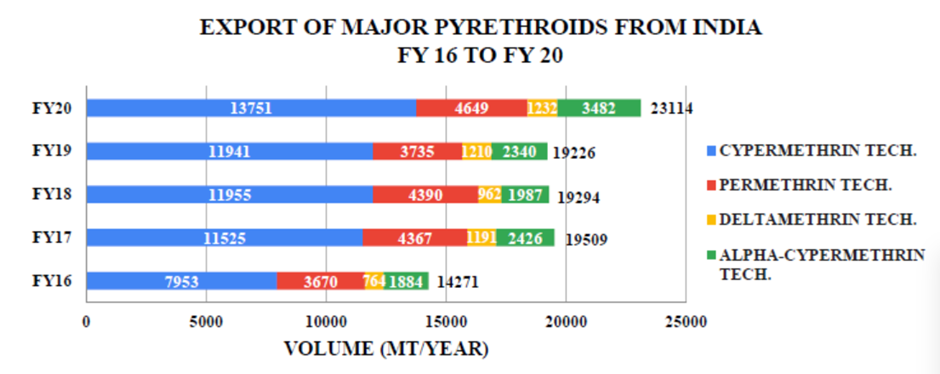

Export contribution by each of the major pyrathroides: (overall and each of the molecules almost doubling in 5 year window between (FY16-20).

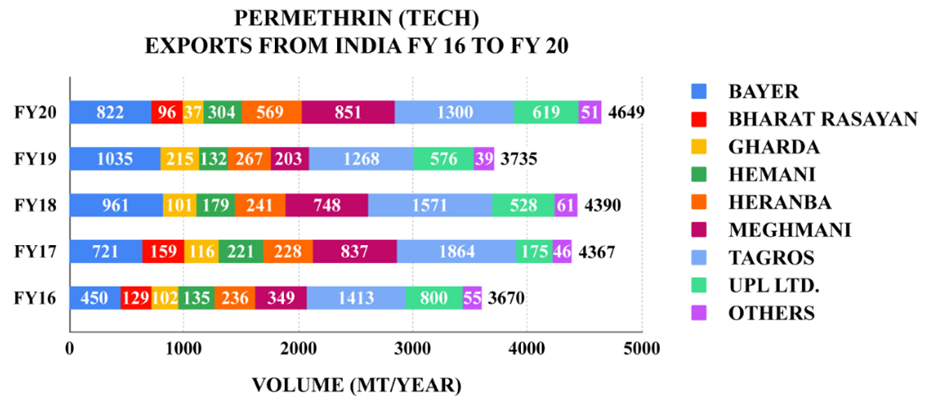

Of all major Pyrethroids produced in the country, Permethrin has a special significance. India is the only manufacturer of Permethrin (Tech.) in the world catering to global Permethrin consumption under all Crop and Non-Crop segments.

Hemani and Heranba has cornered max market share vacated by Gharda and Bharat Rasayan.

Another significant molecule is Transfluthrin, India is the leading producer of Transfluthrin tech. with over 30% market share in the global Transfluthrin tech. business.

Current formulation plant (Ahmedabad) had gone through 2x+ capacity augmentation to 25,500 MT/year between 2022-24 . Running at 51% capacity utilization in FY24. So, significant headroom to ramp-up formulation side of the business. In fact, is well positioned to drive a much better growth aided by backward integration.

Recent capex of ~275 Crs for greenfield capex at Saykha. ~100 Crs each from IPO proceed and Project finance, rest met by internal accruals.

Saykah plant has capacity of 8,000 MT Technical & Intermediates Capacity. Initial plan was for

2,500 TPA dedicated MPBD capacity

2,500 TPA dedicated CMAC capacity

3,000 TPA multi -purpose technical capacity.

However, going by Q4 presentation and concall hints, seems that they have converted MPBD capacity to multi-purpose.

60-70% captive consumption for intermediates • 20 -25% captive consumption for technicals

Somehow, I find striking similarities in the glidepath between Dharmaj and Heranba – be it product profile, break up of revenue across B2b and B2C, domestic vs export, backward integration etc. Hopefully, similarities ends there. (you know what does that mean😉).

Setting up CMAC (Cypermethric Acid Chloride) capacity of 2500 MT/year against the biggest Pyrethroid manufacture Heranba’s backward integrated CMAC capacity of 3000 MT/year is something noteworthy.

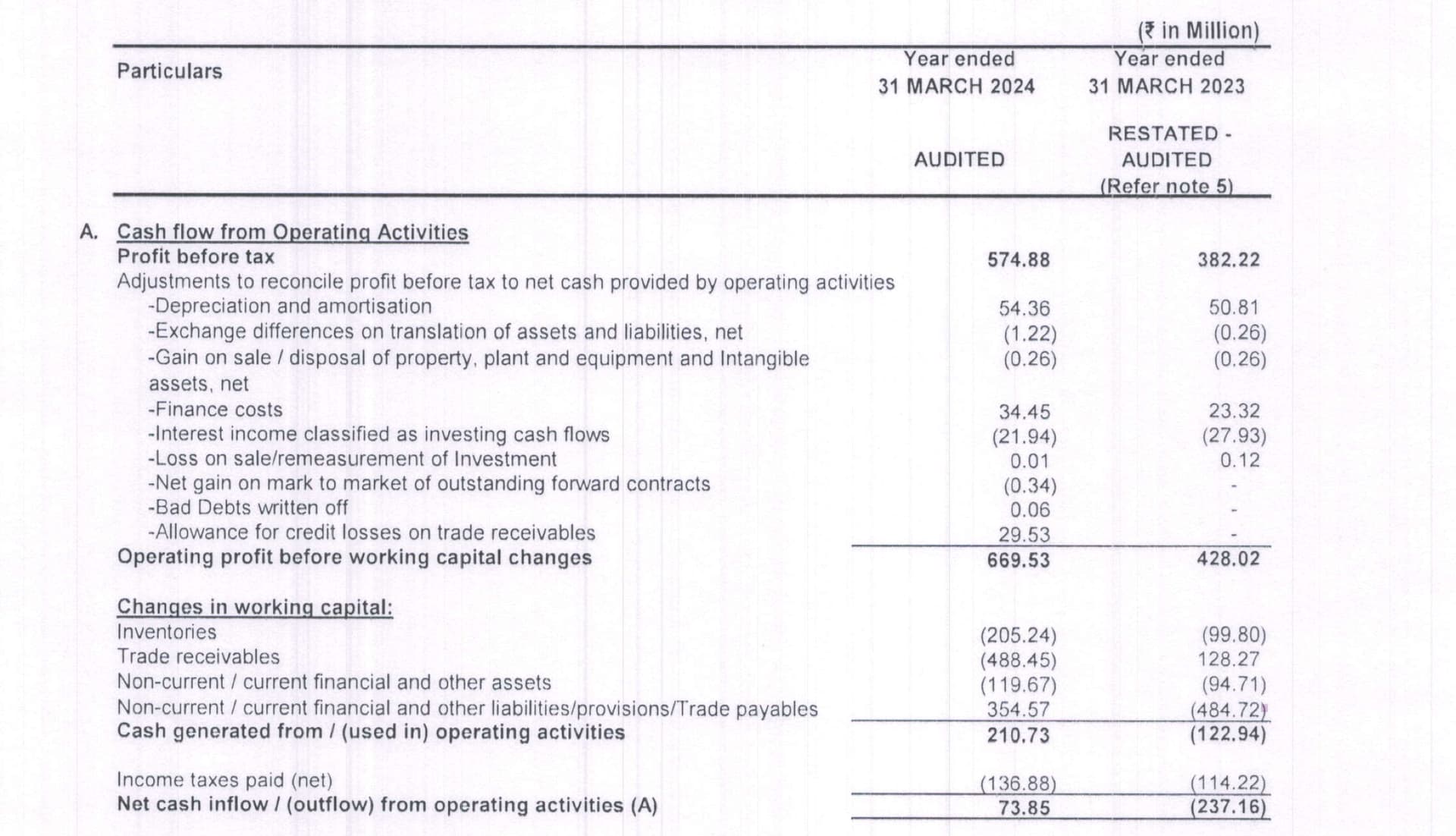

During the latest conference call, one of the analyst mentioned that company currently not generating enough cash flow from operating activities because they’re reinvesting all their cash back into the business. They believe this approach will lead to better cash flow from operations in the future.

Looking at the financial statements, I’ve noticed a couple of key factors affecting their cash flow:

Increase in Inventories: Inventory levels have gone up slightly from 23 to 24, which means more cash is tied up in stock.

Significant Increase in Trade Receivables: There’s been a big jump in trade receivables, further blocking cash flow.

These increases in inventory and trade receivables are the main reasons for the current cash flow issues. To improve cash flow in the future, the company needs to manage and possibly reduce the growth in trade receivables.

By implementing better credit control measures and ensuring timely collections, the company can free up cash that’s currently tied up in receivables, which will help improve their cash flow from operating activities.

Good Q1 numbers, but few red flags from their recent annual report – The auditors draw attention to Note 39 in the financial statements, which discusses the restatement of prior period errors

The auditors referenced a disclaimer in Annexure C that may have an adverse effect on the functioning of the company.

The company’s accounting software had an audit trail (edit log) feature, but it was not enabled throughout the year for certain transactions at the application level. Additionally, the audit trail feature was not enabled at the database level to log any direct data changes

During the year the Company has been sanctioned working capital limits in excess of ` 5 crores in aggregate from Banks on the basis of security of current assets and immovable fixed assets. Based on the records examined by us in the normal course of audit of the financial statements, quarterly returns filed with such Banks are not in agreement with the books of accounts of the Company

According to the information and explanation given to us, the Company has not formalized and documented its internal financial control with reference to financial statements on criteria based on or considering the essential components of internal control stated in the Guidance Note on Audit of Internal Financial Controls Over Financial Reporting (“Guidance Note”) issued by the Institute of Chartered Accountants of India (“ICAI”). Consequently, we are unable to obtain sufficient appropriate audit evidence to provide a basis for our opinion on whether the Company had adequate internal financial controls with reference to financial statements and whether such internal finaancial controls were operating effectively as at March 31, 2024.

The Company has accounted for material prior period errors discovered during the current period, retrospectively by restating the comparative amounts to which the same relate, due to this their last year profit came down from 331cr to 268cr and eps came down from 12 to 9.76

Recently management said – The company is in the process of formalizing internal financial controls to improve business operations. These controls will ensure better systems for safeguarding assets and business continuity. An ERP system has already been implemented to improve transparency and operational visibility.

Seeing good traction with small formulators and have broken through some large customers

B2B growth was driven by Saykha plant, B2C volume growth is higher but lower prices resulted in lower B2C revenue growth

Sales return are always in the range of 1% to 2%, however in FY24 it was slightly above 2% because they have created additional provision on the basis of historical data based on the opinion of newly appointed statutory auditor

Target to launch 8 to 10 product every year With 9(3) registrations in pipeline and it will be a continuous process.

Public and animal health is at nascent stage of growth, they have 12 brands and are expecting good growth in coming years

Have started brand business in southern states and normally it takes 18 to 24 months to develop a market. Around 20% of total revenue comes from new states which were added in recent years.

Saykha capacity will reach optimum utilization in 3-years, current production is in-line with target

50 day cash conversion cycle will not be achievable with scaleup in Saykha plant (higher receivables in B2B + higher inventory). 80-85 days cash conversion cycle is new normal

Normal payables: 45-120 days. Sometimes pay suppliers earlier to avail cash discount

Financial restatement happened after hiring of one of the Big-5 auditor

No major capex plans for 2-3 years

Technical plant they are doing 5 synthetic Pyrethroids and 4 others (CTPR, thiamethoxam, pymetronzine, tebuconzole)

Saw weak exports in Q1 due to delays in export to Bangladesh due to civil unrest

Disclosure: Invested (no transactions in last-30 days)

Dharmaj saw muted formulations growth due to pricing pressure and lower demand, they are expecting a strong rabi season and 15%+ B2C growth. Technical division has ramped up very well resulting in 23% sales growth this quarter. Concall notes below:

FY25Q2

Higher rainfall in August and September disturbed insecticide spraying schedule leading to slower domestic business momentum, expecting strong rabi season

South Indian starts (newly launched) contributed 5.28% to sales

B2C

Witnessed price contraction of ~10% in September which resulted in muted sales despite volume growth, also discontinued 1-2 bulky products.

Expect 15% branded sales growth in FY25

25% of their branded B2C sales come from Gujarat, 12% from Maharashtra, 12% from Madhya Pradesh and 9% from Rajasthan

Technical

Unit 2 at Sayakha witnessed 118 cr. revenues in H1FY25 (manufacturing 8 products). Rampup has been better than projected (50% utilization vs 30% projected). Made ~20% gross margins in Q2. Will be breakeven on EBITDA in FY25, will breakeven at PBT level on 225-230 cr. sales

Targeting peak utilization sales of 450 cr. from technical plant in FY28 with 15-18% EBITDA margins

Higher working capital is due to commercialization of Unit 2 at Sayakha

Incorporating wholly-owned subsidiary in Brazil to expand in LATAM. Applied for registrations for 3 products (Alphacypermethrin, Permethrin and Lambda Cyhalothrin)

Disclosure: Invested (no transactions in last-30 days)

Do you source for this ? Could you please share if you have any report ? On contrary Heranba management commentary is US is a large market for Pyrethroids. I think some where around 2022, the sales from US was 2.5 million dollar and they were expecting 100$ million dollar by FY25. But it didn’t materialize. Still they are at 2.5$ million revenue from US (as per the latest concall).

Though revenue shows an increase YOY, expenses have shot up drastically mainly due to: Cost of Materials Consumed: Increased from ₹794 million in Q3 2024 to ₹943 million in Q3 2025. Changes in Inventories of Finished Goods, Work-in-Progress, and Stock-in-Trade: Increased from ₹ -16 million (negative) in Q3 2024 to ₹ 75 million in Q3 2025.

**Employee Benefits Expense sees a big jump from ₹62 million in Q3 2024 to ₹120 million in Q3 2025.

**Other Expenses also sawa big jump from ₹95 million in Q3 2024 to ~₹ 200 million in Q3 2025

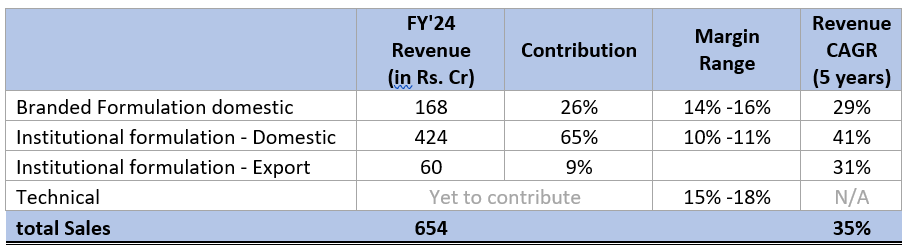

Branded Formulation (20%) 14% revenue growth in FY25

-Institutional formulation domestic(53%) + export (6%)( total 59%). 15% overall growth in FY25

Active Ingredient (21%). Newly commissioned capex in January 2024. 200 cr revenue from first year of operation. Ebitda loss 7 cr Pbt loss 27 cr without 2.5 cr interest subsidy to be recieved. Will breakeven at pbt level for 220-225 cr topline.

Formulation segment has 50% capacity utilisation as of now. So scope of ebitda margin rise and operating leverage going ahead. Though maximum capacity utilisation possible for this segment is 50-60% max possible is 65%

Good cash flow statement among the peers.

Pat margin is lowest historically due to increased depreciation and interest cost due to capex

Q1&Q2 are Seasonally best quarters.

Good ROE&ROCE in last 3-4 years.

Fy26 growth guidance 20-25 % in all segments. Ebitda margin will also improve around 1%. Overall 9.5%. Taking revenue growth of 15% with EBITDA margin as 8% that gives an ebitda of 88 cr vs 75 cr fy25. Fy25 pbt is 46 cr. So fy26 pbt can be 59 cr assuming interest cost and depreciation remains constant. That’s a 28% jump.

Now taking revenue growth of 20% and ebitda margin of 9% gives ebitda of 102 cr that will lead to pbt of 73 cr a 58% jump. 25% rise in topline and 9.5% ebitda margin will give ebitda, pbt and pbt growth of 112 cr, 81 cr, 76%

So range of Pbt growth this year is 28-76%

Q4FY25 concall notes

Industry is going through headwinds in last 2 years.

81% rise in Revenue in Q4 over Q4FY24

FY25 guidance is met for revenue front

Lower pricing environment is going on

Volume growth of 25-30% across segments

Lower product realisation and front loaded expenses didn’t result in rise in profitability.

Met the capacity utilisation and production targets.

Optimistic about khariff season.

Active ingredient segment has operated in lower price range for the full year.

Gained marketshare in industry downturn

Increase in trade receivables due to increase in sales growth

Cash conversion cycle improved from 84 days last year to 67 days this year. This increased CFO

Inventory increase is mainly due to active ingredient business. Remaining is due to upcoming khariff season

Fy26 growth guidance 20-25 % in all segments. Ebitda margin will also improve around 1%. Overall 9.5%.

Not importing finished product from china. Importing RM from china. Will be benefited by china dumping that will lead to rm price reduction.

H1FY26 VS H1FY25 ebitda will be better.

Price is stable. No downward trend March onwards

Stockist like no system. Minor return rehta hai due to wrong product 1-1.5%

Except AI ebitda margin is 11%

Technical level gross margin 19%. ebitda level loss 7 cr Pbt level loss is 27 cr without the interest subsidy of 2.5 cr yet to receive.

Technical can make margin of 22% conservatively this year. At full capacity this plant can do 450 cr revenue. This year did 200 cr.

Pricing situation: stable for last 2-3 month.

Peer: Heranba posting increasing loss.

No major capex going ahead in near term. Chota mota can be done. Like for herbicide segment this year 15 cr.

Ebitda Margin will rise with rise in capacity utilisation.

Capacity utilisation in formulation: capacity utilisation of total Formulation last year was 50% this year is also same inspite revenue growth of around 14% this is due to discontinuation of comodity type products and more focus on high price products. Maximum utilisation possible is 50-60% for formulation facilities as per mgmt. Maximum 65%.

Captive consumption of AI is 31% , 8-10% for formulation of institutionals, remaining is direct sales.for FY25 it was 200 cr.

Technical segment can do 250-260 cr. This should do pbt level breakeven this year. All depends on pricing.

Subsidy is approved. yet to receive. 2.5 cr .

In formulation this year volume growth was 25% but pricing pressure eroded 10% . So this year if pricing remains stable we can do 25% growth in formulation.

Added a lot of new institutional customers this year.

Pricing pressure: due to export being down and over-capacity.

UPL is saying global export should pick up due to inventory destocking is over. So pricing pressure can improve going ahead this year. From UPL concall: UPL reported that global inventory destocking is now largely complete, with most markets returning to normalized buying patterns. FY25 saw strong volume-led growth (13%), though pricing remained weak due to industry overcapacity and price declines (~3%). Active ingredient prices have stabilized, and FY26 is expected to be driven mainly by volume, with limited pricing upside (1–2%). UPL significantly reduced inventory and working capital, positioning itself well with fresh stock and improved liquidity. Overall, the company is transitioning from a recovery phase into sustainable, innovation-led growth.

This year H1 demand situation is much better than last year.

Capacity utilisation target 55-60%

Pat margin guidance: going to improve with revenue growth.

Risk

pricing pressure results in price erosion further down

Dharmaj Crop Guard is finally out of the periodic call auction, and I’m curious if anyone here is tracking the stock. Q1 results were outstanding, if the momentum continues, Q2 alone could potentially deliver earnings close to the entire FY25 EPS, assuming the market environment stays supportive. Would love to hear if others are following this name and how you’re viewing the next couple of quarters.