Looking very good technically

Disc: Invested and biased

Looking very good technically

Disc: Invested and biased

My view is management is very conservative with their guidance of 12% revenue growth with 10-12% margins. 5000cr revenue by 2030 when they are currently at INR 2360cr TTM already with new capex for HFFR and XLPE underway.

Why is market giving this such a low PE multiple - Believe it has had corporate governance issues in past highlighted in Kalpana thread but recent actions of promoter buying till maximum permissible limit upto 75% give some comfort.

Crossed 200DMA today and dont see this having a lot of downside from these levels.

Want to hear the negatives here?

Can you please link that thread/link, so others also can understand the past? Thanks in advance.

[edit - Is this the thread? Kalpena Inds - Stock Opportunities - ValuePickr Forum]

Narrative and Numbers.pdf (728.5 KB)

Management Commentry and the numbers dont match.

Hi,

Please help me to understand two items found in the FY24 Annual Report.

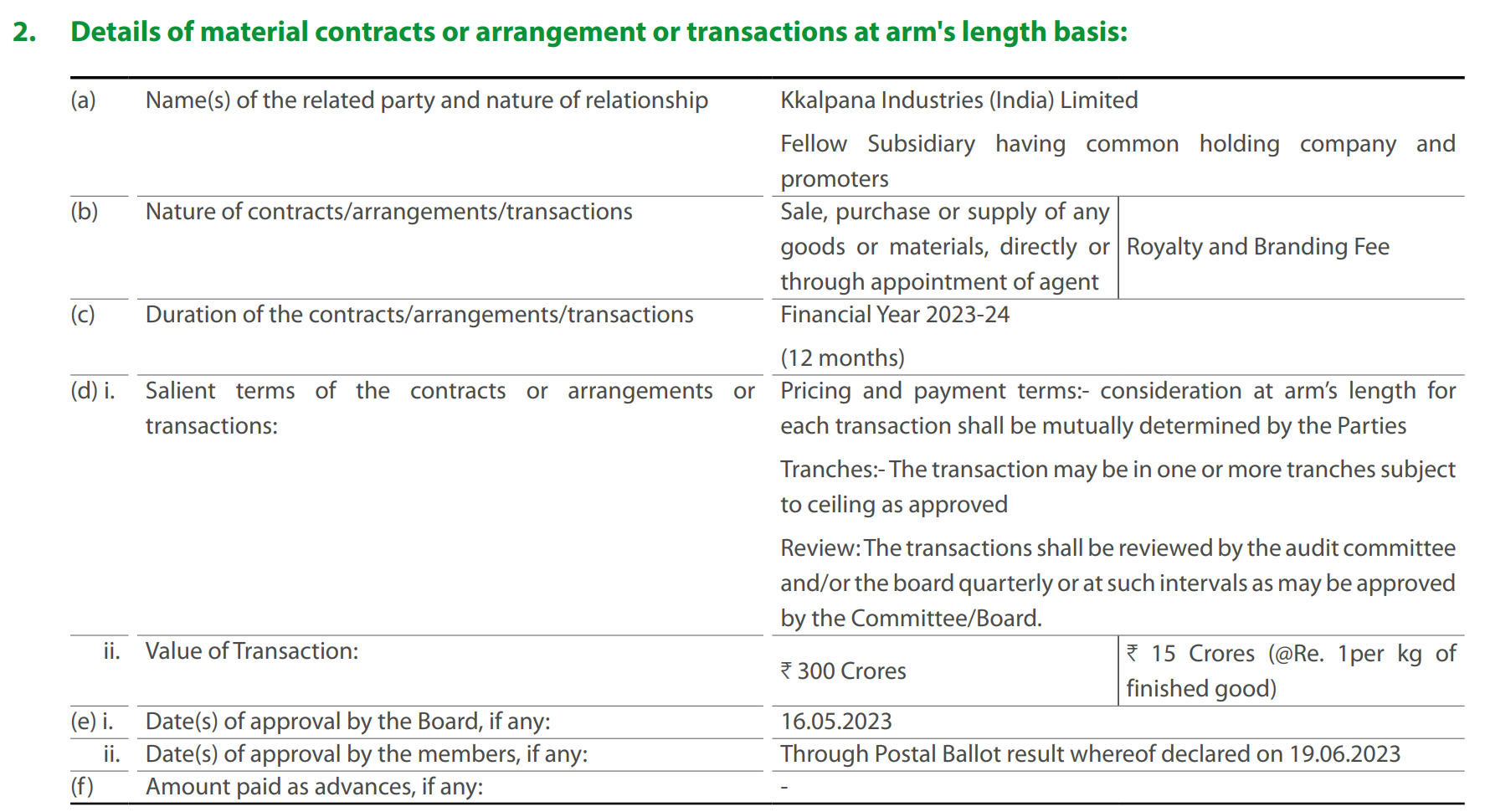

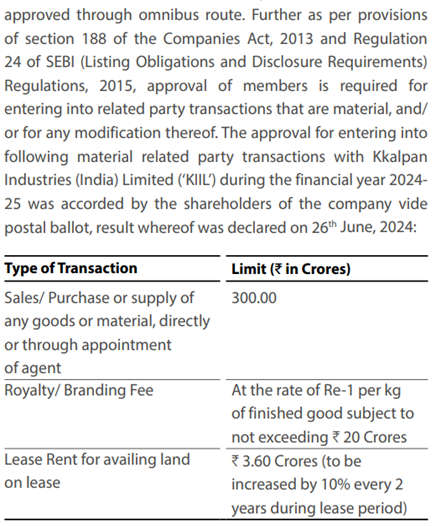

Royalty Expense or Payment done to Kkalpana Industries

Related Party transaction Kkalpana Industries at Page 45 of annual report

Thank you

Seems like one of these has entered today

I have a few basic questions on DDev plastiks. Would request views of the community -

I understand that the selling prices and raw material costs are directly linked to crude prices - so if the crude prices become volatile then is the operating margin of the company defensible? Esp. given that they have approx. 1 month inventory and 2 mths receivable

Competition - the manufacturing process does not seem very complex, so with such high asset turns (implying relatively low capex) and high ROCE/ROE - wouldn’t the space attract several competitors in the space? I understand that the long approval process is an entry barrier, but existing players in chemical/polymer value chain can diversify into this space

With customers also getting into manufactruing of the polymer compound (given low capex and relatively simpler manufacturing) - isn’t that a demand side risk?

what are the red flags (if any) wrt to promoter quality, management, related party transactions, corporate governance issues - i see that there are significant RPT with KKalpana, some royalty payments as well? The financials and past performance track-record of KKalpana (listed) does not show-case a good track-record

If the co. largely focuses on polymers for Wire and Cable industry - isn’t their TAM (Total Addressable Market) rather limited? So this may struggle to be a consistent 15-20% growth story in medium-term if the underlying W&C industry grows at 8-10%?

Finally on valuation - whats the community’s view on a 2year forward PE multiple for a commodity play like this? My sense is, given decent ROCE but modest growth and a commodity play - it may tend more towards a 15x PE rather than the 20-25x band. Given that the stock is at a 16-17x PE TTM basis - then does it imply that the stock-price growth will be limited to the PAT growth of ~15-20%?

Views of the community would by very useful. Thanks

Q1FY26:

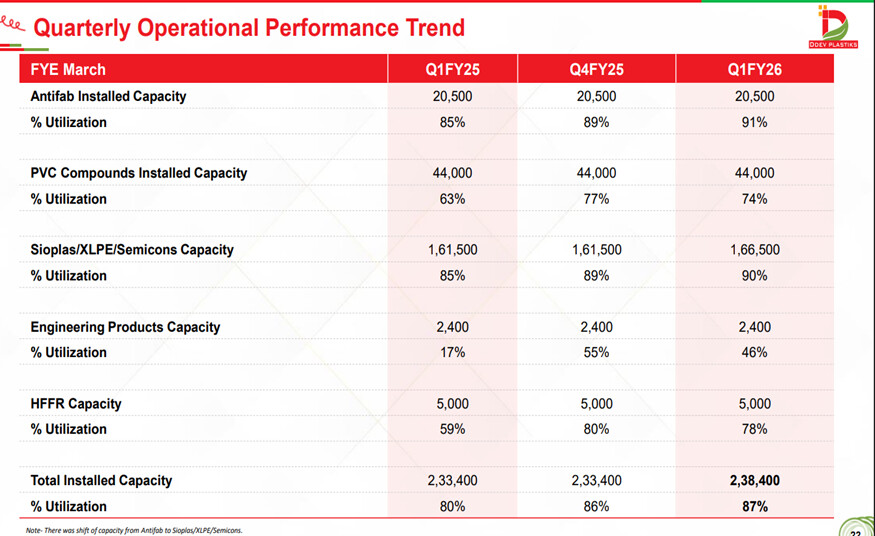

• Current capacity 2,38,400 MTPA. Gross Margin – 16%. EBITDA Margin – 10%

200+ Products.

400+ Employees

• The foray of new players (Adani and Ultratech) in the industry further underscores the necessity of enhancing our production capabilities to effectively serve growing market requirements.

• Efforts are underway to secure certification for our 132 KV cables, with a target to have them commercially available by the end of FY26.

• We remain firmly committed to our long-term goal of achieving ₹5,000 crore in revenue by FY2030, while consistently maintaining double-digit EBITDA margins.

• Multi - location setup; Minimizing transportation costs. Strategically positioned in the East & West coast of India resulting in lower freight costs.

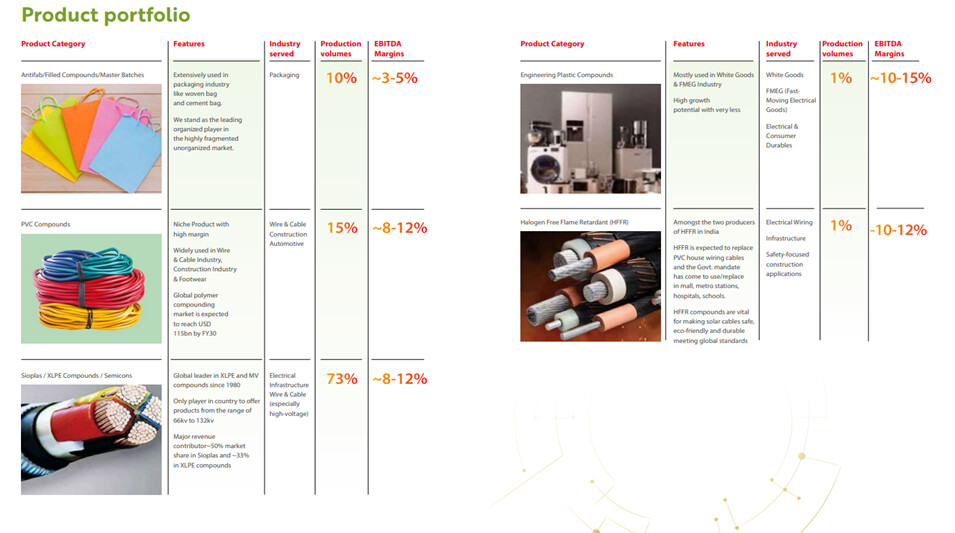

• 50% market share in Sioplas and ~33% in XLPE compounds

• Amongst the two producers of HFFR in India. HFFR is expected to replace PVC house wiring cables and the govt mandate has come to use/replace in mall, metro stations, hospitals, schools.

HFFR compounds are vital for making solar cables safe, eco-friendly and durable meeting global standards

•

• Polymer compounding is a preferred material to electrical industry due to properties such as electrical insulation, corrosion inhibition, excellent heat resistance, high tensile and durability and low density.

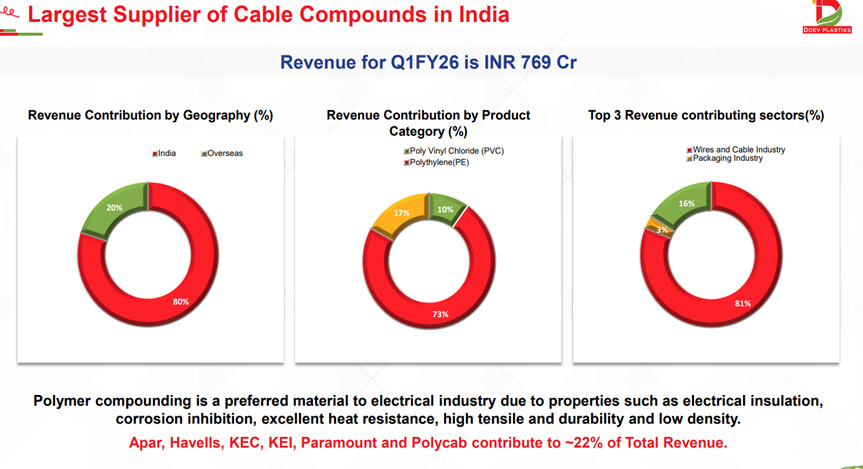

• Indian Cable and Wire Industry projected to grow ~2x of India’s GDP

• 2.5ltpa size of cable compounding industry in India; ~1/3rd of market share with Ddev Plastiks

•

•

•

•

•

• In the quarter, we experienced strong demand from the Cables segment, and our ongoing efforts to shift the product mix towards niche and high - voltage products led to better growth in volumes led by demand from domestic cable players.

CONCALL NOTES:

• Due to critical quality requirements and stringent approval process mandated by end users, polymer compound manufacturing is not amenable to outsourcing. This calls for robust quality control mechanism, advanced in-house R&D infrastructure, and continuous capital investments, making it a high entry barrier industry. With evolving regulatory standards and heightened emphasis on safety and product quality, compliance costs in the wire and cable sector are expected to rise. In this context, legacy players like Ddev Plastiks are well positioned to benefit as large, more organized players.

• Now as big players such as Adani and UltraTech enter the wires and cable space, Ddev Plastiks naturally emerges as the preferred compound supplier, owing to its proven track record and deep industry expertise. As India’s largest listed polymer compound manufacturer, Ddev Plastiks has effectively leveraged the evolving industry dynamics.

• Exports grew 3% yoy in Q1. During the quarter, our export orientation encountered challenges due to geopolitical conflicts. However, we successfully mitigated these impacts by promptly redirecting product to the domestic market, where strong demand enabled swift absorption.

• LONGTERM GUIDANCE: Volume growth of approximately 10% to 15% and revenue growth of 12% to 13%. On a conservative basis, we aim to achieve a revenue of about INR4,500 crores to INR5,000 crores by FY '30. We also expect to maintain a robust EBITDA margin in the range of 10% to 12%.

• 132KV SEGMENT: We would endeavor on getting certification for 132 kV for making it ready for commercial use by end of FY '26, early FY '27.

As we go higher in the voltage rating, the time which is taken for ramping up the volumes is quite long because you have to get the first the cables made, then cables need to get approved. And then the customers will start lifting the product in a small quantum because it is a measure of trust building.

Despite having the certification, the volume growth takes time. So significant volume growth from 132 kV segment alone can be seen beyond 2027, not before that. But the real advantage of being able to deliver 132 kV successfully to the customer and get the approval would be seen in our volume growth for the voltage rating up to 72 kV because when people accept you as a good supplier and reliable supplier, capable supplier for 132 kV, then all the doubts for any voltage rating below that are eliminated and there you are able to grow your business in a bigger way.

132 kV market, I will put the market within the bracket of 132 kV to 440 kV, the market size is just 10% to 12% of the total market size for XLPE insulation for this category. And realizations are generally 10% to 12% higher compared to 72 kV product.

The point is that product is ready with us, but the next step is driven by the fact that it has to be tried by a cable customer. And we are having a tie-up arrangement with a couple of customers, but unfortunate part is that the trial has not taken place yet. So, when we are saying that we will be able to go live in FY '27. It is based on the assurance we are getting from our customers that most likely they will be able to take up our product for trial in the last quarter of, say, third or last quarter of FY '26. It means another 6 months, they will be able to conduct the test and come back with the report approving the product. Then in 2027, FY '27, you may have some volume to start with. So, this is based on the latest interaction we have with the customer. But here, always you can see a possibility of improvement by a couple of quarters in the time line and a delay of a couple of quarters in the time line, depending upon the – how this tie-up delivers.

• 23% sales growth for Q1 FY26 – Volume growth 13%, Value growth 9-10%.

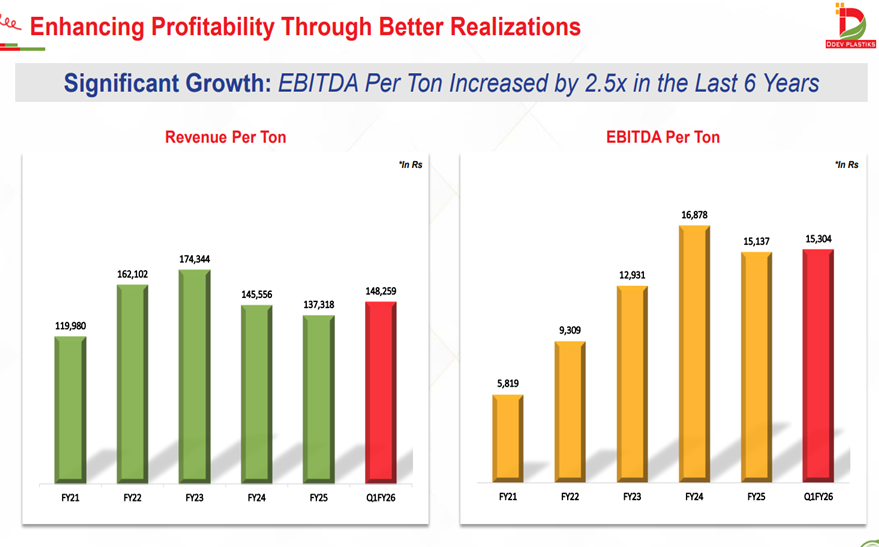

When we see the average selling price, last year the first quarter average selling price was around INR136 and this quarter, we have achieved average selling price of INR148 though as compared to the previous quarter, it is a marginal increase of 50 basis points. But when we compare with the year-on-year quarter basis, it is close to 9%.

• We are targeting a growth of 12% to 13% on a minimum side this year as compared to the previous 3, 4 years. The demand is very strong. And we see that this 12% to 13% minimum growth is there.

• Q2 IS SEASONALLY WEAKER: The quarter-wise volumes may be up and down depending on the environment because second quarter is generally the monsoon season impacts and marginally, the volumes become the lowest as compared to any other quarters. So, we should not see it is on a quarter-on-quarter basis broadly.

So, with the current situation, we see that it may remain at par because monsoon season, generally quarter 2 remains sluggish for us. So as of now, we are seeing it at par.

• Ebitda per ton should improve this year.

• PVC & BUILDING WIRE SEGMENT & ENTRY OF ADANI & ULTRATECH: UltraTech and Adani are planning to enter the wire and cable segment and our inputs from the market and interaction with those investors indicate that the entry will start from the building wires initially. And that is where the PVC’s role is very important.

And our margins because PVC, what we are selling is a basket of multiple products. The product which goes for building wires, the product which goes for the general-purpose jacketing application also. So, building wire per se delivers better margin. So, we are getting ready for that opportunity, which will be offered to us the moment UltraTech and Adani start their building wire activity because we are very strong.

And we have a very strong brand equity as far as this product is concerned because every big wire and cable player, you name anybody starting from Finolex to RR Cable to V-Guard, everybody has started their journey for building wire with our PVC compound to create a brand for themselves. So, we see no difference in case of UltraTech and Adani.

That is why we are adding capacity. And those products are definitely delivering margin of 7% to 8%. So, PVC blended margin might improve as our share for the building wire goes up once these two giants are there in the market.

• UAE COMPETITION & IMPACT OF FTA (DUTY REDUCTION): Sir, in terms of XLPE, is it fair to say that post this FTA with UAE, the competition would have intensified because the import duty on imports done by the UAE-based compounders, they have now become zero. So how are we tackling that competition given that we are also increasing the XLPE capacity?

Yes. So here, the duties have not gone to zero yet because they are going down with a fraction of percentage every year basis. That is one part. And secondly, the people who are supplying from Burj UAE, they are big giants and then their pricing is not driven by this duty advantage. Most of the time, they will try to pocket this duty advantage for themselves rather than passing it on to the customer.

So, they keep on improving their prices wherever there is a duty advantage. So, we have not seen that significant impact. The impact or intensity of the competition is mostly driven by the capacity addition by them. So whenever in say, three, four years, whenever they come up with the additional capacity, then we face a challenge for, say, a couple of quarters or maybe three, four quarters till the capacity gets absorbed in the market. So, we do not see any challenge at this point of time.

• USA MARKET: U.S.A. market is a big market and it will remain our focus because today, the challenge is that the cables which are being exported from India to U.S. market, yes, those will face a challenge and that also for a limited period of time because people will find ways to retain that market because they have created this for themselves with a lot of effort. So, people are working as we are talking to all our cable customers.

But for us, the opportunity is in a different manner. Not only we are supplying to the people who are exporting cables to U.S.A. from India, but we are having U.S. certification. Today, we are having U.S. certification for one product and two products certification is there in the pipeline. Maybe another five, six months, that certificate also will come.

So that will result into an opportunity globally for us. So, we can supply to our product to a customer who is based in, say, for example, UAE. UAE has got a lower rate of duty while exporting to the cables to U.S. market. So, anybody who is exporting cables to U.S. market will become our customer. Only two challenges will be there with us. A, our direct export to U.S. will not grow until this issue is resolved. Second is that our proxy export via our customers in India, yes, that may see a bit of it for some time. But at the same time, the opportunity will emerge from the other markets because those customers will come and buy from us.

• CAPACITY EXPANSION: We are adding when we talk about 3 years horizon close to 15,000-plus tons of HFFR. We have already added 25,000 tons of PVC as a plan for this financial year. And if required, we may add another 5,000 to 10,000 tons. On the XLPE front, on the cable, specifically the transmission and distribution part, we are planning to add close to 60,000 tons of capacity in this next 1.5 years’ time. And that may also increase to another 24,000 tons by next 3 years of time. So, on a consolidated basis, we are talking about close to 1, 30,000-plus tons of capacity being added.

When you talk about the ramp-up, there are two different aspects to it. PVC is, as sir explained, due to the increasing demand expected, it will ramp up with the demand coming in. So, it will be a gradual increase. While XLPE, we already have a demand in place in India and in the global market. So that will see a faster ramp-up as compared to PVC and HFFR. So, on a consolidated level, we see that average utilization would remain above 75% to 80% on a consolidated level.

• There are three categories, I would say. One is low voltage, that is products which are up to 1.1 kV, then the products which are called medium voltage, they are product up to 36 kV and the high voltage, which are product for 66 and 72 kV. So, every segment will have a couple of percentage better margin as we go up higher. Now the margins which we are earning today is a blend of margins we get from the lowest end of the product and the highest end of the product. And as the volumes will grow, so means our projection is not assuming that volume will grow only on a high-end segment. In fact, volumes are higher at the lower end of pyramid. So, volume growth will come from all the segments. So even if we are selling more quantities of high value-added product at a higher end, at the same time, we’ll be selling more product at the lower end of the pyramid also. So blended margins, you will not see much of a difference than where they are today. But at the same time, the introduction of high-end product more and more in our product range and achieving higher volume there would basically protect us from loss of our EBITDA margin because of the growth at the lower end of the pyramid in the volumes.

• Whatever the capex which we are planning, they are not specific to any voltage rating because equipment and the machines are such that they can produce anything starting from, say, 33 kV up to 132 kV in the same setup.

• Going forward, EBITDA growth will be in line with the volume growth (13-14%)

• Targeting to maintain Ebitda per kg of 15-16rs.

• Finance costs to be in current range

• And the biggest demand as we see is the distribution and transmission, 11kV 33 kV and beyond, which we constantly are talking about increasing our capacities. This is a product where due to solar, due to infrastructure improvement, due to electrification of the entire country, not in India, in the global scenario also. This is a major driver of distribution and transmission cables, which is, I will say, is driving the overall growth. So, in terms of percentage growth contributing to the EBITDA, it will always be the distribution and transmission for the next 3 years

• For this current financial year, the volume growth will be probably in the range, similar range (13-14%) because we are already at a very high-capacity utilization levels. Next year, we may see, you can say, a better percentage growth, but that will taper down over a period of time. So, when we see the targets of FY '30, which we have set for us, this average CAGR growth of 13% to 14% of volume growth is coming from that target. It will be initially higher, probably going down at the later part of the period.

• Certain of the other income that is actually operating in nature.

• WHY WOULD A CUSTOMER IN 132KV SWITCH TO DDEV: The customer will switch over to a new supplier because of various reasons. Today, they are fully dependent upon imports. So, they would always love to have the localization. Because the demand for 132 kV is not as consistent and as planned as it is in case of a lower voltage of 66 kV. So, it is all tender-based and certain times, you are having a very good demand in a few months, you have a drop in demand. So, to manage your supply chain well in time to support the demand emerging, you always need to have a local supplier. That is one part.

Secondly, if you don’t have any alternative to imports, you many times end up paying very high premium. It has seen in past in all product categories, our Indian cable customers have benefited immensely, not only Indian, but overseas customers who are buying from us regularly, they have benefited immensely by having a credible supplier like Ddev Plastiks in their portfolio so that they are able to get reasonable prices from their other suppliers\

Just for example, when we say that why a customer for 132 kV should switch to another supplier like Ddev Plastiks. Now I’ll give you an example, say, UAE is a place where the Burj is place they have their plant capacity and they are having some duty advantage over us. Despite that, the customers who are based in UAE preferred continuously to buy certain quantity from us.

So, everybody needs to diversify their supply chain so that they do not suffer shortage of material or the price source.

• So, starting from Finolex, RR Cable, V-Guard, KEI, Havells, all these guys, when they came for launching their building wire, the first PVC compound they bought was from Ddev Plastiks or our Kkalpana Industries. And later on, they might have moved to other suppliers. But initial few years, they have been 100% dependent upon us. Why? Because our product has got that capability of running at a high speed, giving very good surface finish consistent properties, which have been proven over a period of time.

Another aspect, just to give you a perspective, even today, whenever somebody is going for BIS certification for any type of their cable initially, they would prefer to buy material from us. Why? Because they feel safe that, yes, if we are buying this product, we will not face any hiccup in BIS certification because product is above standard, okay? So, this is the reason we are confident that these 2 customers also will be our customer for first few years. That is one. And with both of them, we are already in touch. We do not have any firm RFQ, but we are having indication that they will love to work with us.

• Proxy export to US by our customers in India could be, I think, close to INR100-150 crores.

• So, this is a segment, which I would say starting from 11 kV to 132 kV XLPE insulation market, where rather today, it is 66 KV and going forward, 132 KV, where our current market share stands at anything between 30% to 33%, we want to take this market share beyond 50%. So, this is the biggest growth driver.

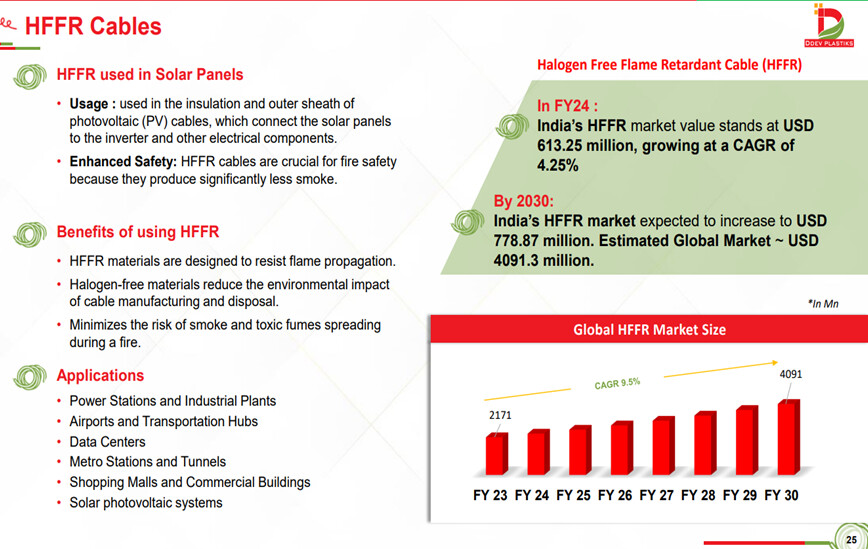

• HFFR: Second is halogen-free flame retardant. There, we have multiple times in our earlier conferences also, we explained that we see this market growing at a good pace, which was close to 25,000 tons per annum kind of a market, which we see with the natural progress, whatever it is showing at the moment should reach close to 100,000 tons per annum kind of a thing by 2030. And there, we are planning a capacity of 20,000 already we have committed, and we are anticipating probably we’ll add more capacity there. So, we’ll have much larger share in that market. Today, our market share is negligible in that segment. Market is very small. So, both the things will happen simultaneously. Market size will grow and our market share will grow. So, these are the two product segments which will drive our growth.

HFFR demand growth, the key driver is the solar cable application. So, if you look at our capacity starting from 5,000 tons and ending up at 25,000 tons by 2030, so it is the kind of 5x growth in that product segment and majority will come from the solar side.

There are many products which can meet the specification, which governs the solar cable. But Halogen-Free Flame Retardant is the most optimum product, which will deliver you right value at right price point, covering all the properties which are required for solar cable application. Like to specify, for example, the weather resistance, weatherability, because the cables are going to stay in open environment for a longer period of time, higher level of UV stability, higher level of flame retardancy, safety against fire. So, all these features, you can incorporate in the most cost optimum way with halogen-free flame retardant. You cannot achieve the same through PVC or XLP.

So, you can anticipate that this year, we’ll be having – this will – we will be closing around 10,000 tons of HFFR and then the following year, we’ll be adding another 10,000 tons

Revenue contribution, more or less you can think that on a broader basis we are anticipating INR250 crores to INR300 crores by FY '28.

EBITDA margin is slightly better than 15%. So, this will be the value-added products from which we will be eyeing to further profitable growth and the incremental margin.

Neat writeup.

Who are the biggest competitors currently to DDev? Internal as well as external?

ARFY26 MISCELLANEOUS NOTES:

•

• Renewable Energy Initiatives: The largest facility in Surangi has approximately 1.7 MW of solar panels installed, supplying almost 20% of its captive power requirement. We also plan to expand renewable energy installations at greenfield sites to the optimum capacity possible. The installation of solar panels at the Surangi unit has reduced carbon emissions by 80 MT per month. Through a Power Purchase Agreement with Amplus Solar, an additional 1 MW of solar power has been installed, bringing the total capacity to 1.7 MW.

• To drive greater operational efficiency, we are collaborating with stakeholders to reduce manual intervention in raw material handling and finished goods packaging. While automation technologies are already integrated into our packaging lines, we are continuously exploring new avenues to extend automation across more stages of our operations - ensuring higher productivity, lower costs and greater consistency

• Smart locations, Smarter logistics: Ddev Plastiks keeps transportation costs in check with a powerful logistics strategy. Manufacturing units placed near key ports in the East and West mean smoother transits, better storage, and more feasible export options. Combined with warehouses and offices in the North, we cut down delivery timelines, optimise routes, and stay closer to our customers than ever before.

The Multi location setup helps minimize the transportation cost by being closer to suppliers (ports) and customers and wide range of extruder capabilities provide flexibility to produce custom quantities for wide range of customers.

•

• R&D and technology: We actively collaborate with leading institutions like IIT Kharagpur and the University Institute of Chemical Technology (Mumbai) to co-develop innovative solutions that meet the evolving needs of modern industries.

The in-house ability for designing and testing new compounds with large fully equipped labs and experienced and skilled team and strong R&D has resulted in large pipeline of new products under development based on the customer’s feedback and requirements.

• We successfully expanded our product portfolio to include High Voltage PE based cable compounds and enhanced Halogen-Free Flame Retardant (HFFR) offerings, further strengthening our leadership in the polymer compounding industry.

We developed a high-performance Water Tree Retardant (WTR) XLPE compound for 72KV cable insulation, which was previously imported and now manufactured in-house, supporting ‘Make in India’ goals. The compound offers superior resistance to moisture-induced electrical treeing, enhancing cable life and performance, and has successfully passed long-term validation tests at the renowned VDE Laboratory in Germany.

We maintained our position as India’s largest manufacturer of XLPE compounds, offering over 200 customised SKUs to meet the evolving needs of diverse industries.

• Development is already underway for 220 KV cable compounds, a technically demanding product with a rigorous approval cycle of two years. Factoring in review timelines, we are targeting commercial availability by FY 2029.

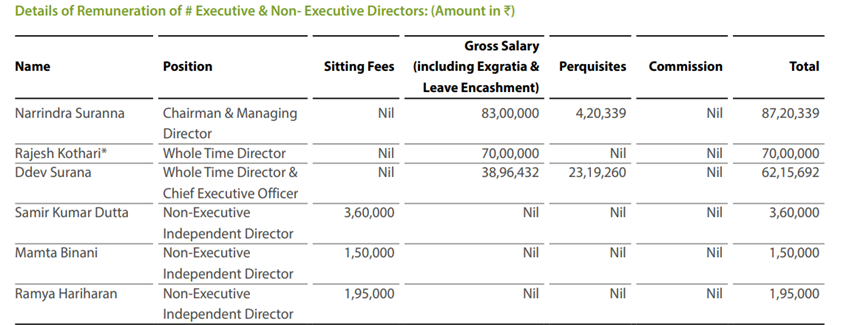

• Ddev Surana (CEO) current remuneration is Rs. 49.50 Lakhs. (Taking into consideration the size of the Company, the profile of the Whole-time Director and Chief Executive Director and the responsibilities shouldered by him and the industry benchmarks, the remuneration drawn by Mr. Ddev Surana is much less when compared to remuneration packages paid to similar senior level person in other Companies)

• The global wire and cable market was USD 267.8 billion in 2024 and is set to register at a CAGR of 7.3% from 2025 to 2034, propelled by the ongoing inflow of funds towards the establishment or refurbishment of transmission and distribution networks to cater to the growing electricity demand across the globe.

• The arrangements with most large suppliers and large sourcing quantities result in priority treatment from suppliers and cost effectiveness.

• Business risks: Your company has to face intense competition from unorganized sector and imports pertaining to plastic compounds.

The Company competes with other producers who manufacture similar goods both in India and abroad in a fiercely competitive market.

There is fierce competition, with global rivals like Dow and LG growing their capacities and market share.

•

• The number of permanent employees on the rolls of Company – 391 (vs 376 in FY24)

Average salary increase of non-managerial employees is 13.26%. (9.2% in FY24)

Average salary increase of managerial employees is 10.58%. (9.8% in FY24)

•

•

•

(Net profit – 185cr. Managerial remuneration – 2.2cr. Even if we calculate royalty income of 4.5cr paid to Kkalpana Industries, total comes to 7.7cr)

•

(26 and 57 in FY24)

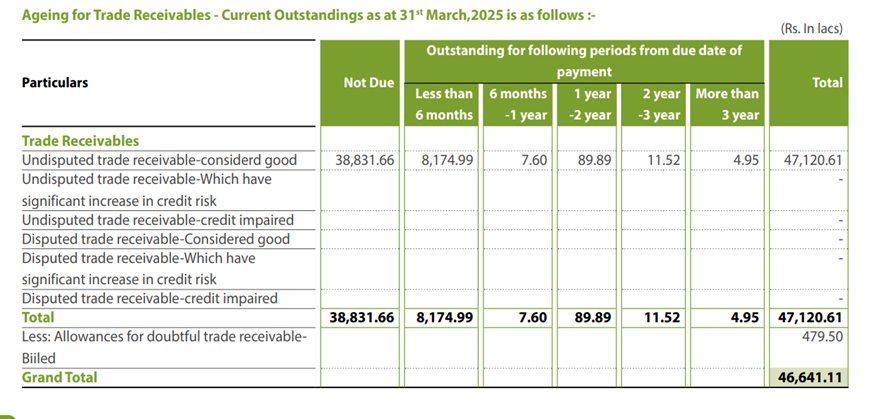

• Provision for Doubtful debts – 0 vs 4.99cr in FY24

Bad debts written off – 79.44 lacs vs 0 in FY24

•

• There are no advances to directors or other officers of the Company or any of them either severally or jointly with any other persons or advances to firms or private companies respectively in which any director is a partner or a director or a member.

•

•

The only red flag which was present in ddev has been substantially reduced this FY.

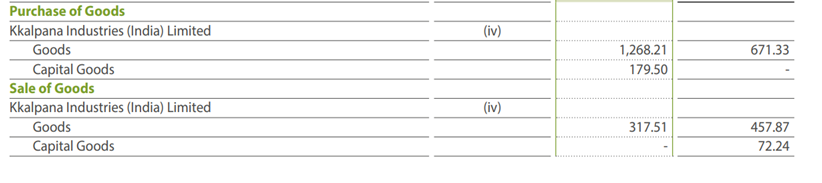

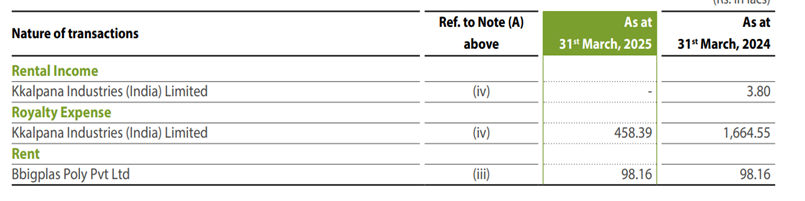

ROYALTY PAYMENTS.. to KKalpana industries

4.58 cr paid (2.4% of net profit for the year) vs 16.6 cr last year (9% of yearly PAT)

This along with managerial remuneration being very acceptable (2.2cr) is a very good sign and hopefully continues in the future.

NO OTHER RED FLAGS

DISCLOSURE - INVESTED