Executive Summary

Ddev Plastiks Industries Ltd. (DPIL) stands as a notable leader in the polymer compounding industry, distinguished by its robust capacity of 239,000 MTPA. The company has carved out a significant market share by producing a diverse range of products such as polyethylene compounds, PVC compounds, and HFFR compounds. DPIL’s strategic approach, leveraging advanced R&D and maintaining a strong clientele base, including marquee names like KEI Industries and Havells India, positions it advantageously for sustained growth.

Despite an environment of high competitive intensity and raw material price volatility, DPIL has consistently showcased financial resilience. With an expanding product mix geared towards higher-margin offerings and a keen focus on operational efficiencies, DPIL has improved its EBITDA margins significantly. It maintains a lean operation with minimal long-term debt and showcases a commendable debt-to-equity ratio, which has been reducing over the years.

In terms of performance metrics, DPIL excels with a ROCE of 32.5% and an ROE of 23.5%. The company has also been proactive in shareholder returns, as evidenced by its consistent dividend policy with yields between 0.5% to 1%.

However, DPIL is not without its challenges. The company must navigate the risks associated with raw material supply dependency, competitive pressures from international giants, and currency rate fluctuations. Corporate governance also remains an area of scrutiny due to the company’s historical associations.

As DPIL continues to invest in high-margin and technologically advanced products, the potential for market re-rating becomes evident. The company’s stock, trading at a PE ratio significantly lower than the industry average, suggests a latent opportunity for value realization. With prudent financial management and strategic market positioning, DPIL appears poised for re-rating and continued prosperity.

Company Overview

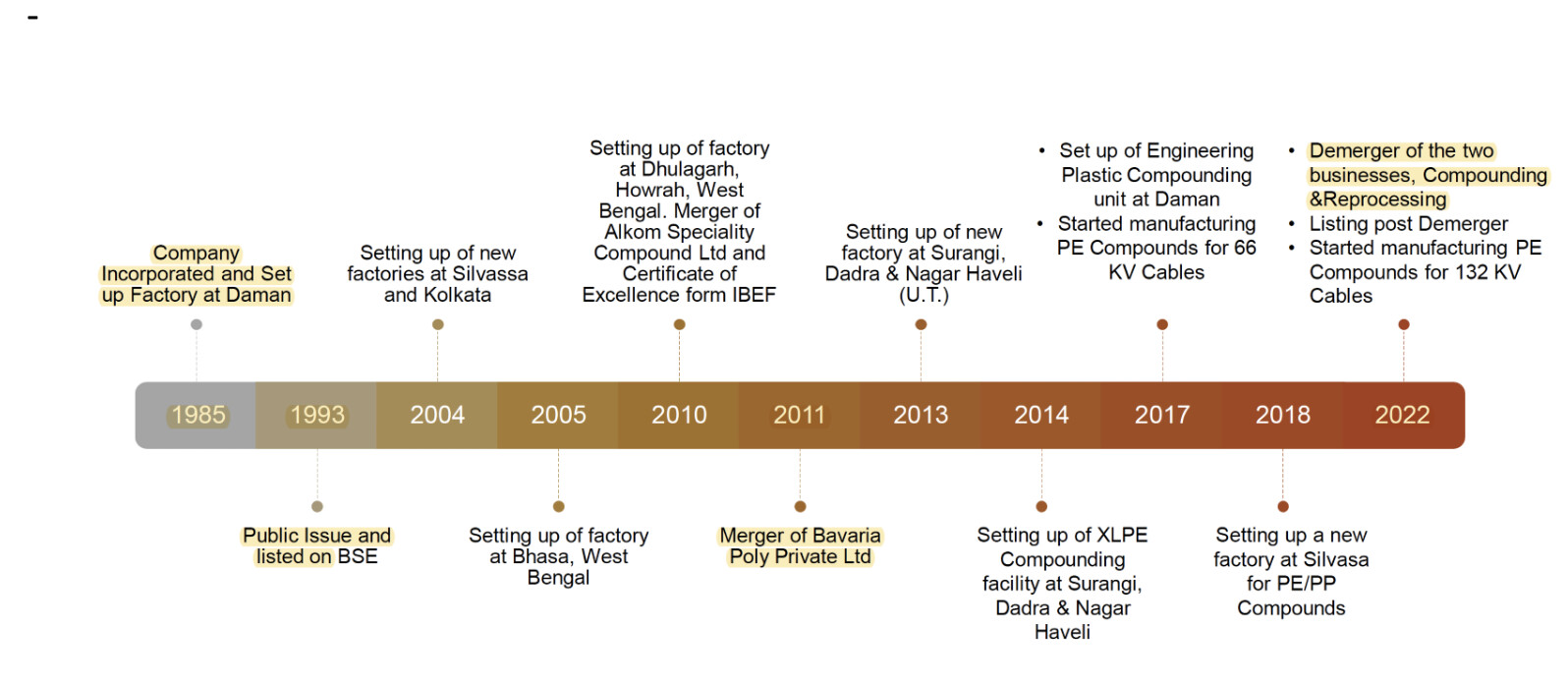

Ddev Plastiks Industries Ltd. (DPIL) is a renowned entity within the polymer compounding sector, emerging as a powerhouse post its demerger from the Kkalpana Group. DPIL’s roots trace back to 1985, starting with a manufacturing unit for PVC compounds in Daman, India. Over the years, DPIL has substantially scaled up operations across various locations including West Bengal, Daman & Diu, Dadra & Nagar Haveli, and Noida, India.

Core Business and Products

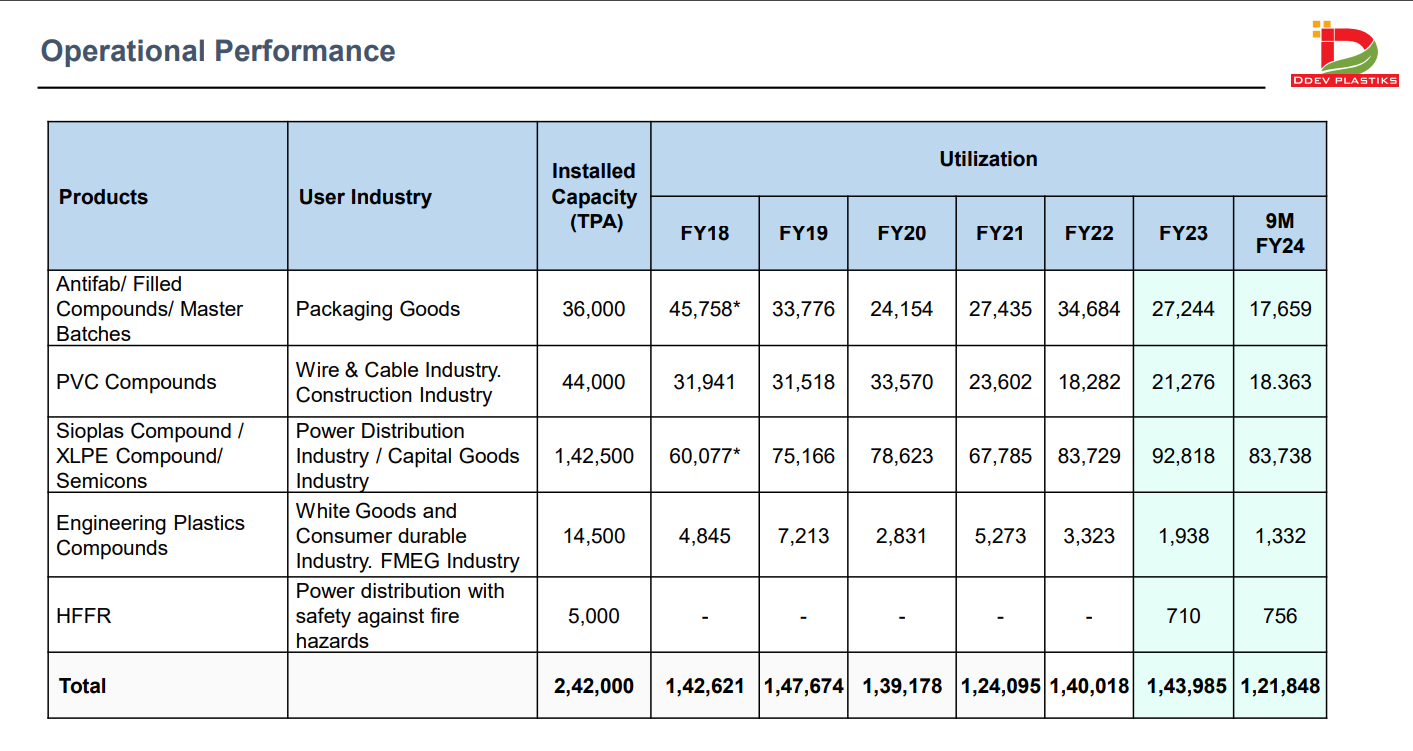

DPIL’s core business revolves around producing a wide array of polymer compounds critical for multiple industrial applications. Their portfolio includes:

- Polyethylene (PE) Compounds: Used extensively in cabling solutions for low to high voltage applications.

- PVC Compounds: Catering to a spectrum of industries from construction to automotive, for various insulation and sheathing needs.

- Cross-Linked Polyethylene (XLPE): Known for its superior insulation properties and used in high-performance cables.

- Halogen Free Flame Retardant (HFFR) Compounds: Reflecting DPIL’s commitment to environmental sustainability and safety, these compounds are used where low smoke and low toxicity are crucial.

Manufacturing Excellence

DPIL has optimized its manufacturing prowess to produce compounds that meet stringent international standards, ensuring a global appeal. Its facilities are strategically located to leverage logistical advantages and cater to a growing export market.

Research & Development

Innovation is the cornerstone of DPIL’s success. The company has invested in state-of-the-art R&D centers to pioneer the development of new compounds that offer enhanced performance while adhering to the evolving environmental regulations and industry standards.

Sustainability and Corporate Social Responsibility

Sustainability is woven into DPIL’s operational fabric. The company has instituted green initiatives, such as solar power adoption and water harvesting, to minimize its environmental footprint.

Governance and Leadership

With a legacy spanning over three decades, DPIL is steered by a leadership team that brings a wealth of industry experience. The company’s governance structure is designed to uphold the highest standards of ethics and accountability.

Industry Analysis

Ddev Plastiks Industries Ltd. operates in the polymer compounding industry, which is a vital subset of the broader chemical manufacturing sector. Polymer compounds are essential materials used across a wide range of industries, including automotive, electronics, construction, and telecommunications. The demand for these products is closely tied to the growth of these end-use sectors.

Market Dynamics

The polymer compounding market is characterized by its diversity of applications and the continual evolution of material science. Innovation drives the development of new compounds that meet increasingly stringent industrial, environmental, and safety standards. In recent years, there has been a significant push towards sustainable and eco-friendly materials, such as HFFR compounds, driven by regulatory changes and shifting consumer preferences.

Competitive Landscape

The industry is competitive, with several large multinational corporations dominating the high-end specialty segments of the market. These players, with their expansive product lines and economies of scale, pose a competitive challenge to smaller players like DPIL. However, DPIL’s focus on specialty and high-margin products has allowed it to carve out a niche and remain competitive.

Market Positioning of DPIL

DPIL has established itself as a leader in the domestic polymer compounding market, particularly in PE compounds for the wire and cable industry. The company’s significant market share is supported by its diverse product range, large-scale operations, and robust R&D capabilities. DPIL’s strategic focus on high-margin products and continuous product development has allowed it to maintain and expand its market position despite intense competition.

Industry Growth Prospects

The industry’s growth is forecasted to remain strong, propelled by global trends such as urbanization, infrastructure development, and technological advancements in the automotive and electronics sectors. The Indian market, in particular, is expected to see substantial growth due to the government’s focus on infrastructure and the increasing demand for energy and telecommunications services.

Key Drivers and Restraints

- Drivers: Growing infrastructure projects, technological advancements, increasing demand for electrical and electronic products, and a shift towards sustainable materials.

- Restraints: Volatility in raw material prices, regulatory challenges, environmental concerns, and the threat of substitution by alternative materials.

Financial Analysis

A comprehensive examination of Ddev Plastiks Industries Ltd.'s financial health reveals a strong fiscal position and noteworthy growth metrics. Let’s break down the key financial elements:

Revenue Growth and Profitability

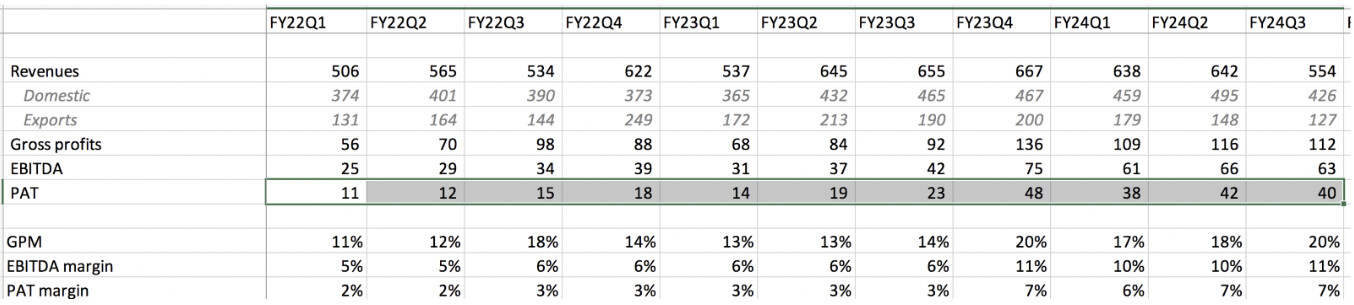

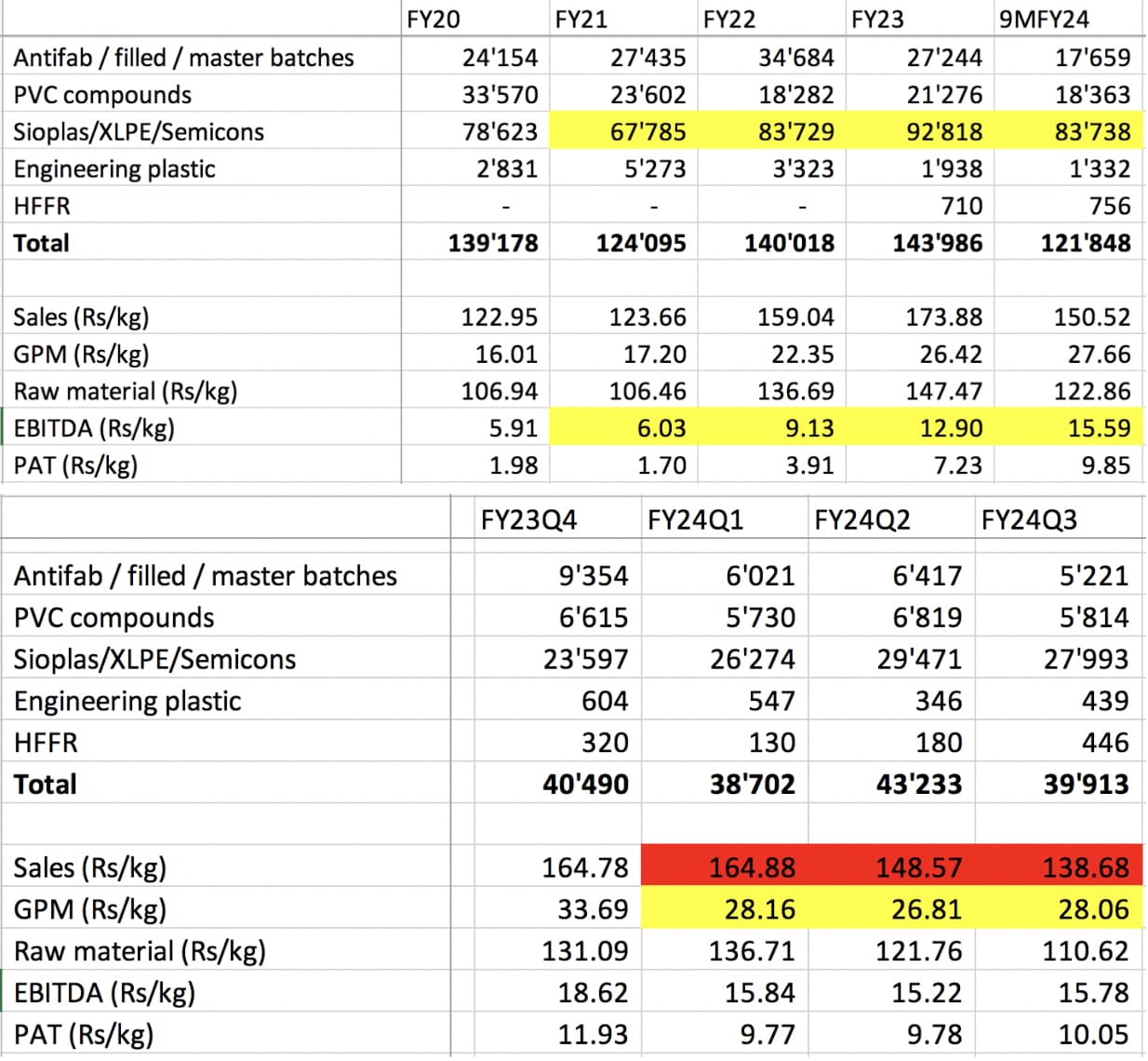

DPIL has consistently displayed a robust revenue trajectory, with operating revenue reaching ₹2,509 Crore. This growth is propelled by the company’s strategic initiatives to expand its product portfolio and penetrate new markets. The improved profitability, with an operating margin that has increased from 5% in 2022 to 10% in the TTM period, is indicative of effective cost management and a higher proportion of value-added products.

Return on Capital and Equity

The company’s return on capital employed (ROCE) and return on equity (ROE) are exemplary, with figures of 32.5% and 23.5%, respectively. These metrics are among the highest in the industry and illustrate DPIL’s efficient use of capital and shareholder equity to generate profits.

Debt Management

DPIL has demonstrated prudent debt management, significantly reducing its debt from ₹130 Crore in 2021 to ₹45 Crore in September 2023. The debt-to-equity ratio has followed this downward trend, dropping from 0.33% to an impressive 0.08%. This reduction underscores the company’s commitment to sustaining a strong balance sheet and reducing financial risk.

Cash Flow Metrics

Cash flow efficiency is a hallmark of DPIL’s financial stability, with a CFO to PAT ratio of 139.42% and a CFO to EBITDA of 112%. These ratios reflect the company’s ability to generate cash from its operations, funding continued expansion and innovation without relying excessively on external financing.

Dividend Policy

DPIL’s dividend policy has been consistent, offering yields between 0.5% to 1%, demonstrating its commitment to providing shareholder returns. The steady dividend payouts, even amidst expansion and growth, speak to the company’s sound financial planning and confidence in its cash flow stability.

Liquidity and Capital Expenditure

With robust internal accruals and controlled capital expenditure, DPIL maintains strong liquidity, enabling it to navigate market uncertainties effectively. The company’s capital allocation strategy balances between reinvesting in the business and rewarding shareholders, positioning it well for sustainable growth.

The financial analysis paints a picture of a company with disciplined fiscal management, impressive growth, and profitability metrics, and a solid foundation for continued success.

Valuation and Market Performance

Evaluating Ddev Plastiks Industries Ltd.'s market performance and valuation involves analyzing how the stock is priced relative to its earnings, the returns it provides to shareholders, and its market capitalization.

Stock Valuation

As of the latest financial data, DPIL’s stock trades at a price-to-earnings (PE) ratio of 10.5, significantly lower than the industry average PE ratio of 30.4. This disparity suggests that the stock may be undervalued, presenting a potential opportunity for investors, especially when considering the company’s robust financials and growth prospects.

Market Capitalization

With a market cap of ₹1,773 crore, DPIL is considered a small-cap stock. This classification often comes with higher growth potential and possibly higher volatility. However, given the company’s strong fundamentals, it may also mean that DPIL is poised for re-rating as it gains more visibility among investors.

Dividend Yield

DPIL’s dividend policy reflects a yield ranging from 0.5% to 1%, underscoring the company’s commitment to consistently rewarding its shareholders. This yield, coupled with the company’s low PE ratio, contributes to making DPIL an attractive stock for value investors.

Historical PE Ratio

Historically, DPIL has traded at higher PE ratios. The current PE of 10.5 is at a historical low since the company’s listing, indicating that the stock might currently be trading at a discount to its intrinsic value based on earnings.

Promoter Holding and Insider Trading

Recent insider trading data show that the promoter has increased their holding, purchasing 1,25,000 shares at ₹175, signaling confidence in the company’s future. This purchase price is slightly above the current trading price of ₹171, further indicating that the promoters believe the stock is undervalued.

Institutional Interest

With minimal institutional holding and no significant DII involvement, DPIL remains largely undiscovered by major institutional investors. This factor could be seen as a potential for upside if the company attracts institutional attention, leading to increased demand for the stock and possible re-rating.

Comparison with Industry Peers

When compared to its peers, DPIL’s financial metrics, particularly the growth in OPM from 5% in 2022 to 10% in TTM, stand out. This comparison underlines the company’s operational efficiency and effectiveness in capital utilization.

Strategic Initiatives and Future Outlook

Ddev Plastiks Industries Ltd. (DPIL) has embarked on several strategic initiatives that align with its future outlook and core objectives of growth, innovation, and sustainability.

Product Expansion and Diversification

DPIL has significantly expanded its product portfolio by introducing high-margin products like XLPE compounds and Halogen Free Flame Retardant (HFFR) compounds. These products are in line with global trends towards more environmentally friendly and safety-compliant materials, particularly in the construction and automotive industries.

Targeting New Markets

The company is aggressively targeting new markets to expand its global footprint. With 30% of its revenues already coming from exports, DPIL is focusing on enhancing its international market share, particularly in regions with growing infrastructure and construction sectors.

Capacity Expansion

With the industry poised for growth due to increased demand in the wiring and cables sector, DPIL has plans to double its current capacity by FY25. This ambitious expansion is set to position DPIL as a leading ancillary player in the market, taking advantage of economies of scale and enhancing its competitive positioning.

Research and Development

DPIL has consistently placed a high value on R&D, investing in new technologies and processes to develop innovative products. This commitment is evident in its transition to more advanced, higher-margin products that have contributed to an EBITDA margin expansion from 6% to 11%.

Sustainability Initiatives

Sustainability is a key component of DPIL’s long-term strategy. The company is investing in sustainable manufacturing practices, including waste reduction, energy efficiency, and resource conservation, to ensure its operations are environmentally responsible and align with global sustainability goals.

Corporate Governance and Management

DPIL emphasizes strong corporate governance and ethical management practices. Following its demerger, the company has reinforced its commitment to transparent operations and adherence to regulatory standards, aiming to build investor confidence and long-term shareholder value.

Future Outlook

DPIL’s outlook is robust, with the company set to benefit from several tailwinds in the industry. The focus on infrastructure development, the rise in the electric vehicles market, and the increasing demand for telecommunication services are expected to drive demand for DPIL’s products. With its strategic initiatives in place, DPIL is well-equipped to capitalize on these opportunities and sustain its growth momentum.

Risks and Challenges

Despite the strong positioning and growth prospects of Ddev Plastiks Industries Ltd., there are inherent risks and challenges that the company faces which could potentially impact its business performance and investment outlook.

Competition and Market Penetration

DPIL operates in a highly competitive industry with both domestic and international players. The company’s ability to maintain and increase its market share is contingent upon its competitive pricing, product innovation, and customer service. Intensified competition could lead to pricing pressures, margin contraction, and loss of market share.

Raw Material Volatility

The company’s profitability is susceptible to fluctuations in the prices of raw materials, such as LDPE/HDPE and PVC resin, which are crude oil derivatives. Volatility in these input costs could affect the company’s gross margins and overall financial performance. The management’s ability to hedge against these price fluctuations is crucial to maintaining stable margins.

Supply Chain Disruptions

DPIL is dependent on the steady supply of raw materials, a significant portion of which is imported. Any disruptions in the global supply chain could lead to production delays or increased costs, which could adversely affect the company’s operations.

Regulatory Compliance and Environmental Risks

As DPIL expands its product range and enters new markets, it must navigate an increasingly complex regulatory landscape. Compliance with environmental, health, and safety regulations across different jurisdictions can lead to additional costs or alter market dynamics.

Corporate Governance

Given the historical corporate governance issues related to the erstwhile parent company Kkalpana Industries, DPIL must continue to demonstrate its commitment to high governance standards to maintain investor confidence.

Technological Disruption

The polymer compounding industry is subject to rapid technological changes. Failure to keep pace with technological advancements could result in obsolescence of current product lines and impact DPIL’s competitive advantage.

Currency Exchange Risk

With a considerable portion of revenue coming from exports, DPIL is exposed to currency exchange risks. Unfavorable currency movements could affect the company’s earnings in its reporting currency.

Geopolitical Risks

Global political tensions and policy changes in key markets can create an unpredictable business environment, affecting trade relations and market access for DPIL’s products.

SWOT Analysis

Strengths

- Market Leadership: DPIL is the largest domestic producer of polymer compounds with a robust manufacturing capacity, enabling economies of scale.

- Diverse Clientele: Relationships with top-tier companies across industries and geographies provide stable revenue streams.

- Innovation and R&D: A strong focus on R&D leads to the development of advanced materials, keeping DPIL at the forefront of industry trends.

- Financial Health: The company demonstrates strong financial metrics with high ROCE and ROE, and low debt, underscoring operational efficiency and fiscal prudence.

- Export Revenues: A significant portion of revenue from exports helps diversify market risks and capitalizes on global demand.

Weaknesses

- High Competitive Intensity: DPIL operates in a market with substantial competition from both domestic and international giants.

- Raw Material Sourcing: Dependence on large suppliers like Reliance Industries and IOCL for 70% of its raw materials could impact bargaining power and cost management.

- Corporate Governance History: Past associations with the Kkalpana Group may necessitate continuous efforts to build and maintain stakeholder trust.

Opportunities

- Industry Growth: Increasing demand in wiring & cabling due to infrastructure and renewable energy projects presents significant growth opportunities.

- New Product Lines: Expansion into high-margin HFFR compounds opens up new market segments and potential for increased profitability.

- Strategic Expansion: Plans to double capacity by FY25 can meet growing demand and increase market share.

Threats

- Input Cost Volatility: Fluctuations in crude oil prices can unpredictably impact raw material costs.

- Regulatory Changes: Stricter environmental regulations could require additional investments and alter market dynamics.

- Global Supply Chain Disruptions: Ongoing geopolitical tensions and trade disputes may lead to supply chain uncertainties affecting production and cost efficiency.

In conclusion, DPIL’s strategic positioning, coupled with its financial and operational strengths, presents it with ample opportunities for growth. However, it must navigate the industry’s competitive landscape and external risks diligently.

Conclusion and Recommendations

Ddev Plastiks Industries Ltd. (DPIL) stands out as a formidable player in the polymer compounding industry, backed by its strong financial performance, strategic market positioning, and commitment to innovation and sustainability. The company’s comprehensive product portfolio, catering to diverse industrial applications, and its focus on high-margin, specialized compounds position it well for continued growth amidst evolving market demands.

Conclusion

DPIL’s robust operational strategies and financial metrics underscore its potential as a compelling investment opportunity. The company’s proactive approach to expanding its product lines and entering new markets, coupled with its strategic initiatives aimed at capacity expansion and technological advancements, bodes well for its future prospects. Furthermore, DPIL’s efforts in maintaining high corporate governance standards and its strong emphasis on R&D and sustainability initiatives reinforce its commitment to long-term value creation.

However, potential investors must consider the inherent risks associated with raw material price volatility, competitive pressures, and regulatory changes. DPIL’s ability to effectively manage these risks will be crucial in sustaining its growth trajectory and market leadership position.

Recommendations

- Investment Consideration: Given DPIL’s strong financial health, growth prospects, and current valuation at a historically low PE ratio, the stock presents a potentially undervalued opportunity for long-term investors. Those seeking exposure to the industrials and materials sector could find DPIL an attractive addition to their portfolios.

- Monitor Market Developments: Investors should closely monitor developments related to global supply chain disruptions, raw material price trends, and regulatory changes affecting the polymer compounding industry, as these factors could impact DPIL’s operational efficiencies and cost structures.

- Corporate Governance: Continued transparency in corporate governance and operational practices will be essential in enhancing investor confidence. Potential investors should seek reassurance on DPIL’s governance mechanisms and ethical business practices.

- Diversification Strategy: Given DPIL’s strategic focus on high-margin products and the expansion of its export markets, investors should consider the company’s diversification strategy as a hedge against domestic market volatility.

In summary, Ddev Plastiks Industries Ltd. presents a balanced profile of robust growth potential tempered by industry-specific challenges. With its strategic initiatives geared towards innovation, sustainability, and market expansion, DPIL is poised to navigate the complexities of the polymer compounding industry successfully. Investors willing to bear the industry risks could potentially reap the benefits of the company’s growth and re-rating prospects.