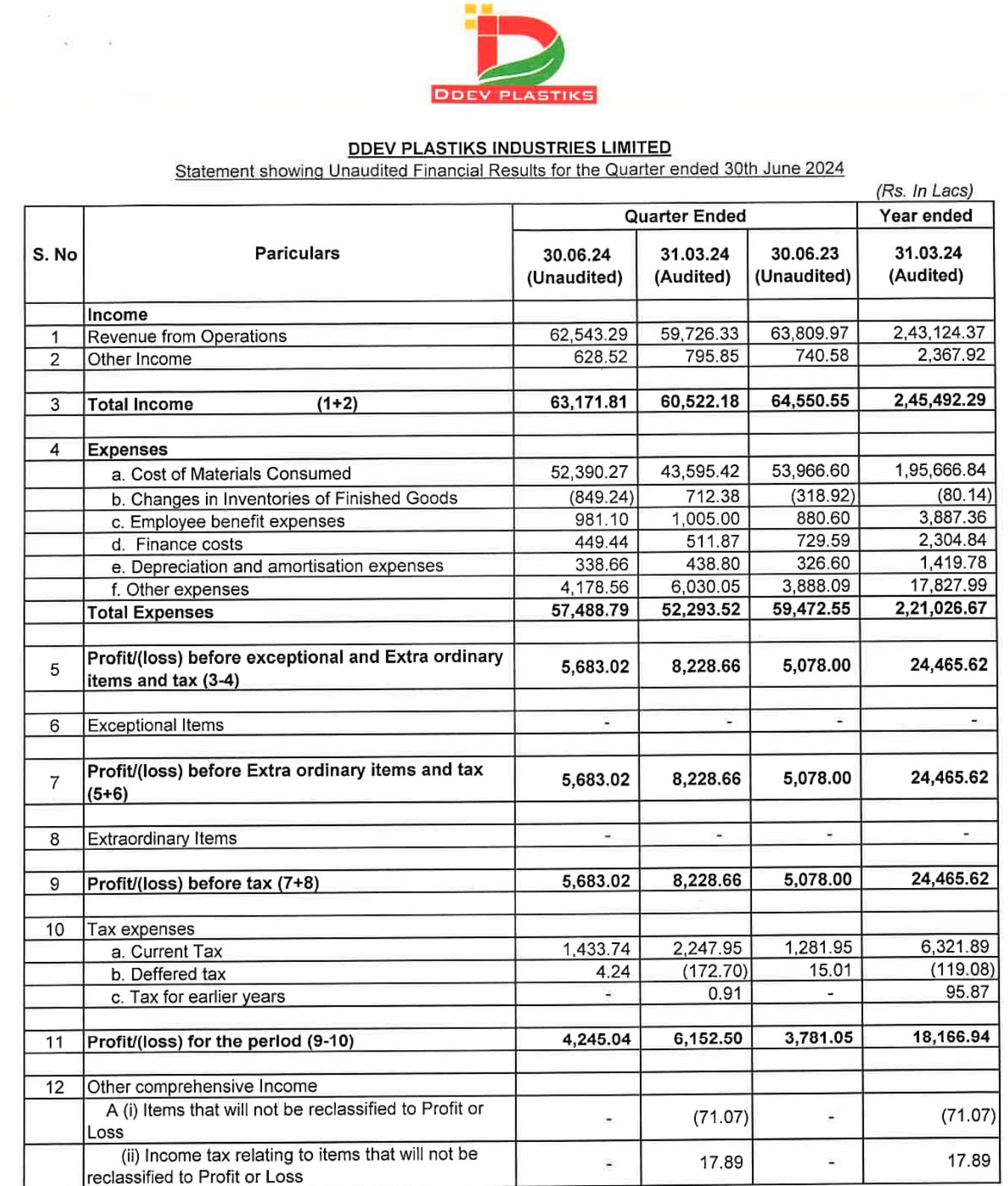

Great set of result.

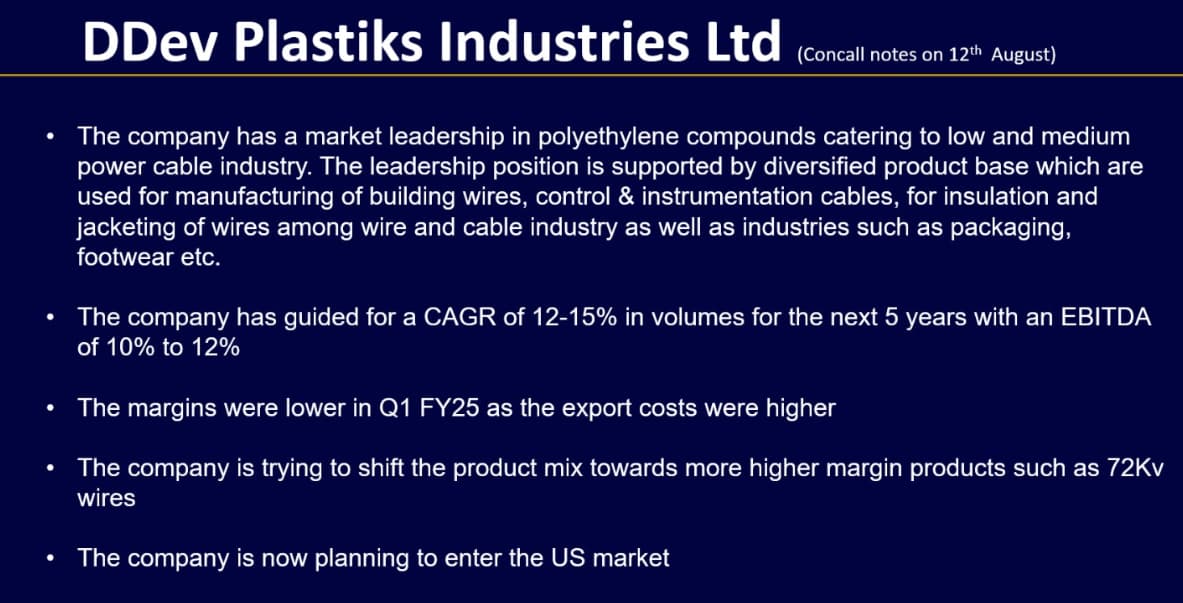

Company did their first concall, got to understand lot on their future plan.

Short brief:

- our industry is more of passing on the raw material cost. That is why if you see the turnover has come down with the reduction in raw material prices. It is straight passed on

- HFFR will be additional product contributor, which will be contributing 10%-15% of revenue over a period of time.

- the profitability improvement in last 2 years has come mainly from the product range improvement or product portfolio improvement because we have moved more towards medium voltage and high voltage insulation compounds + increased share of export

- HFFR, this year we have been able to utilize around 30% of our capacity, which we hope that next year in Financial Year ‘25, we should be able to achieve capacity utilization of almost 60% to 70%

- we are expecting to grow at 12% to 15% CAGR with the EBITDA margin of roughly 10% to 12%

- hffr The other player is Shakun Polymers

- And cable approval is a long-term process. They will make the cable. They will test in their own laboratory, first at compound test, then at cable test, electrical test, and field test. So, all these tests take time. Any approval with any customer generally takes 6 months to 1 year’s time.

- hffr 5000 tons full utilization, we expect a turnover of roughly Rs. 80 to Rs. 85 odd crores in the overall product basket.

- 300 cr capex is for land and building and electrical installation kind of infra which we are creating is going to handle 15,000 tons of HFFR capacity additionally and another 45,000 to 55,000 tons of other products. So, in totality, anything between 60,000 to 70,000 tons of fresh product.

- targeting a 12% to 15% CAGR and a conservative site for next 5 years, turnover will be roughly Rs. 5,000