A good news for the company.

4 Likes

17a316e0-cecc-4755-8d14-4bb579b5aaf6.pdf (4.3 MB)

Very poor results!!!

Wasn’t expecting blockbuster numbers in Q1 - but what’s posted is quite poor and lower than my basic expectations.

I am guessing some execution may have been delayed. Also guessing mgmt will maintain their guidance - which means the remaining 3 quarters can be heavy.

Staying optimistic - waiting for tomorrow’s call.

2 Likes

The management of this company keep their financial data as it is.No window dressing, no inflated sales nothing. Business model of the company is good. I will keep holding my stake in it

1 Like

Now i understood why promoter sold in large quantities prior to june24 result . Make sense.

1 Like

DCX has received contracts/orders for INR 107,08,89,320/- from Domestic and Overseas Customers.

BOOM ![]()

1 Like

This order will not save the sinking ship.In Q4 management said we have very high receivables which will reflect in Q1.

Nothing like that happened and company posted the worst quarter in last five years.Promoter is offloading,He is very smart, Talking smartly and delivering Nil.You ask anything and anwer is "This will be accounted in next quarter."Management has habit of posting about orders whenever they post bad results .

#Holding with lost hope

3 Likes

You shouldn’t hold any company where you don’t have complete confidence.

There are many other opportunities.

2 Likes

Confidence comes from revenue/profit numbers.

Will surely look to exit if bad numbers comes in Q2.

1 Like

Chola_Securities_Initiating_Coverage_on_DCX_Systems_Ltd_with_33%.pdf (1.7 MB)

Good read, will give you some insight into the business & potential.

I fail to understand the intention behind posting this report Dt 26.03.2024. The projected price is already achieved and share price is presently ruling at projected level even after last few days sizable dip. Also since this report, results of 2 qtrs have been published and below market expectations.

Admin should look into this aspect. These kind of reports are very misleading and are generally posted out of ignorance or ill intention. Both the cases are not desirable. Would like to know views of esteemed boarders.

3 Likes

- Purpose of sharing the report was to share information about the company, sector, and prospects.

- You have drawn reference only to the TP

- The report is not misleading and should not be construed as such - and if it is then every single published report across sectors by any research house should be called misleading.

If you have constructive notes, research, or views on DCX - please share them.

2 Likes

20240816072658_DCX-Systems-160824-kr.pdf (497.5 KB)

You can refer this latest report dated 16 Aug 24.

2 Likes

The management has stated during the concalls that the revenues and cash flows are lumpy. The company works on a Cost-plus model with its customers. In electronics manufacturing, there are typically these stages:

- PCB design

- PCB fabrication

- BoM procurement

- PCB Assembly

- PCB qualification/acceptance testing

- Delivery

I am guessing DCX gets the PCB designs from its customers and its role starts from fabrication onwards.

Since these are defence & aerospace PCBs the entire process could take up to 6-7 months to complete, because the PCBs have to undergo many tests during each of the above steps. For eg. there is something called as a burn-In test, where the assembled PCBs are kept in a thermal chamber at an elevated temperature for ~100 hours (will vary from product to product). After every few hours they have to be functionally tested while still in the chamber. Some of these tests happen on the entire lot while some happen only on a small % sample. Then there are also some tests which will happen at the customer’s end.

I am guessing that DCX gets some mobilization advance payment from the customer when the contract is started. This is for component procurement etc. The invoicing likely happens when the customer finishes all the tests at their end after the PCBAs have been delivered to them.

So it might happen that while the work related to a contract happens throughout the year, the billing will only happen in one of the quarters. So instead of tracking the company on the Q-to-Q basis it is better to track it on an annual basis. The primary metric to keep a track of is the order book. As long as they have ~2 years worth of orders that is fine. Order book as of June 30th 2024 is Rs. 1,937 crores, which is 1.36x the FY24 revenue.

Stake sale by the promoter is a very big negative. Especially the manner in which it was done i.e. in-between a fantastic quarter and a very poor quarter in terms of numbers. As a general thumb rule I am skeptical of promoters in small & mid caps. Trust only develops after many many quarters of walking-the-talk. So while I am still invested in DCX (<5% of my portfolio), I will be cautious.

4 Likes

4 Likes

The article makes some startling revelations:

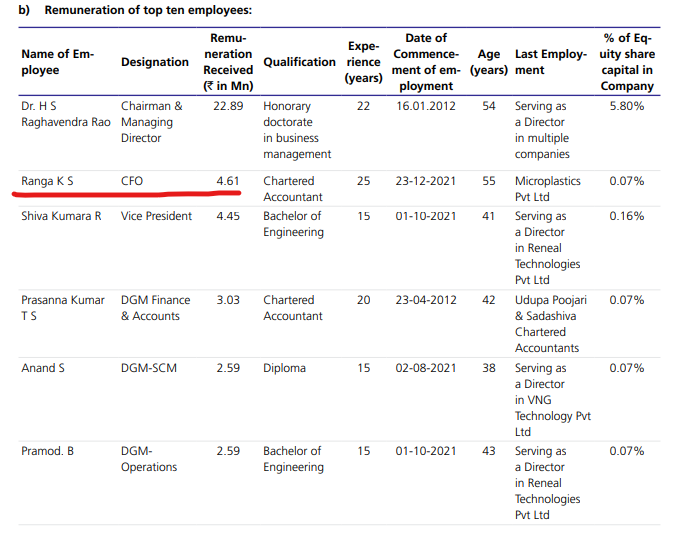

Nearly everyone on the top management team made less than INR 20 lakhs a year at the time of the IPO, which is weird, given these guys’ work experience/qualifications. Perhaps we have a skewed idea of salaries, but you generally wouldn’t expect a CFO of an INR 600 crs + sales company (at the time of IPO) to make INR 12 lakh a year (the CFO is a wizened CA, which makes it even more surprising).

Quite surprising, given the company does not declare any dividends. Why would a top-management caliber person in electronics manufacturing want to work at such low salaries? I cross-checked this with the AR for FY23 and found that some of these findings are incorrect. As the image below indicates the CFO draws a salary of Rs 46 lakhs.

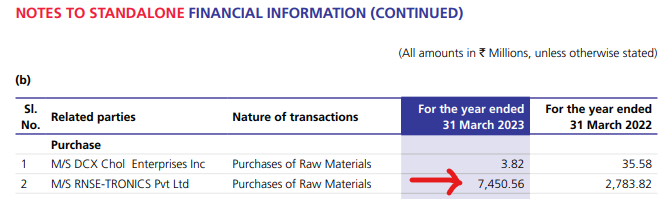

In FY22, around 25% of the raw materials were sourced from the promoter-owned firm, which promptly increased to 50% in FY23. Of INR 1200 crores in raw material costs, INR 700 crores seems to have been supplied by the promoter-owned firm.

This is correct. As per the FY23 AR around Rs 750 crores worth raw material was sourced from a promoter owned company.

This is a big red flag. Need to dig deeper into this. Usually such kind of things are done so that the majority of the “juice” is squeezed by the unlisted promoter owned entity. No wonder DCX has an OPM of only around 6% for FY24.

4 Likes

The first part. I think post IPO salaries have gone up for the top guys quite well, this low salary was pre IPO as per DRHP, maybe there are some technicalities here. You could the check the AR for current salaries.

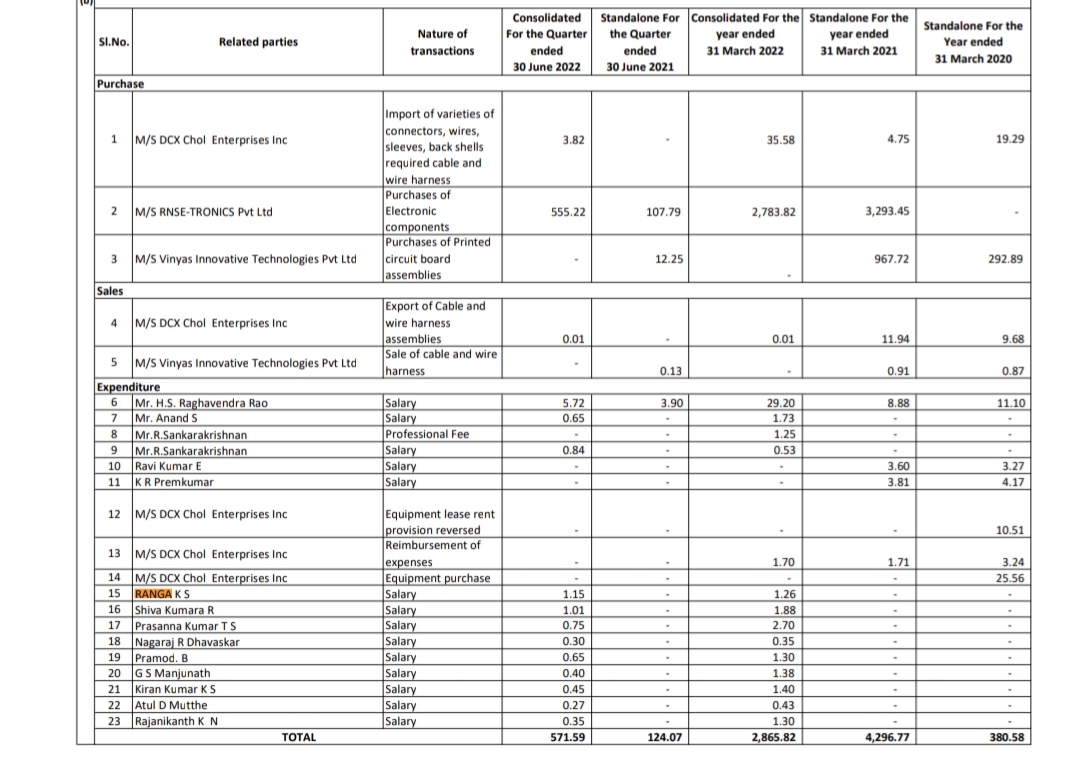

The second part is visible in the FY23 AR and certainly needs to be checked. The co has taken approval for procurement of around Rs 800 cr from 1 entity and utilised around 700+ last year.

I think this was being referred to.

2 Likes

Isn,t the same broker who has earlier (before 4Qr result) recommended 30% upside.Looks total fix.

1 Like

Bulk deals today

NCBG (Promoter group) sells 100cr - 2,959,100qty

Ajay Upadhyay buys 50.69cr - 1,500,000 qty

Price 337.95

Unsure who bought the other 50cr

1 Like

Things are making sense except this -

I’ve studied Ajay Upadhyay’s history, portfolio size, past company choices, failures & success in markets - he isn’t a punter, trader, or your average Joe. He’s extremely prudent and I’d like to think that he knows very well what he’s doing.

Usha martin, Elecon, Genus, Time Technoplast, Skipper Ltd, Dollar, Precam, all super solid companies, and also a master of turnarounds in WIL, Vascon, etc.

I’d like to think that it is very unlike him to continue to invest in a company that may seem to have CG issues (OMAXE feels like an outlier to me, at least for now).

So obviously, he is comfortable with the promoter sale which took place earlier and the one today.

As he holds more than 1% and I think after today’s deal maybe near or slightly more than 2%, the questions in my mind are:

-

Being such a large shareholder, would he have to be informed by the CS (or owner) of the reason for the promoter group sale? The fact that he bought half of it, maybe yes…?

-

The company seems primed and the runway can be huge - if this is so (that’s why he’s buying?) - what could potential reasons be for promoter to offload? Just some cash generation?

-

If if was just cash generation - then why are they selling on the first uptick post good news, where price is just reversing and surely by end of the week / month it could possibly be much higher. They sold today at 20 less than their previous sale. Surely, they are not living off the street in need of immediate cash.

There seems to be more to this and one cannot truly understand by just looking at this sale information in a single dimension.

Would love to hear thoughts & ideas around this.

Invested & holding a healthy position.

6 Likes