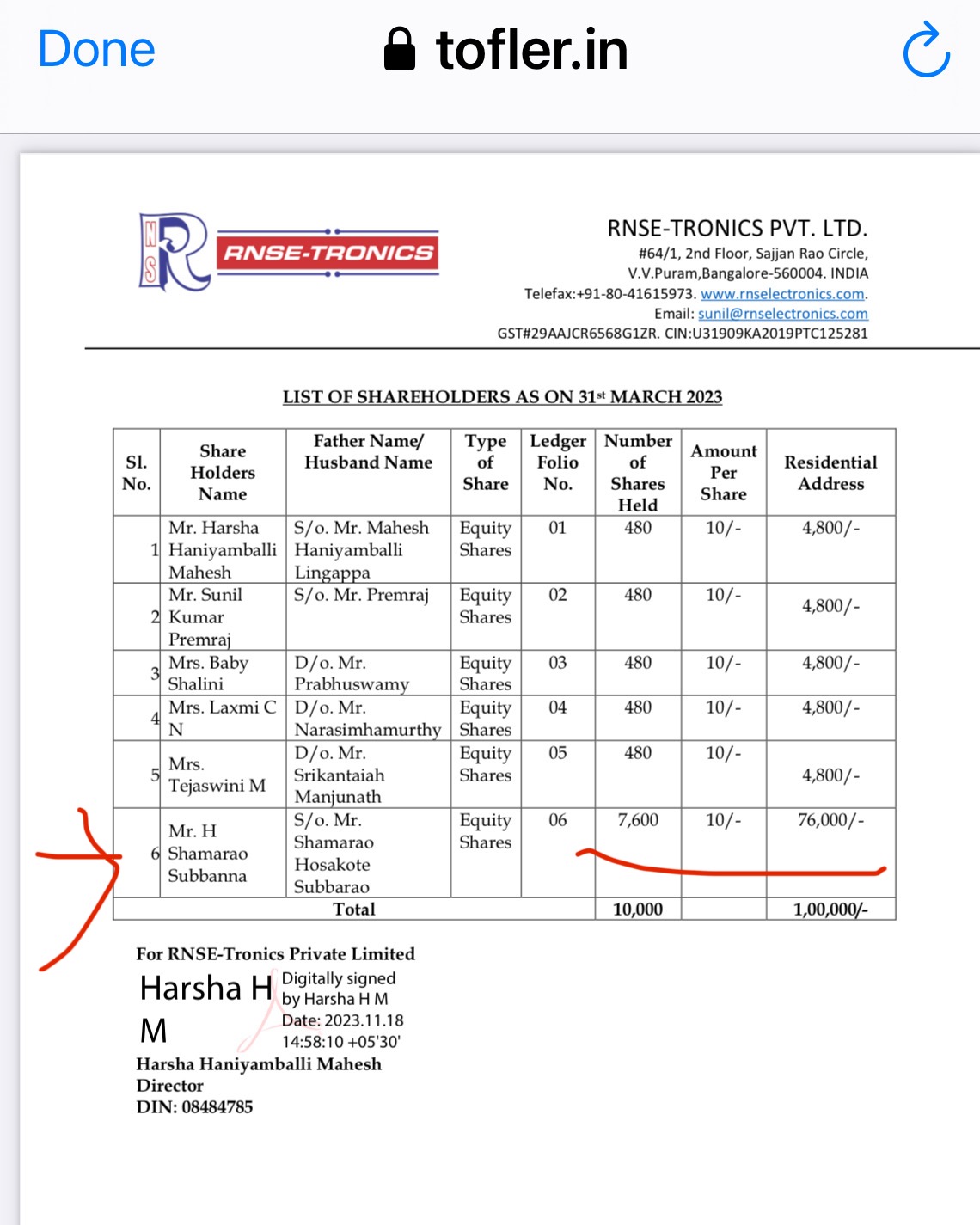

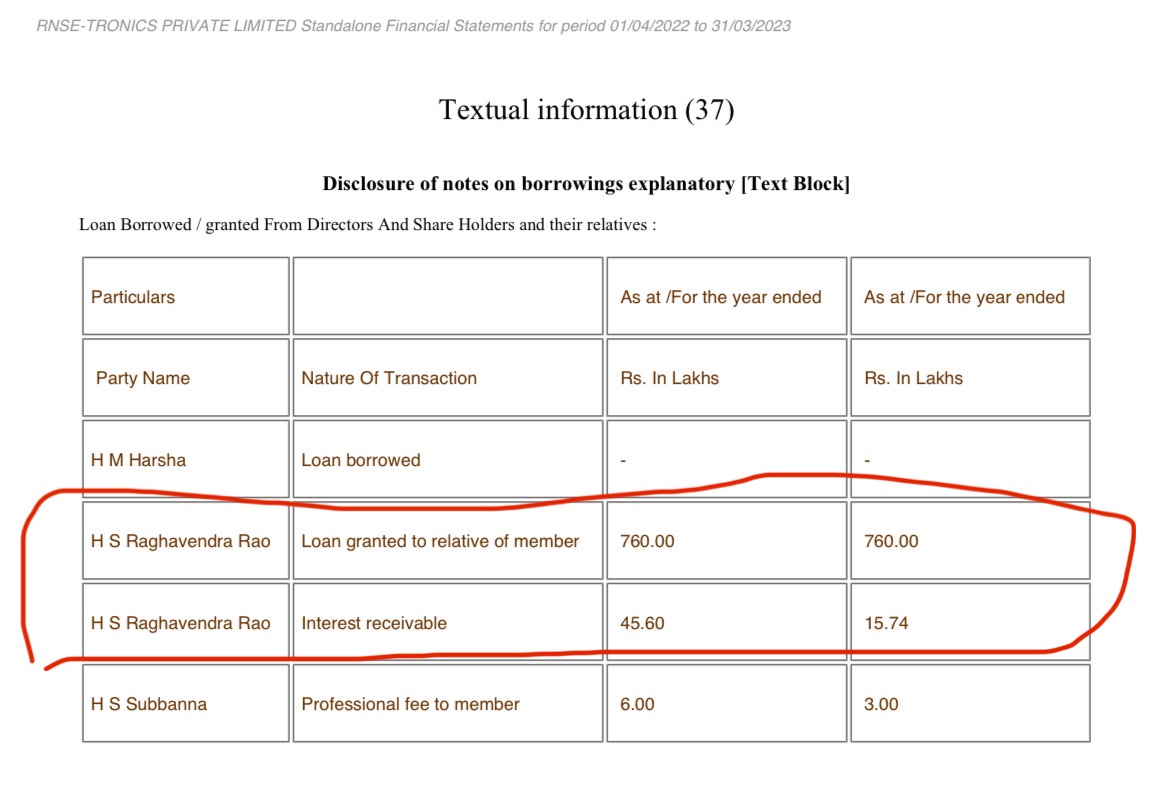

So I downloaded the financials of RNSE-Tronics Pvt Ltd from MCA via Tofler. This is the same promoter owned company which supplied components to DCX. Here are my findings.

76% of the shares of this company are owned by the MD.

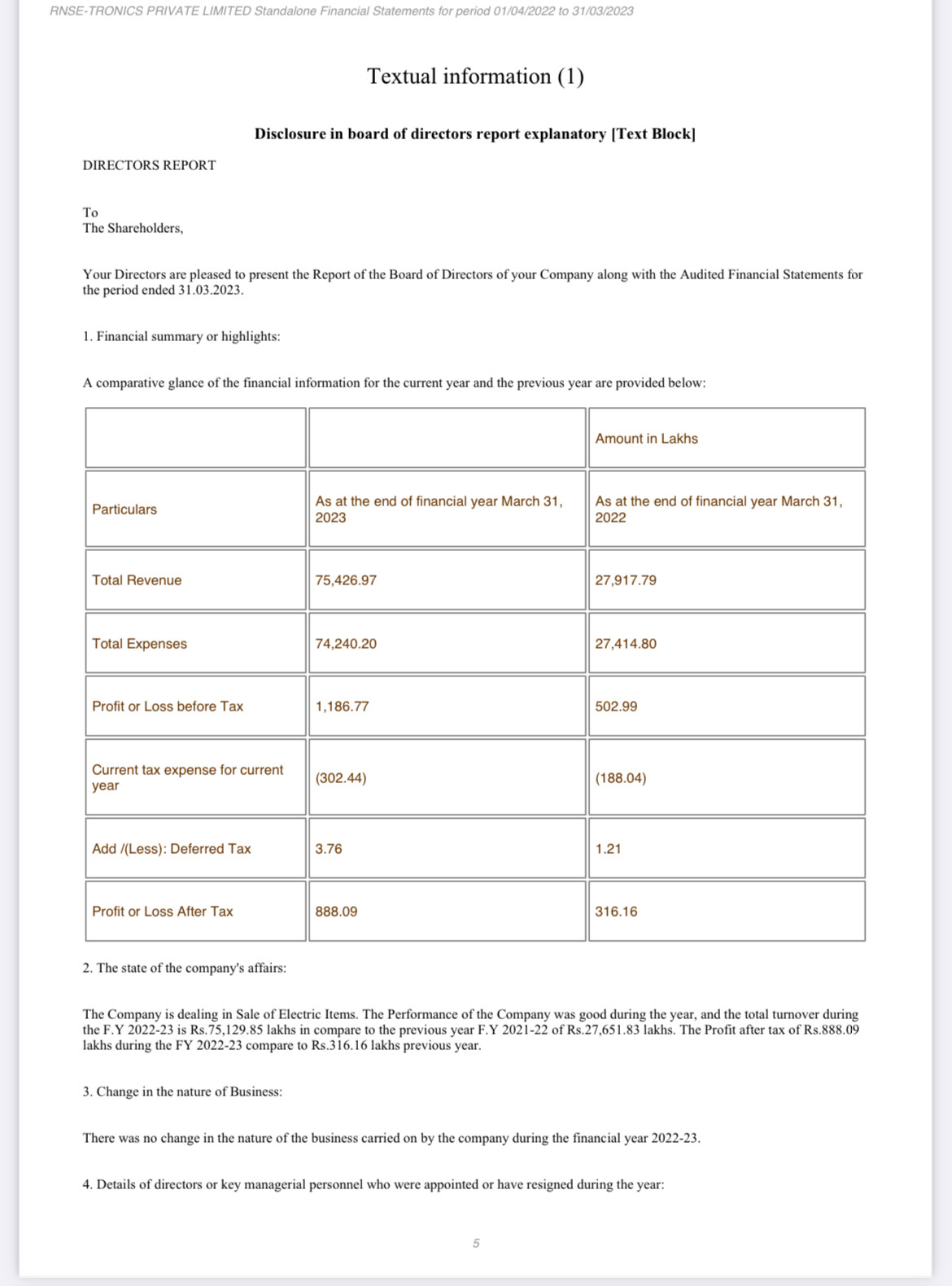

Low profit margins are not the issue here. Its more about the nearly 13% more profit (even more when buying economies of scale etc are considered) , that the minority shareholders didn’t potentially earn.

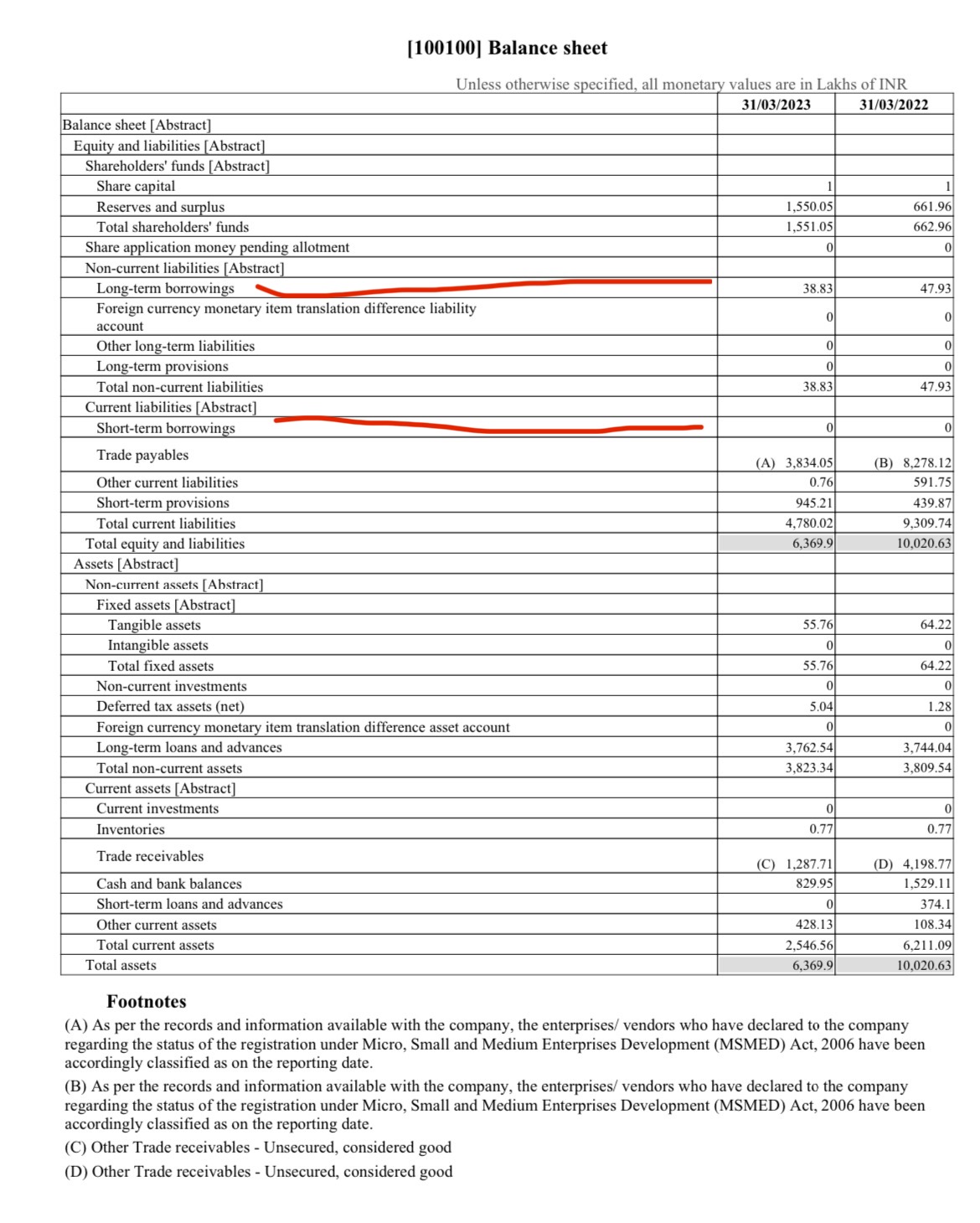

The company’s trade receivables would be a better indicator of DCX’s payment timeliness - which appears to quite good in FY23. It also seems to be a trading co since it has just INR 55 lacs in fixed assets - so im not sure if it is adding any value here.

Unless an independent supplier offers worse terms or price, I would be sceptical.

Good reasoning. However, it’s important to keep an eye on their operating margins in the upcoming quarters, as well as their ability to secure the Bill of Materials guarantee payments from clients.

Bit disappointed with the interviewers. They did not ask any questions related to promoter stake sale. Nor did the MD bring it up. Markets are not going to rerate the script if the promoters themselves are selling.

Do not expect any further upside basis management commentary. We’ve heard enough from them and their words on future prospects / potential is well priced in already.

Market will rerate only basis marque order inflow and order execution.

DCX Systems Limited has received an industrial license for its subsidiary, M/s Raneal Advanced Systems Private Limited, to manufacture microwave submodules, avionics, defense electronic equipment, radar systems, and EW systems. The license will be valid for 15 years and falls under the highest level of security. No withdrawal or cancellation of the license has been reported.

And

DCX Systems secures an export order from Elta Systems in Israel for RF electronic modules valued at ₹154.80 crore.

We wish to inform that our Wholly Owned Subsidiary M/s. Raneal Advanced Systems Private Limited has received export orders from M/s. Lockheed Martin Global Inc, USA for US$ 45,199,440.00 (Equivalent to about INR 379.67 Crores at exchange rate of 1 USD = INR 84).

DCX Systems Limited has received export orders from M/s. Lockheed Martin Global Inc, USA for US$ 54,798,120.00 (Equivalent to about INR 460.30 Crores at exchange rate of 1 USD = INR 84) for supply of Electronic Assemblies. The order is to be executed within 12 months.

What’s the moat in this business ? Or its just assembly work

Will they manufacture PCB ? When they say going into backward integration. I don’t think they manufacture PCB here.

NIART :

DCX Entered into JV with ELTA subsidiary of IAI.

Why to give technology transfer to DCX ?

Based on my reading on DCX -

DCX does system integration work, they are into assemblies when they talk about Backward Integration, I don’t think they do manufacturing. They are just into assembly work. ( Not manufacturing)

We can simply compare with Vinyas.

JV wrt Railways need to be seen. - Scale up needs to be seen.

Defence orders from Largest Defence Company.( System Integration Work) - Is this an offset business that Lockheed Martin needs to fulfill that’s why the orders are flowing to them or they cracked the clientele. Which is hard to believe.

Dcx is not looking like a company which has to ability to convert these high profile orders into growth. I might be wrong with this assumption but when I tried comparing it to similar competitors and its own past performance. I see divergence from the growth path.

Here is a short conclusion of various factors as to why it might not be looking like a decent bet. The company might do well of course but i guess there are better places to deploy the cash.

Lockheed Martin POs = major account and just beginning.

NIART System approved by Indian ministry

Raneal up & running

Rebranding - shows a positioning statement

Negatives

Delay in previous BOM related recoveries

Margin expansion pending

Order book needs to grow

Thoughts

Lack of clarity due to the nature of the business (lumpiness), nature of promoter (prefers to not give clear guidance), nature of the industry (NDAs & confidentiality)

Long cycle due to approvals etc but once the account opens, it can do well - Lockheed from a trial of 15cr to two PO’s of approx 900cr in total

Delay in railway related safety spending by GOI - hence kavaach too delayed. NIART is approved, opportunity is very large, orders need to be given

Q3&Q4 will be an improvement. How heavy of an improvement, remains to be seen

If this FY doesn’t end remarkably better than last FY - then investors may loose patience and the wait may be a tad longer

Is uniquely setup and now needs to explode - but, needs three things to sing in this FY

1- diversified order inflow

2- recoveries of past BOM + some margin expansion

3- execution that reflects in numbers