- It means tensions in Israel did affect it business.In last concall they were asked this question and they replied we wont have any affect. Sad to see management not being clear about the business condition. 2. They didn’t gave an update on order book with results they usually use to give it… Their order has been de-growing since IPO

Investor presentation is up.

https://dcxindia.com/wp-content/uploads/2024/02/Investors-Presentation-Q3-FY-2023-24.pdf

DCX announces two new orders totalling to approx 475cr

-

Company has received a contract/order for export

orders from overseas customers valued at approximately US$ 55,130,093.33 (which is equivalent to INR

457,57,97,746.80 at exchange rate of 1 USD = INR 83). -

Company has received a contract/order for

US$ 1,991,600.00 (which is equivalent to INR 16,53,02,800.00 at exchange rate of 1 USD = INR 83) from

M/s. Lockheed Martin Corporation, USA.

6 Likes

Sadly there is no mention of why results are soft in Q3 FY 24…No slide giving qualitative details about the most important quarter i.e. last quarter.

As an investor, we need to check if management hinted at short term softness in last concall or atleast tempered down expectations. If so, I am ok with current quarter. If not, it would be red flag in my books.

Discl - invested recently but need to listen to concall to understand management intent

They didn’t mentioned any softness in the demand in their last concall. And the things is other electronics companies are giving good result. This result should be company specific. Let’s see what they say in concall. At least finally they got orders since the IPO.

It was a good con-call. Except the intermittent loss of sound.

Management is clear

- Do not judge DCX on quarterly results.

- 500cr raised, of which, 209cr goes to the JV against 60.1% ownership

- ELTA fund infusion into the JV is nil as they have spent millions in the tech and are bringing that to the table

- The product is unique and the only tech available that can detect 1km+ range to see what is on the track (obstacle, animals)

- India is a big market for this tech, considering railway tech budgets / expansions, but the product is valid globally and DCX will manufacture all the orders for the product

- The product is not a sub-system. It is fully ready to use. Comes with under railway safety as well.

- Revenue will come in end FY24 starting FY25

- The tech is different to Kavaach

- This is a standalone system with complete visibility to the driver

- Present order book Rs 1569 CR

- Of which major is exports.

- Subsidiary - invested 25-30cr in state of the art machinery. Have global approval. Also have internal consumption for the same.

- High end engineering & aerospace focus only.

- Lockheed is a major player and this is our first order. We are now in their system and will pop up as a vendor for all branches.

*could not catch parts of the call due to poor connectivity and unclear voice from the speakers.

Management is bullish. Refuse to give any number guidance. Plead to shareholders to remain patient and look at the history, we will not disappoint you, we want to grow and are very clear on the approach.

Feel like price may have seen a near-term bottom. I have added more quantity today during the call.

Let’s wait for more order updates & execution flow.

Dream on

7 Likes

Since company preponed the concall, I missed on attending it. So I am curious to know whether management mentioned exact reasons of why sales were lower this quarter (YoY as well as QoQ). Also “Don’t look at quarterly numbers” tune should have been played during good quarter (which was last quarter), not during bad one like now. Sorry for being skeptical here but I have seen many companies playing this game. Good numbers are always due to them and bad numbers are due to “n” numbers of reasons beyond their control. Also timing of declaration of receipt of new orders is highly suspicious.

All in all, I am hopeful that my doubts are unfounded. But it is better to be safe than sorry, since it our own money. Would like to wait for few more quarters before allocating more capital to this company.

5 Likes

dcx system research.pdf (1.3 MB)

complete research report by KR choksey

2 Likes

Latest concall . Every thing answered by them

1 Like

Have substantially increased my allocation between yesterday & today.

*The product is not similar to Kavaach. They are not competitive products. *

3 Likes

Got some queries on how this is different from Kavach.

Kavach is an anti-collision system for 2 trains running on the same Track.

DCX’s system is a driver alert system to detect any object in front of the track for a range of about 1.5KM, in all-weather conditions.

The end user may need both systems.

Globally, there is no other system like the one DCX will offer. The opportunity is tremendous, in my opinion.

Management has to deliver in Q4 and Q1FY25. If they execute the way they’re talking, then we are looking at an absolute gem in the making.

2 Likes

Please find below my detailed company analysis -:

DCX Systems Ltd

=======Sector: Electronics - Components

About the company:

DCX Systems Limited specializes in providing comprehensive solutions for high-end system integration, cable and wire harnesses, electronic subsystems, and PCB assembly, primarily for the Defence and Aerospace industry. Established in 2011 , and went public in 2022

-

It stands as a major Indian Offset Partner (IOP) to the Israeli Defence Company, IAI, and is expanding its reach in various geographies for both IOP and non-IOP projects.

-

Its core strength lies in the solutions of electronics manufacturing with a focus on backward integration in PCBAs, facilitated by its wholly-owned subsidiary, Raneal Advanced Systems, incorporated in 2022 catering to both internal consumption and external markets.

-

DCX has been also focusing beyond Defence and Aerospace segment to fortify the resilience of future growth and with this objective the company has incorporated NIART Systems Limited –JV between DCX & ELTA Systems, formed in 2023, for obstacle detection solutions in Railways

-

DCX Systems has been expanding from a defence focused system integration company to a product manufacturing company with increased focus in Make in India through its JVs using ToT(Transfer of Technology)( especially from Israel, US) in medical, railway, and other civilian sectors with more focus on margin accretive non-offset projects .

Govt. identified list of indigenous products (cannot be imported, must be manufactured in India) – DCX aims to get ToT for such products & supply to MoD(ministry of defense) and export market

** IOP - requirement imposed by the Indian government on foreign defense contractors to fulfill offset obligations when winning contracts in India. When a foreign defense company secures a contract with the Indian government, it is typically mandated to invest a certain percentage of the contract value back into India. This investment can take the form of technology transfer, establishing manufacturing facilities, or partnering with Indian companies.

- State of the art manufacturing facility covers an expansive area of 30,000 sq. ft situated in SEZ in Bengaluru, commissioned in 2020.

o Also, a newly established facility spanning 40,000 sq. ft. in Bengaluru is exclusively dedicated to the manufacturing of EMS has commenced operations from Sept’23.

2024 updates:

-

Raised Rs. 500 crores in the month of Jan - 2024 by way of QIP comprising of Institutional investors like MF, FII, and IC.

o 250 crores was to invest in Subsidiary – NIART Systems Limited

o 200 crore for JV focusing on Make in India -

DCX has latest order book of INR 1570 crore (approximately) as mentioned in the earnings call.

Strength and Investment Rationale

1. Expansion in EMS with Raneal Advanced Systems:

- Current operating Margin of DCX is 6-7% and focuses largely on system integration, is strategically expanding into commercial electronic manufacturing services.

- This expansion includes a focus on Printed Circuit Board (PCB) assemblies and complex box builds, among other aspects

- This set-up of Raneal will enable the company to augment its EMS business, contributing 12% to the top line with enhanced profitability in the near term.

- The focus for Raneal would be to deliver higher value products since these are very much complex PCBAs.

- Raneal Advanced Systems has done 40 crores in captive consumption, aiming for 200 crores by March 2024

- Raneal is geared up for large orders with two SMT lines and focus on high-end engineering

-----Capacity is sufficient to handle high-value orders in aerospace and defense sector. - Consequently, this will not only allow the company to capture a larger wallet share from customers, thereby growing the top line, but it will also enhance the company’s profitability due to the high-value nature of these products.

-----The company’s EBITDA margin is also expected to increase as it intensifies its focus on EMS.

2. Expanding into monopoly product and high-growth sectors such as Railway through NIART Systems

-

DCX has entered into a joint venture with a foreign company, ELTA Systems, leading to the formation of NIART Systems Limited.

-

DCX holds a majority ownership stake of 50.1% in this venture.

-

NIART’s primary focus is the development of advanced technology solutions for railway tracks obstacle detection mechanisms , which would significantly reducing the risk of accidents.

-

While most trains currently have obstacle detection mechanisms with a range of 600-700 meters, DCX’s joint venture with ELTA will enable the manufacturing of obstacle detection systems with a range of up to 1.5 kilometers

-

NIART JV commercial production expected to start in FY25

-

In India, the railway sector, with its 34000 crore budget and over 14,000 locomotives in operation, exhibits a high demand for such advanced systems. DCX is also in talks with USA ,Europe for usage of this product. It has no competitor for this product currently

-

DCX Systems is also poised to benefit from the PCBA requirements of NIART Systems through Raneal Advanced Systems. It intends to leverage its capabilities in cable and wire harnessing to meet the demands of NIART Systems.

3. Increase Profit through Backward Integration of PCBA:

- In the electronics sector, the primary raw material required for module construction is the Printed Circuit Board (PCB), constitutes approximately 80% of the total cost of the module.

Given that PCBs are a significant cost factor in module production, the company has decided to integrate PCB assembly (PCBA) processes backward.

-

With the incorporation of Raneal Advanced Systems, DCX is now positioned to fulfill 30%-40% of its PCBA needs internally with Raneal, while outsourcing the remaining approximately 70%.

-

Backward integration through Raneal Advanced Systems grants the company enhanced control over its supply chain, manufacturing processes, and resource management, which were previously managed through outsourcing.

-

Such integration is anticipated to result in an improved top line and profit margins as it reduces the raw material cost.

4. Geographic Expansion and Order from Lockheed Martin:

-

DCX is strategically positioning itself to capitalize on the recent changes in Indian defence policies and leverage its capabilities to expand its international presence in the A&D sector.

-

The company is shifting its focus beyond its existing market in Israel, targeting the United States, Korea, and other global economies, with a particular interest in the USA for its margin-enhancing opportunities.

-

Received 2 million order from Lockheed Martin for electronic assembly and expects further orders due to Make in India from Lockheed

-

Received 457 crores export order for electronics modules from new confidential geography.

5. Expansion into new sectors

- DCX has largely focused on the aerospace and defence segment but given its strong presence in the value chain of the electronic solutions it is focusing beyond aerospace and defence and entering into areas such Medical, Railway and other sector.

- The new facility of Raneal has also received approval from most of the prominent OEMs from D&A as well as Medical sector and the recent incorporation of NIART Systems Limited is also formed to serve the railway sector.

DCX is strategically positioning itself to expand into non-defence & aero-space segment in a calibrated manner. In the coming years, the management has also highlighted that, it is targeting the non-defence and aerospace segment to grow to 40%-50% range.

6. Improved structure on IOP (Indian Offset Partner) & Non-IOP:

- The company had nearly 90%+ revenue coming from IAI (Israel Aerospace Industry) few years ago and it has reduced the exposure to 55% in FY22 itself.

In FY22 and FY23 the company has added many more customers in domestic market which is helping the company to reduce its reliance from offset business to non-offset business to further strengthen the portfolio structure.

-

In the system integration segment, it targets to grow the non-offset segment from 15% to 40% over the years to mitigate the risk from high dependence on offset projects and drive better margin.

-

While the company is focusing on Non-IOP segment for further resilience of its portfolio but there is a big opportunity of $13.5 billion from the IOP category which is to be executed in seven years.

-----DCX systems is well positioned to capitalize on this IOP contracts given its long-standing presence in IOP category. -

Out of $13.5 billion nearly $4 -$5 billion would be electronic requirement and DCX is well situated and capable to capitalize on this opportunity

7. Joint Venture in Defence- Make in India

India govt has been focusing on localization by introducing positive indigenization list and there has been an increasing shift of contracts from offset to make in India.

-

Foreign OEM has to be manufacturing minimum 60% of Indian content indigenous content.

-

DCX has the opportunity to tie up with global OEMs for defence radar and missile systems leveraging its system integration, PCBA and cable & wire harnessing capabilities.

-

It can also explore the opportunity to tie up with DPSUs for supplying

-------Take the business more towards manufacturing rather than only focusing on system integration which has higher margins

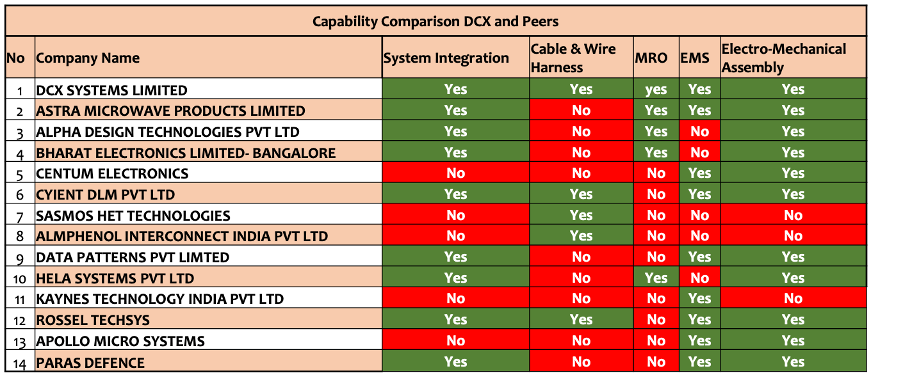

8. Competitive Superiority:

The fiscal policy taken by the government to push indigenous production within India has been instrumental for MSMEs to generate robust business.

The companies with significant experience in this are also offset fulfilment partners to foreign players.

- companies which are full system manufacturers are likely to gain more projects going ahead because many clients prefer company which can cater to all their needs.

9. Advanced Aerospace Manufacturing Facility& Strategic Location

- The company’s 70,000 square feet manufacturing facility in Bengaluru, Karnataka, strategically located in the Hi-Tech Defence and Aerospace Park SEZ, offers several advantages.

----The facility enjoys digital security and restricted access control, safeguarding operations. Being in SEZ grants duty-free imports, GST exemption, and zero-rated supplies.

----Advanced machinery and equipment and in-house testing capabilities meet industry standards.

The location of the facility is in the same city as certain of DCX’s key domestic customers like Bharat Electronics Limited, Alpha Design Technologies Pvt. Ltd., Alpha Elsec Defence and Aerospace Systems Pvt. Ltd. and Centum Adeno India Pvt. Ltd., which ensures shorter delivery time.

10. Transfer of Technology & Opportunity in Cables & Wire Harness

-

DCX has been focusing on expanding the revenue contribution from cable & wire harness segment.

-

Reserved 200 crore to ToT and JV.

-

In 2019, DRDO marked a significant milestone by signing 30 agreements with 16 Indian companies at the Vibrant Goa Global Expo. This is expected to substantially strengthen India’s domestic manufacturing capabilities.

-

Government’s introduction of 10 Production-Linked Incentive (PLI) Programs in 2020 ,aiming to attract new investments in both consumption and export-heavy sectors.

In 2019, India and the US signed a defence technology transfer agreement, and the Industrial Security Annex (ISA) has facilitated collaborative efforts between Indian and US private companies in developing defence technologies. The Defence Technology and Trade Initiative further strengthens this partnership with three additional agreements aimed at co-developing critical technologies.

UK has also emerged as a key technology transfer partner since 2017, with agreements focusing on the co-production of military platforms and weapon systems.

This collaboration is strategically aimed at positioning both countries more strongly in the global arms exports market. For DCX, these developments open up vast opportunities.

Result Highlights for Q3FY24:

- EBITDA Margin and PAT margin for the nine months stood at 11.13% and 6.32% respectively in 9MFY24 in comparison to 7.76% and 4.11% respectively in 9MFY23.

- Current EBITDA 9MFY24 is 70.63 , with Q3FY24 21.28.

- EBITDA had increased significantly to Rs. 83.67 Crores in FY23 (FY22: Rs.66.99 Crores) and on the margin front it has improved to 6.67% in FY23 (FY22: 6.08%).

- Revenue from Operations Q3FY24 is 197.98 cr, Q2FY24 : 355.95 cr

-----Company’s operating income improved by ~14.13% to Rs.1253.63 Crores in FY23 from Rs.1102.27 Crores in FY22.

-----Current Operating Income 9MFY24: 677.20 crore , compared to 9MFY23: 743.08 crore

Key Concal Highlights:

Raised 500 crores through QIP in January 2024

- Investing 209 crores in NIART JV- railway obstacle reduction system. Trials succesfull and prototype shared with Indian Railways and prototype was satisfactory

—Investing 200 crores in JV and technology transfer for Make in India program

—Balance 77 crore – general corpus fund - Majority of orders are in aerospace and defense sector

- NIART JV for railway has a total investment of 25 million dollar

- DCX will supply to NIART’s PCB requirement too

- Raneal Advanced Systems has seen an investment of 30 crores

- Company is looking to acquire technology for Make in India subsidiary with a budget of 200-250 crores

New Products and Ventures:

- Joint venture with IAI ELTA systems and DCX called NIART Systems Limited for railway security

---- Not part of Kavach technology

-----No competitor in world - Received 16.5 crore order from Lockheed Martin for electronic assembly, expecting more to come

- Lockheed need Indian supplier because of the 60% Indian content they have to offset

- Received 457 crores export order for electronics modules from new customer , new geography

- Raneal Advanced Systems contributing to internal consumption, expected to start commercial production soon – 70-80 % internal, 30-20 % direct orders.

---- Plant Approved for medical , aerospace and defense companies - JV with ELTA for NIART Systems involves no additional investment, technology worth $50 million

- DCX aiming to transition from system integration to product manufacturing company

Financial Performance:

- Revenue for Q3 FY24 was Rs. 197.98 crores with EBIT of Rs. 21.28 crores

- Revenue for 9 months FY24 was Rs. 677.2 crores with EBIT of Rs. 70.63 crores

- PAT for 9 months FY24 was Rs. 42.16 crores

- Outlook on order book is positive with confirmed orders of 1,569 crores

- 20% contributed by Indian PSUs in last 6 months

- Order book as of December 2023 was 1,095 crores- all from aerospace and defence(80% export – offset/non-offset), with additional 474 crores from Lockheed order

— Cable -5%

— Electronic assembly – 25-30%

— System Integration -60%

— EMS -10-15% - Company is confident on total revenue going up by end of year and mentioned not to get caught up in quarter comparison

Market Expansion:

- Expanding marketing base to India, Israel, US, and European countries

- Aerospace and defense opportunities are significant due to Make in India initiative

Operational Updates:

- Expecting production and revenue to start in next year for NIART railway JV

- Raneal Advanced Systems has done 40 crores in captive consumption, aiming for 200 crores by March 2024

- Raneal is geared up for large orders with two SMT lines and focus on high-end engineering which can cater upto 2000 crore business

- Capacity is sufficient to handle high-value orders in aerospace and defense sector

Use of Funds:

- Cash and cash equivalents used for fixed deposits against bank guarantees issued to customers, with a portion available for general corporate use

----Funds will be used for technology acquisitions and working capital

---- Company is scouting for new technology for acquisitions - Margins are expected to improve with Raneal’s operations

— 80% cost of product is PCB so will improve margins in coming year - Company is confident in achieving profitability in FY24

- Planning to close term loans of 20-25 cr for Raenel using internal money -cant use IPO money for same

Product/Sales Mix – YoY comparison

System Integration

• 85.3% of FY22 revenue

• 95% of FY23 revenue

• 60 % of December orderbook – FY24-FY25

Cable and Wire Harness

• 2.7% of FY22 revenue

• 1% of FY23 revenue

• 5 % of December orderbook – FY24-FY25

Knitting and Electronic assembly

• 12% of FY22 revenue

• 4% of FY23 revenue

• 25 % of December orderbook – FY24-FY25

EMS

• FY22 and FY23 not applicable

• 15 % of December orderbook – FY24-FY25

Fundamentals

• Net profit increasing except in FY24Q3 , Q4 quarter expected to be higher in range of 30-40

• Company has been able to be grow the reserves - +ve

• Zero Long term Debt, Short Term debt is 409 – which is Working capital

–Inventory + Trade receivable -75+214 = 116 crore

• Cash Equivalent is fallen between March 2022- March 2023 – new manufacturing establishment of EMS used 8.5 crore and rest as term loans

• FII,DIIs increased , promoters raised 500 crore through QIP

Industry Growth

Leadership

Mr. Raghavendra Rao and Mr. Neal Jeremy both have an experience of over three decades into the industry. Further, Company has an operational track record of more than a decade and has achieved significant growth in the last 4-5 years.

Longstanding presence of the directors in the industry has helped the company to establish strong relationships with customers and suppliers and diversify the product profile.

Risk

1. Exposure to Regulatory Risk Defence is a highly regulated industry

Any changes in Offset Programme by Ministry of Defence, India might impact on the order inflow though it is unlikely to happen soon considering India’s dependency on foreign OEMs for defence sector related requirements.

With the increase in Defence requirement and the huge Backlog of Off-set obligations from the overseas Defence OEM’s, the revenues will continue to surge for the years to come.

DCX Systems Limited must closely monitor policy changes, engage in effective advocacy, and proactively adapt its business strategies to mitigate potential risks associated with policy uncertainties.

2. Intense Competition: DCX Systems Limited faces the threat of competition from both established companies and emerging start-ups offering similar services. To maintain its competitive position, the company must continually innovate, differentiate its offerings, and provide exceptional value to its clients

3. Raw Material Price Volatility: DCX Systems Limited is vulnerable to fluctuations in raw material prices, which can impact its profitability and cost structure. Sudden price increases or supply shortages can strain Annual Report 2022-23 45 the company’s margins and affect its ability to deliver products at competitive prices. Effective supply chain management and proactive hedging strategies are necessary to mitigate this threat.

Company has agreements with a majority of our customers, pursuant to which pass on any fluctuation or increase in cost of raw materials to their customers

4. Availability of raw materials: Shortage in supply of raw materials may result in an increase in the price of the products. An increase in raw material prices could result in a reduction of our profit margins.

5. Uncertainty in Tendering Processes: The tendering processes in the defence and aerospace sectors can be complex and uncertain. DCX Systems Limited may face challenges in winning contracts due to factors such as intense competition, changing customer requirements, or delays in the tendering process.

The company needs to closely monitor market dynamics, develop strong relationships with customers, and adapt its strategies to navigate this potential threat.

6. Credit Risk

Credit risk on accounts receivable is managed through credit approvals, establishing credit limits and continuously monitoring the creditworthiness of customers to which the Company grants credit terms in the normal course of business.

7. Liquidity Risk

- Any further significant rise in working capital intensity or unplanned capex leading to deterioration in the liquidity position.

- Any dip in operating income and/or profitability thereby impacting the debt coverage indicators and/or any deterioration in the financial risk profile.

8. Market Risk

foreign exchange rates and interest rates, will affect Company’s income or the value of its holdings of financial instruments

- Foreign Currency Risk

- Interest Rate Risk

9. Export Shipping Cost/Risk

- Increase in export shipping cost .

- Utilizing road, sea, and air transport, the company is vulnerable to disruptions from natural events like weather extremes or man-made issues such as strikes and accidents. Additionally, the loss of third-party transportation providers, coupled with their potentially inadequate insurance coverage, poses a risk. Such challenges in transportation could lead to financial and operational setbacks for DCX Systems.

My outlook for DCX Sytems

- Budget may focus on Defense – and open up further opportunities.

- With its capabilities in system integration, the recent addition of a PCBA facility, and expertise in cable and wire harnessing, DCX Systems is well-positioned to benefit from push for indigenized manufacturing.

----Captive consumption will also have an increase in margins in coming year - Company is strengthening in system integration through backward integration and the commercial use of its PCBA facility.- Major source of Revenue

- Company is also moving from high dependency on offset projects to non-offset projects in system integration

- Company is also expanding defence opportunities with foreign nations such as the US and other economies. Already received export orders from new countries/clients

- Company is getting into new segments – medical and Railways which could be higher margin opportunities and increase in revenue

- Company has the funds (200 crore) in Jan 2024, allocated to ToT JV utilizing Make in India policies, which help it to grow itself to product company in next 1-2 years

- If company gets the contract from Railways in next 4-5 months , company can show significant rise in stock price

- Company management pretty confident the year will end of positive note with revenue and PAT not going lower than last year

- DCX while has a high P/E of 44 it is much lesser than the sector which averages around 97

Current RSI: 49.9

Current Share Price:338 INR

Current P/E : 45

Recommended Buy : Company is focusing on growth and margin increase.

Share Price may grow up to 500+ in next 2 years owing to above data points, subject to risks

Sources : Trendlyne, Screener, company website, News Articles, Company presentations, Earning calls, credit reports , krchoksey report, and ofcourse Google

14 Likes

From where this data is sourced?

@Devanshi02 thank you for contributing.

The only part of your write up that I am not aware of is:

*While the company is focusing on Non-IOP segment for further resilience of its portfolio but there is a big opportunity of $13.5 billion from the IOP category which is to be executed in seven years.

-----DCX systems is well positioned to capitalize on this IOP contracts given its long-standing presence in IOP category.

** Out of $13.5 billion nearly $4 -$5 billion would be electronic requirement and DCX is well situated and capable to capitalize on this opportunity”

Can you share the original reference for this information?

dcx system research.pdf (1.3 MB)

1 Like

Have attached the research Pdf - Its from KrChoksey Research

3 Likes

thanks for the reply.

Order book from Lockheed as of December 2023 was 1,095 crores- all from aerospace and defence(80% export – offset/non-offset) , with additional 474 crores from Lockheed order

The above statement is wrong, since DCX received Lockheed order for US$ 2 Million, which translates to only INR 16+ crores, not INR 484 crores as mentioned. Please correct it. Thanks.