DCX Systems

Seems to be a fantastic play on wiring & systems for defence and aerospace. Not as overvalued as compared to peers in this category.

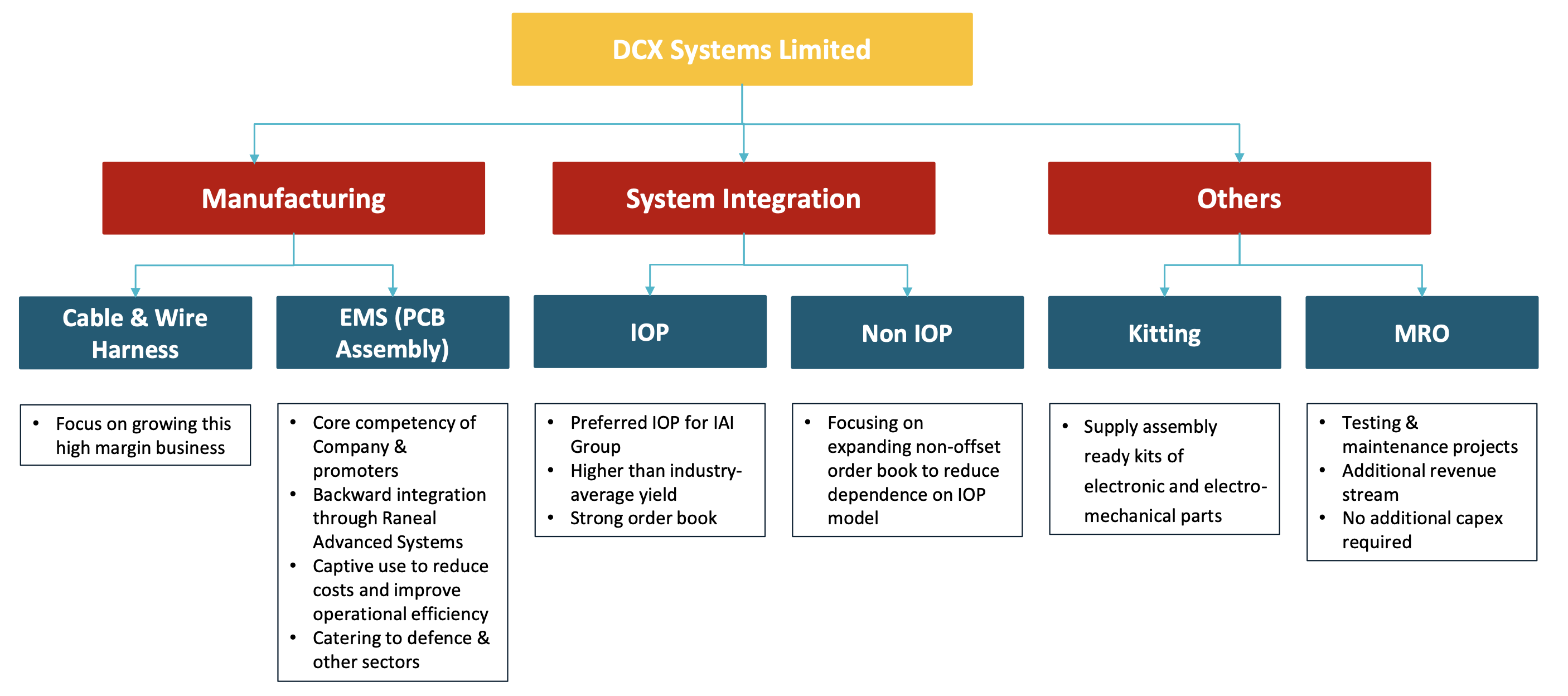

DCX has a unique business model providing end-to-end solutions of cable & wire harnesses, electronic sub-systems, high-end System Integration and PCB Assembly for Defence & Aerospace Industry.

Key Points

-

DCX is a preferred and largest Indian Offset Partner to leading Israeli Defence Company, IAI, for its offset obligations.

-

Core competency in electronics manufacturing with focus on backward integration in PCBA’s through 100% subsidiary, Raneal Advanced Systems – both for captive consumption and other markets

-

Diverse mix of domestic and international customers across Israel, US, Korea and India

-

Strategically located Manufacturing facility in SEZ in Bengaluru, spread over 30,000 sq. ft.

-

New 40,000 sq. ft. facility in Bengaluru dedicated for EMS manufacturing

-

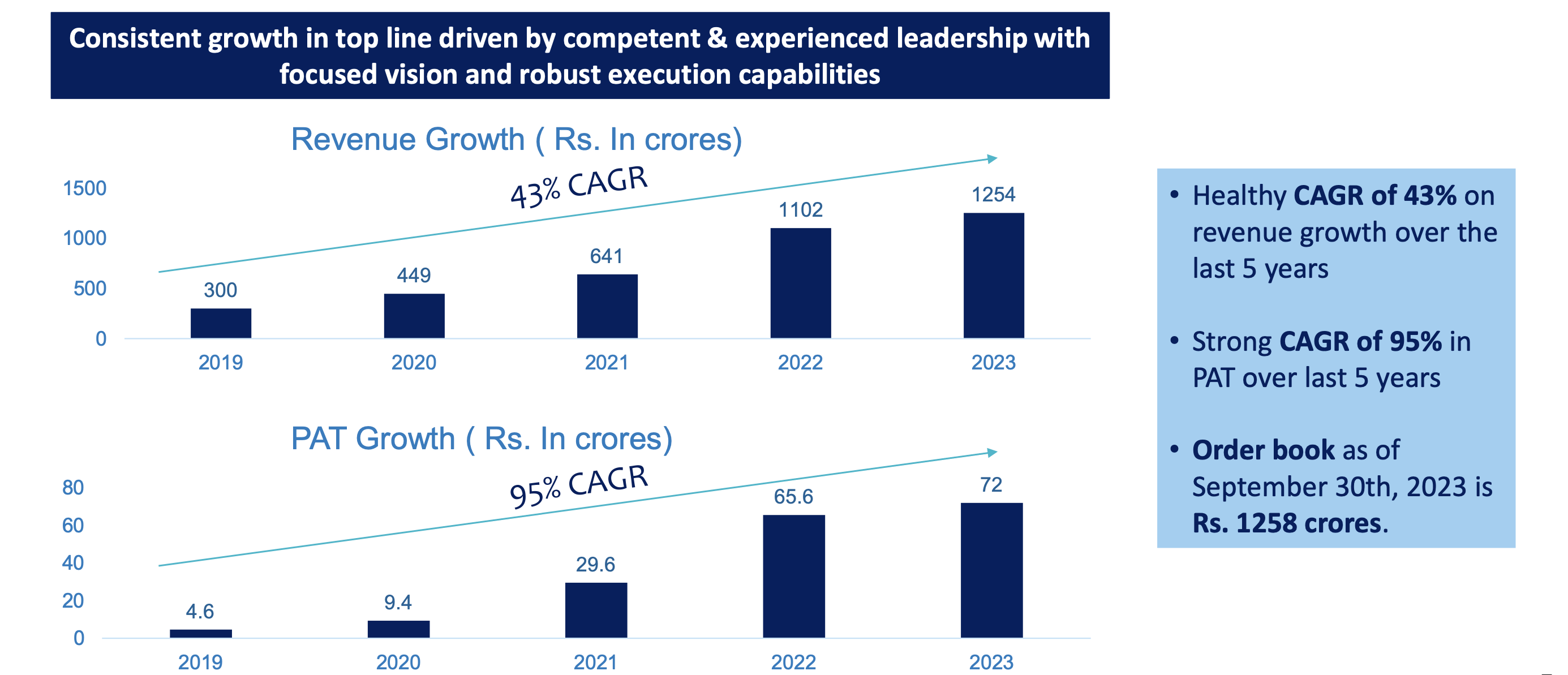

Healthy CAGR of 43% on revenue growth over the last 5 years

-

CAGR of 95% in PAT over last 5 years

-

Order book as of September 30th, 2023 is Rs. 1258 crores.

USPs

Over a decade of supplying to one of Israel’s top defence companies. Very strong relationship that has now made DCX from a supplier into a partner, through the recent JV with ELTA

IOP / Non-IOP partner for Israel / US OEMs to supply wide range of products for Aerospace & Defence

Domain expertise in developing & manufacturing aerospace & defence electronics products on Build to Print Model

Equipment for testing etc. supplied by OEMs, thus facilitating asset light business, despite capital intensive product portfolio

Among preferred Indian Offset Partners for defence & aerospace industry across geographies

Backward Integration into EMS to manufacture PCBA’s for defence & civilian sectors

–

–

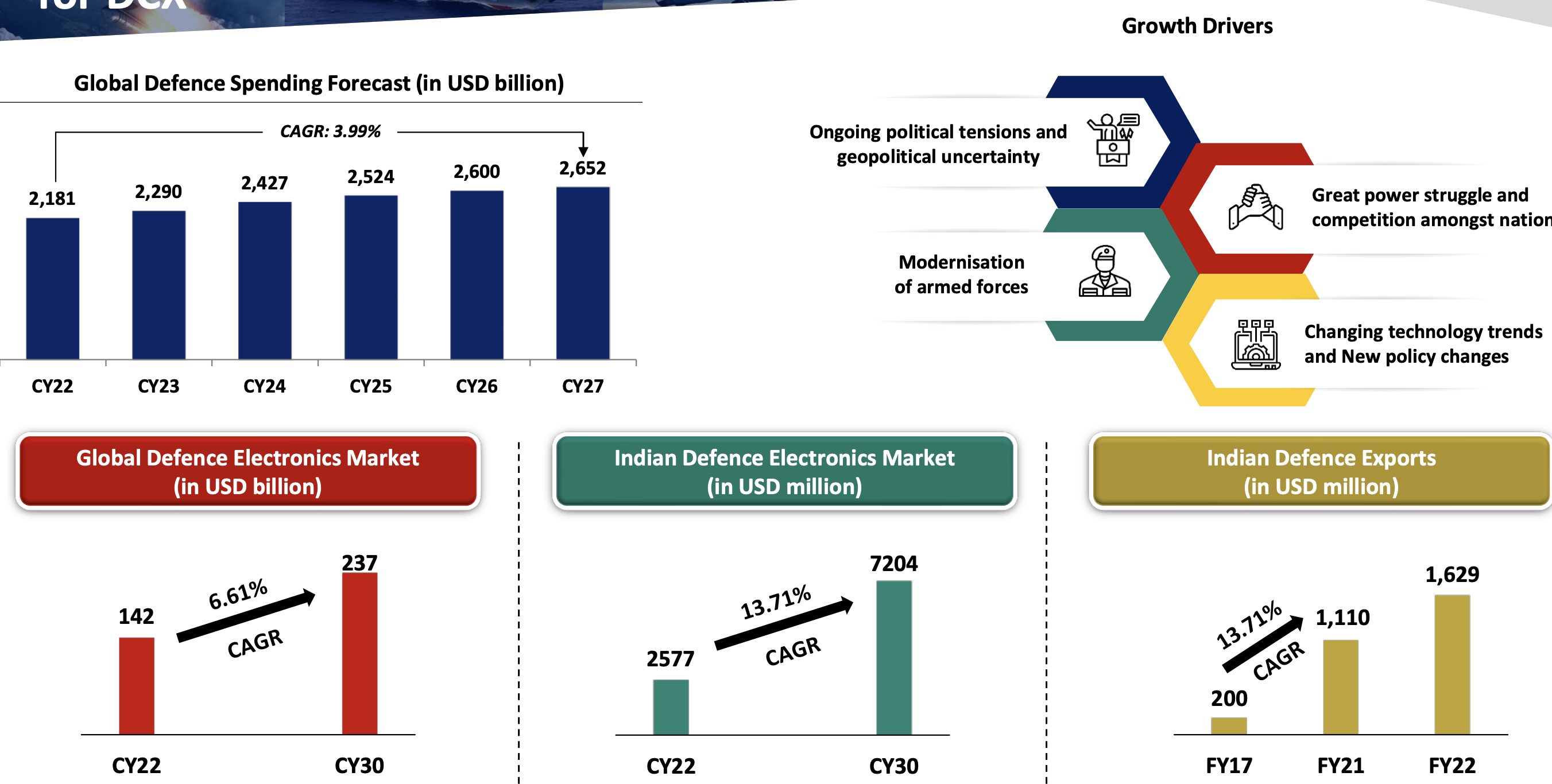

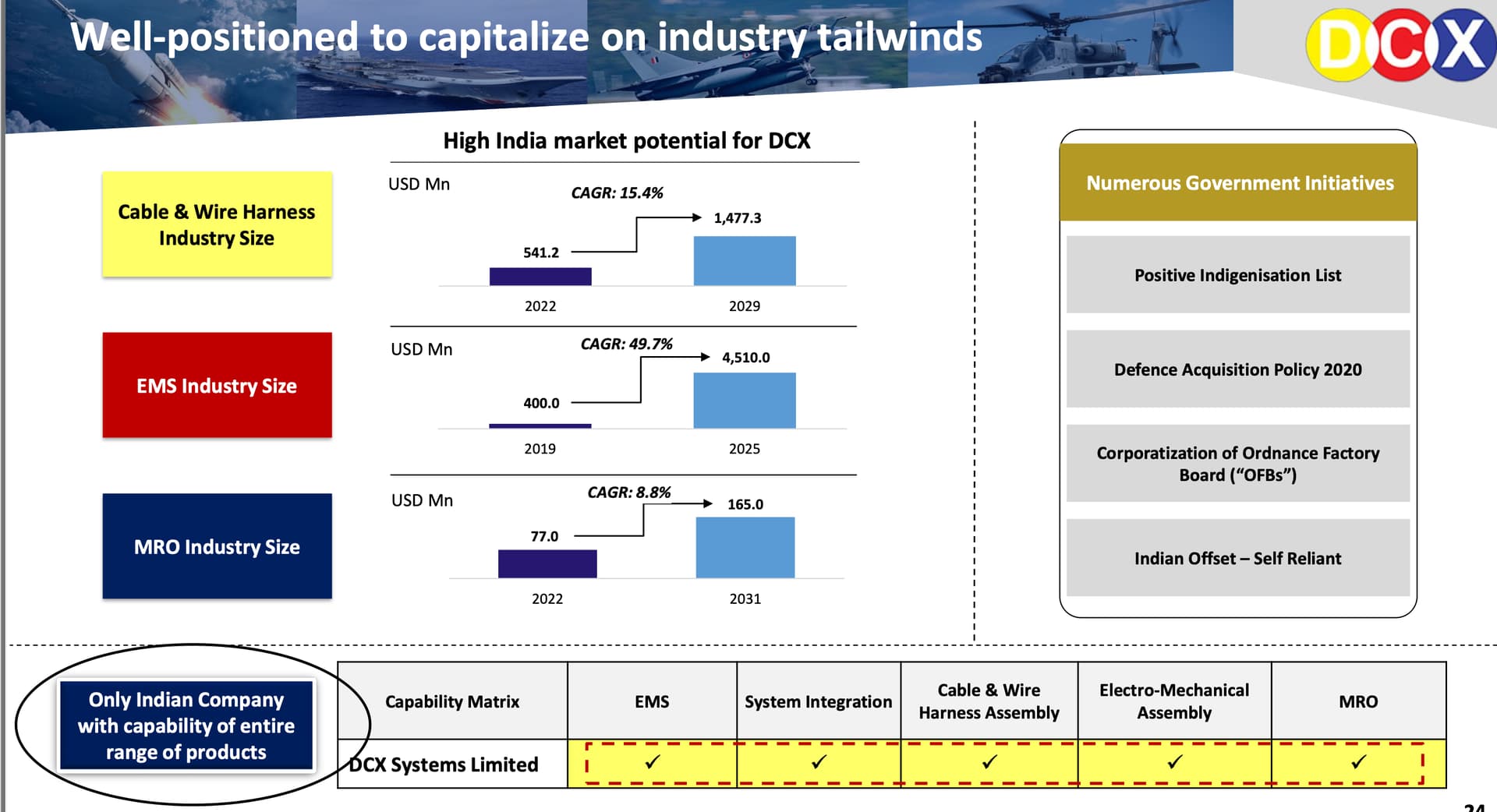

Industry Overview

–

ELTA has developed the tech for optical & radar based anti-collision systems for railways. ELTA has partnered with DCX Systems via a JV. DCX owns 51% while ELTA owns 49%. ELTA will supply the tech, DCX will do the manufacturing. The product will be manufactured by DCX and then sold to the JV company, which will then in turn sell it to the Indian government for railways, and also globally to international clients. The global market for this system is $7billion USD. The tech lies with ELTA, manufacturing with DCX, sales with the JV.

–

Found the company and management to be forward thinking and very knowledgable on the domain. Strategic partnerships, backward integrations, end-to-end in-house control, are all very appealing.

Position taken.

*Disclaimer: I invest on management depth, market leadership, sector growth & demand. My holding periods are long, and I’m alright with drawdowns, as long as corporate & business hygiene is intact. NOT an expert, just a dreamer