DCM Shriram Industries was formed in 1990 post restructuring of the erstwhile DCM Ltd wherein different businesses were split up. Some of the other companies which were part of the restructuring have given multifold returns to their shareholders. Noticeable ones being –

SRF Ltd: 68,000Cr mcap

DCM Shriram Ltd: 14,000Cr mcap

About DCM Shriram Industries

Market Cap: 708Cr, Revenue: 2350Cr, PAT: 60Cr

DCM Shriram Industries operates 4 key verticals:

Sugar: Segment results

FY2023: Revenue: 1429Cr, PBIT: 48Cr

FY2022: Revenue: 1298Cr, PBIT: 80Cr

Full forward integrated facility located at Meerut, Uttar Pradesh into cogeneration and distillery operations that de-risk the core sugar business

Expanded distillery capacity from 150 to 215 KLPD – operational from Dec 2021

Produced 31176 KL of alcohol in FY2022

As of FY2022, 45% of total sugar production has been contracted for exports

Ethanol capacity also enhanced from 85 to 155 KLPD

Commenced bottling of country liquor

During FY22, around 63% of sugar cane crushed was towards B heavy molasses as against the target of 70%. In future, company is planning to use 100% of sugar crushed towards B heavy molasses to enable higher anhydrous alcohol production

Rayon: Segment results

FY2023: Revenue: 464Cr, PBIT: 66Cr

FY2022: Revenue: 442Cr, PBIT: 45Cr

Manufacturing facility located at Kota, Rajasthan

Manufactures Nylon Chafer fabric – supplied mainly to domestic tyre companies and carbon disulphide for captive consumption – also sells Anhydrouse sodium sulphate

Manufactures rayon tyre yarn, greige and treated fabric – used as reinforcement material in tyres - Capacity of 9,855 tonnes p.a

Implemented a rayon capacity expansion project

Dipping facility also upgraded

Chemicals: Segment results

FY2023: Revenue: 458Cr, PBIT: 45Cr

FY2022: Revenue: 383Cr, PBIT: 39Cr

Sells chemicals for Pharma, Agrochemicals, Perfume, Dyes, Paints and other products

Capacity of 20,931 tonnes p.a

Engineering products: Segment results not reported separately

Forayed into defence equipment: Armoured Vehicle vertical – Granted type approval certificate in Aug 2021 – Only the second company to receive the approval for Light Bullet Proof Vehicle – Can sell to paramilitary and state forces – Being provided for no cost no commitment trials - Manufacture most parts (50%) on our own and import some parts (50%)

Obtained license to provide Unarmed aerial vehicles, communication equipment and opto electronic devices. Recurring contract since July 2018 for supplying 500 drones to GOI annually – till indefinite period

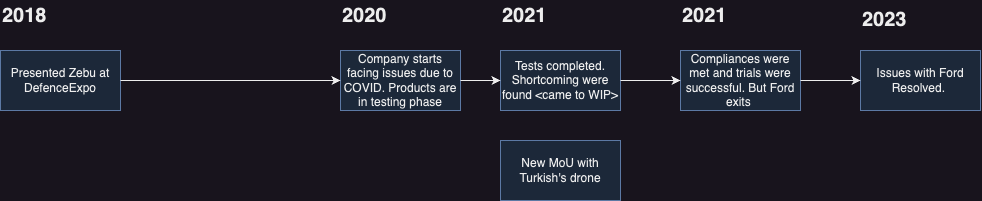

Ford India major supplier – decided to exit India

In talks with Ford India to supply from Thailand and also looking at other manufacturers

Acquired 30% stake in Zyrone Dynamics (Turkey) engaged in developing drone technology for 8.6Cr ($1.05 Million)

ZD will extend tech to company to develop different types of drones in India

Sampling and trial phase for drones with all forces

Considering the size of operations of the company and the diverse segment it operates in, DCM Shriram Industries looks to be undervalued.

With the Make in India push and tailwinds for the defence sector and venturing into engineering product division in recent years, this company looks ready to exploit the opportunity. Some of the products that are being made are as below:

To know more about the products, you may visit their website – DCM Shriram Defence

Lastly, with the recent liberalisation of policy for the export of drones or unmanned aerial vehicles under civilian use category, may open up a new segment for them, moving further away from the traditional sugar business (Link to the recent policy change)

Given this is my first crack at posting an idea on a public platform, there may be some shortcomings. Happy to hear your feedback and thoughts on the same.

I could not believe it was your first post, so very well put, I decided to take plunge and take a position looking at the CFO, this share looked cheap and also not so voltaile earnings as other sugar stocks. Thank you.

Some of the products that are being made are as below:

* Armoured Vehicle (Zebu, Carmel, Carmel Lite)

Proof of concept for Zebu was developed way back somewhere in 2017 or 2018. It was also presented to the interested parties at DefenceExpo but the management never clarified the outcome. So, I assume there were some shortcomings and no orders were received.

Defense projects can have a high gestation period but I hope management clarifies and provides some clarities on the timelines - since it has been 6 / 7 years since they entered this space.

I was going through their FY2023 Annual report and noticed the following updates relating to engineered products:

Progress on the armoured vehicle: The project had slowed down since Ford exited India and now they are in advanced discussions with Ford USA to support on the production of the vehicles. Further, they’ll are engaging with Israeli armored vehicle specialist company, GAIA Automotive to work on the design. They have also started process of registering the new vehicle with ARAI, Pune for Type Certification

Anti Drone: Signed a MOU with Skylock, Isreal (part of Avnon Group) another Israeli company for partnership to make Counter Drone Systems in India. DCM will have the exclusive rights for manufacturing and marketing their systems in India. They are also saying that a definitive agreement with Police and Defence forces is in the pipeline

What capabilities does DCM Shriram have? What do they bring to the table? Both are highly competitive fields.

Armored vehicle: Tatas, Mahindra and Leyland are present

Drone: Reliance, Adani present through smaller companies. A lot of startup backed by marquee investors

Can DCM Shriram only loose money through these ventures.

I am assuming that between 2018 to 2019, the product was being improved after which Covid came and then Ford’s exit.

However, this does make me question DCM’s approach and I have concerns over this collaboration. Ford’s good with the SUV segment but the armored vehicles are a different dimension altogether and not just an upgraded SUV.

My guess with this tie-up is that Ford is providing their SUV expertise while DCM is remodeling the vehicle. This isn’t new and companies often use Ford’s trucks as a base for such projects (Reference). You can also read their last AR - they explained some details there @nav_1996

These are the open questions I still have:

Why defence: Why would DCM choose to enter defense space? Why not expand agrochem or look for distillery space or perhaps something the management has experience in?

What’s the end goal: Is company shooting blind? From armored trucks to drones, the company has been doing everything at once. Each of these is a very specialized segment. Why not focus on one and use the available resources on one segment → achieve something (or at least discard) → then move to other? It’s not like the company has thousands of crores to burn

Speed of execution: Speed of execution is quite important in a technology-driven space. You cannot sell 3G systems if 5G is invented. You cannot make big in Mach 1 anti-missile systems if the world is moving towards hypersonic missiles. Have been tracking some other companies. Let’s call them company X and Y (not taking any names). Company X started making anti-drone system somewhere near Covid and have had much more success than DCM. Company Y has entered the autonomous drone space in the last 2-3 years - and has been making much faster progress.

Defence equipments are technology-driven and it may be very wrong to compare each of these companies. One feature can change the timelines and success. However, I do see that the other players were able to execute during Covid while DCM is still offering no clarity.

If my understanding is correct, the company should get small defense orders over the next few years. I continue to have concerns about the scalability of DCM in the defense sector. I am living with the hypothesis that the management will start to offer some clarities after Q4 or post-election.

Disclaimer: Invested (PF sizing here). This is not a buy/sell recommendation. I may add/sell anytime. Do not have any insider information and my views may change.

Scheme of arrangement: The Company has approved a composite scheme of arrangement that involves the merger of Lily Commercial Private Limited (the Transferor Company) into the Company, followed by the demerger of two business verticals of the Company, i.e., chemical undertaking and rayon undertaking (including defence and engineering projects) into two existing companies, while the residual undertaking comprising of sugar, alcohol, and power would be retained in the Company.

Simple Words:

The plan involves:

Merging with Lily Commercial Private Limited: This is a private company that invests in the Company and is owned by the same promoters. The Company will issue new shares to the shareholders of Lily Commercial Private Limited in exchange for their shares. This will simplify the promoter shareholding structure and eliminate shareholding tiers.

Demerging into three separate companies: The Company will split its three business verticals, i.e., chemical, rayon, and sugar, into three different companies. The chemical business will go to DCM Shriram Fine Chemicals Limited, the rayon business (including defense and engineering projects) will go to DCM Shriram International Limited, and the sugar business (including alcohol and power) will remain with the Company. The shareholders of the Company will get an equal number of shares in each of the three companies. This will allow each business to have more focus, efficiency, flexibility, and growth potential.

So, After this restructuring, there will be 3 separate companies:

1. DCM Shriram Fine Chemicals Limited. { will have the chemical business.} 2. DCM Shriram International Limited. { the rayon business (including defense and engineering projects)} 3. DCM Shriram Industries Limited. { the sugar business (including alcohol and power)}

Share exchange ratio: The Company will issue equity shares to the shareholders of the Transferor Company and the Resultant Companies in the ratio of 1:1 and 1:1, respectively, based on the valuation reports and fairness opinions provided by independent valuers and consultants.

Rationale for the Scheme: The Scheme is expected to provide greater management focus, operational efficiency, financial flexibility, shareholder value, and business growth for each of the demerged undertakings, as well as streamlining the promoter shareholding and facilitating succession planning.

Approvals and disclosures: The Scheme is subject to the approvals of the shareholders, creditors, regulators, and tribunals of the companies involved in the Scheme, and the disclosures required under the applicable laws and regulations. The Resultant Companies are proposed to be listed on the stock exchanges upon the completion of the Scheme.

As far as I understand there is no revenue from defence segment yet. Industrial fibre division contributes to 21.64% (which would perhaps include defence).

A good time to look at the company is when it is not talked much, slowly and gradually have moved and now consolidating in a range, possibly getting ready

Approval from exchanges/SEBI was received mid-September 24. The next major milestone is NCLT approval which may come during Q4 (given it takes 3-6 months). Demerger may have around Q1-26.