Data Patterns (India) Limited is a vertically integrated defence company and have design capabilities catering to the entire spectrum of defence and aerospace (land, sea, air and space) platforms. It is one of the fastest growing companies in the defence and aerospace industry.

Core Competencies

- Product prototype design and development

- Electronic hardware design and development

- Software design and development

- Firmware design and development

- Mechanical design and development

- Functional testing and validation

- Environment testing and verification

- Engineering services

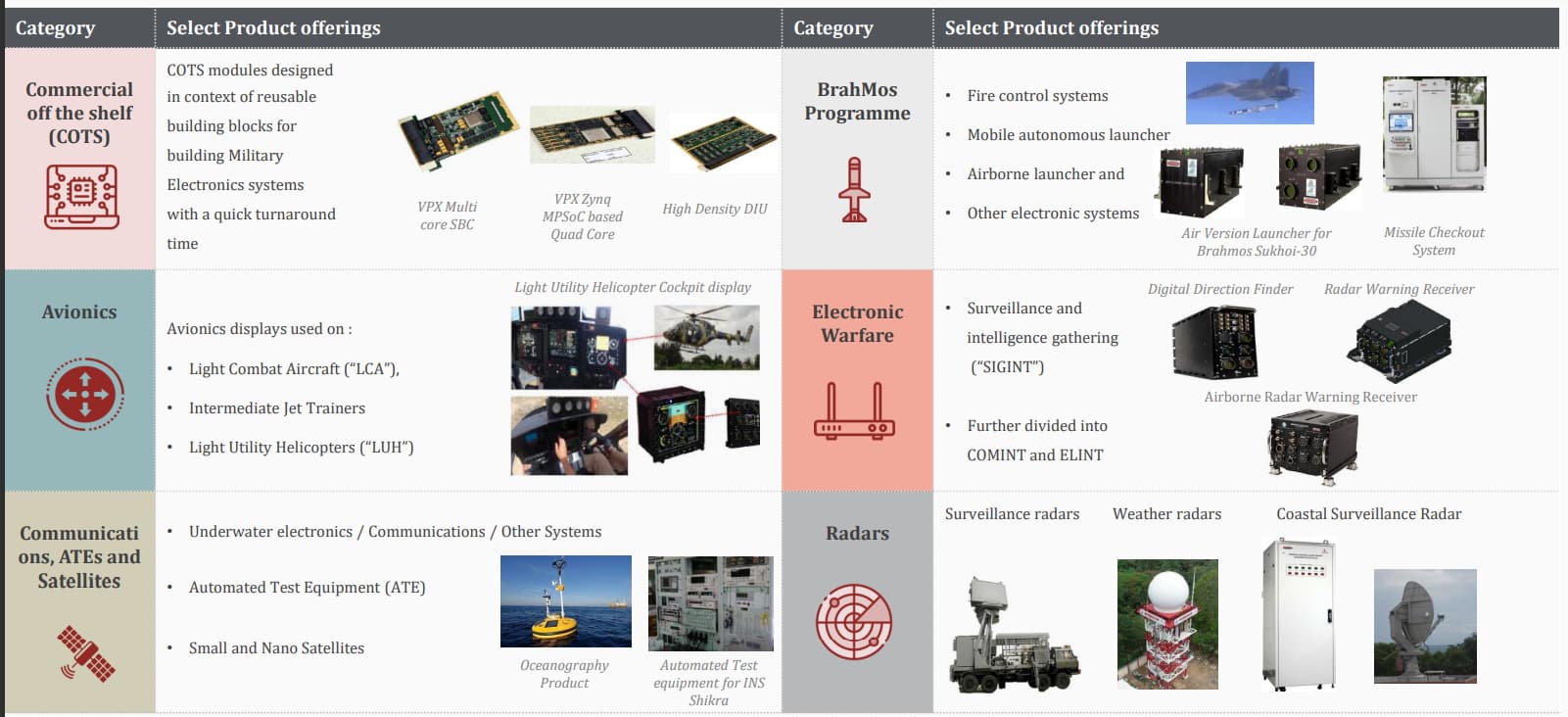

Key Product Offerings

Source:- Q3 Investor Presentation

- Radars

-

Surveillance Radar - used in detecting moving targets

Data Patterns has developed several electronic components for Ashwini, an import substitute product of Electronics and Radar Development Establishment (LRDE) of the Defence Research & Development Organization (DRDO). -

Weather Radar - used for cloud and rainfall measurement

The company has executed 2 orders for Weather radars in Mumbai and Chennai. -

Wind Profiler Radar - used in determining the direction and intensity of the wind at various altitudes

They have designed and developed the world’s first 205 Megahertz (MHz) system in Cochin, which is used for atmospheric research. -

Tracking radars - used by ISRO to monitor the flight trajectory of PSLV and GSLV launch vehicles, sounding rockets that are launched from SDSC Sriharikota and from Thumba Equatorial Rocket Launching Station at Trivandrum.

-

BrahMos missile seeker - the portion of the missile which searches for the target and thereafter guides the missile to its target.

- Underwater electronics/Communications/other systems

The oceanography products are used for data acquisition requirements of ocean resources like

-

Air and Seawater temperature

-

Salinity

-

Wind speed and its direction

-

Wave Intensity

The company is vertically integrated in this category.

-

Avionics display - These are used in the cockpits of aircrafts and helicopters.

The company has developed the entire glass cockpit for Light Utility Helicopter along with the data interface unit. -

Automated Test Equipment - Used in electronic devices for functionality and performance. The Indian government space organization requires various types of automated test equipment for the development of its test benches for the Polar Satellite Launch Vehicle (PSLV) and Geo Stationary Launch Vehicle (GSLV). All the electronic systems on the PSLV and GSLV as well as some satellite sub-systems are tested by the Indian government space organization using such ATE.

This has been the core business for the company for over 25 years and it is the only company in India

to have developed these complex ATE modules and is well established to capture the opportunity.

The following are the notable achievements and various test equipment indigenously designed and developed by the Company.

Source:- RHP

Industry Overview

The global defence expenditure is expected to grow to $ 2 trillion by 2025 due increased geo-political uncertainties. The CAGR of global defence expenditure in the last 5 years is approximately 3.6%. The top 15 spenders contribute to 81%of the global defence expenditure. The Indian defence budget has grown at a CAGR of 7% in the last 5 years.

The government has recently increased the defence expenditure from Rs. 4.8L crores to Rs. 5.2L crores in FY23. 68% of the outlay for defence procurement will be set aside for buying from domestic industry and that 25% of the allocation for defence research and development (R&D) will be kept for collaboration with the private sector.

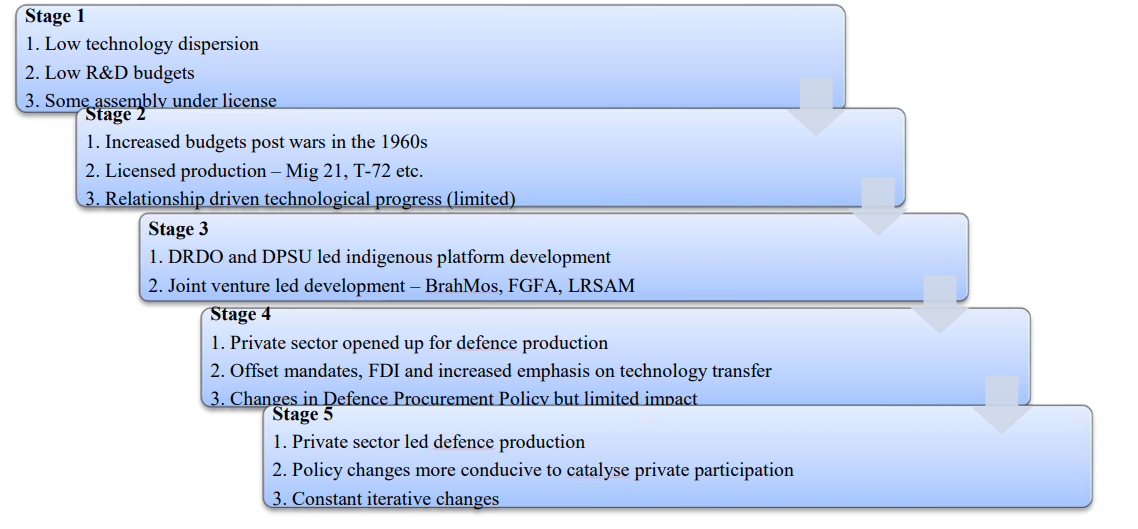

The Indian defence industry going through a major change where private sector participation is increasing. Below is the transition of the Indian defence industry over various stages.

Source:- RHP

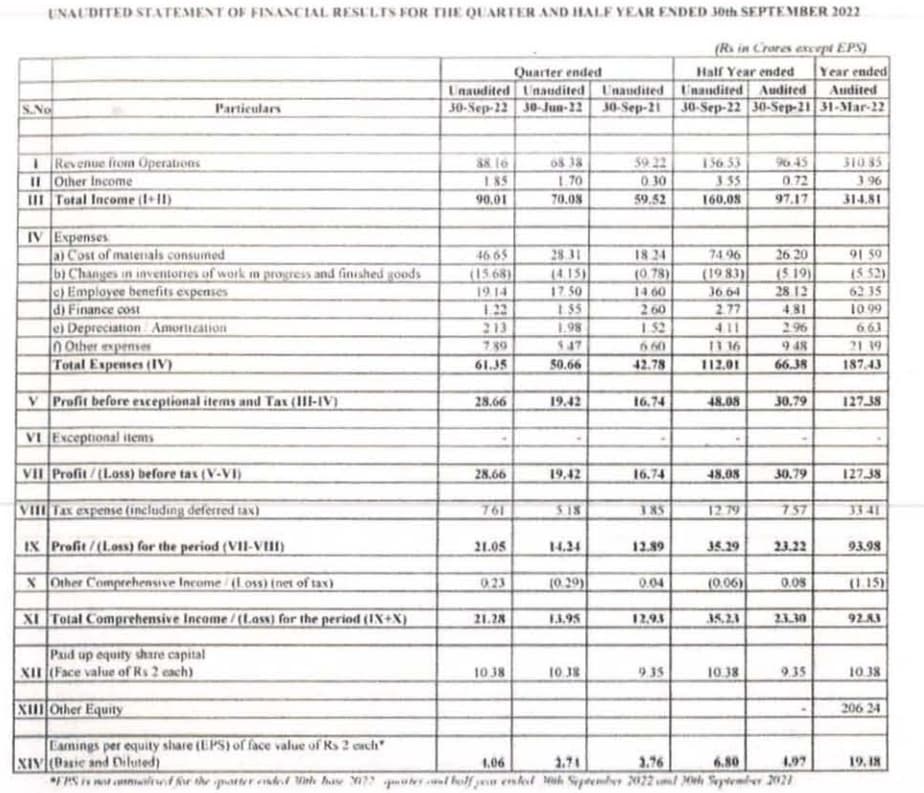

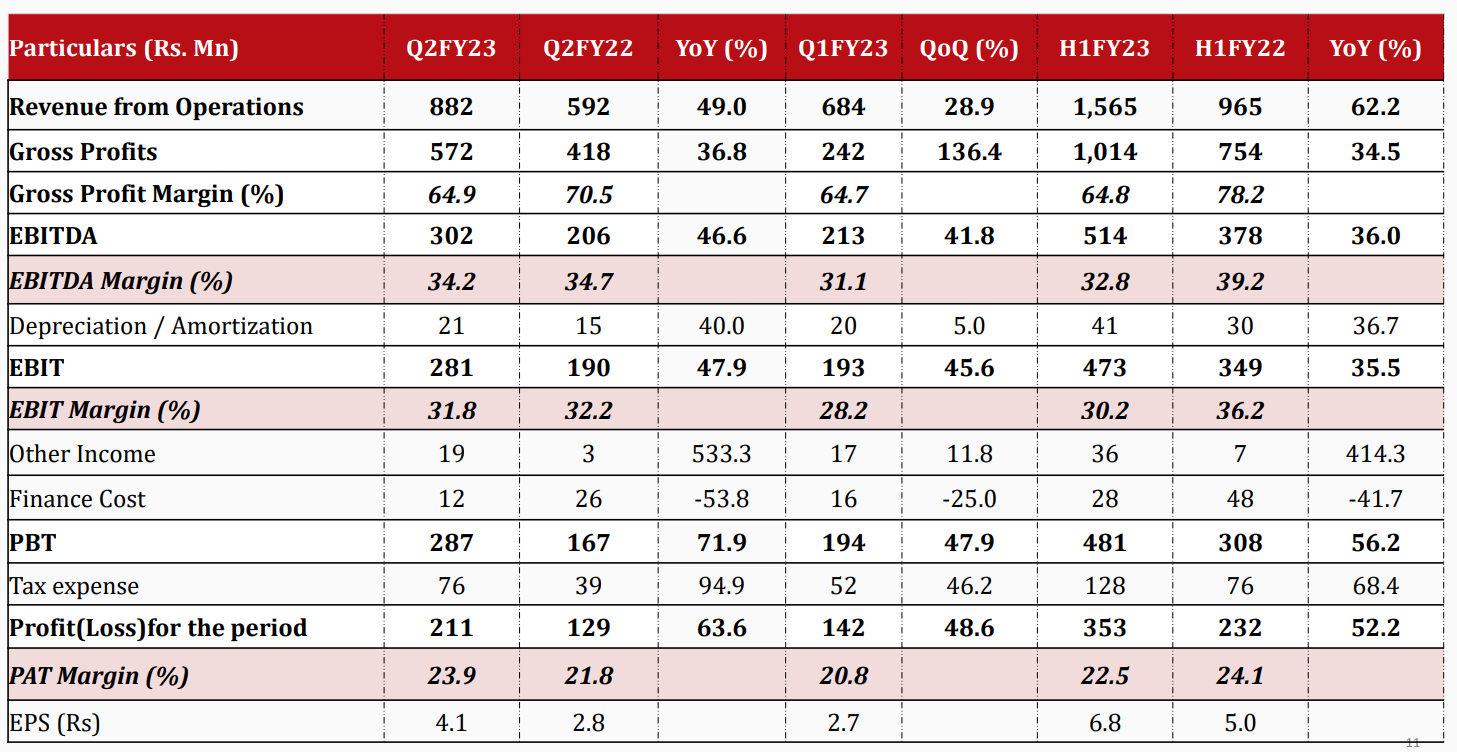

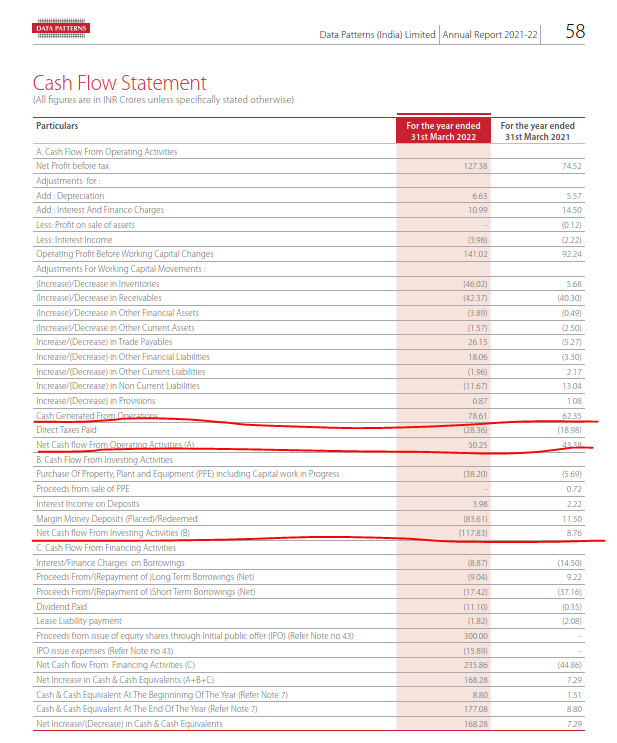

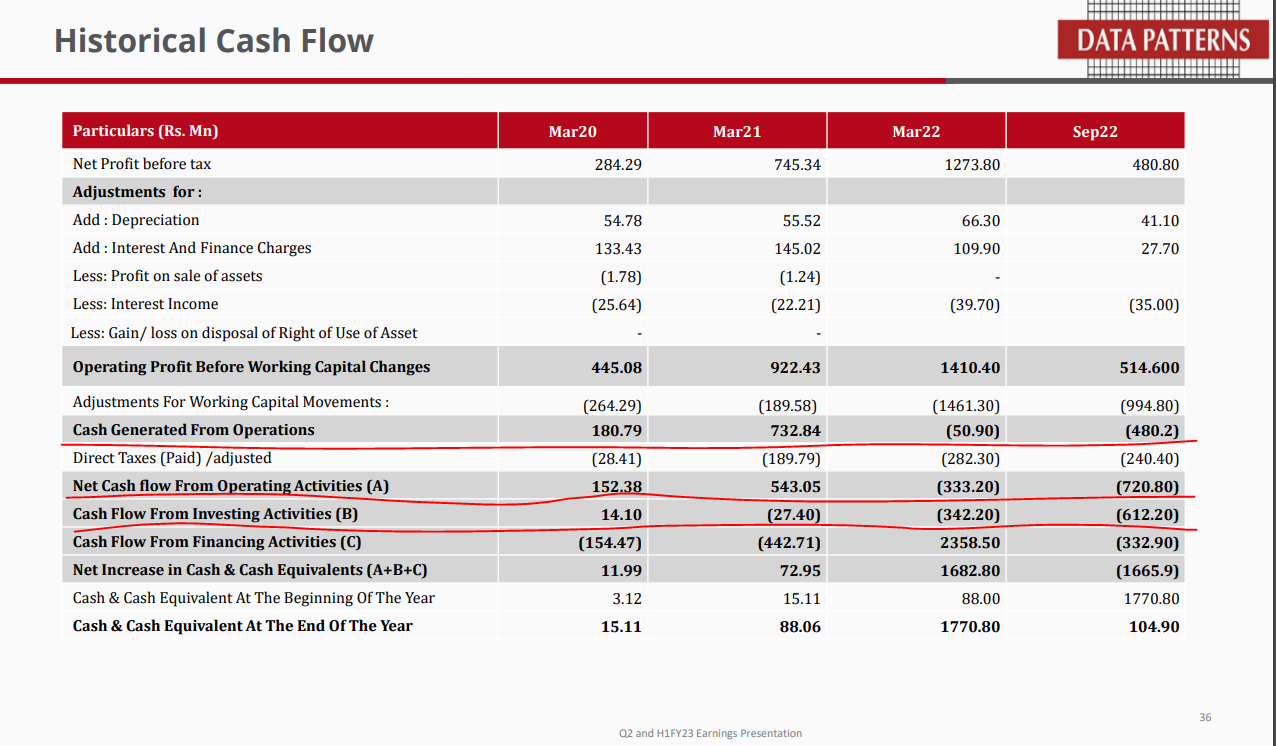

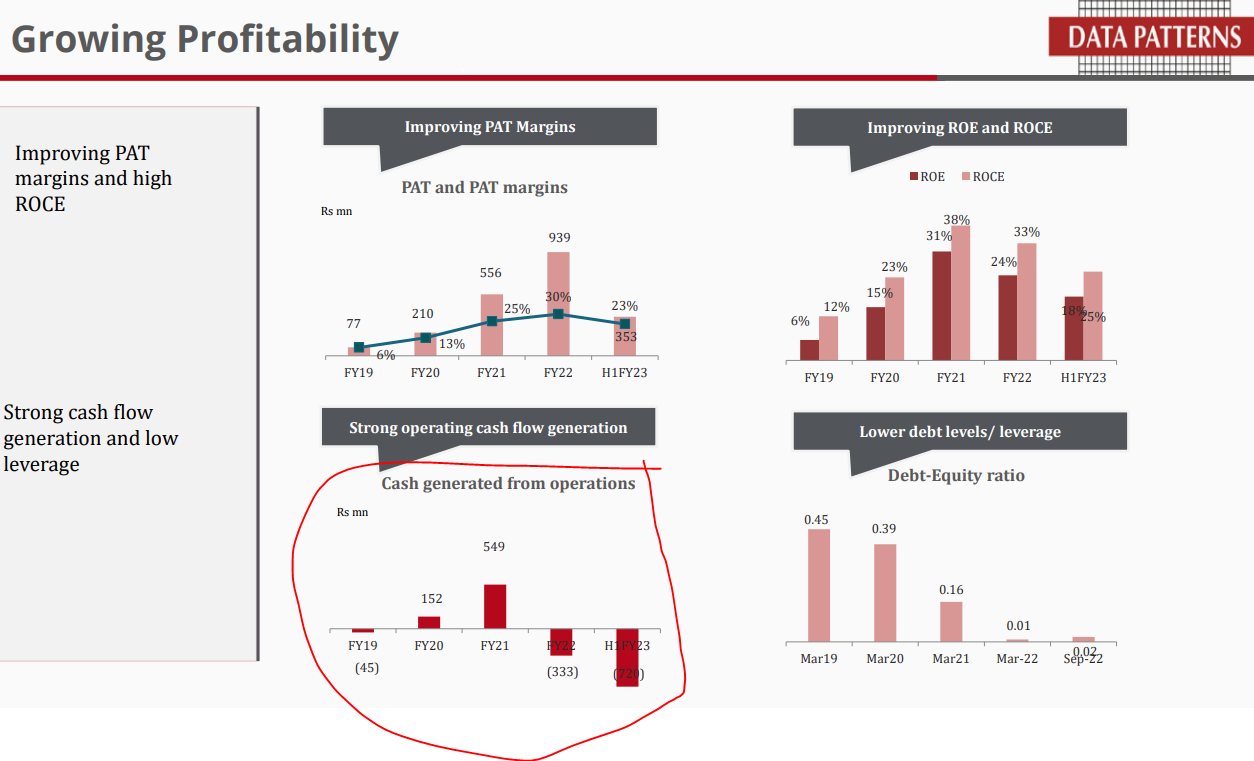

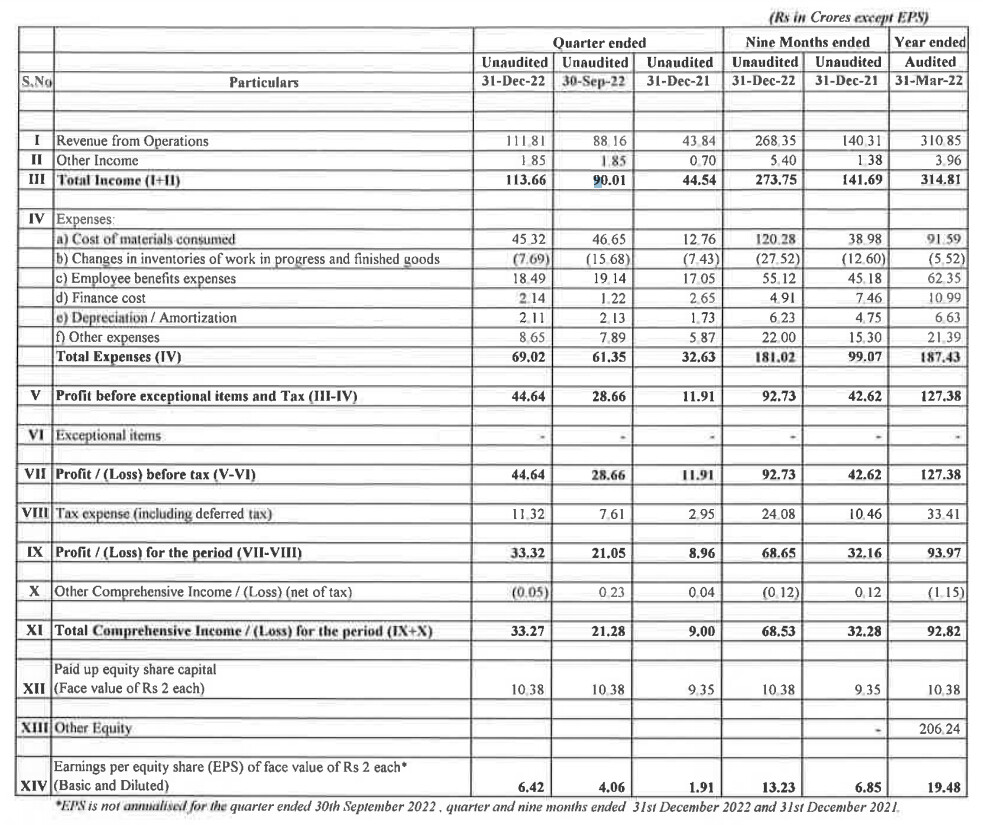

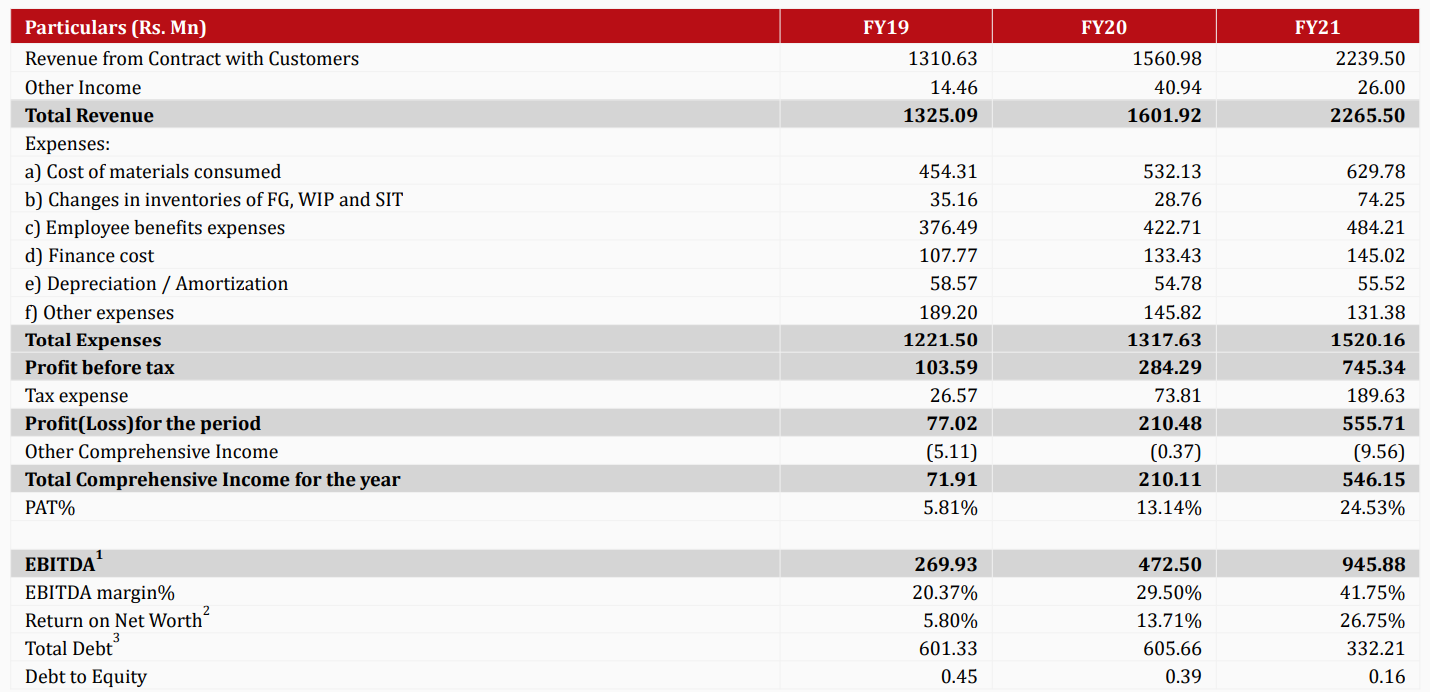

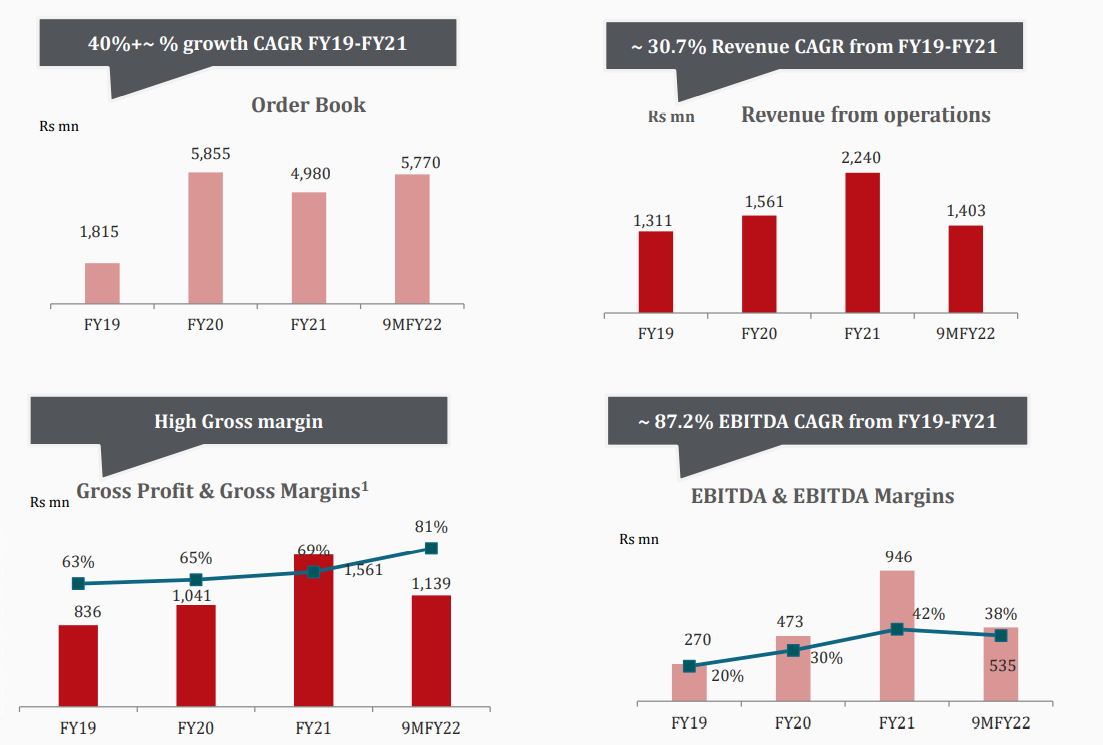

Financials

Source:- Q3 Investor Presentation

Key Strengths

-

The Indian defence industry is evolving into a self-sustaining industry with major focus on the indigenous manufacturers with themes like Make in India and Aatmanirbhar Bharat. The company is well-positioned to capitalize on this opportunity.

-

Focused on in-house development and manufacturing facilities led by innovation and design and development efforts.

-

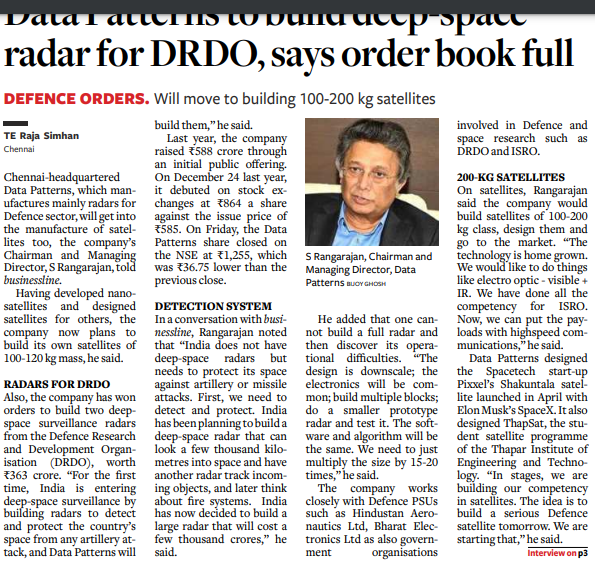

A strong order book of Rs. 577 crores (as of 31st December 2021) which is 4x the current revenue run-rate.

-

Certified manufacturing facility of international standards and consistent track of profitable growth due to a scalable business model.

Risks

-

Large dependence on Government of India and Defence PSUs.

-

Concentration risk because of very limited customers which contribute to their major revenue.

-

Heavy dependence on winning the bids from the government.

-

The shares pledged by the promoters is more than 55% of their total shareholding post IPO.

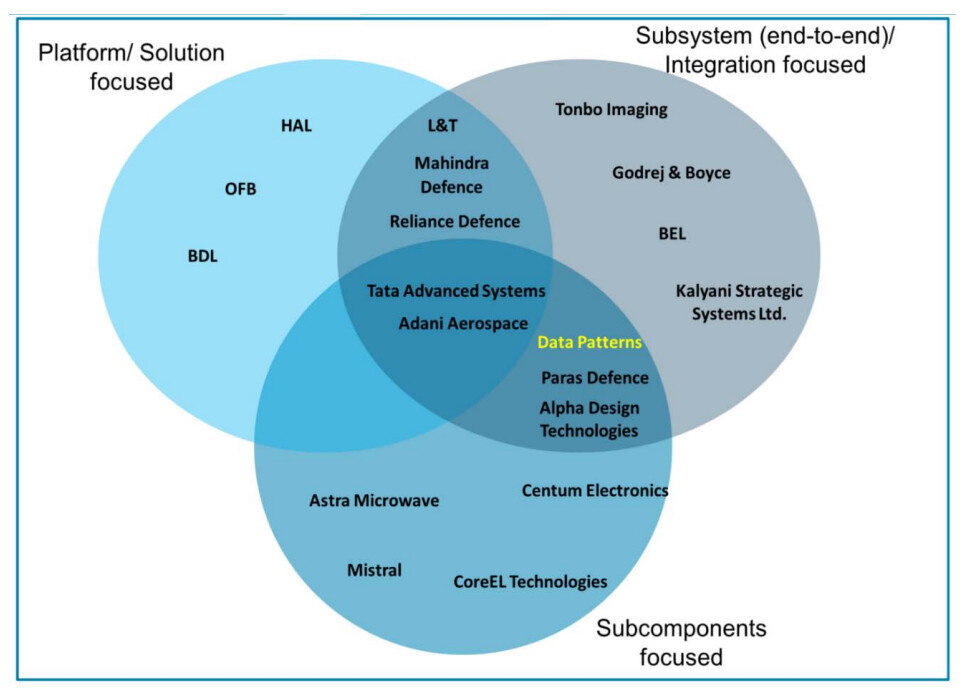

Competitors

They face a strong competition from listed players such as L&T, Bharat Electronics, Mahindra Defence, MTAR Technologies, Alpha Design Technologies and Astra Microwave Products. (not exactly an apple to apple comparision)

Source:- RHP

Investment Thesis

The company’s innovation focused business model, large market opportunities in Indian defence & aerospace, Make in India initiative, strong order book across product categories, consistency in profitable growth due to a scalable business model are likely to help improve its growth and margins in the long run.

The valuation is currently at a P/E ratio of 67x and at a P/S ratio of 17x, which is reasonable when compared with MTAR and Paras Defence trading at higher levels.

Below is the DRHP and Q3 FY22 Investor Presentation for reference.

Disclosure:- Invested from IPO levels.

I’m not a SEBI registered advisor nor associated with the organization. Please do your own due diligence before investing. This is not an investment advice and is for educational purposes only.