IMO, this is the most important slide as I see Data Patterns to be a long term sectoral play.

Though the valuation is a bit expensive, the growth rate is sustainable with good order book visibility. Furthermore, the export potential is huge going forward. Currently only 10% of revenue is from exports.

Positives to look out for:

More value added products with increased sophistication

Increased client base

Sectoral tailwinds:

Commercialisation effort of Indian defense - govt is quite keen to improve the export fraction

Make in India - Particularly for defense, India wants to be self reliant

Data Patterns diverse product range includes it products supplied for products like LCA-Tejas, Light Utility Helicopter, BrahMos missile.

I understand outlay from budget may be for various major defense products but Data Patterns product range diversification will always find its applications like Radars, Communication Systems, Electronic Warfare and Satellite.

Though the fundamentals look strong and revenue growth prospects are there, the current stock valuations seem to account for a very high growth far into future.

If the PAT becomes 3x over next 5 years, the current valuation is still justifiable.

Few questions in my mind right now:

what is the revenue & PAT projection that is reasonable for Data Patterns? As per reverse DCF, something around 40% growth in PAT is priced in.

will their orderbook growth continue over to next few years?

will they be able to service their orderbook with their capacity additions?

is there more upside from a fundamental POV considering the current rich valuation?

Just putting this out as defence sector has run up a bit and we need to be cautious not to get caught in cycle peak / bubbles.

I have a followup question, as the no. of shares is increasing through IPO/QIP/QIB etc the EPS growth might get impacted ? hypothetical example, if the PAT grows by 10% and same year company increase no. of shares by 10%, the EPS would remain constant inspite of the growth and hence minority shareholder doesnt get the full benefit of the growth?

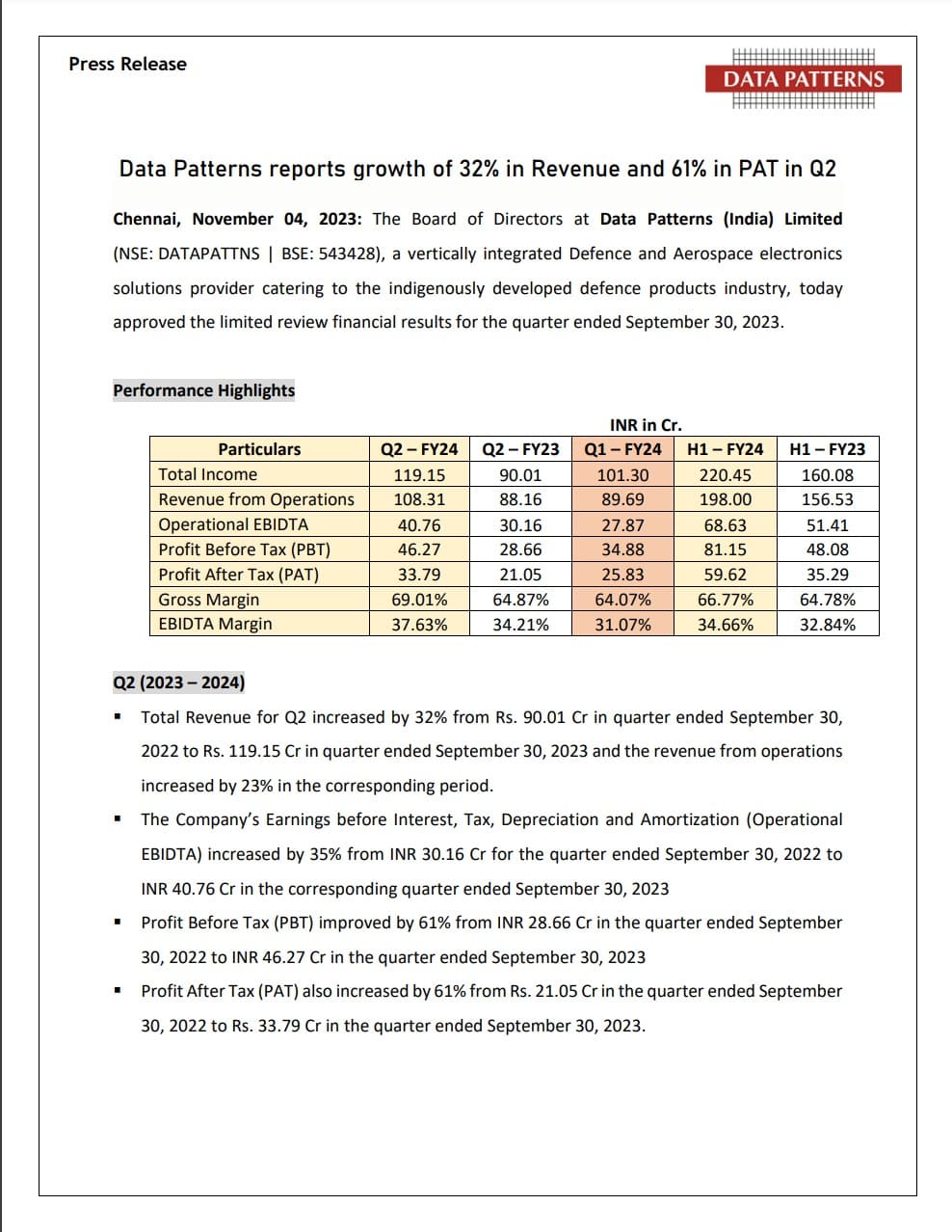

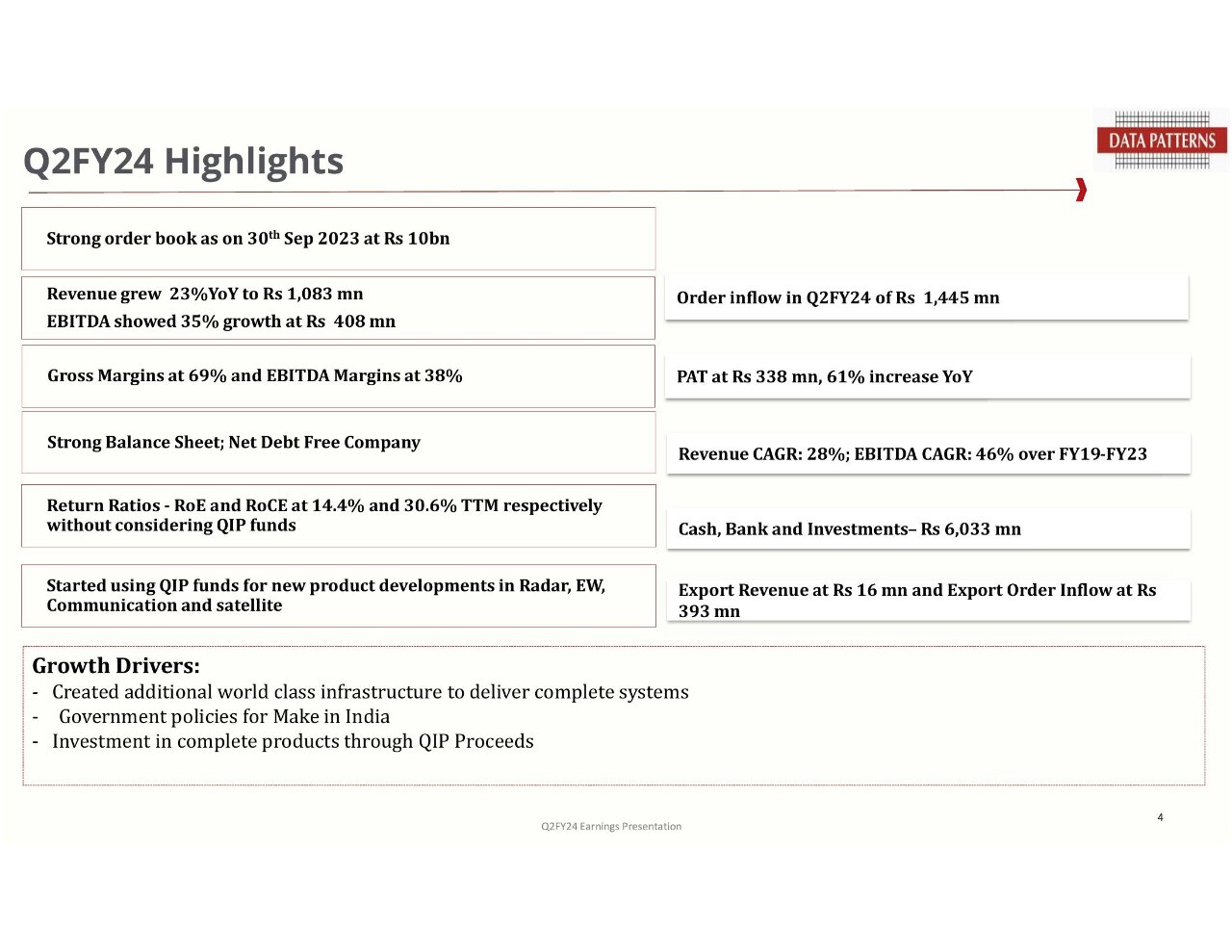

Data Patterns (India) Limited, a defense and aerospace electronics solutions provider, has reported significant growth in its financial results for Q2 FY 2023-24.

Total income for Q2-FY24 increased by 32% compared to the same period last year.

Revenue from operations in the same quarter increased by 23%.

Operational EBIDTA increased by 35%.

Profit Before Tax (PBT) improved by 61%.

Profit After Tax (PAT) also increased by 61%.

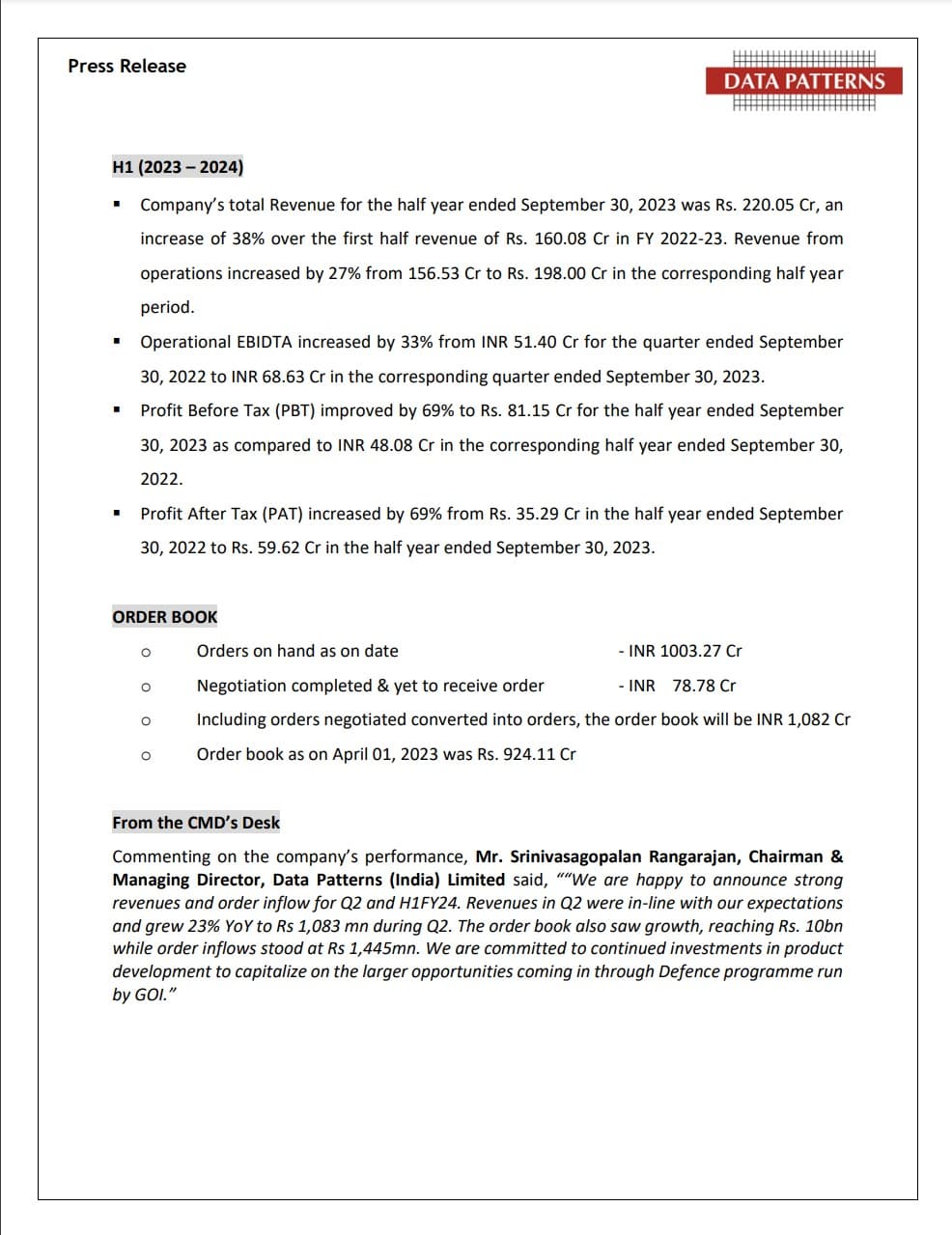

For H1 FY 2023-24:

Total revenue for the first half of the year increased by 38%.

Revenue from operations in the corresponding half-year period increased by 27%.

Operational EBIDTA increased by 33%.

Profit Before Tax (PBT) improved by 69%.

Profit After Tax (PAT) increased by 69%.

Additionally:

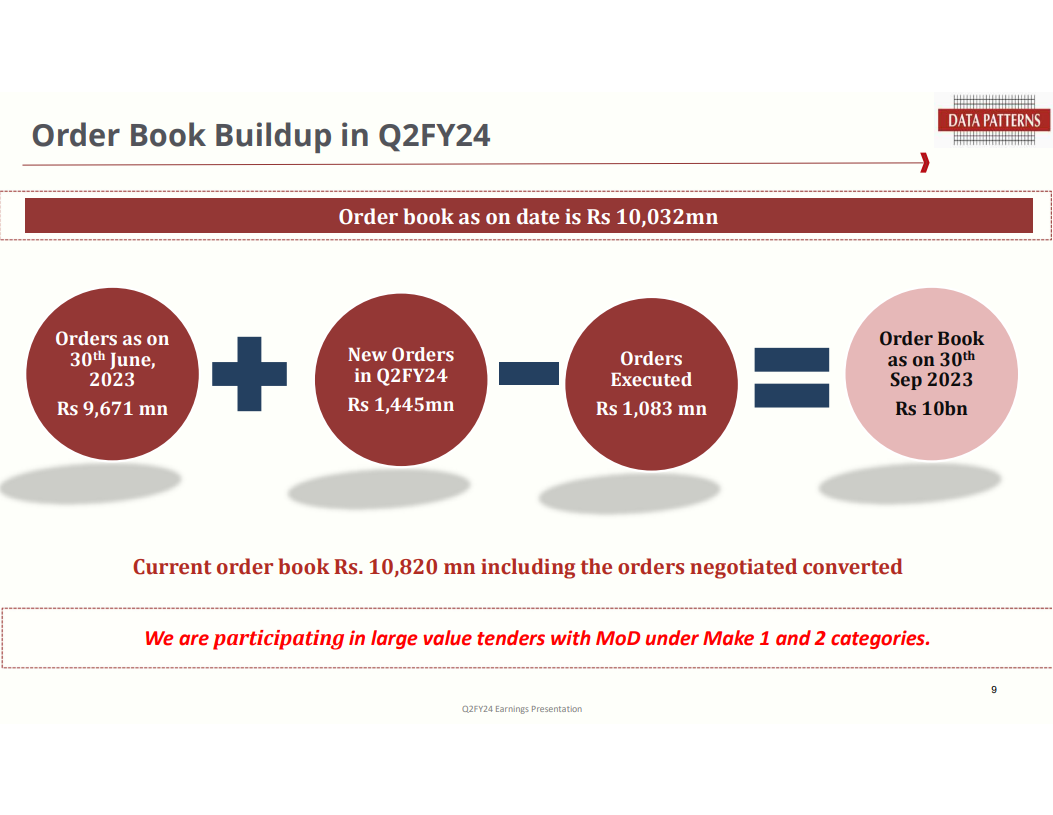

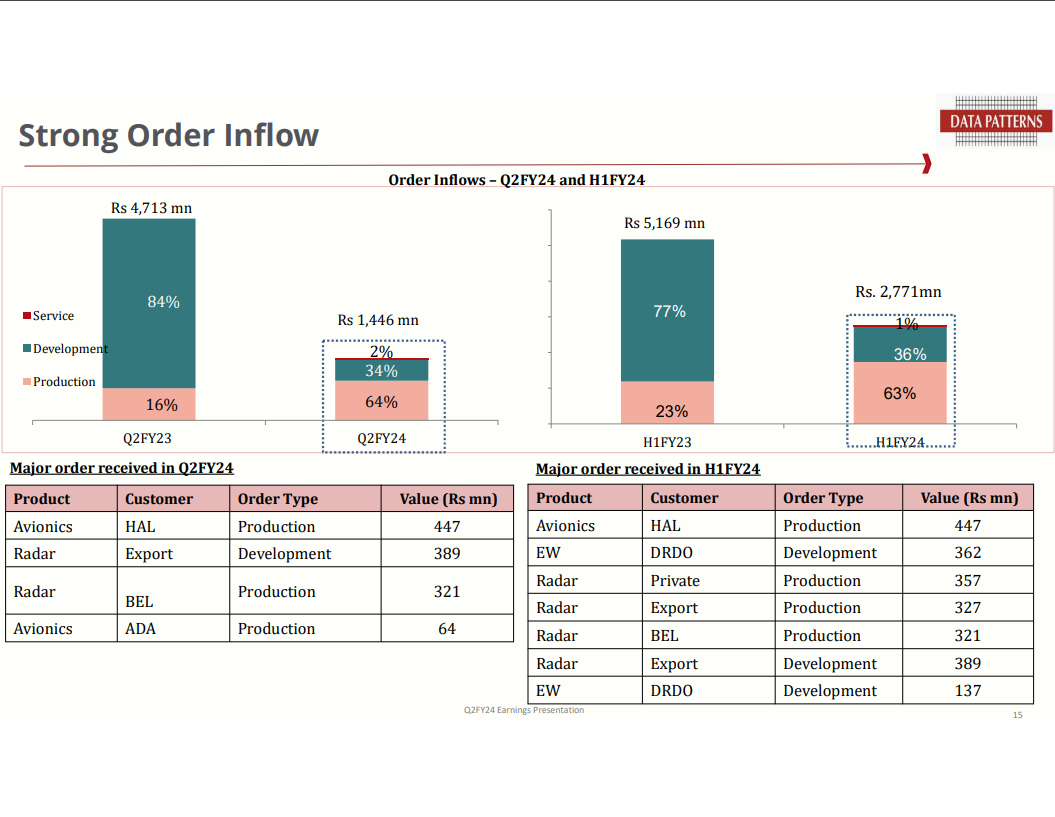

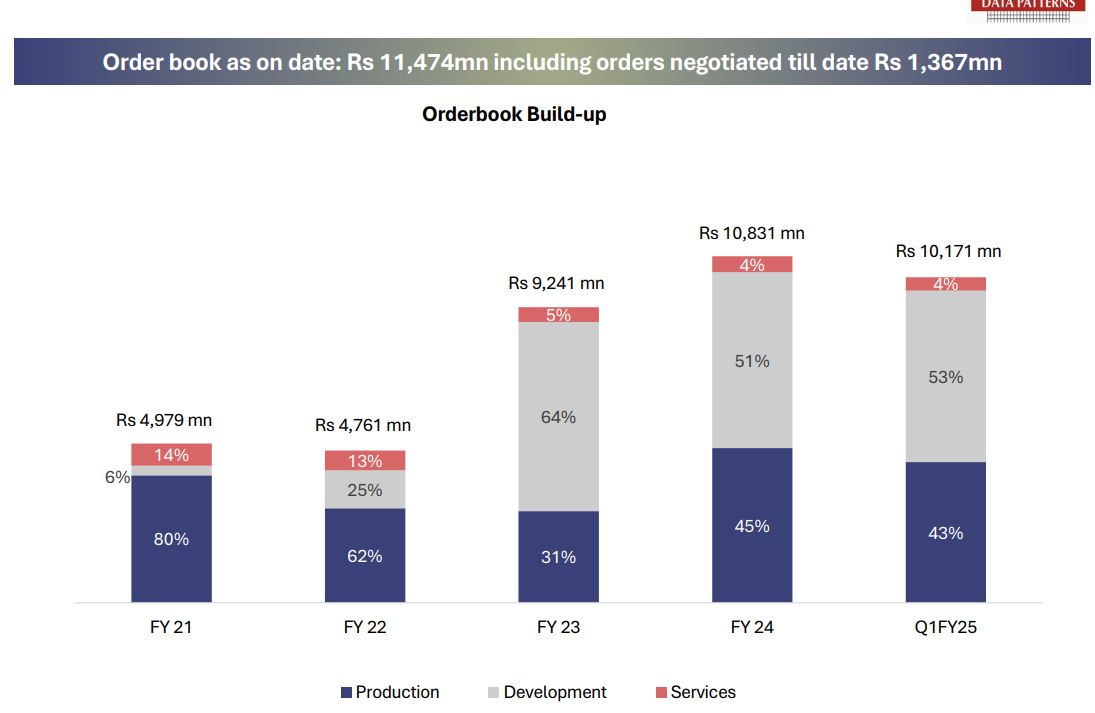

The company’s order book as of the date stands at INR 1003.27 Crores.

Orders negotiated but not yet received are at INR 78.78 Crores.

Including converted negotiated orders, the total order book reaches INR 1,082 Crores.

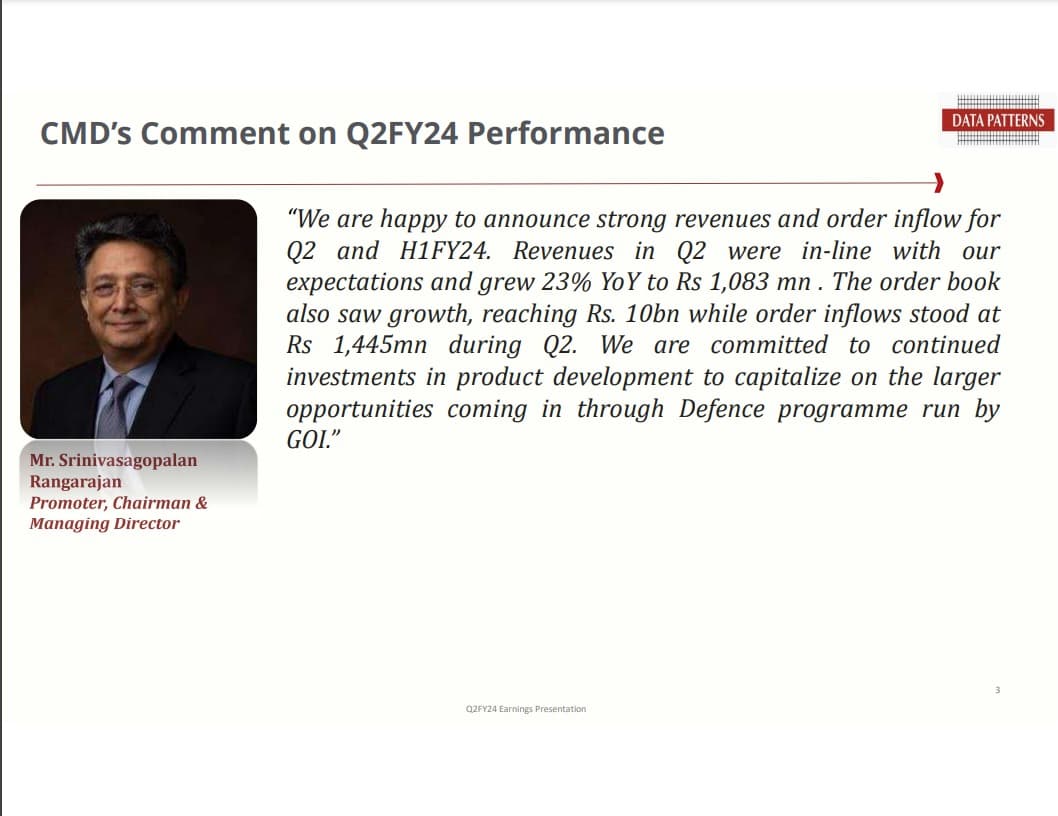

Mr. Srinivasagopalan Rangarajan, Chairman & Managing Director of Data Patterns (India) Limited, expressed satisfaction with the strong revenues and order inflow for Q2 and H1 FY24. The company is committed to further investments in product development to capitalize on the opportunities in the defense program run by the Government of India.

Singapore sovereign wealth fund GIC bought a 6.3% stake for ₹650 crore, while Mirae Asset Mutual Fund acquired about a 2% stake for ₹201 crore. Similarly, Kotak Mahindra Mutual Fund purchased shares worth ₹100 crore, and HDFC Mutual Fund bought ₹25 crore worth of shares.

Underwater UAVs & more: DRDO awards 7 cutting-edge defence projects to start-ups and MSMEs

The radar signal processor with active antenna array simulator will enable deployment of multiple target system for test and evaluation of multiple short-range aerial weapon system. It serves as the basic building block for larger radar systems. The project has been sanctioned to Data Pattern (India) Limited, Chennai.

Data Patterns continues to demonstrate strong growth potential in India’s evolving defense technology sector. The company reported 15% year-over-year revenue growth and 33% EBITDA growth in Q1 FY25, with EBITDA margins at 36%. With a robust order book of 1,147 crores and a focus on in-house product development, Data Patterns is well-positioned to capitalize on India’s push for indigenous defense manufacturing.

Strategic Initiatives:

Emphasis on in-house IP development: The company is investing heavily in developing proprietary products to address a larger total addressable market (TAM) of 15,000-20,000 crores.

Vertical integration: Data Patterns is moving up the value chain by developing comprehensive systems using reusable building blocks.

Focus on full system development: The company is transitioning from subsystem supplier to full system provider to directly address Ministry of Defense requirements.

Trends and Themes:

Increasing indigenization of defense technology in India

Shift towards full system development rather than just components or subsystems

Growing emphasis on electronic warfare, radars, and communication systems in defense

Industry Tailwinds:

Government’s Atmanirbhar Bharat and Make in India initiatives

Increased capital outlay for defense sector (6.21 lakh crores for FY25)

Push for domestic capital procurement in defense (1.06 lakh crores earmarked)

Industry Headwinds:

Potential delays in customer acceptance and order execution

Complex certification and testing processes for defense products

Global supply chain challenges for certain components

Analyst Concerns and Management Response:

Concern: Slowing revenue growth (15% YoY in Q1 vs. previous guidance of 20-25%)

Response: Management expects stronger growth in Q3 and Q4, maintaining 20-25% annual growth guidance

Concern: Delays in order inflows

Response: Company expects 800-1000 crores of order inflows in FY25, primarily in Q3 and Q4

Concern: Dependence on government contracts and potential delays

Response: Diversifying product portfolio and customer base, including exports

Competitive Landscape:

Data Patterns faces competition from both domestic players and international OEMs. However, its focus on in-house IP development and full system capabilities gives it a competitive edge in addressing India’s defense requirements.

Guidance and Outlook:

Revenue growth of 20-25% annually

EBITDA margins of 35-40%

Order inflow target of 800-1000 crores for FY25

Capital Allocation Strategy:

Significant investment in new product development (54 crores spent from QIP funds)

Planned capex of 150+ crores over next two years for infrastructure development

Focus on retaining cash for future growth opportunities rather than dividends

Opportunities & Risks:

Opportunities:

Expansion into new defense technology areas (e.g., UAV radars, military radios)

Growing export potential

Increasing domestic defense production targets

Risks:

Dependence on government contracts and potential delays

Technological obsolescence in rapidly evolving defense tech landscape

Geopolitical risks affecting defense spending

Regulatory Environment:

Favorable regulatory environment with government initiatives supporting domestic defense production and increased capital allocation for the sector.

Customer Sentiment:

Strong customer interest in indigenous defense technologies, but potential delays in order placement and execution due to complex procurement processes.

Top 3 Takeaways:

Data Patterns is well-positioned to capitalize on India’s push for indigenous defense technology with its focus on in-house IP development and full system capabilities.

The company maintains strong growth and margin guidance despite near-term challenges, supported by a robust order book and promising product pipeline.

Successful execution of the company’s product development strategy could significantly expand its addressable market and drive long-term growth.

If I recollect, the business line article during IPO, that mentioned, the Data Patterns have a moat of recurring revenue streams of around 25-30%, which is a major differentator with other defence companies.

This might help.

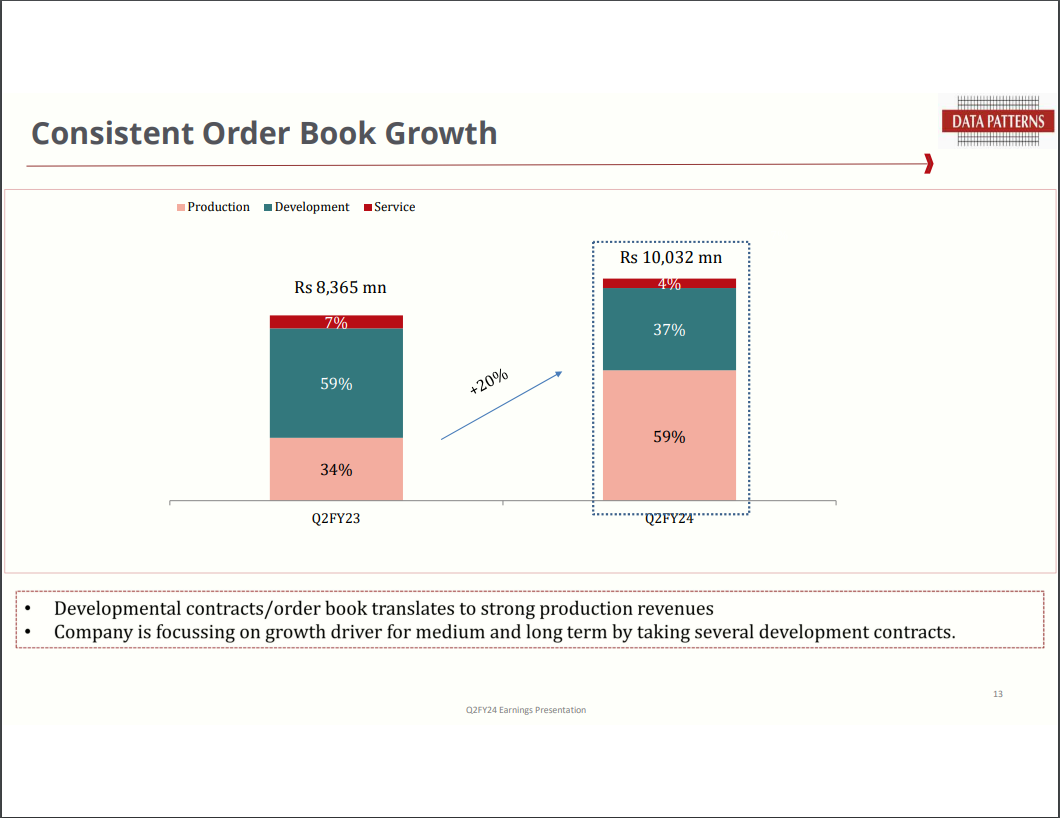

The company has had tough time in growing its revenue for last few quarters. Orderbook (which is a leading indicator) has largely remained flat over the last 4-6 quarters while other companies in the sector are seeing continuous increase. Further, 50%+ of the current orderbook is developmental orderbook which usually has much longer delivery timelines.

While the current price levels look interesting, wondering if the company has the ability to leverage sectoral tailwinds and keep growing faster than the market.