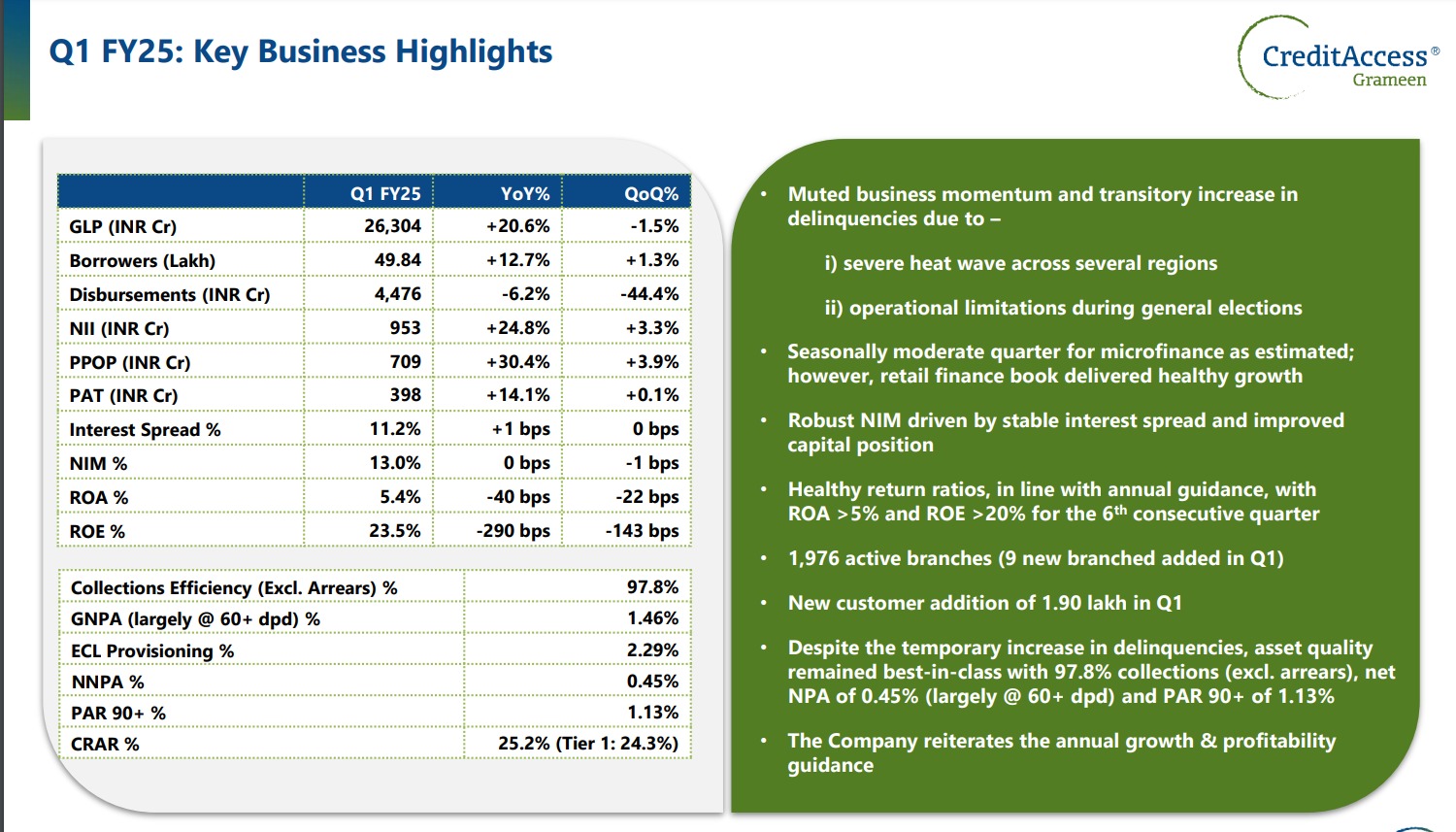

Weak Q1FY25 print on the back of muted disbursements, y-o-y degrowth of 6.6% and increase in gross non-performing assets by 56 basis points to 1.46%.

Management sounded optimistic of its full year guidance despite Q1 weakness, however, it remains to be seen how growth picks up in the coming quarters.

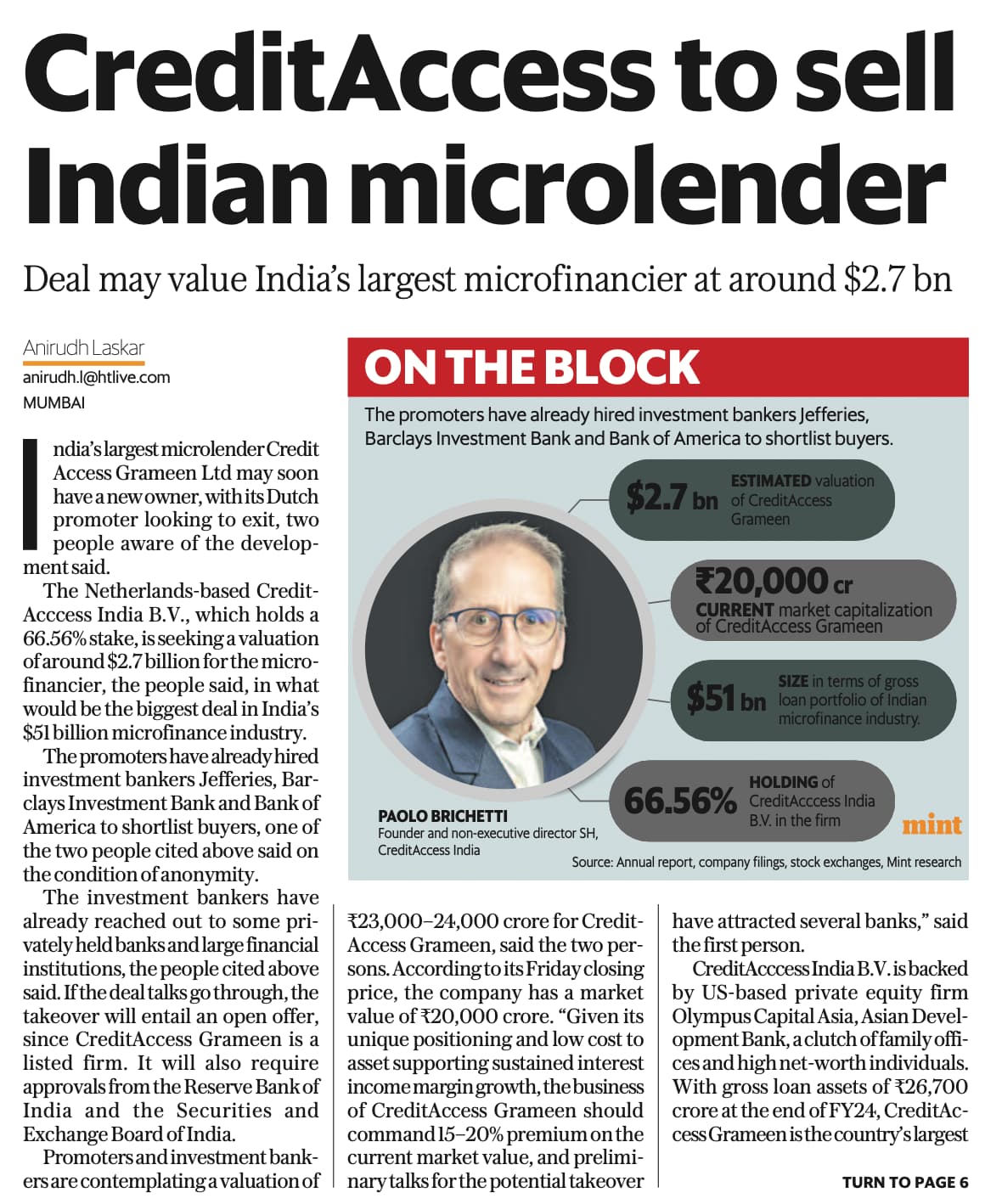

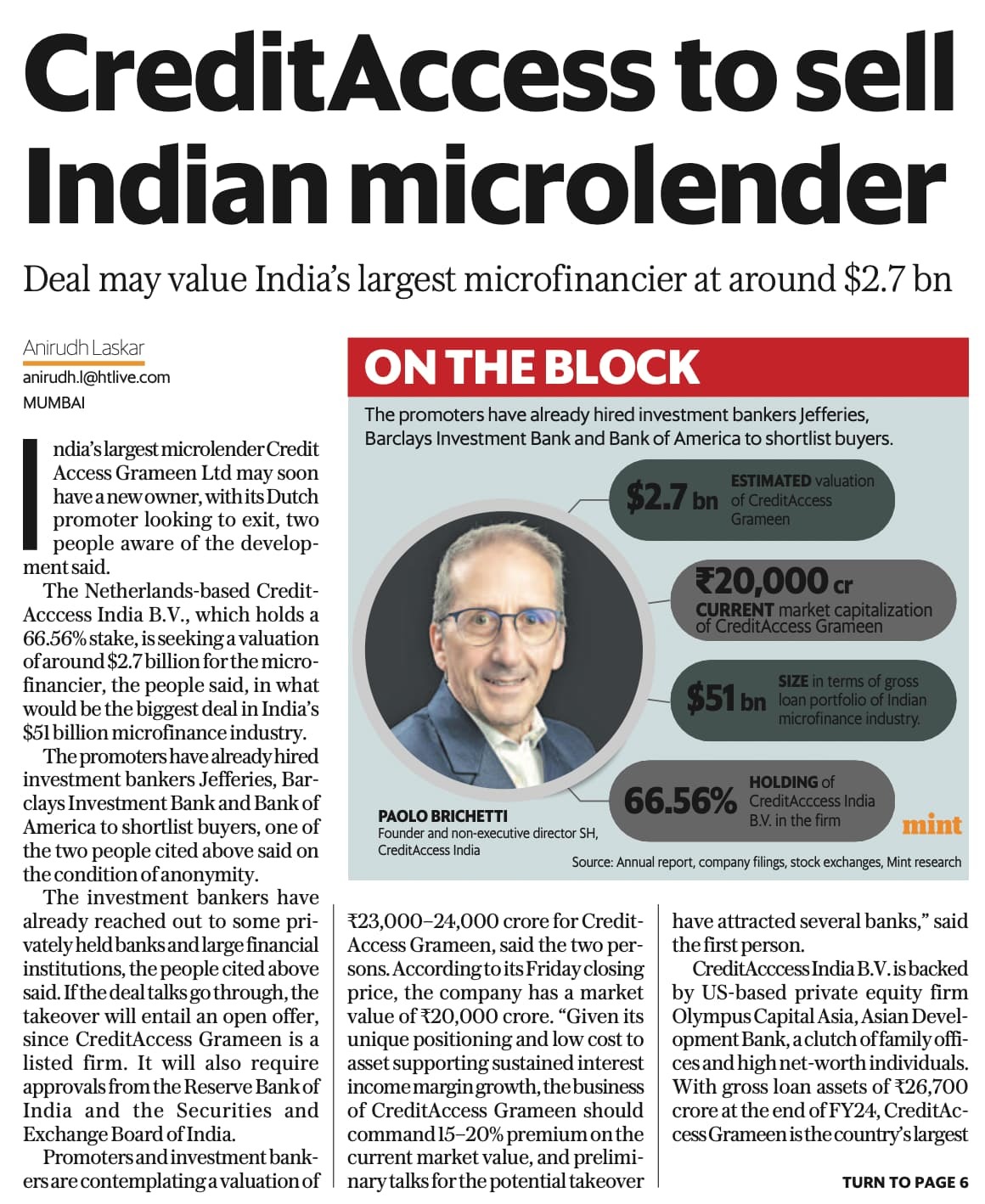

Trying to make sense of recent news, whether the owner exit will be a overhang wrt valuations and becomes a value trap in near term.

As per fundamentals, the stock is available at a best bargain since COVID times. So, it is still attractive from that POV.

As per the owner exit / change, I am trying to build the best and worst case scenarios.

Best case scenario is if is bought by another prominent player with more funds and more reach. Worst case scenario is to be bought over by a player with poor track record of governance / asset quality management. Neutral scenario is to go with status quo.

We can take the owner’s expectation of 15-20% premium as a baseline return in a year’s time.

Contrary to certain media reports, the company has refuted the speculations of a stake sale by the promoter. Currently, the promoter entity of CAGrameen is CreditAccess India, which was an outcome of the vertical demerger at the parent company level.

Sale or No Sale Does Not Matter

Company has proven it’s mettle .

Good Management, Good Operations.

Then Micro Finance has it’s own set of Problems.

Recent Heavy Rains in parts of Tamilnadu, Gujarat, Rajasthan, MP will hit them in Short Term.

I am expecting Bumpy ride

CreditAccess Grameen is looking attractive after the recent sell-off for a few reasons:

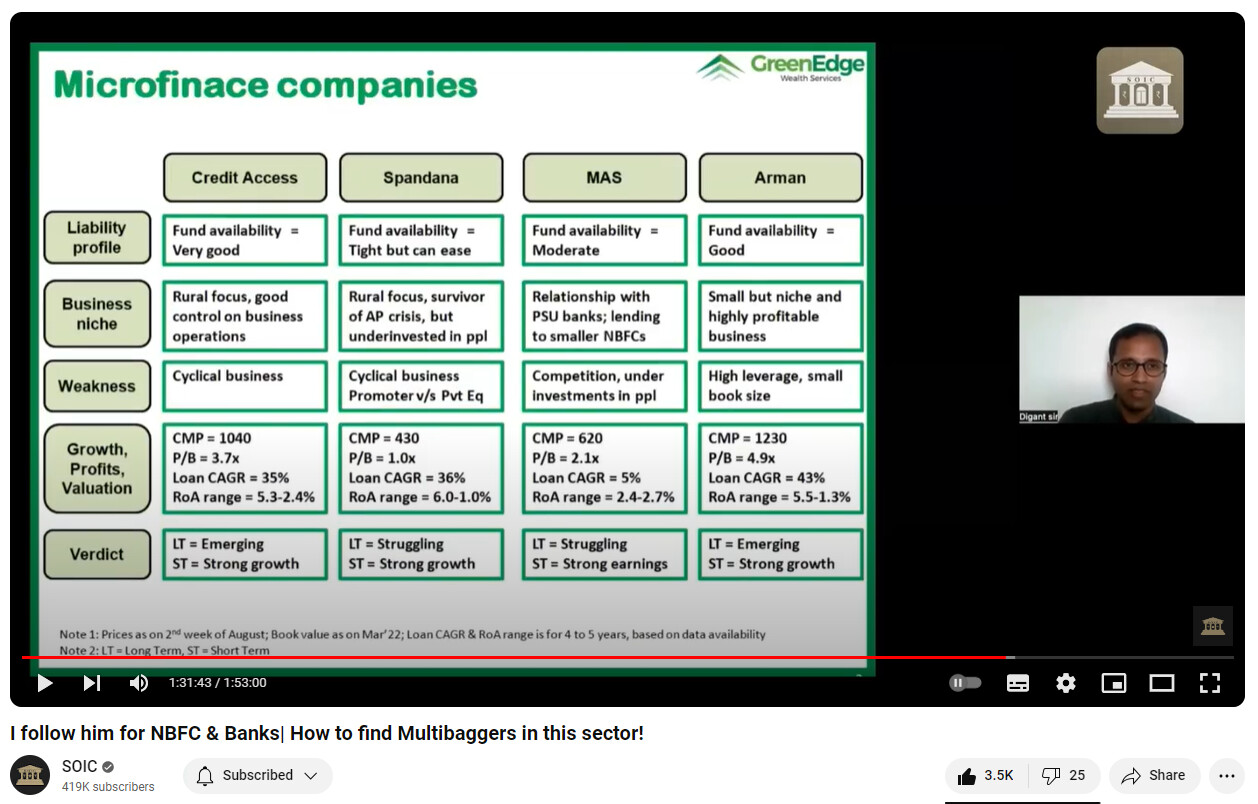

Largest amongst the NBFC micro-finance cos. with 5M+ customers across 16 states; They’ve developed the largest network and knowledge within the rural lending space

Growing at 20% CAGR; this is bound to slow down in the future, but there is still a lot of room to grow and I also expect them to increase their market share due to their best-in-class interest rates

Financially conservative; NIM of 13%, ROE of 23.5% and CRAR of 25.2%

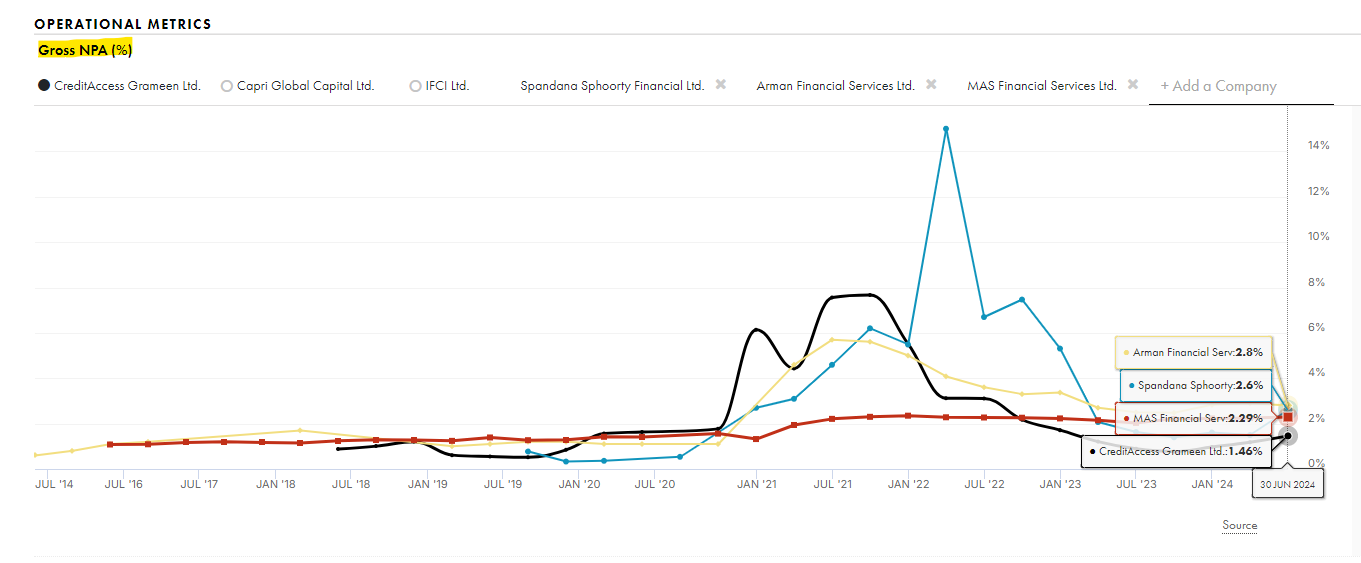

Seem to be lending conservatively as well: GNPA of 1.46% and NNPA of 0.45%. However, this could shoot up in case of economic distress (GNPA went to 7.6% during COVID)

Current PE of 10 & earnings yield of 9%+

Paolo Bruchetti, a Dutch national, is the prompter with 66% ownership. Both him and the current management team have a long track record of successful growth and zero frauds that I could find

Microfinance industry will exist and thrive for the next few decades, as there is still a large percentage of the population that doesn’t have access to traditional banking products or wouldn’t be able to get approved for low interest loans

One of the reasons that the stock has dropped is the concerns over their promoter selling off their stake. However, the promoter is not involved in day-to-day operations even today, so I don’t expect any major changes to management team or company culture.

I didn’t find any obvious red flags, so seems like a great long-term opportunity. Please let me know if I missed any major points.

Valuation wise, stock has corrected to lowest historical levels - 2P/B at around 900levels.

Hopefully that’s the bottom, but nonetheless a good price to invest for the long term (2+years)

The current MFI stress should get resolved in 1-2 quarters and the company will resume on its growth path.

Let see how the next quarter results plays out especially on npa front. This quarter gnpa is less than Arman financial gnpa. Stock price plummeted a lot but still it has higher P/B in comparison to Arman due to lower gnpa.

Prof. Sanjay Bakshi recently mentioned the micro-lending industry in an interview:

"Let’s take the example of what is happening in the micro-lending industry right now. There are a lot of regulatory actions which have resulted in a market-wide selloff in the micro-lending business. But if you look at the history of the micro-lending industry, it has grown and grown over the years. The strong players keep getting better and better and more profitable over time. The weak players or the aggressive players will get dropped out of the game.

But that’s not how the markets are treating the stocks of all the companies in that particular industry. Everything gets sold off the moment you start looking at it from a parimutuel point of view and you start thinking, ‘Well, you know, there is a downturn, but this downturn will actually remove some of the bad practices that are being followed in the micro-lending business.’

Whatever RBI is doing is actually a good thing by stopping all the aggressive lending practices that are being done. Therefore, the more conservative players, the more well-financed players, the more well-run players are going to be better off in the long run. But the stocks are still down. In fact, they have fallen almost as much as the stocks of other ones. So that gives you an opportunity. So that is the lesson that I want to leave the investor: think about the market as a parimutuel system."

Based on my research, CreditAccess Grameen is the strongest player in Indian microfinance (lowest interest rates, efficiently run, healthy capital adequacy and funding). It seems to be following Charlie Munger’s “Win-Win-Win” model.

Are there any other micro-lenders in India that are better quality than CreditAccess Grameen considering the long-term runway (5~10 years+)?

Target cut announcement and fund raising on the same day. what a co-incident! I have brought around 867 levels and planned to buy more on this levels, but Target by Goldman sacs to 564 is somehow fearing me.

One thing, I always remember in tough time is that ‘uncertain time gives chances to buy things at throwaway prices. Certainty in business always brings higher cost associated with it.’

Will look forward to deploy more cash near to Q3 results. Time correction, price correction and uncertainty are the price which one has to pay to create long term wealth. I may be completely wrong or right, future might tell me otherwise.

When the big players want to buy these brokerages give sell call downgrade call and vice versa. I have seen this in KPIT Technology. I also bought my first tranche of investment into a mfi bucket yesterday starting with CAG. I intend to buy CAG, Arman Finance and Muthoot Microfinance slowly.

Planning on bottom phishing at these low valuations ? I would suggest one to listen to Mr Digant Haria’s interview on the MFI cycle.

Will we see further reduction of book value in Q4 results due to increased write offs in Q3 and Q4? No one knows.

You think market doesn’t know that? Market started derating the sector back in Mid 2023 when nobody was suspecting a thing.

Disclosure: have a small allocation in CAG.

If starting H2 FY25-26, we can see green shoots, can we say that by the virtue of the market being 6 month forward looking, by Feb/March, we can expect good uptick in the stock price from here?

Very high accelerated provisioning made by management in excess of 180+ dpd of (around 250 crores). As per management this will also cover the NPA that is going to happen in next 2 quarter.

Just went through the results. The increase in GNPA (3.99% currently vs. 2.44% in last quarter) and increased ECL provisions (5.07% vs. 3.52%) seems to be due to tighter underwriting norms mandated by MFIN & RBI. I think this should lead to lower defaults in the long term, benefitting CreditAccess, as they avoid lending to high-risk borrowers. The next few quarters might have volatility , because GNPA will probably increase, but the management expects asset quality to normalize after Q1~Q2 FY26. Still seems to be a good long-term prospect at current prices.