CreditAccess Grameen

The VP forum has multiple threads for MFIs and players operating in the MFI domain, however post the acquisition of the MFIs by banks or transitioning of the erstwhile MFIs into Small Finance Banks (SFBs)/Universal Banks, I wasn’t able to find a thread for the biggest NBFC-MFI operating in India i.e. CreditAccess Grameen. There are other listed NBFC-MFIs (Satin CreditCare and Spandana) however CreditAccess Grameen/Grameen Koota (referred to as GK or CAG hereon) operates a far superior business vis-à-vis the other MFIs.

In order to analyse the business, I have gone with the approach of understanding the business and its functioning and post that only arriving at the financial performance analysis, so that at least I am able to figure out what’s driving the financial performance before presenting the numbers.

Some glossary/key words used in the post:

- CRE: Customer Relationship Executive - This is the person who performs the front-line operations of sourcing of customers, formation of group, doing the collections as part of the group meetings

- GLP: Gross Loan Portfolio - This is the total loan outstanding that the MFI is handling. It can include loans on the MFI’s own balance sheet, loans securitised by the MFI to bankers or other NBFCs, as well as direct assingment/BC portfolio

- DPD: Days Past Due - This means how many days is the loan EMI past its repayment date. i.e. if the loan EMI is expected to be paid of 1st of March and the customer hasn’t paid the loan till 15th March then the loan becomes DPD 15

- PAR: Portfolio At Risk - This is the sum total of the GLP for which on-time repayments have not been received by the MFI. This is similar to DPD. So if a MFI says PAR 30+ is 50 Cr and 2% of portfolio then it means Rs. 50 Crore of loans are overdue for more than 30 days and is 2% of GLP

- Case Load: Number of clients handled per CRE. Higher the case load, the better it is from productivity perspective

- JLG Loans: Joint Liability Group loans are unsecured loans which are disbursed to a group of borrowers, where apart from the borrower’s ability to pay the social pressure of the group incentivizes the customer to pay back the loan. While the loans are disbursed to and used individually, the liability of repayment is on the group.

- Background of GK’s promoter:

- GK, was incorporated in 1991 as Sanni Collection Private Limited and before turning into a NBFC-MFI it was already engaged in the business of providing micro-loans in Karnataka.

- Post the AP-crisis, the company obtained the NBFC-MFI license from the RBI in Jul,2013 and was called Grameen Koota.

- In 2014, CreditAccess Asia N.V (“CAA is primarily engaged in providing, through controlled companies, financial services to micro and small businesses and self-employed people in emerging countries. CAA also participates in, finances or conducts the management of other companies or enterprises. Presently, CAA has investments in micro-finance institutions in India, Vietnam, Indonesia and the Philippines.”) as part of the acquisition, GK was rebranded as CreditAccess Grameen (“CAG”)

- As part of the transaction CAA acquired 99% of the stake in the company and post the IPO hold 80% in the company (therefore within the next 2 years there is a 5% dilution that CAA will have to do in GK).

Main Point: GK has international parentage of promoters who are focused on providing micro-credit internationally, hold majority of the shareholding and therefore their interest should largely be aligned with the interest of the shareholders.

- Industry:

As there is a parallel thread going on the MFI industry, I am not covering the details of the industry, its size and future potential (refer here: Link).

• The key latest information about the Microfinance and MFI industry are below (as of Q3 FY 20):

o Size: Rs. 2.11 Lakh Crore

-

DPD 180+: Rs. 2900 Crore

-

Active Loan Accounts: 10.11 Crore

-

Avg. Outstanding per customer (Avg. O/S): Rs. Industry: 20,870, NBFC-MFI: 18,100

-

Composition of lenders: Banks ~40%, NBFC-MFI 31.3%, SFBs: 17.6%, NBFC: 10.2%

-

Borrowers by Geography Volume | Value: East & NE: 36% | 40%, South: 27.5% | 28%, West: 15% | 14%, North: 13% | 11%, Central: 8.5% | 7.6%

-

Borrower by end-use: Agri & Allied: 57%, Trade & service: 32%, Manufacturing: 7%, Household Finance: 4%

-

Pricing for large MFI (Portfolio > 500 Cr.):

- Median Cost of Funds: 12.6%

- Median Lending Rate: 22%

- Spread: 9.4% against RBI’s permissible cap of 10%

- Productivity (for large MFIs):

- GLP per CRE: 1 Crore

- CRE per branch: 5.2

- GLP per Branch: 5.2

- Customer per CRE: 448

- Urban Rural Mix: 46% Urban, 54% Rural

Main Point:

• Microfinance industry is a large industry, however is being competed strongly by the banking sector through organic business (majorly PSBs due to their last mile infrastructure), inorganic business (acquisition of BFIL by IndusInd, BSS by Kotak, Gramal by IDFC), MFIs turning into SFBs.

• SFBs typically operate more in urban areas than rural areas (past MFIN data showed urban portfolio having higher %, however post transition of MFIs into SFBs, the rural % increased, therefore indirectly pointing to SFB turned MFIs focusing on urban areas)

• Risks:

- Industry is exposed to agri & allied (usual political loan waivers don’t cover MFIs, therefore risk is not from loan waivers, but more from floods and droughts),

-

informal industry: GST & formalization may bring stress among the customer; however the target customers for MFIs are more centered on intra-village businesses, (my assumption/bias no data point for this)

-

like any MFI loans, these loans are unsecured in nature

- CAG’s product and modus operandi:

At a broad level, the product offered by GK to its customer is similar to what the competition offers, i.e.

- Joint Liability Group (JLG) loans for one year and two year (comprising min 85% of the portfolio)

- Group meeting led repayment methodology

- Branch/operationally heavy last mile delivery of financial services

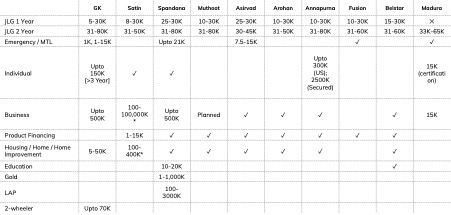

- Refer screenshot below for the comparison of the MFI products offered by the top 10 MFIs (ex-Samasta and Svatantra since they don’t publish their annual reports on their website)

- Follows the same Compulsory Group Training (CRT) and Group Recognition Training (GRT) of the CRE performing the CRT for 5 days and the Branch/Area Manager doing the GRT, and visiting customer premises before approving the group formation and then loans are disbursed.

Main difference(s) in the modus-operandi: - Instead of doing cycle based loans, where loan is taken for a cycle and only a mid-term or emergency loan is given, GK provides a line of credit to the customers, wherein customers can avail loans against this limit any time, however as a risk management practice before any loan disbursal they perform the mandatory checks of over-exposure, multiple lenders etc.

- Customer has the choice with respect to the amount of loan required, period for which the loan is required, repayment frequency. Therefore within a group the following differences can occur:

- The loan amount can differ across members of the group

- The interest rate among the members also differs based on their vintage of relationship with GK as well as other parameters, such as repayment behavior as well as the center’s vintage with GK

- The repayment frequency is decided by the customer, however the meeting happens on a weekly basis. This allows the customers to align their repayment frequency with their cashflows. Current repayment mix: 55.5% weekly, 38.3% bi-weekly, 6.1% monthly

- Benefit of such methodology: The loan product is customized to each customer’s behavior, vis-à-vis other lender’s approach of pushing their product prototype thus leading to customer satisfaction

Other products:

- As an NBFC-MFI, 85% of the products have to be JLG, and therefore the MFIs have an option to expand into other products and slowly and steadily majority of the MFIs especially the larger ones are have done so.

- GK also in the same way has also expanded its product offerings which provides GK the following benefits:

- Customers who mature across the loan cycles and have higher loan requirements can avail these loans and not be restricted by the MFIN/RBI guidelines, thus the customer is retained within the GK ecosystem

- GK is able to charge higher interest rates from the customer as the ticket size is higher and is not restricted by the 10% margin cap

Following is the product offerings of the top MFIs, along with the ticket sizes (as disclosed by the MFIs)

Non JLG product strategy: As mentioned earlier, GK has started offering the non-JLG products to its existing customers (internally referred by GK as “Retail Finance”). In order to provide these products to its customer while not directly cannibalising the JLG business it has defined an eligibility criteria [atleast three year customer of GK with good repayment behaviour], and GK understands that the CRE for JLG customer is different from individual loans, and therefore has created a separate sales channel. The details of the progress of the product is mentioned below:

Product & Performance

• Upto Rs. 5 Lakhs, upto 5 years with 20-22%

• Avg. O/S: 66K with Avg. Ticket Size: 90K

• 100% Monthly collection

• Retail Finance Product up from 3.3% of GLP to 5.1% YoY

• GNPA: 0.24%

Retail Financing Channel

• Branches: 70

• Employee: 1100, CRE: 695

• Portfolio per branch: 6.5 Cr

• Portfolio per CRE: 0.7 Cr

• Borrower per CRE: 96

- GK’s business performance vs peers:

A. Higher GLP per CRE through customer retention

The table below summarizes the different productivity metrics of the MFIs as being considered important by the MFIs. As can be seen clearly GK has been able to manage a higher GLP per CRE through a higher outstanding per client, rather than the approach followed by other MFIs of pushing a higher case load per CRE to achieve a higher GLP per CRE.

This higher outstanding is being driven by higher customer retention, as higher retention enables GK to disburse higher loans, and as per my understanding of the industry, the retention rates are the highest in the industry (BFIL retention rate ~ 80%).

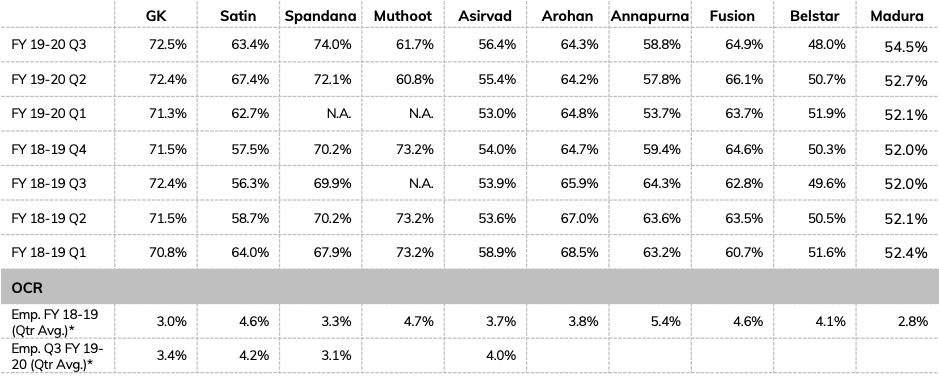

B. Lower OCR through higher productivity

As MFI’s NIM on the JLG product is regulated by RBI, the critical metric that is tracked by the MFIs is the Operating Cost Ratio (Opex/Gross Loan Portfolio). With respect to OCR, GK has been able to establish industry leading standards of the lowest OCR of 5%. Refer the table below for the comparison of business performance of GK vs other MFIs along with the OCR performance.

The higher productivity combined with higher customer retention has enabled GK to maintain the industry leading OCR inspite of having one of the higher rural portfolio (which are characterized by longer distances, lower population density and lower customer loan ticket demands).

Given the situation in Assam, one might question if loans are being pushed by GK rather than becoming the largest lender to the customer by choice. The following metrics may be crucial to allay the concerns:

• The MFIN guidelines of not providing more than 80K of loans to a customer, not lending to a customer who has loans from two MFIs and one Bank is applicable on NBFC-MFIs and not on banks, (eg. Bandhan Bank, now IndusInd with BFIL acquisition), therefore chances of over-lending to customers by GK is lower

• GK’s ability to retain customers (through the product customisations mentioned earlier), enables it to increase the ticket size over period to customer’s who have a good repayment history (table repeated for reference)

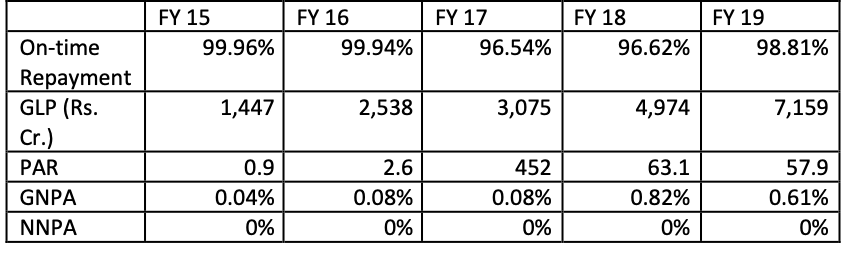

C. On-time repayments and NPAs

NOTE: FY 17 spike is due to demonetization and FY 18 onwards spike is attributable to transition of the company to IND-AS from the earlier I-GAAP.

Even with a faster growth in the overall portfolio the PAR number has grown slowly reflecting management’s ability to grow the loan book in a quality manner while not sacrificing on the growth either.

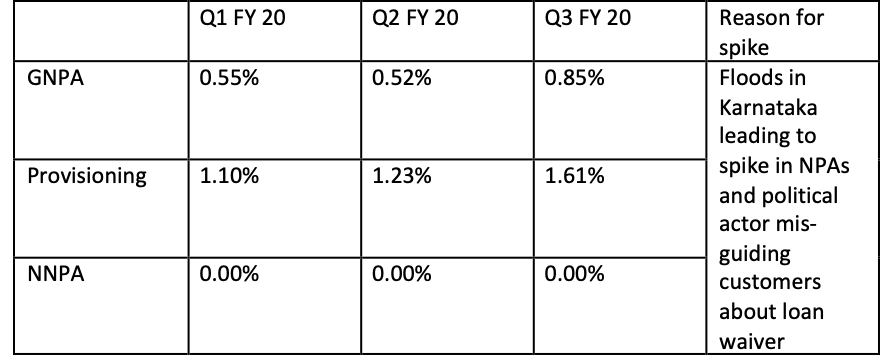

Recent Performance:

The management has been conservative with respect to making provisions, while at the same time not sacrificing on the quality of the loan book

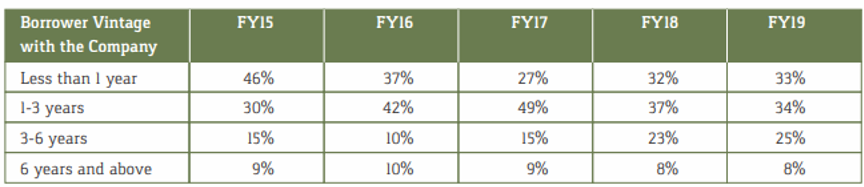

D. ONE AREA WHERE GK LAGS Bandhan Bank: Customer vintage with GK vis-à-vis Bandhan Bank

As per Bandhan Bank’s management commentary [Bandhan taken as reference coz it’s the listed MFI with large exposure to the troubled state of Assam]

“But first three cycles we are very conservative, our retention rate, dropout rate is high in first three cycles, so we are divided in that way. So, if I come to on that point, our 55% of the customer which is more than three cycle with us, and their average alone outstanding is Rs. 49,358 rupees, so those are with us. Average if you say that, out of 18 years 3 years, you divide 15 years, seven and eight years average these people are with us. But if I go to these the other customers who are not with a very much as the latest coming on that, and they are coming on that with 45%, their average is Rs. 29,000 rupees on that.“ Link

Vs. GK’s vintage composition of the customers

However Bandhan’s Avg. Customer outstanding is 38,190 vs GK’s 32,000 reflecting 20% lower avg. outstanding, which may point (though a weak pointer, I admit) of GK not over-leveraging the customers.

• Also, unlike other players which incentivises the last mile CREs for the case load, GLP and adherence to the processes (weightage differs from player to player), GK has delinked the incentive completely from the business performance of GLP and collections and have linked it to number of customers serviced and quality of service, thus potentially avoiding the situation of over-leveraging.

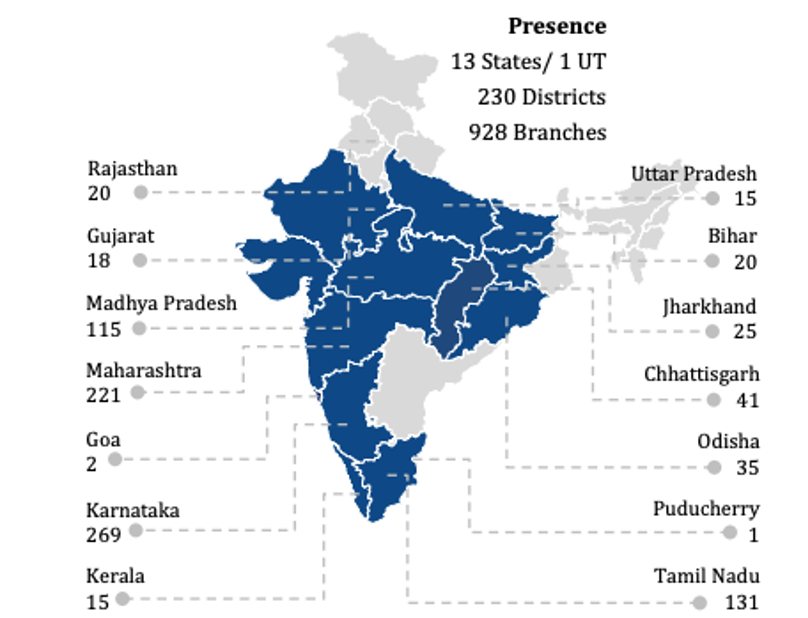

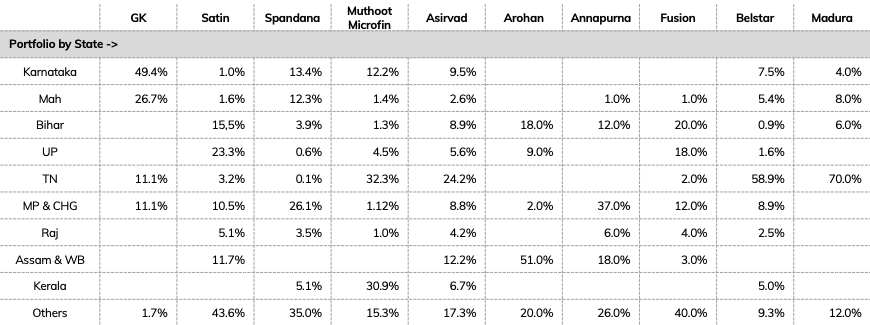

E. Pan-India Presense:

GK has followed the philosophy of expanding its business operations through contiguous districts, while avoiding the bad districts which have bad repayment history. The strategy has enabled GK to:

• build deeper penetration in each of the respective state of operations, rather than just expanding every where,

• contiguous expansion also provides the advantage of the CREs of not facing a major cultural or language change

Through this approach, GK has been able to expand into 230 districts in India, with presense in 13 states and one UT, through a network of ~930 branches.

While GK has established presence in multiple states and districts, the business is primarily coming from the five states of Kar, Mah, Tamil Nadu, MP and Chg which is primarily driven due to vintage of operations in the states. As GK expands into multiple other states, the loan book is expected to further diversify.

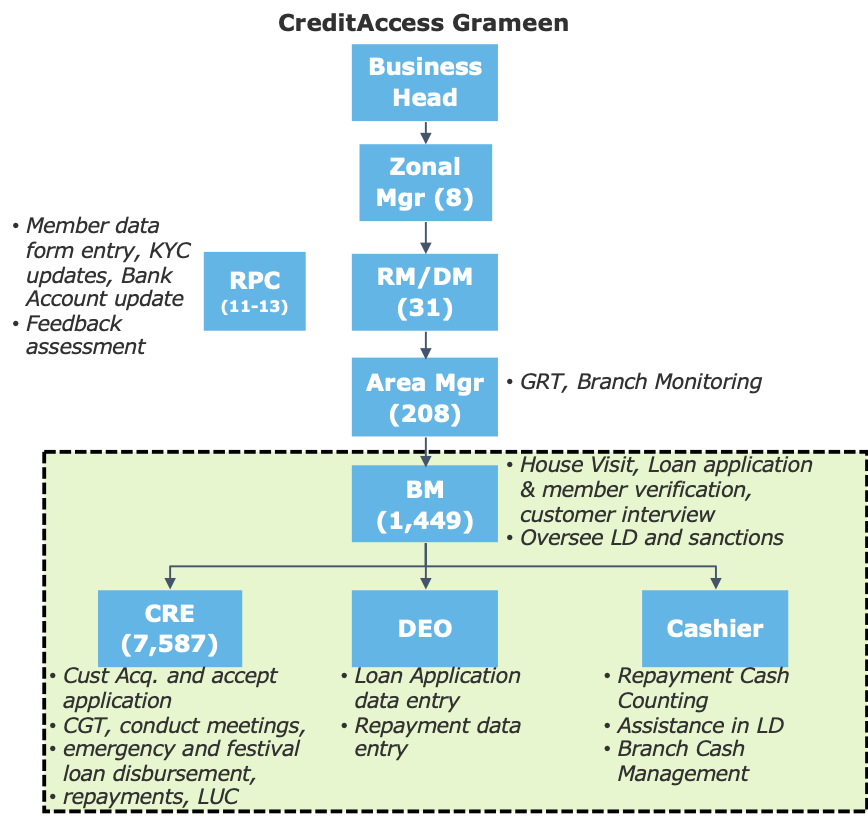

F. Higher Productive Employees vs Managerial employee:

GK has been able to consistently increase its CRE headcount, which has provided it with the following advantages:

- CREs are lower cost employees, therefore higher the % lower is the avg. employee costs

- CREs are the resources which sources business for all the MFIs, and therefore higher the number reflects higher revenue possibilities

From the table below, it can be seen that there is a very strong co-relation between the CRE headcount to the overall employee level OCR for the MFIs.

In order to realize such a larger % of CRE headcount, the operating model for a branch has been analysed to understand what provides GK the ability to support such a large employee base with limited managerial headcount (text in italics is the R&R of the people in the respective roles).

Through investments in process optimization, removal of inefficiencies, technology (has Temenos 24 as the core banking system for loan management), centralization, GK has been able to make its CREs more productive and removed the administrative activities from the managerial personnel R&R thus making them also more productive.

Extract from management commentary:

*“*Regional Processing Centers help to improve controls in the following manner:

1) Check data entry of newly enrolled customers;

2) Improve and maintain integrity in data quality;

3) Independent data entry of new customers;

4) Ensure complete and proper documentation”

“Our Regional Processing Centers have not only improved our operational efficiencies allowing our field staff to focus more on actual business workstreams but have also significantly improved the data quality of our Customers’ information.”

- Management:

a) MD & CEO: Udaya Kumar Hebbar is the MD & CEO of the Company. He is a certificated associate from the Indian Institute of Bankers and holds a diploma from Vanderbilt University. He has served as the head, commercial and banking operations at Barclays Bank PLC, Mumbai for three years. He also served at Corporation Bank for a period of over ten years. He was also associated with ICICI Bank for over eleven years. He joined GK in 2010.

b) CFO (Diwakar B.R.): He has 20 years of experience in the financial services sector. Prior to joining GK, he worked with Small Industries Development Bank of India, as Chief Manager at ICICI Bank Limited and as Commercial Supervisor at ACCION International. He was also associated with Life Insurance Corporation of India and IFMR Capital Finance Private Limited. Diwakar B.R. joined our Company on October 30, 2011.

c) Risk, Gururaj Kumar KS Rao is Senior Vice President, Risk. He holds a bachelor’s degree in commerce from Bangalore University and is a certified internal auditor from the Institute of Internal Auditors. He has 14 years of experience in the area of auditing. Prior to joining our Company, he was associated with Yusuf Bin Ahmed Kanoo W.L.L and Mallya Hospital, Bangalore. Gururaj Kumar KS Rao joined our Company on July 1, 2009. He was appointed as a Key Management Personnel on July 1, 2013.

d) VP Strategy & Planning: (Anshul Sharan) He holds a bachelor’s degree of technology in metallurgical engineering and materials science from the Indian Institute of Technology Bombay and a post graduate diploma in management from the Indian Institute of Management Indore. Prior to joining our Company, he was associated with Reliance Power Transmission Limited, Kanbay Software (India) Private Limited and INDXX Capital Management Services Private Limited. Anshul Sharan joined our Company on July 13, 2012.

e) VP Technology: (Arun Kumar B) is the Vice President He holds a bachelor’s degree of technology in textile technology from Allagappa College of Technology, Guindy, Chennai and a post graduate diploma in management from the Indian Institute of Management, Indore. Prior to joining our Company, he was associated with Infosys Technologies Limited and Barclays Bank PLC. Arun Kumar B joined our Company on November 10, 2010. He was appointed as a Key Management Personnel on April 1, 2014.

f) Operations:

a. Gopal Reddy A R is Vice President, Operations (Maharashtra, Madhya Pradesh and Chhattisgarh) of GK. He holds a bachelor’s degree in commerce from Bangalore University. He has over 15 years of experience in microfinance operations. Gopal Reddy A R joined our Company on May 30, 1999 and was employed with GK untill December 31, 2011. He later rejoined our Company on April 10, 2012.

b. Srivatsa HN is the Vice President, Operations (Karnataka and Tamil Nadu) of GK. He holds a pre-university certificate issued by the Education Department, Government of Karnataka. Srivatsa HN joined GK on December 13, 2002. He was appointed as a Key Management Personnel on April 1, 2014.

Main Point:

• The management has over 15 years experience at the minimum at the leadership level, with the CEO and CFO having over 20 years of experience, which implies that the management has seen many of the economic cycles

• They have been with GK for over 10 years, which means that they have atleast seen two tough economic downturns of 2009 recession, demonetization

• Management continuity: The management has been with the company for over 10 years which means that they know the business in & out

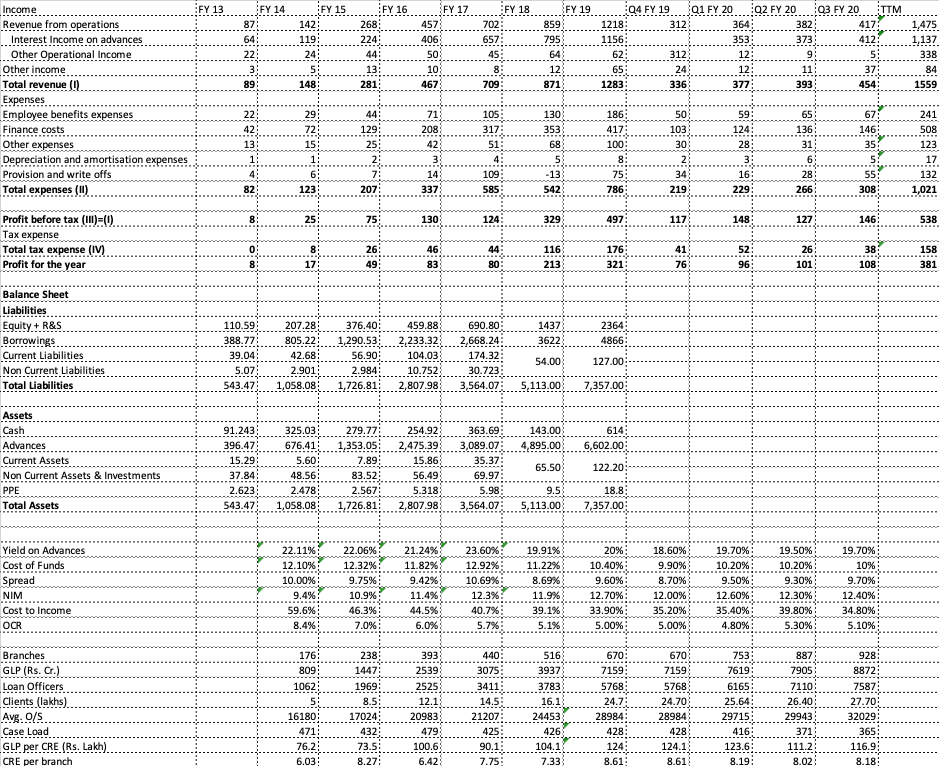

- CAG’s business performance:

Balance Sheet, P&L and Key Business Metrics

For the editable of the above excel refer Link

From the above table, observe the following key trends:

- Case Load has been coming down over a period and Avg. O/S standing has been consistently growing → Business transitioning from commodity MFI business to a differentiated one

- CRE per branch has been increasing inspite of higher branch expansion → Penetration within the geographical coverage of a branch

- OCR and Cost to Income has been steadily reducing, inspite of expansion → Strong control on costs, supported by higher GLP per branch

- NIM has been maintained over 10% inspite of the RBI cap, reflecting contribution of non-JLG products in realising higher NIM

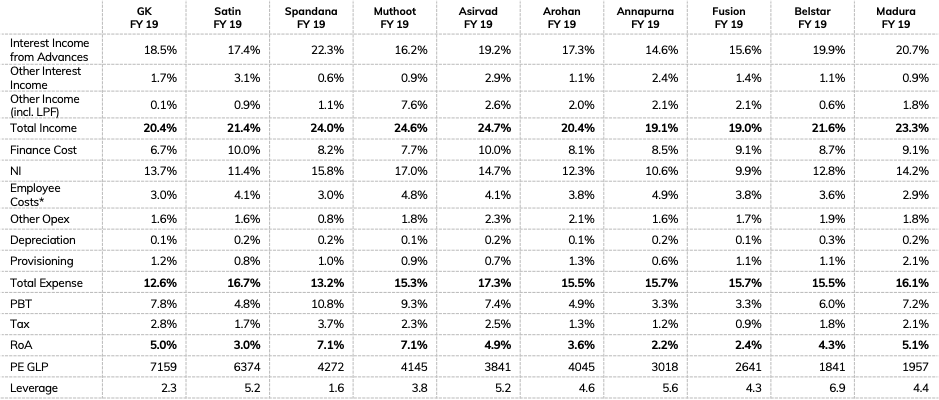

Financial Performance vs Peers (RoA Tree comparison)

From the above table, observe the following key trends:

- Lowest Employee costs driven by higher CRE headcount (as discussed earlier)

- Industry leading RoA of 5% (Spandana has a higher RoA, but enjoys the benefits of CDR therefore ignore), Muthoot’s RoA is driven by other income rather than operations therefore ignored

- Cost to income also kept in check by realizing lower other opex despite CAG following a weekly meeting model vs. fortnightly and monthly model being adopted by other players

Compliance to the 10% Margin cap

- Acquisition of Madura Microfin:

In Nov 2019, CAG announced the acquisition of Madura Microfinance and details of the transaction has been provided by CAG here.

I have not analyzed the Madura business in detail, however the metrics of Madura’s business has been provided in the above analysis, peer benchmarking. My high level hypothesis with regards to the acquisition is the following: - Madura has been a strong player in TN and tried expanding into the other geographies with limited success. The transaction therefore helps both GK and Madura as GK gets access to the high vintage customer of Madura, get presence into the states where GK has recently entered and the branch infra doubles up in Orissa and Bihar (which are one of the fastest growing MFI states), gets 2X additional branch infra in TN (which is considered one of the good states for MFI business)

- The asset is operating at similar RoA levels as GK, therefore merger is not of a distressed business (my hypothesis is that financial services business is where distress acquisition should not be done)

- NNPA are 0% therefore the bad loans have been provisioned for

Similar and other benefits of the transaction has been mentioned by the management in the presentation

Strength of business: Refer sections 3,4,5 for strengths in product, operations and costs efficiencies

Weakness/Challenges of business:

- Unsecured loan portfolio by design and regulatory requirements

- Bank’s trying to encroach into the traditional MFI customer segments/areas

- Merger of Madura Microfinance, till now GK has grown its business organically, and this is their first inorganic acquisition, ability to merge the culture, align/streamline processes will be critical

- COVID’s impact on the MFI business leading to disruption in collections and new customer acquisition

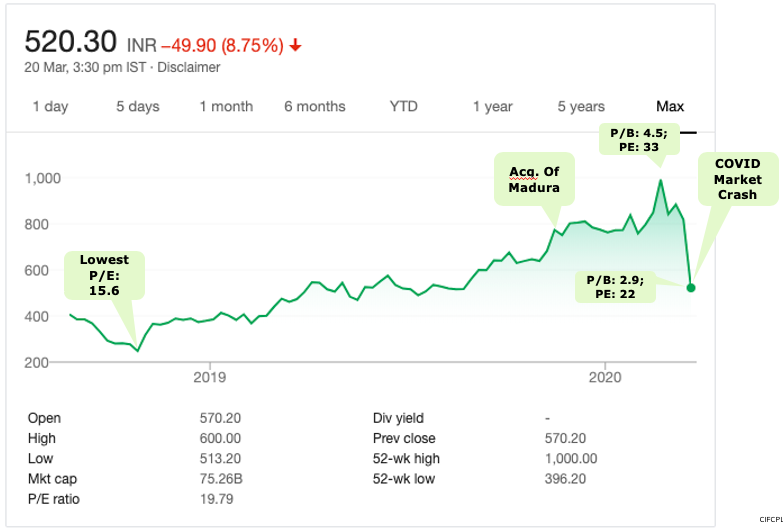

Stock Valuation and Performance:

Following is the stock chart of CAG, up until the market crash, CAG has been trading at a steep valuation, supported by superior business performance and lower NPAs, however post the market crash is it trading at price similar to mid 2019.

While I have been able to analyse the business performance, I am not able to comment on the price of the stock if its trading at an attractive valuation or not, since I am generally poor in valuing stocks but consider myself decent with respect to analyzing a business.

Views, Comments and Questions with regards to the analysis invited.

Sources: DRHP, Investor Presentations, MFIN, Annual Reports of the MFIs

Disclosures: Bought 250 shares @ price of 800, bought during the market crash