Very good results.

Madura has also joined this time. it was drag on Parent since long

1 Like

Fabulous Results.

Growing on Full Throttle.

1 Like

Is there any Change in Collection efficiency in Karnataka after regime change ?

Can someone from Karnataka check the reality at ground ?

Anyways I am holding and it’s 28% of My Portfolio

Very informative document.

Most Important information out of it after High Court verdict they are going to enter in Telangana and AP where MF penetration is less than < 1%.

Hugh Opportunity.

1 Like

Current valuations of P/B = 4x, is there much upside left here?

And

Why is promoters holding doing down. Is this secondary sale?

Update on Tax Demand for AY 2018-19

The Commissioner of Income Tax (Appeals), has vide its order dated October 17, 2023, has considered and accepted the appeal of the Company thereby effectively rejecting all the grounds on which the Income Tax Demand of ₹122.63 Crores was made against the Company for AY18-19.

3 Likes

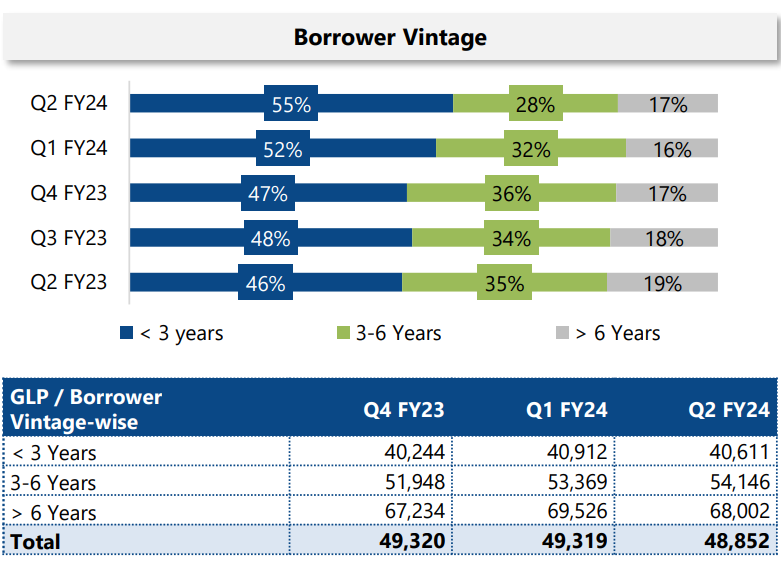

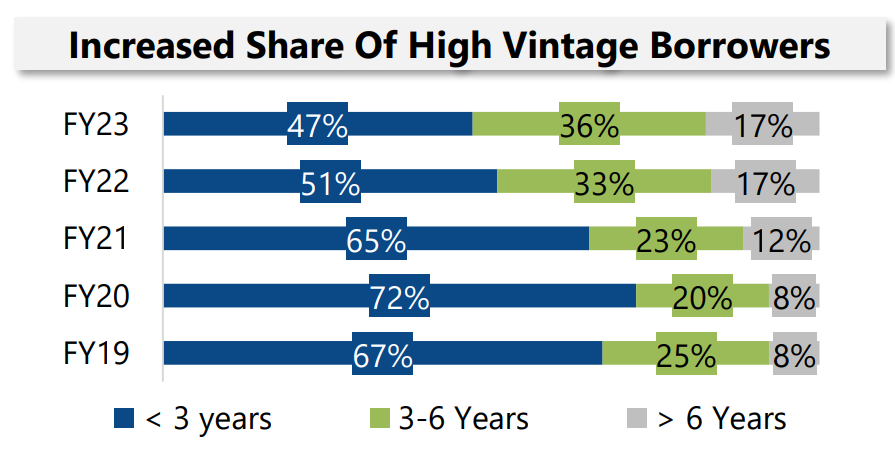

Wanted to focus on the borrower profile and how the company is scaling up to see if it is sustainable.

Some observations:

- New borrowers are being added with entry into new markets

- Some existing borrowers (3-6 years) migrate to > 6 years, which results in maintaining the ratio of > 6 years pie

- Some of existing borrowers (3-6 years) stop borrowing and churn

The GLP ratio per vintage profile shows a slightly different picture.

- The quantum of GLP for new borrowers is roughly constant in last 3 quarters

- More loans are given to existing borrowers

- GLP ratio of > 6 years is also fairly constant compared to Q4FY23.

This means that the company is issuing smaller ticket sizes compared to last year. May be because they are scaling up their home improvement loan, which has almost doubled since last year. This is also reflected in their loan ticket size, which is much smaller for home improvement compared to income generating loan (IGL).

So, all the three checks out well: Borrower vintage, GLP distribution and Loan ticket size.

The good points are:

- They are not adding risk by scaling their new customer base and associated GLP. So, seems like a sustainable growth with a tight control on NPAs (GNPA is 0.77%).

- They are also able to retain their customers better which establishes a strong & stable base

- They are scaling up home improvement, which is good as this sector is expected to grow

- Retail finance is growing fast, but has a smaller base. But this is another growth area.

Disc: Invested

5 Likes

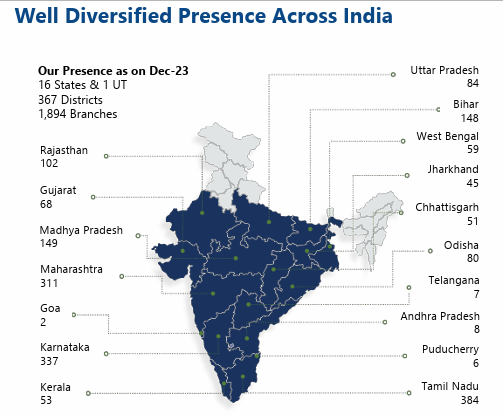

Important Takeaway for me is their entry into Telangana and Andhra Pradesh.

After SKS Fiasco these states are highly underserved, big opportunity available for Credit access.

it’s only matter of a year or 2 before these states become part of their legacy portfolio.

However they are treading cautiously.

Capturing Border districts from Maharastra,Karnatka,Tamilnadu and Odisha

Recent rating upgrade by CRISIL to AA-/Stable.

This could reduce their cost of capital by few basis points.

3 Likes

Best Small NBFC(10000-25000 Cr) Award

1 Like

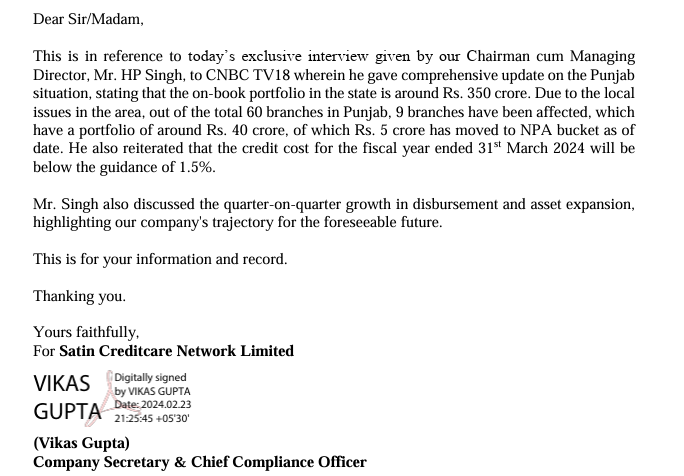

Satin is struggling in Punjab.

Any other state where there is trouble as such from Microfinance point of view.

And if Credit Access has exposure to that state ?

If not then Market Leader shall command better valuations

1 Like

Hi Guys,

I am new to the entire value investing thing and while I was scouting for stocks to invest and found out CreditAccess. However, I am confused with the recent price movement of CreditAccess.

While I understand that there is ambiguity due to RBI’s stance on NBFC and MFI, however, I felt that this stock has fallen sharply compared to other peers in the industry.

I was trying to list down possible reasons for the same:

- RBI policies [impact seen in the entire industry]

- Increasing D/E [?]

- Future guidance towards the cautious side [?]

- Increasing NPAs [?]

- Also, this industry is cyclical and we are at the cusp of a “bad cycle” now [?] …somewhere increasing NPAs would point towards that [?]

- Election uncertainty: I noticed that a few politicians are talking about loan waivers [?]

IMO, the scrip looked strong fundamentally and rudimentary DCF shows that the stock is undervalued by 20-25%. Also, whenever the fed rate cuts happen, it would have helped with the overall growth of the industry as well.

I was surprised to see a sharp correction of this stock even with good Q4’24 results.

It would be helpful if someone who has a strong understanding of MFI or tracking this stock for a longer period could present their hypothesis.

Thank You.

1 Like

Their projection till FY 28 is strong as given earlier for FY 25. They have met the guidance for last FY. Basis their track record, I fell the CAG will meet its guidance. Price correction, probably, is an opportunity to add.

Disc: Invested. Added small quantity recently during the correction

1 Like

What would be the impact of change in RBI priority sector lending norms for MFI lenders?

IMHO, it is not negative for CreditAccess in terms of creating more competition. They have one of the lowest NPAs, a very good collection efficiency and a good network in tier 2 and tier 3 regions. So far, they have been going into regions where there is not much competition. The opportunity is still huge. With the govt push, it could actually benefit CA with the customer base expanding more rapidly.

Meanwhile, it will take a long time for other players to enter and eventually hit NIMs of CA.

I find valuation of CA is now a bit more attractive than early this year. They have been growing their book value consistently without taking any hit or having any controversy.

Disc: Invested and biased. Might add a bit more.

3 Likes

Maharashtra Farm Loan Waiver demand

Uddhav Thackeray, Shiv Sena (UBT) chief and former Chief Minister of Maharashtra, has demanded a complete farm loan waiver from the Eknath Shinde government. His demand comes ahead of the state’s annual budget presentation, with expectations of financial aids for farmers.

If implemented, this could create credit behaviour indiscipline among borrowers. Would like to see how the situation evolves and impacts the MFI industry in general and CreditAccess, which has a large book in Maharasthra.

Disc: no holding, no transactions. tracking the space.

1 Like

Net Profit up by 15% at 398 crores , QoQ Flat.

credit-access.pdf (2.1 MB)

I was reading the google reviews and I see a very concerning trend at CreditAccess Gramin. They are promising the customers with an interest of 11% and after signing off, the actual loan is disbursed at 21%. The weaker section is being exploited with false promises.

disc. Invested in small quantity, recently.

Have you checked on the ground ?

Had it been following vulture practice how will they grow in rural area where word of mouth travels like wildfire. people live in close knitted communities there.

I suggest you recheck and do update if you find anything. Thanks in advance.

Credit Access is one of the Most Ethical company in the Micro Finance Industry No one come near it. They offer Micro loans at better rate than anyone else in the Market.

Results are flat: 1. Cash movement was restricted due to general elections 2. There was severe heatwave in many parts of India.

Disc: I have Invested with the company since 2021.

2 Likes