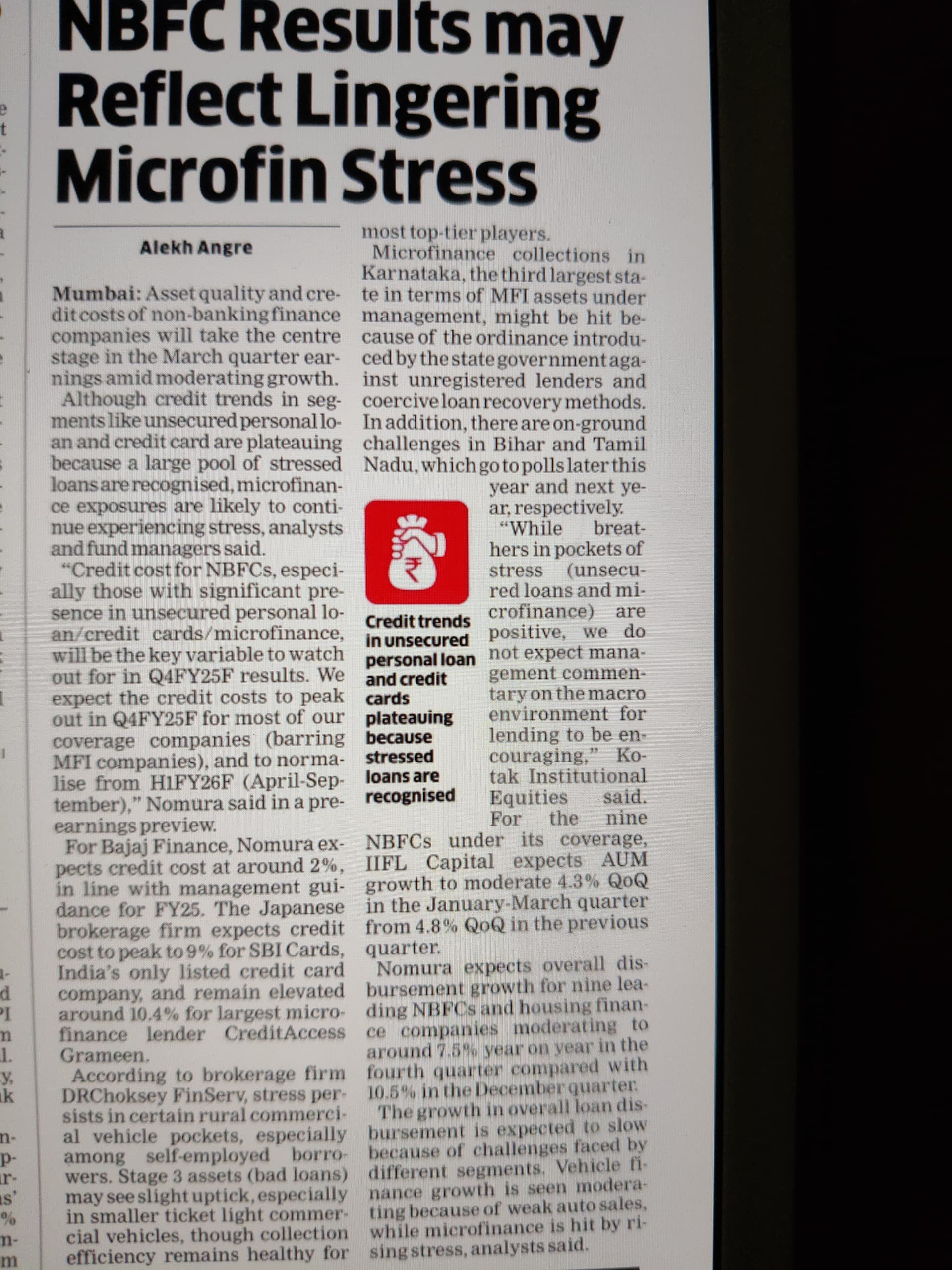

Likely to see more pain as Karnataka government going to pass ordinance on MFI company. This can increase NPA as it will stop the reportedly unethical practices followed by companies to recover their loan amount from their lenders. Karnatka constitute 10% of total MFI book of country in rough sense. Read the article.

May not be a problem for Genuine Companies like CAGrameen. Government in Karnataka wants to bring law to curb lenders who prey on borrowers. Without checking the borrower’s repay ability lenders shall not be allowed to lend. These lenders later outsource loan collection to local goons which led to some borrowers committing suicide.

CAGrameen works with borrowers to increase their income level rather than just giving loans.

In fact these suicide incident might be good for the company from Business point of view.(I feel bad writing the last line.)

considering the current scenario, we are aiming for an AUM

growth of 7%-8%, NIM of 12.8%-13.0%, credit cost of 6.7%-6.9%, ROA of 2.3%-2.4% and an

ROE of 9.5%-10.0% in FY25. The preliminary outlook for FY26 projects healthy 18%-20%

AUM growth, 4.2%-4.5% ROA and 17%-19% ROE.

More write offs coming in the following quarters. More pain ahead although this will lead to conservative lenders flourishing even more and the smaller ones get taken out of the equation..

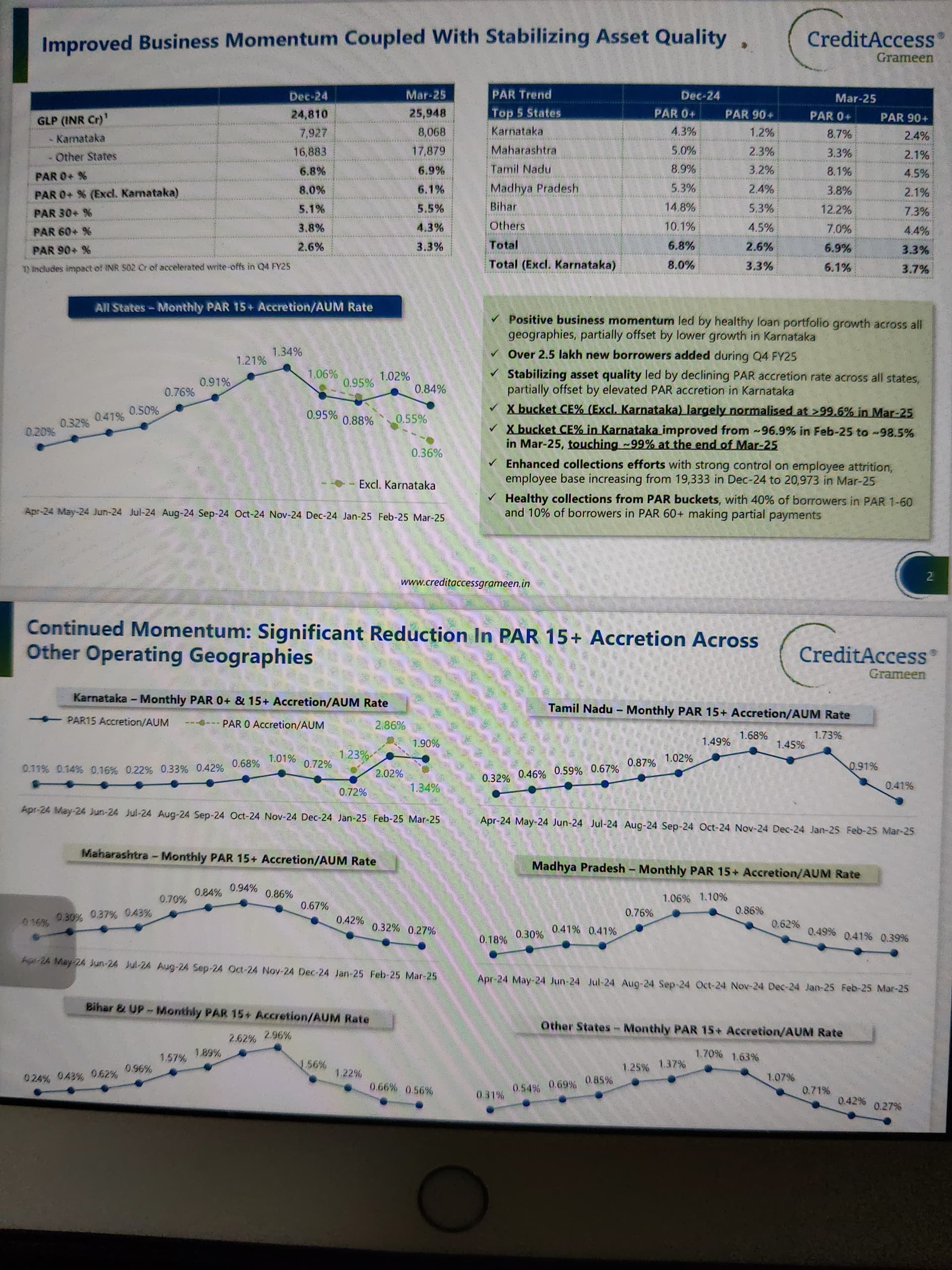

I think a PAR0 in Dec’24 would naturally lead to higher Par90 in March’25. So, the lower Par0 numbers (excluding Karnataka) in March’25 should lead to lower Par 90 (excluding karnataka) in June’25. So, the improvement in Par numbers should be reflective by next quarter rather than this quarter.