Yes lower RM prices should help increase margins to some extent. But now demand slowdown impact is difficult to estimate.

Partial reopening of operations in guj

Interview of CEO of Cosmo Films. Nothing significant information that the members of this post may not be aware of. Just sharing.

@jitenp sir your view on COSMO FILMS’S RESULT?

1 Like

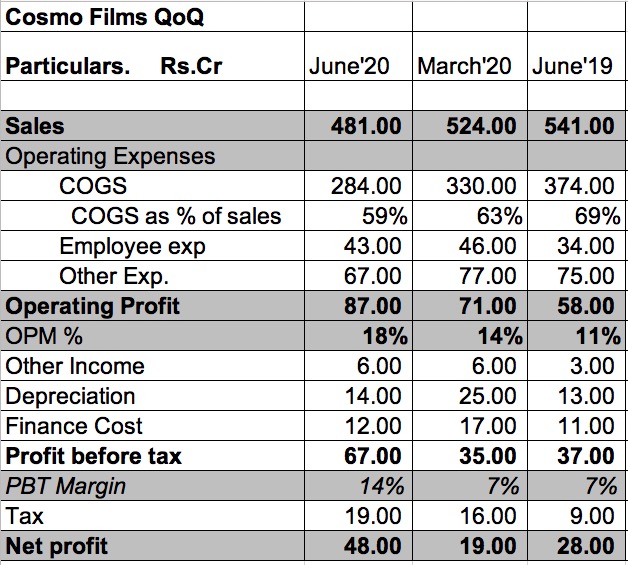

They took some one-time impairment and hence NP is down. Margins as envisaged have improved, and PBT is up smartly.

Management interview

1 Like

Quite bullish commentary from management. If there is really not much supply coming in over the next 1-2 years as stated by management, this could be a great year for Cosmo.

2 Likes

Good cycle playing out in BOPP films. Had alerted here about uptick in cycle. Demand-supply is in equilibrium and cycle can expected to be playing out further.

Packaging is one sector which has tailwinds, especially due to CoVid. As demand for packaging will increase.

BOPET cycle also playing out well. Spreads improved in both type of films.

8 Likes

Anvil wealth management has bought 100,285 shares. The company has d/e ratio of 1.05. Is there something, I am missing

First out one the valuation front - we are getiing 2,88,000 tpa capacity for an EV of 1280 cr which translates roughly to Rs 45,000 per ton. Average Gross margins per kg are Rs 15 per kg - giving us a payback of 3 years at this point. From the valuation front its easy to see the value.

Some notes from the concall

- BOPP films per kg spread has improved from Q3-15/Kg, Q4 - 23/Kg and April - 35 and May - Rs 30

- Co has cash and liquid investments of Rs 170 cr

- Dont expect more than 200k tons capacity addn in the next 2 years. Earlier China used to rule the roost in terms of capacity addn but in last 2 years it has come down a lot

- Effective interest rate for debt is 6%

- Textile demand which forms 20% of the overall demand is yet to pick up

- Incremental turnover expected from Master Batches is Rs 100cr. New line will come in a month.

- Chemical division is just beginning. Looking at 3 verticals in the speciality chemicals division - including adhesives

- No intention to become a converter and compete with customers

- Currently 3 years payback.

- Capacity utlization back to 90%

- Intent is to take Speciality business to 70% in volume terms 3 years down the line

- No credit is given to dealers and distributors. Provide very selective credit to large brands and converters

Best

Bheeshma

14 Likes

Packaging film margins have improved significantly in Q1 for both Max Ventures and SRF. Also commentary given by both for FY21 is very bullish. Expecting bumper margins from Cosmo this quarter.

5 Likes

Does Cosmo Films produce BOPET ??

They are coming up in BOPET, not yet in numbers

1 Like

No they are not. They cancelled their plans. They are only going to focus on specialty films.

1 Like

Co. posted highest ever Quarterly EBITDA of 87 Crores and stock hits ATH today!

How long will the margins sustain is to be seen?

3 Likes

Any updates on buyback record date and procedure there after. Yet not received any communication from company. Thanks in advance for any assistance.

Great Q2 results. Spectacular bottom line.

But sustainability of this may be a concern for the market (may be that is why the stock hasn’t moved up after the result). But going by the management’s views on speciality business, the perception of cyclicity of the stock should go down.

1 Like

The buy back offer came,

In the post buyback notice I see that the general category acceptance ratio = 1077256 /2872790= 37.5%

Whereas for me, only 15.8% of tendered has been accepted in buyback.

Am I missing something here?

Company has posted highest ever EBITDA of 63 crores and has announced a dividend of Rs 25 per share

97d6bc44-0fd1-4402-9c82-79fe165d0399 (1) (1).pdf (485.7 KB)

Are the margins sustainable now that raw material prices have started increasing

1 Like