The point is that it has managed debt in the past and still paid dividends. Anyways, they have no major plans for expansions currently, so deleveraging should happen in the future. This company has been able to handle cycles well. I have been tracking the company for more than a decade now.

The company is increasing share of value-added films (I still don’t like the word specialty), which have higher margins. But, I still maintain that there is a cyclicality to it, albeit it can be a reduced one.

I always try to give views on the company operations and sector. Absolutely, no buy/sell/hold recommendations on the company.

Disclosure : Holding, with no transactions in last 30 days.

CU and EBITDA margins can be good indicators of demand. Is there any other way to gauge demand better. what are the factors affecting demand? Is the current increase in demand due to better growth in their consumers or is it due to them shifting from other materials to bopp films. Can the increase in EBITDA margins be seen with the competitors too…

Iam working to find out answers to these things.

Specialty Films - tried understanding it in detail from the company when i visited their plant in December. As per the management some of their specialty films earns upto INR 50/- per kg gross margins against BOPP which had fallen to single digits last year and at about INR 14-15/- per kg in H2-2019. The reason why the company does not convert completely into a Specialty Films manufacturer is that the demand base for these products is very low right now and is developing over time. So Cosmo adds about 10000 tons of Specialty capacity every year and as per the management they plan it to be atleast 1 year ahead of the demand!

BOPP cyclical margins were exceptionally low in 2018 and whatever EBITDA they could generate were mostly on account of the specialty products. Net net my understanding is that the company continues to be cyclical but at the peak of the cycle it could generate higher margins on account of higher proportion of specialty films than what it has done historically. they will continue adding 10000 tons of specialty films every year!

management has said that actual capacity utilisation can only go upto 75% of the nameplate capacity. On tht basis company is operating at near 95% utilisation.

As mentioned by @jitenp, the co has done well to maintain its cash flows during downcycles. It has a good cash flow statement during the rough periods.

yes true, the company has said tht they plan to increase value added by 10000 tons pa and capex requirement for that is not much. Also the concery regarding debt, i had the chance to meet the cfo recently and he had indicated tht 90% of the debt is repayable within 3yrs. Also the comapny has given detailed instalments payable of each debt in the annual report.

agree but if you see last 12 years, sales have quadrupled at the same times debt also quadrupled. Fixed assets have grown by 5 times. Also, their margins have never been great. Also, all players are talking of specialty films, in addition to that industry capacity seems to more than demand.

Descl: Had invested at 330 odd levels, exited in loss during 2018.

Sir they mentioned in last call that CU is at 95%. This might me nameplate but they had mentioned once that industry usually operates as per nameplate CU. Can they operate higher than nameplate capacity? Also when we look at last 3 quarters, there has not been much topline growth, only bottomline has improved.

Again, one should look at volume, rather than topline. As polyfilms are a crude derivative, prices vary. Spread between RM and finished goods is important. Do understand what is nameplate. Anyways, I have shared whatever little I know of the sector and the company. One can draw their own inferences.

The plan of the mgt is to have a revenue mix that consists majorly of specialty films. For this they plan to backward integrate into producing master-batches and coating chemicals. Co is targeting to have 70% of biz from value-added films in the next 5 years.

margins in Speciality films are almost 3x what you make in base BOPP films.

Inhouse R&D did a successful trial for the production of certain masterbatches and coating chemicals. This will provide - Backward integration (margin expansion) & Sales of these New products (masterbatches & coating chemicals) will start a new business line altogether and will contribute to topline in the coming quarters (Initially 20-25 cr in the 1st year). A new subsidiary has been incorporated and manufacturing will be done at the existing facilities at Aurangabad ( masterbatch plant to be operational in Q1 of FY21 and coating chemical by Q3 end of FY21). Out of ~10k tons capacity for this masterbatch plant in house consumption will be 5-6k tons while rest will be sold to their existing customers.

Size of Masterbatches market ( i guess domestic) is 3500cr

only 10 suppliers worldwide for BOPP Masterbatches

45 cr capex envisaged in 2021 mainly for this purpose ( masterbatch + coating chemicals )

increasing the headcount of R&D staff from 15 to 30 by end of the year.

There is a shift happening to mono-layered films which come from the same polymer family and thus can be easily recyclable. For e.g the packaging used in soaps is paper + film and is not recyclable ( this is as per my understanding called rigid packaging), however as big fmcg moves to flexible packaging ( wherein packaging film is from a single polymer family),there is going to be a steady improvement in demand from converting cos( those like uflex, huhtamaki etc).

Demand and Supply scenario for BOPP

1 new BOPP line by Jindal expected to come ( expect normalized prodn of ~40k MT). Very few capacity additions globally in BOPP ( < 1.5L tons). Global demand is ~8mil MT. There may be a BOPP few lines added by domestic players in the next 2 years

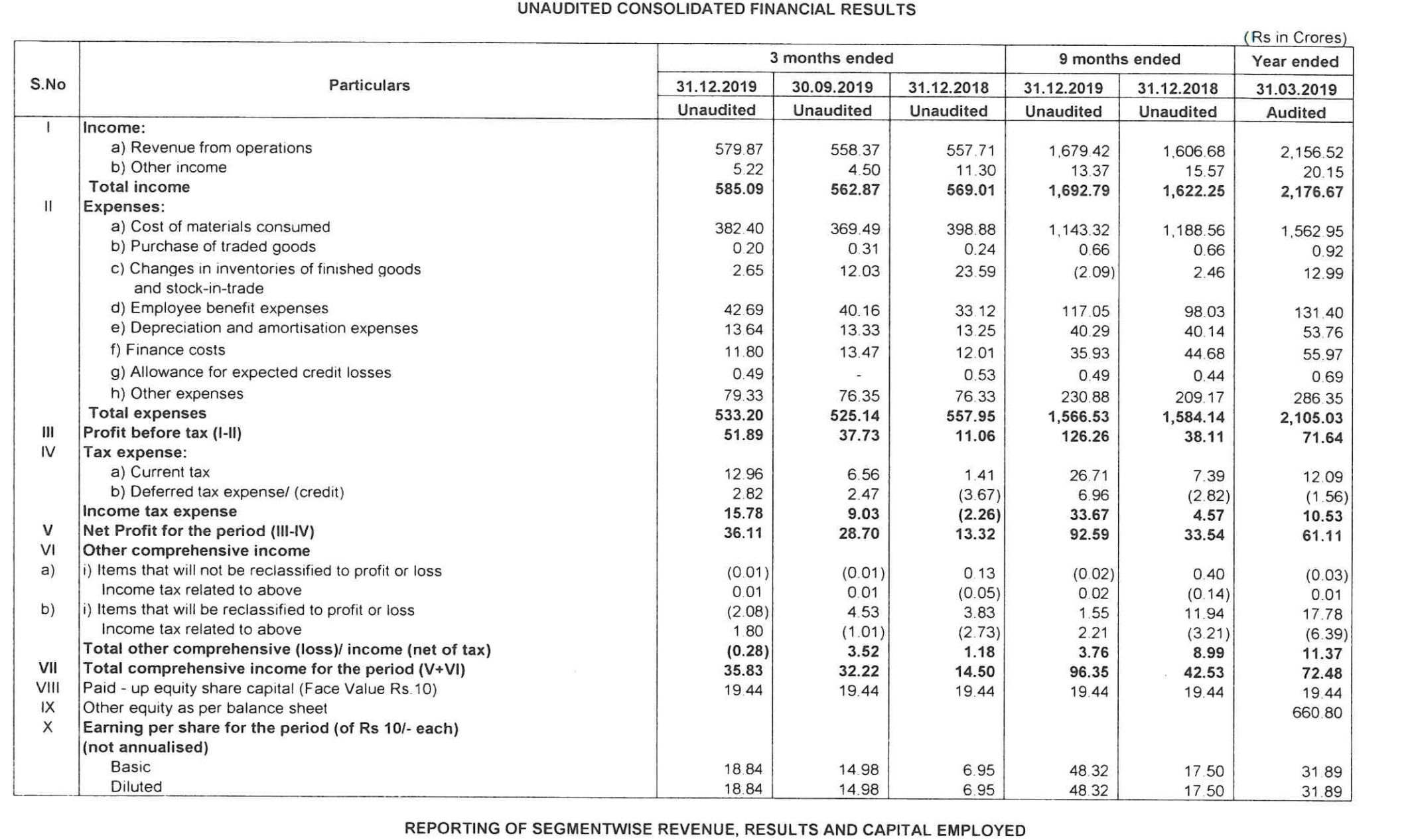

Topline growth of 4% - due to higher mix of value-added films and volume growth.

Running at more than 95% of CU

BOPP spread ~Rs 20 in Dec’19 quarter (Rs 10 last time)

BOPP spread in the last year was one of the lowest in the last decade

Increase in spread due to balanced demand and supply in the domestic market

Rs 20 is the long time normalized spread in BOPP film

8-10 cores R&D spend

15% peak EBITDA margins in last 12 years (for BOPP)

low crude will translate into low working capital requirements

RM prices depend upon oil and conversion of oil to Polypropylene ( which was $1300 last year which has come down to $975 this year) - there has been capacity addn in PP which has bought down PP prices and has had a favourable impact on Cosmo margin profile

Overall, the mgt seemed positive about the move into the higher-margin business lines. These initiatives are in the very early stages and right now remain on paper only. Currently, the co remains very much a commodity business with favourable tailwinds and available at a low single digit PE multiple.

True. Any idea on how much capacity is expected to be added globally over next 1-2 years? Management speaks only about India capacity addition and was not very clear on global capacity addition.

Yes but not sure how much to trust that. As global demand growth is 8 lakh tpa. That will create a big supply gap. So just want to confirm if this number is reliable.

Currently the consensus across the mgt of all major players (Jindal, polyplex , uflex and Cosmo) is that no major capex addn globally or domestic in the next 2 years and margins to sustain. The fear of margin erosion due to capacity addn in the recent past are still fresh. Cosmo and Jindal together control a major chunk of the BOPP capacity domestically and overall BOPP industry is a little more consolidated compared to BOPET. In BOPET there are relatively many players compared to BOPP. So there are differences in the industry structure as well.

You can Google edelweiss film industry report - it has a lot of good quality numbers on the BOPET industry including some on BOPP as well.

What we do know is that BOPP margins have gone up substantially compared to BOPET (both have increased). Industry demand is growing at a steady rate of 5-10% and several players are operating at 80% + CU. Demand will overtake supply in 2-3 years and the cycle will will continue as it has in the past. The long term ROCs in the packaging industry are 10% whether you are a flilm manufacturer or a converter so cyclical downturns are rough when they happen. Logically, a well managed non cyclical co with 10% ROE/ROC should be available at a normalized multiple of 10-12 so from that angle all players in the packaging industry are cheap on the valuation front. Let’s see if Cosmo is able to diversify into chemicals which has better margins.

Can we trust the mgmt commentary? A simple search for BOPP masterbatch does not show it to be a rare process/commodity in India, while Cosmo claims to be only 10 suppliers globally.

The above article explains that “masterbatch” is a technique of pre-processing to allow better printing on the BOPP. It is with Indian context.

I agree that BOPP cycle has turned favourable and that is why I wanted to understand the amount of supply coming in BOPP over next 1-2 years because supply becomes the most important thing to track now going ahead. I have read the edelweiss report and it gave good numbers on BOPET supply coming in but nothing was given on BOPP supply.

And for Cosmo, diversifying into chemicals such that it becomes material is still a long way to go and a little far fetched at the moment. So for now even if they successfully increase their specialty share to 75% over next 3 years as they intend to, that is good enough to increase their base margins and reduce volatility of being a commodity player.