Hi Jiten

Since you seem to be the most knowledgeable on this business, I want to ask you about this or any other expert members who know the answers. This concerns mostly the latter part of this reply.

However, since you’ve also spoken about the management, want to ask what you know about the management too.

I read this year’s ConCall Transcript. The management seems to sound over-optimistic and looks like they’re trying a bit too much or a bit overtly to create a good impression.

(Peter Lynch warns against this and says some industries with pessimistic to moderate expectations are good, while those constantly in hyperbole deserve a sceptic approach to understanding them.)

Is it because the business is good or are they trying to look good and pretty all the time? Some of them are convincing while some are not.

For example, while talking about Direct Thermal Printable Films, these days I refuse to even take the Print receipt from Petrol Bunks.

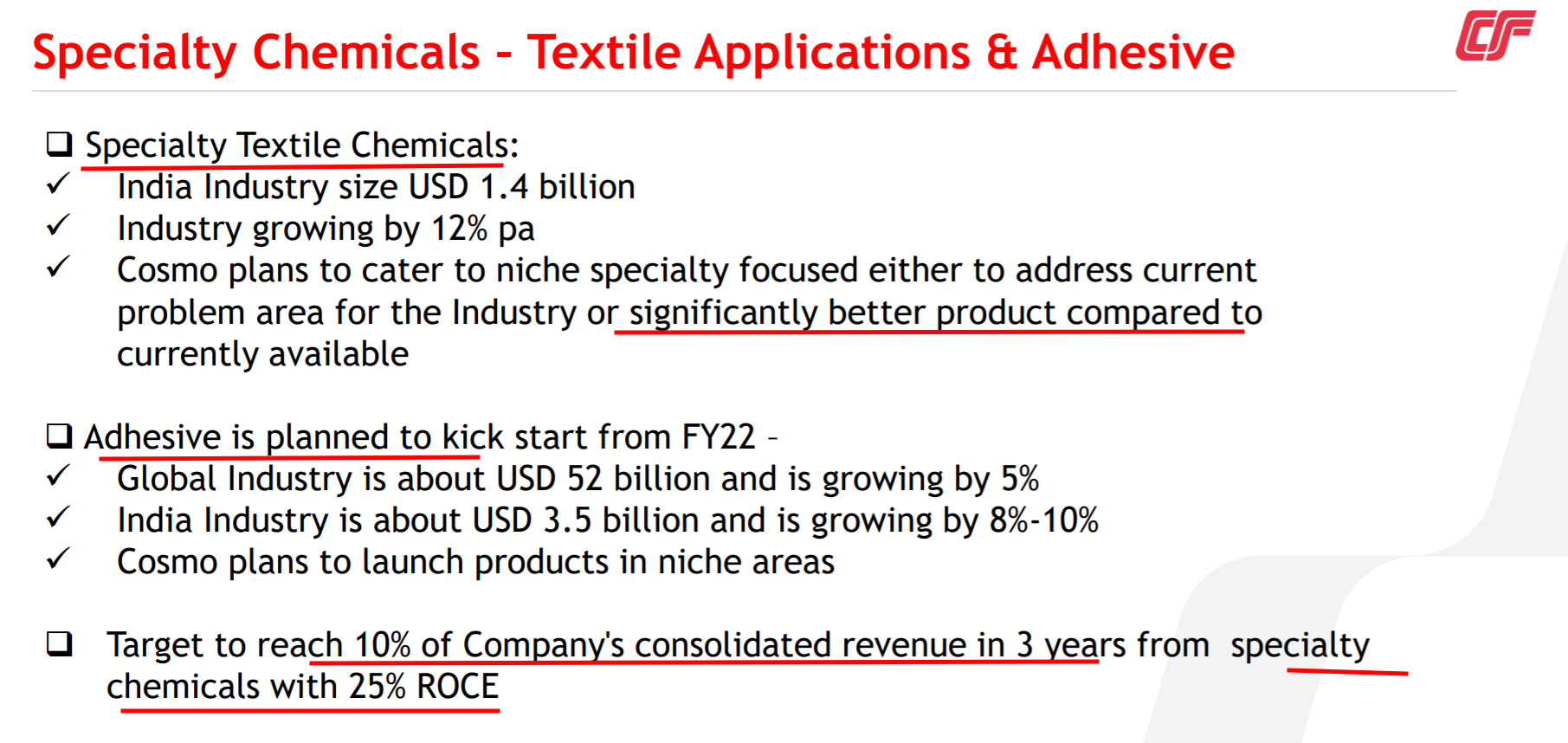

But they’ve invested a lot in R&D of DPT Films to come up with a Printable Film that has a 5 year shelf-life of the print, since currently it fades too soon. (Besides, is this a slow industry or an industry undergoing rapid change?)

Why do I need a 5 year shelf-life, if I’m not even going to take the receipt because I get SMS and statements online?

Are there any other applications of a DPT Film that the company will benefit out of like they said something about use in hospitals, wrap-arounds or used on wrists or something.

Is DPT unique to them? As a Google search turns up only Cosmo Films. Is it important by size in volume, price, revenue and margins? Or is it something insignificant to be ignored?

If it’s their own finding out of their R&D, should any of us ask if they have any patents in the next ConCall? Is a patent required for this or any other offering of theirs, if they’re from their own labs?

I’m way too ignorant of this field and I think this is the only company currently with good numbers.

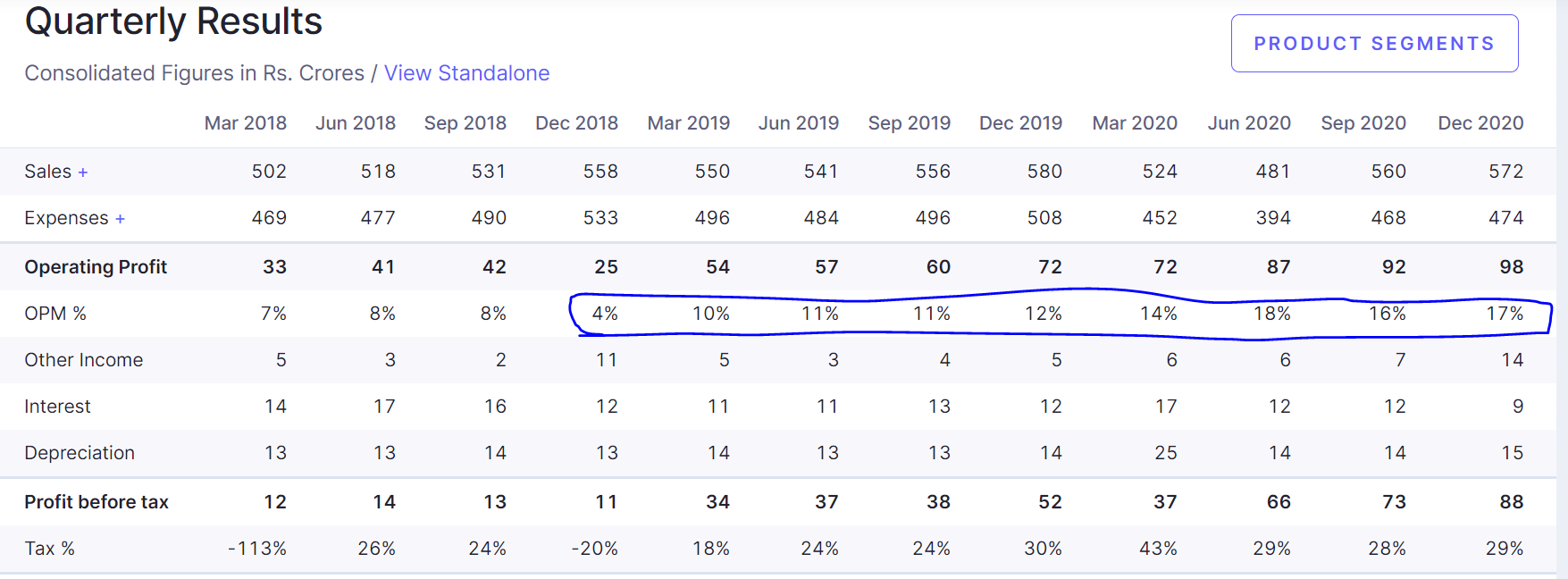

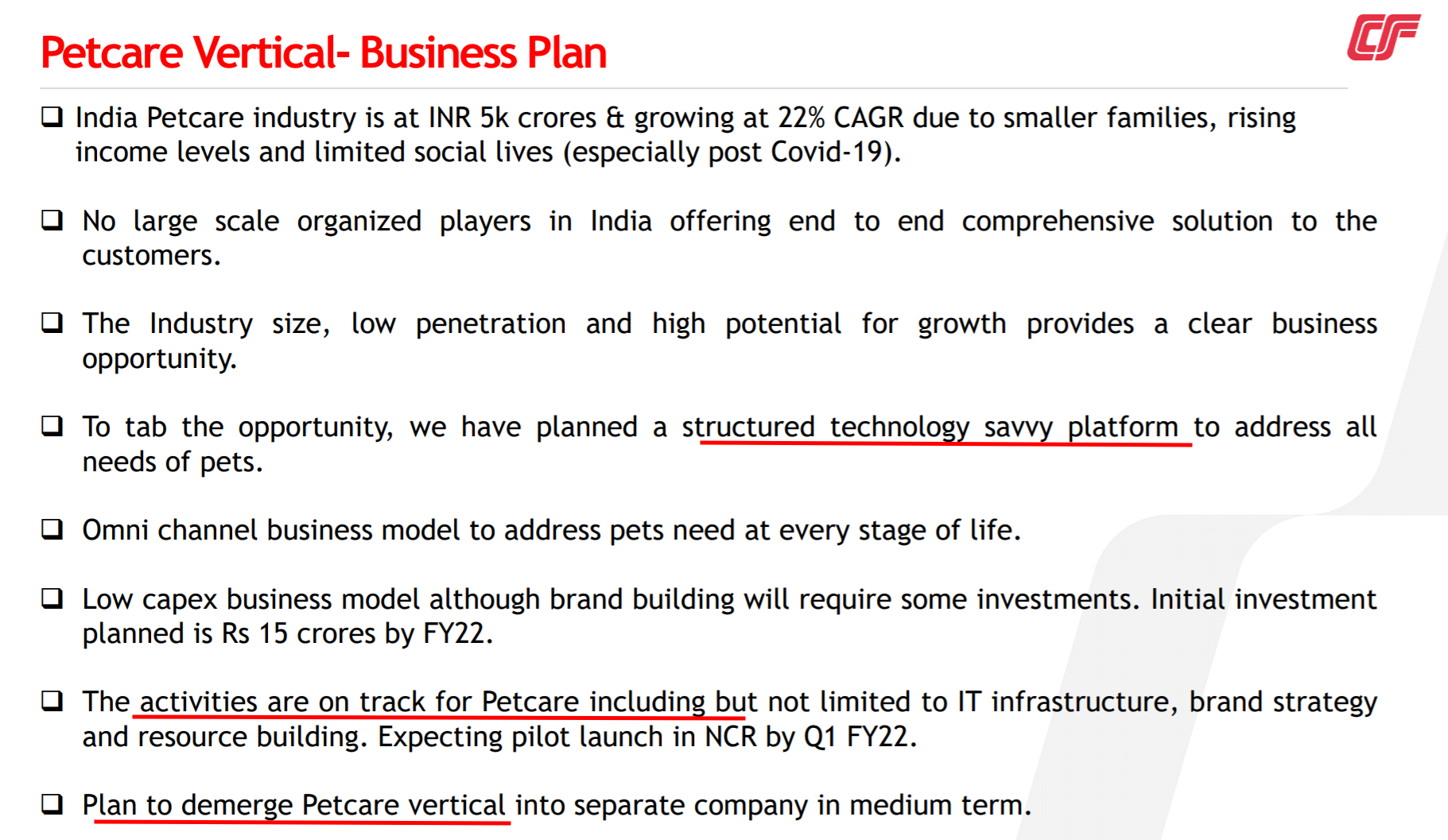

Do you also think their good numbers are a concern too due to the cyclical nature of their business? There seems to be some tailwinds for their business for the next couple of years at least. Doesn’t it?

Please let me know your thoughts on these aspects of this company, when you can. Thanks In Advance

Regards

Dinesh