Brief Description

Coromandel International Limited is engaged in the manufacture and trading of farm inputs consisting of fertilizers, crop protection, specialty nutrients and organic compost. The Company’s business divisions include Fertilizers, Specialty Nutrients, Crop Protection and Retail. It offers various products in fertilizer segment, including Nitrogen, Phosphatic and Potassic in various grades. Its specialty nutrients consist of water-soluble fertilizer, sulfur products, micronutrients and organic manure. Its crop protection products consist of insecticides, fungicides, and herbicides. Its retail outlets operate as Mana Gromor Centers. It manufactures a range of fertilizers and markets over 3.2 million tons. It operates a network of over 800 rural retail outlets under its retail business across Andhra Pradesh, Telangana, and Karnataka. It has manufacturing facilities in Andhra Pradesh, Tamil Nadu, Karnataka, Maharashtra, Madhya Pradesh, Uttar Pradesh, Rajasthan, Gujarat, and Jammu and Kashmir.

Sector Overview.

UPA Govt introduced Nutrient-based Subsidy Scheme( NBS ) in 2010. It was meant to reduce subsidy burden on the government. While it did not achieve the desired results, it created more problems especially its impact on farming practices and soil health. The immediate outcome of this was a sharp decline in the use of phosphoric and potassic fertilizer mix, with an increase in urea consumption. There is a prescribed usage ratio of fertilizers. Ideally, the NPK usage ratio should be 4:2:1. For the year 2013-14, NPK ratio in Punjab was 61.7:19.2:1; in Haryana, it was 61.4:18.7:1; in Rajasthan, it was 44.9:16.5:1; and in Uttar Pradesh, it was 25.2:8.8:1.

Now the government has decided to fix this issue through Direct Benefit Transfer(DBT) along with soil health cards. Direct Benefit Transfer (DBT) in fertilizers was introduced on a pilot basis, with pan India rollout likely to follow in 2018. DBT has the potential to overcome the distortion of NPK usage as the farmers will now have the choice in deciding the usage. Besides the fertilizer industry has been suffering due to the increasing receivables due to govt subsidy policies. DBT will also address this issue and benefit the companies in this industry. The 2016 Economic Survey estimated that only 35% of the subsidy reached intended beneficiaries, and as much as 41% of urea was redirected to industry or smuggled out of the country. Nearly half the farmers bought urea at above MRP in the black market. DBT will incentivize the industry to create more supply.

Also, the government is hell-bent to reduce the imports of all kinds of fertilizers especially Urea. Source

Company Overview

Coromandel belongs to murugappa group. So it has a very decent management, which is evident from its operating efficiency of previous years. In an industry which is suffering from govt policies, coromandel stands out. Its ROE and ROCE are well above the industry average. This was possible due to its product mix and continually tried to increase revenues from non subsidized fertilizers. In addition, the Company also holds 14% equity stake in Foskor Pty Limited, South Africa, through combined holding of Coromandel and CFLMauritius Limited and a 15% equity stake in TIFERT, a strategic investment of the Company to secure supply of Phosphoric acid which is the raw material for its fertilizer business. Due to this Coromandel is the lowest cost producer of Phospharic fertilizers.

Its also investing into crop protection chemicals and farm mechanization. Its 800 plus GRoMor stores will nicely complement these new ventures.

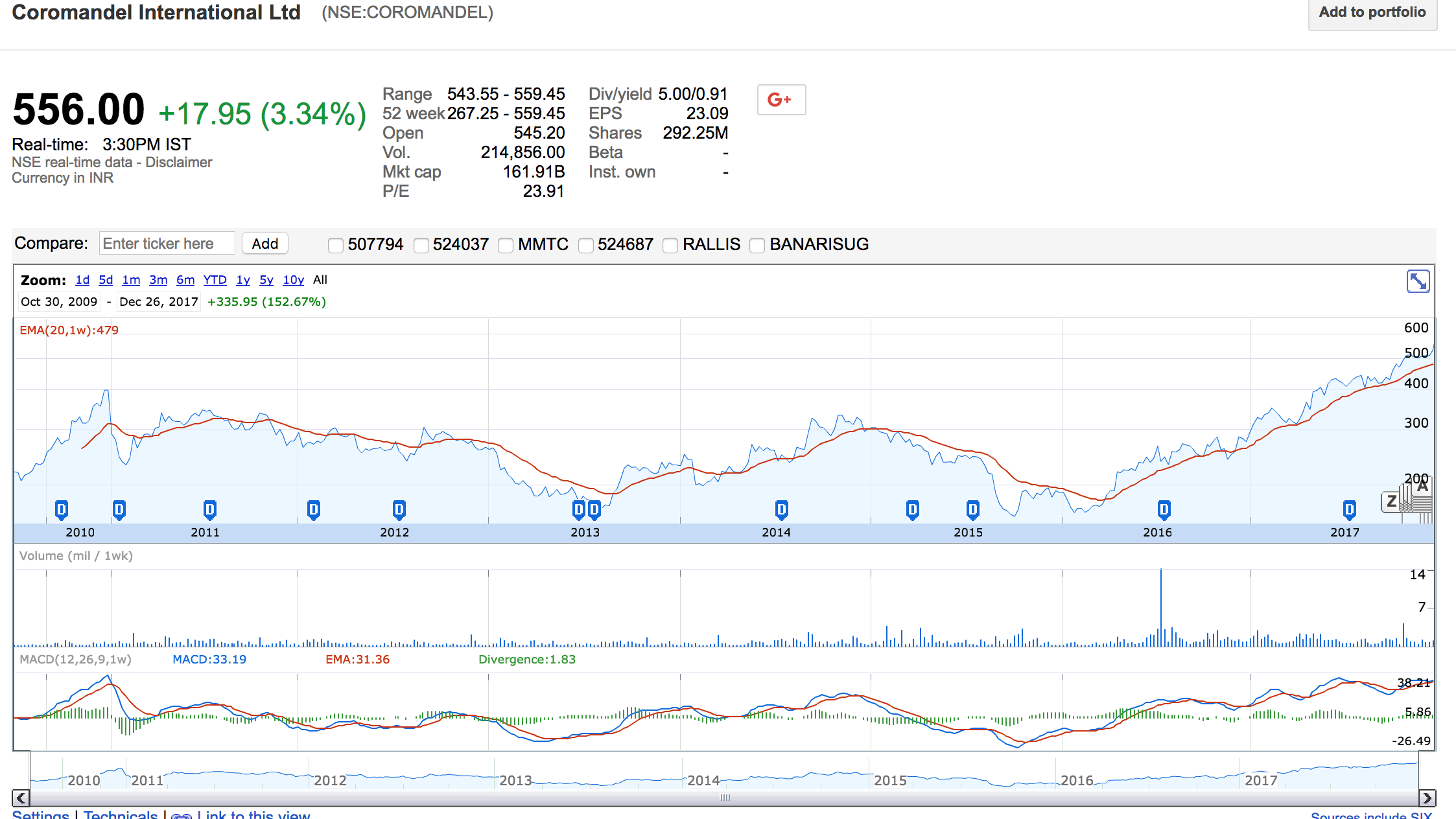

Its evident from the below graph that the stock almost traded sideways for the last seven years and looks like a strong uptrend has started.

Major risks include

- Govt not able to implement the planned reforms.

- problems in its subsidiaries especially the ones which are in tunisia, south africa from where it sources its raw materials.

Disclosure: Invested 10 % capital at 500 levels.